uk energy policy - amazon simple storage service · ©2012 energy technologies institute llp -...

TRANSCRIPT

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 1

©2012 Energy Technologies Institute LLP The information in this document is the property of Energy Technologies Institute LLP and may not be copied or communicated to a third party, or used for any purpose other than that for which it is supplied without the express written consent of Energy Technologies Institute LLP. This information is given in good faith based upon the latest information available to Energy Technologies Institute LLP, no warranty or representation is given concerning such information, which must not be taken as establishing any contractual or other commitment binding upon Energy Technologies Institute LLP or any of its subsidiary or associated companies.

UK energy policy – Can it deliver? Will it deliver?

David Clarke Chief Executive ETI 2012 Bridge lecture

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 2

UK energy policy has a long history...

• Professor Peter Pearson Low Carbon Research Institute of Wales Cardiff University

• Professor Jim Watson Sussex Energy Group University of Sussex

• Available on the IET website

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 3

©2012 Energy Technologies Institute LLP The information in this document is the property of Energy Technologies Institute LLP and may not be copied or communicated to a third party, or used for any purpose other than that for which it is supplied without the express written consent of Energy Technologies Institute LLP. This information is given in good faith based upon the latest information available to Energy Technologies Institute LLP, no warranty or representation is given concerning such information, which must not be taken as establishing any contractual or other commitment binding upon Energy Technologies Institute LLP or any of its subsidiary or associated companies.

System level strategic planning Technology development and demonstration

Informs effective decision making Underpins national energy systems policy Develops capacity, technology and engineering Increases investor confidence

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 4

Making energy policy work for the UK

Energy power, heat, transport, infrastructure

Wealth creation gross value added, direct employment, secondary jobs and impacts, exports, inward investment

Capacity Skills, training, infrastructure, science, R+D

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 5

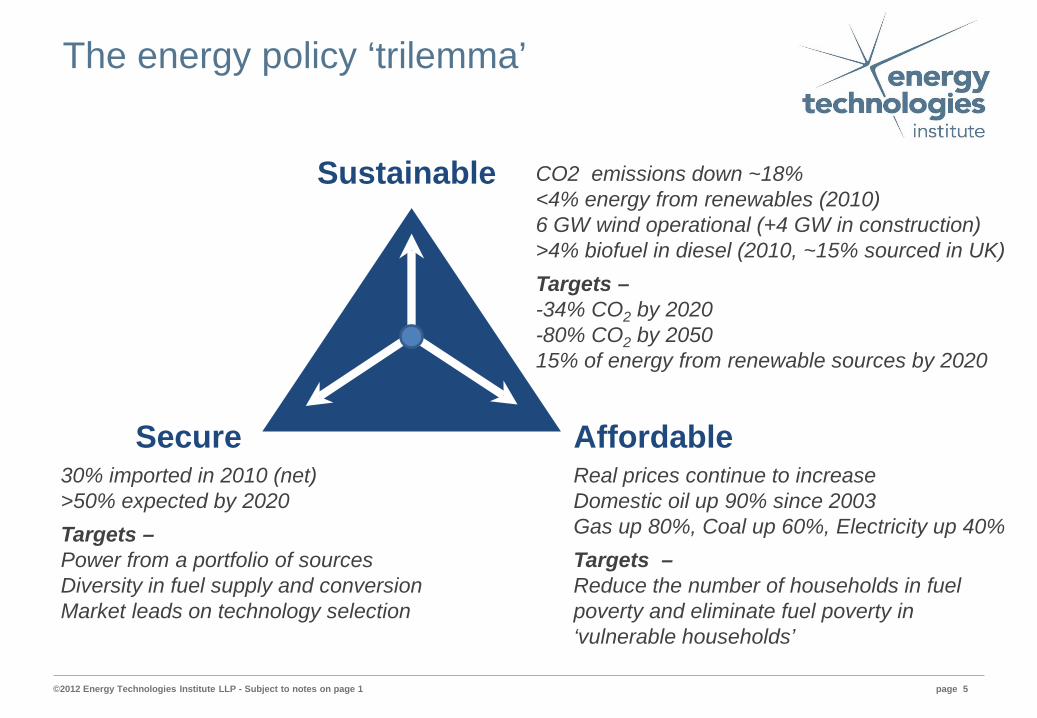

The energy policy ‘trilemma’

Sustainable

Secure Affordable

CO2 emissions down ~18% <4% energy from renewables (2010) 6 GW wind operational (+4 GW in construction) >4% biofuel in diesel (2010, ~15% sourced in UK) Targets – -34% CO2 by 2020 -80% CO2 by 2050 15% of energy from renewable sources by 2020

30% imported in 2010 (net) >50% expected by 2020 Targets – Power from a portfolio of sources Diversity in fuel supply and conversion Market leads on technology selection

Real prices continue to increase Domestic oil up 90% since 2003 Gas up 80%, Coal up 60%, Electricity up 40% Targets – Reduce the number of households in fuel poverty and eliminate fuel poverty in ‘vulnerable households’

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 6

Scale of the UK challenge...

