venezuela · databases and as direct feeds to corporate intranets. for further information, please...

TRANSCRIPT

COUNTRY REPORT

Venezuela

September 2001

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

Venezuela at a glance: 2001-02OVERVIEWIndustrial relations are set to remain fractious ahead of the elections for newunion authorities, in which the pro-government union, the FBT, will nowcompete. Attempts by the FBT to build a parallel organisation failed, leadingthe union to compete for control of union politics from within theopposition-controlled CTV. President Hugo Chávez will remain popular, buthe is vulnerable on the issues of rising crime and the unemployment rate.Weakening oil revenue will not only hit the fiscal accounts but also theexternal accounts, where last year's surpluses are set to shrink. Theeconomy should grow steadily this year, largely driven by increased capitalspending on part of the government. Rising consumer spending should alsoadd to growth. The inflation rate as well as the unemployment rate willremain above 10%. The most important risk to inflation would be a severeweakening of the bolívar. The Central Bank is using its full arsenal ofmeasures, including tightening liquidity, raising rates and selling US dollars,to defend the currency.

Key changes from last monthPolitical outlook• Although the FBT had initially rejected participation in the CTV elections

on the grounds that the opposition-dominated organisation was corrupt,it will participate in the elections, which are now set for October 25thfollowing two postponements.

Economic policy outlook• In a further attempt to bolster the weakening bolívar, the Central Bank

raised its discount rate to 37%, from 32%, on September 10th.

Economic forecast• Tightening liquidity and rising interest rates will undermine domestic

demand in 2001 and put some downward pressure on GDP growth.

The Economist Intelligence UnitThe Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through our digital portfolio, where our latest analysis isupdated daily; through printed subscription products ranging from newsletters to annual referenceworks; through research reports; and by organising seminars and presentations. The firm is a member ofThe Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1007Fax: (44.20) 7830 1023E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 0248E-mail: [email protected]

Hong KongThe Economist Intelligence Unit60/F, Central Plaza18 Harbour RoadWanchaiHong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

Website: www.eiu.com

Electronic deliveryThis publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, onlinedatabases and as direct feeds to corporate intranets. For further information, please contact your nearestEconomist Intelligence Unit office

Copyright© 2001 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

ISSN 1350-7133

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

Venezuela 1

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

Contents

3 Summary

4 Political structure

5 Economic structure5 Annual indicators6 Quarterly indicators

7 Outlook for 2001-027 Political outlook8 Economic policy outlook9 Economic forecast

12 The political scene

17 Economic policy

22 The domestic economy22 Economic trends25 Oil and gas27 Industry28 Agriculture29 Infrastructure30 Financial and other services

32 Foreign trade and payments

List of tables

9 International assumptions summary10 Forecast summary18 Public finances, Jan-Mar 200119 OPEC quotas19 Tax targets and results20 Total budgetary impact of minimum wage rise23 Car sales24 Retail sales24 Consumer price inflation27 Physical production trends in key sectors, 200130 Bank deposits31 Bank lending33 Trade balance33 Selected exports34 Current account35 Foreign reserves

2 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

List of figures

12 Gross domestic product12 Bolívar real exchange rates23 Economic growth26 OPEC crude oil production, 200126 Oil prices, 2001-0934 Current account and trade balance

Venezuela 3

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

Summary

September 2001

Hugo Chávez’s government will face continued industrial relations unrest asunions struggle to mobilise support ahead of the election of new unionauthorities in September. However, in spite of the street protests Mr Chávezremains popular. The legislature will focus on its backlog of bills, whichincludes the controversial Hydrocarbons Law and Land Law. Despite a steadystream of oil revenue, the fiscal accounts remain under pressure. The CentralBank will take further measures to defend the weakening bolívar, drawingfurther on its large stock of foreign reserves. The economy will grow slowly thisyear, largely driven by government investment and some consumer spending.The external accounts will remain in surplus, but will deteriorate on account ofthe drop in oil revenue and growth in import spending.

Elections for Venezuela’s largest union, the CTV, have been postponed untillate October. The government-backed FBT union will field a unity candidatewho enjoys Mr Chávez’s open support. The legislature has been takingextraordinary measures to speed up the process of implementing legislation.Mr Chávez has been seeking to rebuild his grassroots support base as tensionsin his own party could undermine his legislative support.

PDVSA’s dividend payment flattered April-May fiscal revenue data. The CentralBank has tightened liquidity and interest rates have risen. Import controls arelikely to back up support for the bolívar. There is concern about the Hydro-carbons Law. The cancelled electricity sale could contribute to an energy crisis.

The economy is recovering only slowly as a result of a lack of private-sectorinvestment. Inflation is proving stubborn, but unemployment is declining. TheHydrocarbons Law could curb foreign investment in the sector, and the LandLaw proposals are also causing much concern. More agricultural credit shouldbecome available. Construction of government-sponsored housing has been slowto pick up. The financial sector is facing difficulties, with deposits continuing tofall, mutual funds suffering outflows, and new measures to improve stock-exchange liquidity unlikely to increase the market’s attractiveness substantially.

Venezuela and CAN have argued over trade preferences. The trade surplus isnarrowing. Petrochemicals exports are facing difficulties owing to a weakerglobal scenario and the strong bolívar. Pressure is increasing on the balance ofpayments, but foreign direct investment has held up well. The government hasmade another foray into the international markets, while a further tranche ofIBD money is on the way. Capital flight is rising.

Editors: Ondine Smulders (editor); Justine Thody (consulting editor)Editorial closing date: September 10th 2001

All queries: Tel: (44.20) 7830 1007 E-mail: [email protected] report: Full schedule on www.eiu.com/schedule

The domestic economy

Economic policy

Foreign trade andpayments

Outlook for 2001-02

The political scene

4 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

Political structure

The Bolivarian Republic of Venezuela

Federal republic comprising 72 federal dependencies, 23 states, two federal territories andone federal district

The president is elected for a renewable six-year term and appoints Council of Ministers;Hugo Chávez began a fresh six-year term following elections in July 2000 to relegitimisepublic posts under the 1999 constitution

165-member unicameral National Assembly, headed by the president, which replacedthe bicameral Congress abolished by the new constitution in December 1999

Supreme Court at the apex of the court system; appoints judges and magistrates inconsultation with civil society groups.

Presidential, legislative and state government elections were held in July 2000 and thosefor municipal authorities in December 2000; legislative elections due in 2005; nextpresidential election likely in 2006

Government: the president’s party, the Movimiento