• 62m people ....................................................... growing to 77m by 2050

• 24m cars .......................................................... growing to 40m by 2050

• Over 380 ‘significant’ power stations ................. many in remote locations

• Over 85GW generation capacity ....................... from 1MW to 3.8GW

• 24m domestic dwellings .................................... 80% will still be in use in 2050 total dwellings 38m by 2050

• Final users spent £124bn on energy in 2010 .... 9% of GDP

• 5.5m households in fuel poverty ........................ 70% are ‘vulnerable households’

• Energy consumption rising at >3% / year

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 7

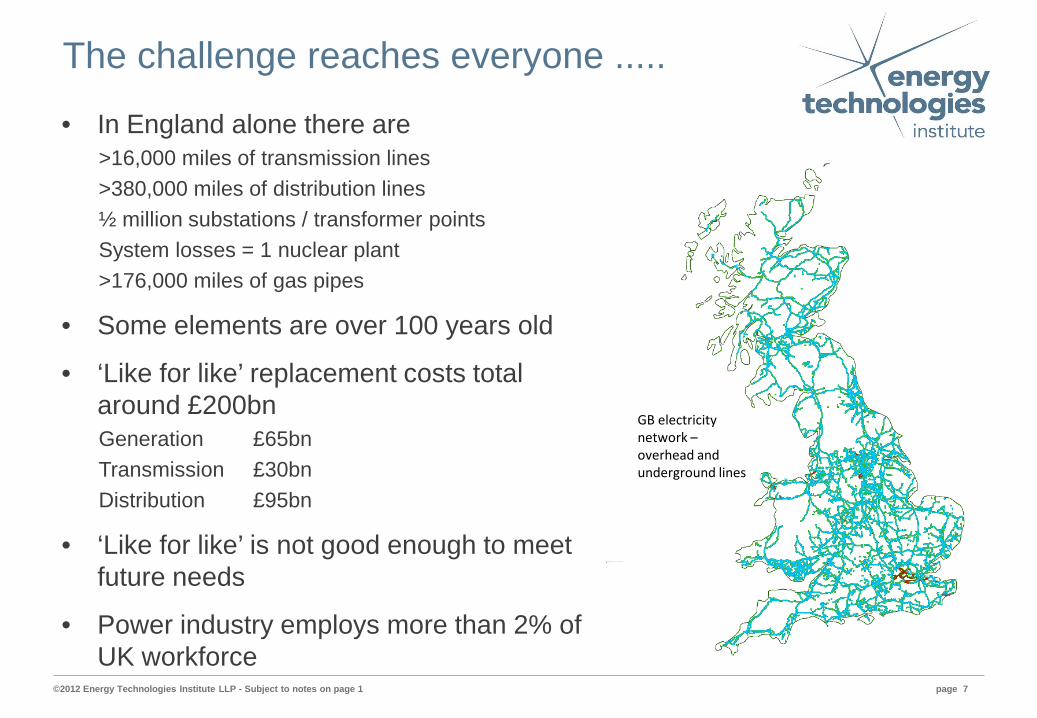

The challenge reaches everyone .....

• In England alone there are >16,000 miles of transmission lines >380,000 miles of distribution lines ½ million substations / transformer points System losses = 1 nuclear plant >176,000 miles of gas pipes

• Some elements are over 100 years old

• ‘Like for like’ replacement costs total around £200bn Generation £65bn Transmission £30bn Distribution £95bn

• ‘Like for like’ is not good enough to meet future needs

• Power industry employs more than 2% of UK workforce

GB electricity network – overhead and underground lines

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 8

What might the UK energy system look like in 2050...

• Decided by global developments – not just UK events, decisions and policy

– UK and global economy

– Industry and technology developments

– UK demand changes – scale and segmentation

– Global socio-political events

– International market confidence

– ..........

• The future is uncertain and we need an energy system design that allows for this

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 9

A national energy system design tool Integrating power, heat, transport and infrastructure

searching for the lowest cost solution

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 10

ESME is used to inform decisions and answer questions... • What might be ‘no regret’ technology choices and pathways to 2050?

• What is the total system cost of meeting the energy targets?

• What are the opportunity costs of individual technologies?

• What are the key constraints e.g resources, supply constraints?

• How might uncertainty in resource prices and availability influence technology choices?

• Where should new generating capacity optimally be located?

• How might accelerating the development of a technology impact the solution?

• How might policies and consumer choices influence technology development?

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 11

Typical ESME Outputs

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 12

Getting to 2050 .... UK primary energy diversifies Nuclear and gas are pillars - 50% of energy imported

• Increasing role for nuclear and renewables

• Fossil fuel persists with CCS in power and as gas in heavy vehicles

• Biomass, onshore wind, hydro and imported biofuels become fully exploited

• Wet wastes must be used effectively – includes conversion to biogas

• Increased range and number of key assets

Primary Energy Mix (Mean)

Electricity 2010 = 365TWh, 2050 = 440TWh

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 13

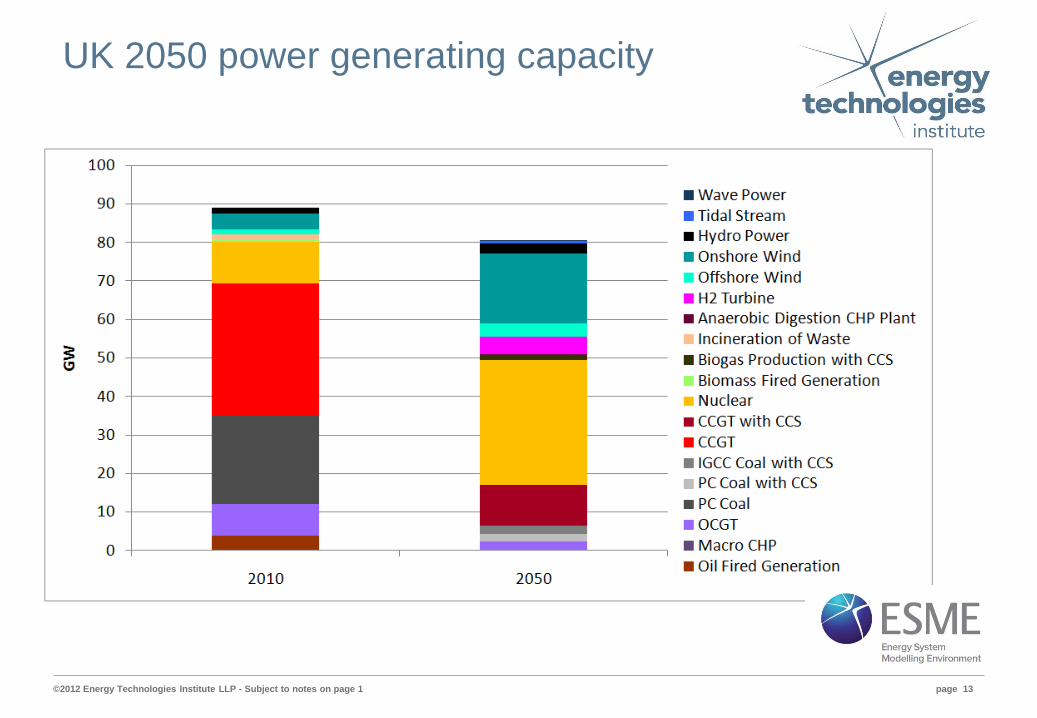

UK 2050 power generating capacity

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 14

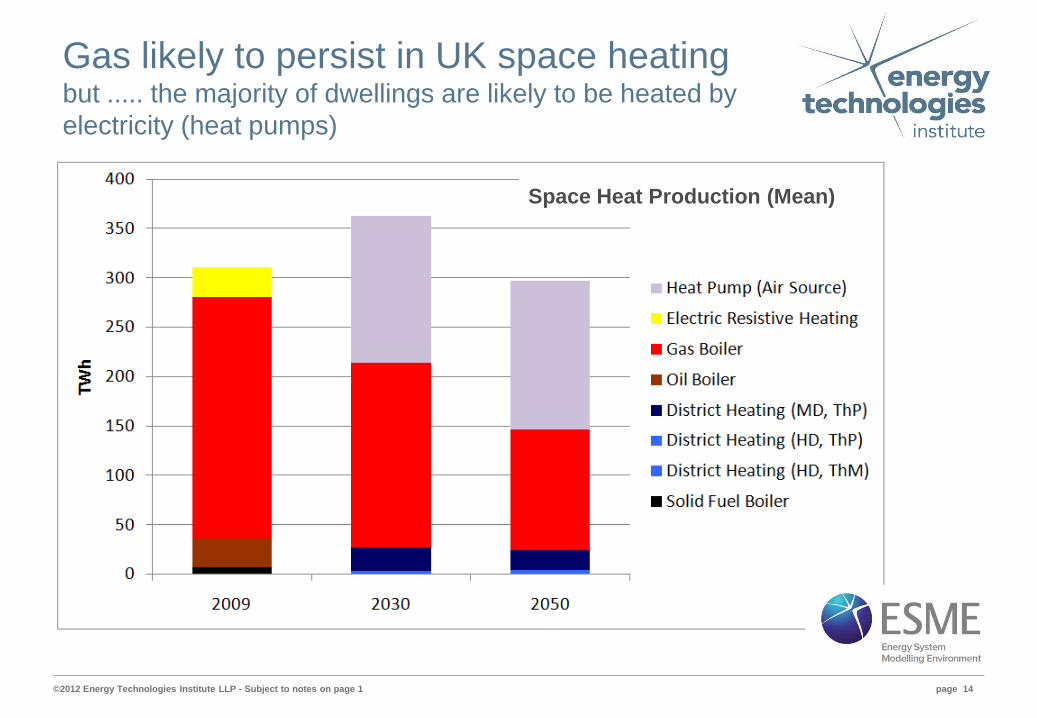

Gas likely to persist in UK space heating but ..... the majority of dwellings are likely to be heated by electricity (heat pumps)

Space Heat Production (Mean)

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 15

Why is gas so valuable for heat ? UK system has to cope with 6x heat demand swing

Data source: UKERC (2011)

Hea

t / E

lect

ricity

(G

W)

0

50

100

150

250

200

Jan 10 Apr 10 July 10 Oct 10

HeatElectricity

Design point for a GB heat delivery system

Design point for a GB electricity delivery system

GB 2010 heat and electricity hourly demand variability - commercial & domestic

Heat demand

Electricity demand

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 16

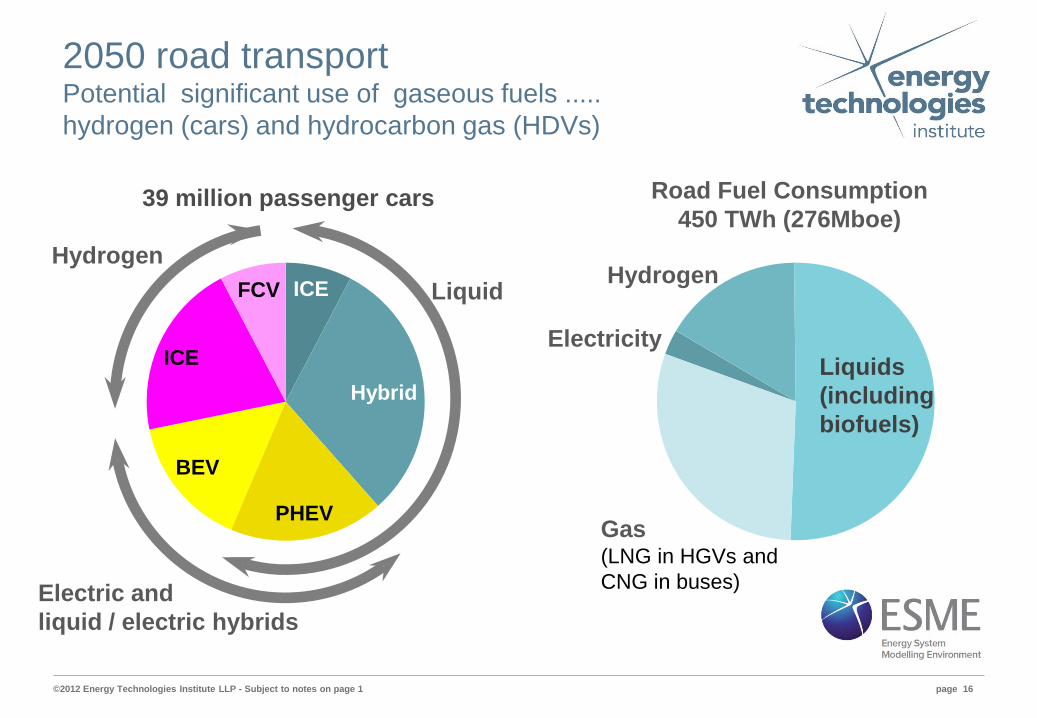

2050 road transport Potential significant use of gaseous fuels ..... hydrogen (cars) and hydrocarbon gas (HDVs)

ICE

Hybrid

PHEV

BEV

ICE

FCV

39 million passenger cars

Liquid

Electric and liquid / electric hybrids

Hydrogen

Road Fuel Consumption 450 TWh (276Mboe)

Gas (LNG in HGVs and CNG in buses)

Hydrogen

Liquids (including biofuels)

Electricity

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 17

Geographic factors are critical in optimising system cost

Statfjord

Brent

Forties

Morecambe

Indefatigable

Leman

Bunter Domes

35

21

9

• Population • Weather / climate • Resources • Power generation • CO2 storage • Transport needs • Energy storage • ...

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 18

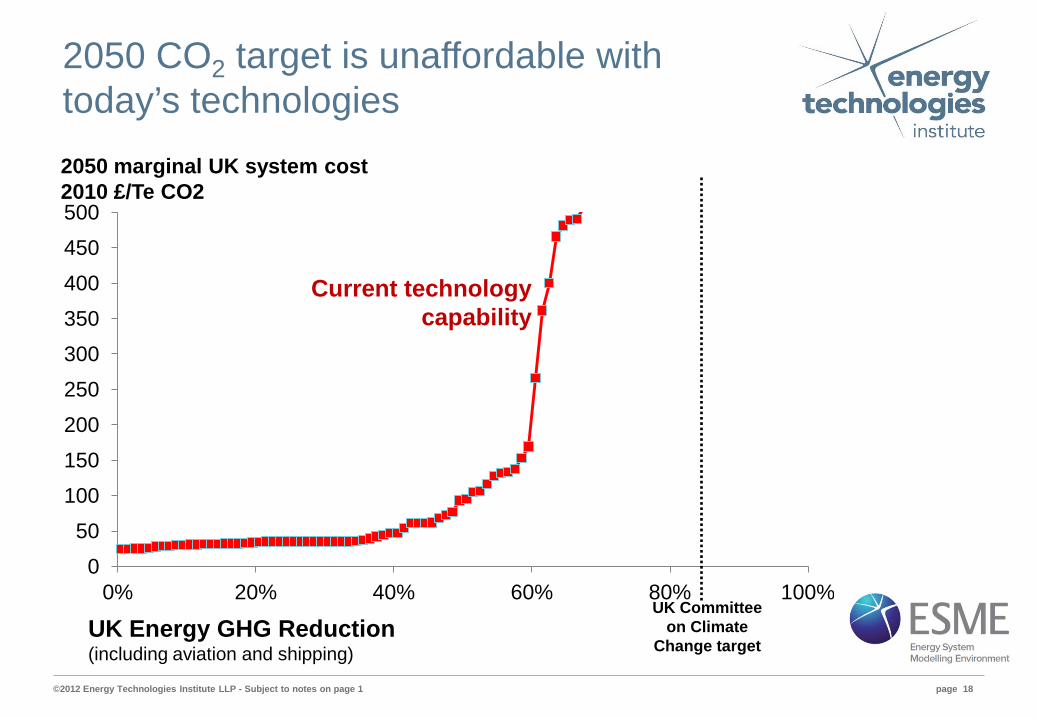

2050 CO2 target is unaffordable with today’s technologies

0

50

100

150

200

250

300

350

400

450

500

0% 20% 40% 60% 80% 100% UK Committee

on Climate Change target

Current technology capability

UK Energy GHG Reduction (including aviation and shipping)

2050 marginal UK system cost 2010 £/Te CO2

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 19

ETI projects focus on reducing these levels

further

Successful technology selection, innovation and

development

2050 abatement costs can be acceptable if ... we develop and apply the optimum technologies

0

50

100

150

200

250

300

350

400

450

500

0% 20% 40% 60% 80% 100% UK Committee

on Climate Change target

Current technology capability

Expected improvement in technology capability

UK Energy GHG Reduction (including aviation and shipping)

2050 marginal UK system cost 2010 £/Te CO2

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 20

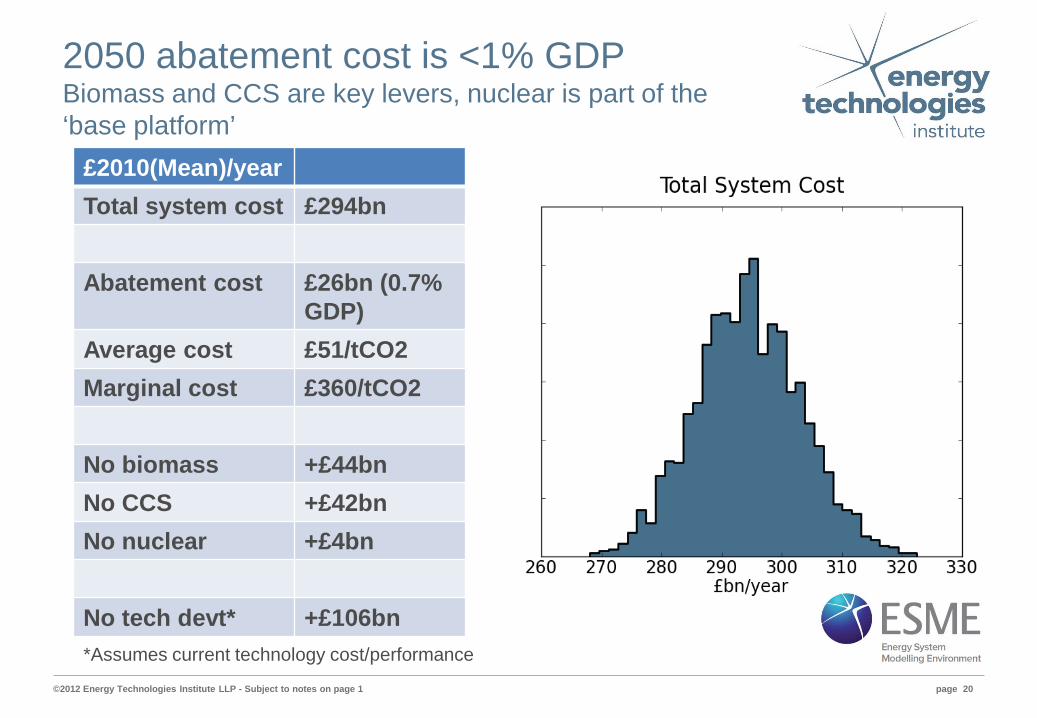

2050 abatement cost is <1% GDP Biomass and CCS are key levers, nuclear is part of the ‘base platform’

£2010(Mean)/year Total system cost £294bn

Abatement cost £26bn (0.7% GDP)

Average cost £51/tCO2 Marginal cost £360/tCO2

No biomass +£44bn No CCS +£42bn No nuclear +£4bn

No tech devt* +£106bn *Assumes current technology cost/performance

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 21

• Focus on the ‘big levers’ is crucial to maximise impact of scare resources - money, skills, supply-base and time

• Investment in innovation is critical to reduce costs

• Engagement of industry and consumers is essential

• ETI view immediate development priorities for 2050 as ... – Efficiency (technology, consumer demand, storage) – Nuclear – CCS – Bioenergy – Offshore wind – Gas for transport

Effective national policy needs to focus on things which will ‘move the dial’

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 22

Efficiency All future emission reduction scenarios utilise efficiency improvements

• Waste heat recovery • Building insulation • Efficient vehicles • Energy systems management

• ETI targeting through system demonstration and technology development projects – ‘Smart systems’ £95m+

– Marine and Land Heavy Duty Vehicle efficiency £30m+

• Plus, ongoing ETI projects in building refurbishment , energy management systems and energy storage

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 23

Nuclear Supply chain development and early deployment is critical in realising the optimal 2050 UK energy system design

• Broadly a mature technology

• Appears economic under most emission reduction scenarios

• Primarily an issue of deployment – Planning – Licensing – Supply-chain development – Finance support

• Cost impacts post-Fukushima need clarification – international approach needed

• ETI supported recent development of R+D roadmap for the industry

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 24

CCS A key lever - particularly combined with bioenergy Long development time requires early start • Potentially very wide use

– Power – Hydrogen and ‘Synthetic

Natural Gas’ (SNG) production

– Heavy industry

• ETI investing over £60m in enabling CCS for coal, gas and biomass – Improved separation

technologies – Storage appraisal – Transport system design

tools

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 25

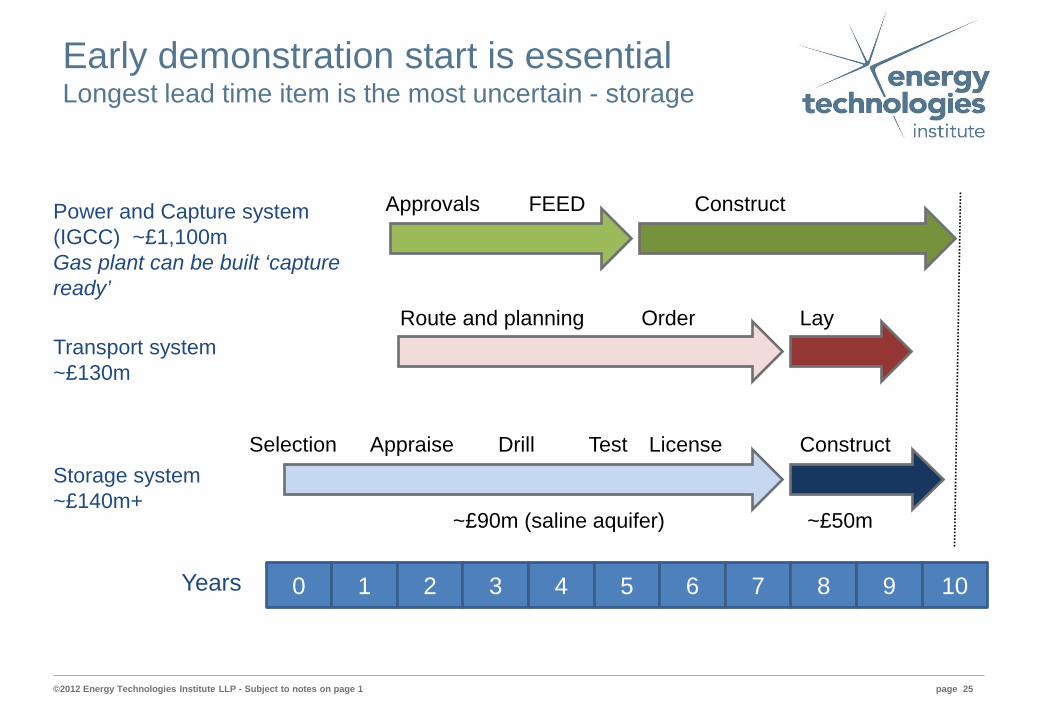

Early demonstration start is essential Longest lead time item is the most uncertain - storage

0 1 2 3 4 5 6 7 8 9 10

Power and Capture system (IGCC) ~£1,100m Gas plant can be built ‘capture ready’

Years

Storage system ~£140m+

Transport system ~£130m

Selection Appraise Drill Test License Construct

Route and planning Order Lay

Construct FEED Approvals

~£90m (saline aquifer) ~£50m

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 26

Bioenergy A key lever – particularly with CCS Requires sustainable supplies – imports and indigenous

• Major potential for creating ‘negative emissions’ via CCS

• Could support a range of conversion and utilisation routes – Hydrogen – SNG – Heat

• ETI investing in soil science, logistics and value chain models

• Informing decisions – “what do we grow ?” – “where do we grow it ?” – “how do we handle it ?”

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 27

Offshore Wind The marginal power technology and an important hedging option – cost reduction is critical

• DECC cost reduction task force identifying routes to achieving 10p/ KWh by 2020

– Contract and project structures – Financing and risk management – Technology innovation

• ETI has already invested £40m in technology development projects

• Another £30m of projects in contracting - next generation, low cost, deepwater platform and turbine technology demonstrations

• ETI Targeting 8.5p/KWh post 2020

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 28

Gas Likely to replace heavier fossils in ‘hard to electrify’ and backup applications

• Fossil gas likely to remain cost effective and widely available

• Low CO2 emissions vs heavier liquid fossil fuels likely to lead to gas replacing diesel in HDVs

– Technology already available – Energy density supports long-distance vehicle

applications

• Hydrogen from fossil fuels could become an increasingly important energy vector

– Creates system flexibility (with CCS and storage) – Light vehicle transport applications

• ETI already investing in enhanced control and safety systems for powerplants using hydrogen rich fuels

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 29

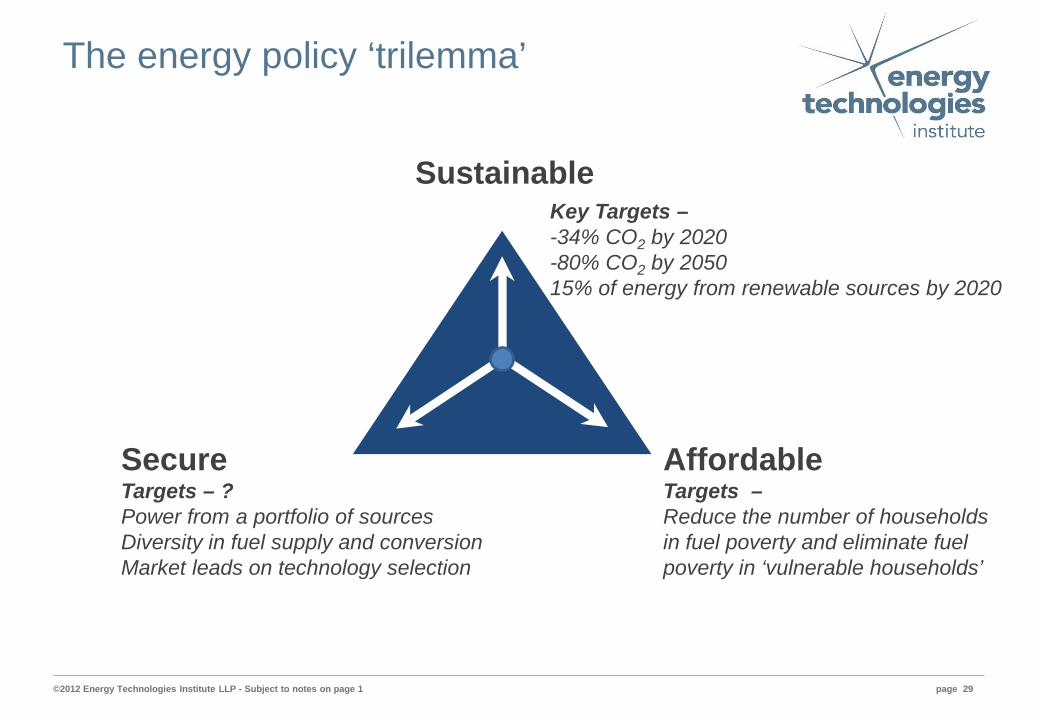

The energy policy ‘trilemma’

Sustainable

Secure Targets – ? Power from a portfolio of sources Diversity in fuel supply and conversion Market leads on technology selection

Affordable Targets – Reduce the number of households in fuel poverty and eliminate fuel poverty in ‘vulnerable households’

Key Targets – -34% CO2 by 2020 -80% CO2 by 2050 15% of energy from renewable sources by 2020

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 30

UK energy policy Can it deliver ? • 2020 / 2050 CO2 targets are viewed as increasingly challenging in today’s

economy

• Demand reduction (efficiency) is key to ensuring progress

• UK policy focus is on measures to engage industry and consumers – Planning reforms – ‘Green Deal’ for efficiency – Electricity Market Reform – contracts for difference, capacity payments, FITS/ROCS,

Emissions Performance Standard, .... – Carbon Price Floor

• Being driven by increasingly urgent regulation and standards – Building regulations changes – Smart meter roll-out – ...

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 31

UK energy policy Will it deliver ?

• The assured availability of affordable, sustainable energy is a critical element in delivering long-term economic development and growth

• UK policy will deliver a system that combines these 3 elements but ...

– Will it meet the targets ? – Will it be the optimum solution ?

• Success will need industry and finance to be persuaded to invest in .....

– widespread innovation – major, long-term infrastructure developments

(in an uncertain market)

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 32

UK energy policy Will it deliver ?

• Virtually all the technology elements in the UK energy system will need to be replaced over the next 40 years

– Power, Heat, Transport, Infrastructure

• 2050 CO2 target is unaffordable with today’s technologies

• 2050 CO2 abatement costs can be acceptable if we prioritise, develop and apply the optimum technologies

• Informed, robust decisions are critical

• Early demonstration of cost effective options for national priorities is critical

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 33

Potential implications for the UK ......

Efficiency measures waste heat recovery, building insulation, and efficient vehicles make a contribution under all emission reduction scenarios ETI targeting through ‘Smart’ (including vehicle electrification infrastructure and HDV projects)

Nuclear mature technology and appears economic under most emission reduction scenarios - primarily an issue of deployment (planning / licensing, supply-chain, finance etc) Cost impacts post-Fukushima need clarification – international approach needed

Bioenergy major potential for negative emissions via CCS and might include a range of conversion routes – H2, SNG, process heat ETI investing in science, logistics and value models

Offshore Wind the marginal power technology and an important hedging option ETI developing over £30m of investments in next generation, low cost, deepwater platform and turbine technology demonstrations

CCS A key technology lever given potential wide application in power, hydrogen and SNG (gas) production, and in industry sector ETI investing in separation, storage and system design – for coal, gas and biomass

Natural gas potentially a material role as a 2050 destination fuel including power, space heating, transport and process heat applications

Hydrogen increasingly important energy vector providing system flexibility (CCS and storage) and light vehicle transport applications

Abatement costs UK 2050 target appears affordable with intelligent energy system design and investment in technology development

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 34

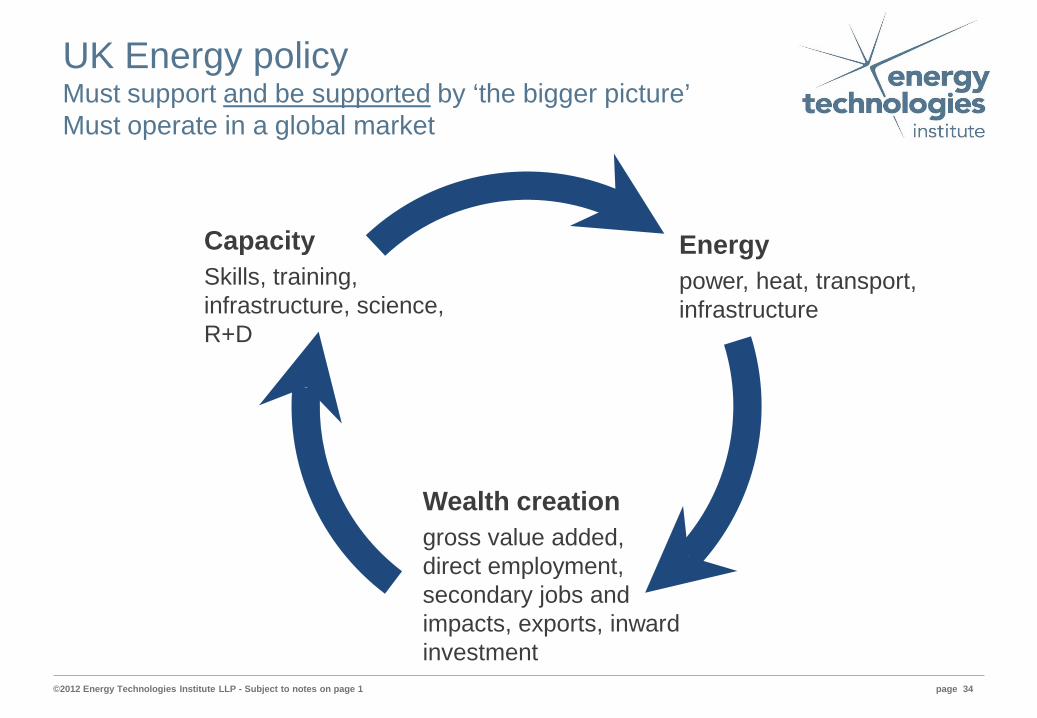

UK Energy policy Must support and be supported by ‘the bigger picture’ Must operate in a global market

Energy power, heat, transport, infrastructure

Capacity Skills, training, infrastructure, science, R+D

Wealth creation gross value added, direct employment, secondary jobs and impacts, exports, inward investment

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 35

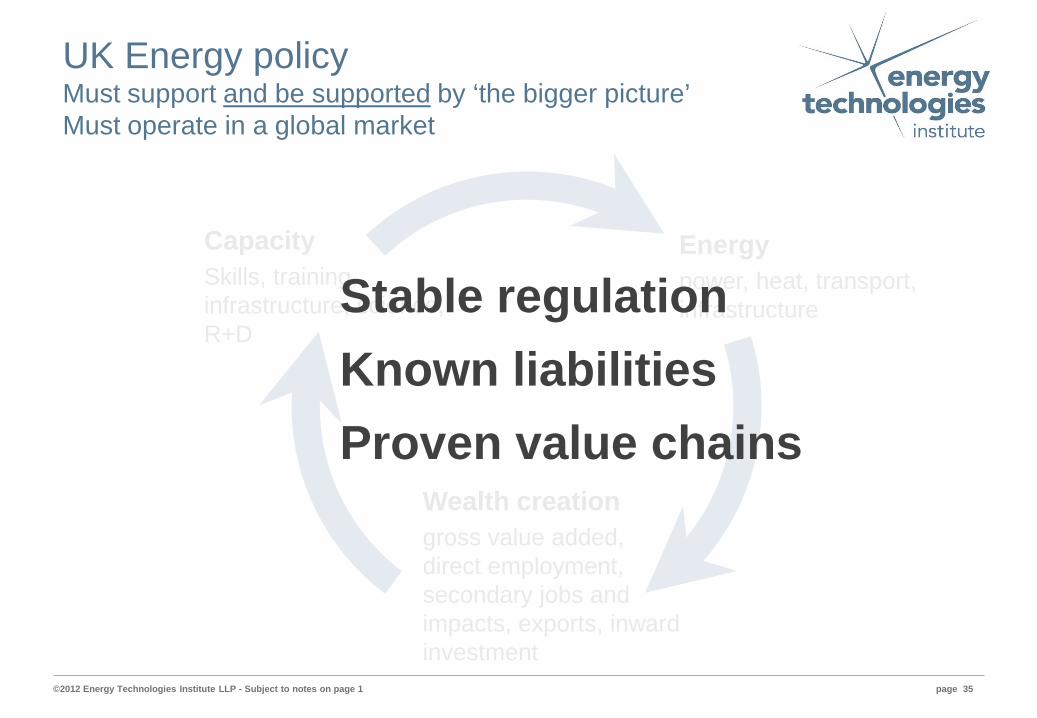

UK Energy policy Must support and be supported by ‘the bigger picture’ Must operate in a global market

Energy power, heat, transport, infrastructure

Capacity Skills, training, infrastructure, science, R+D

Wealth creation gross value added, direct employment, secondary jobs and impacts, exports, inward investment

Stable regulation Known liabilities Proven value chains

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 36

©2012 Energy Technologies Institute LLP The information in this document is the property of Energy Technologies Institute LLP and may not be copied or communicated to a third party, or used for any purpose other than that for which it is supplied without the express written consent of Energy Technologies Institute LLP. This information is given in good faith based upon the latest information available to Energy Technologies Institute LLP, no warranty or representation is given concerning such information, which must not be taken as establishing any contractual or other commitment binding upon Energy Technologies Institute LLP or any of its subsidiary or associated companies.

Delivering low carbon energy technologies Supporting economic growth

www.eti.co.uk

by... Informing policy Building partnerships Delivering innovation Sharing risk Creating affordability

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 37

Addressing the challenges of climate change and low carbon energy Improving energy usage,

efficiency, supply and generation

Demonstrating systems and technologies

Developing knowledge, skills and supply-chains

Informing development of policy, regulation and standards

Enabling deployment of affordable, secure, low carbon energy systems

Energy Technologies Institute (ETI)

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 38

©2012 Energy Technologies Institute LLP The information in this document is the property of Energy Technologies Institute LLP and may not be copied or communicated to a third party, or used for any purpose other than that for which it is supplied without the express written consent of Energy Technologies Institute LLP. This information is given in good faith based upon the latest information available to Energy Technologies Institute LLP, no warranty or representation is given concerning such information, which must not be taken as establishing any contractual or other commitment binding upon Energy Technologies Institute LLP or any of its subsidiary or associated companies.

Reducing risk and enabling…

Large-scale deployment through development with major industries

Innovation and pull-through with smaller enterprises and academia

Informed decisions on sustained, targeted development of regulatory frameworks, skills, supply-base and infrastructure

©2012 Energy Technologies Institute LLP - Subject to notes on page 1 page 39

For more information about the ETI visit www.eti.co.uk

For the latest ETI news and announcements email [email protected]

The ETI can also be followed on Twitter at twitter.com/the_ETI

Energy Technologies Institute Holywell Building Holywell Park Loughborough UK LE11 3UZ

For all general enquiries telephone the ETI on +44 (0)1509 202020.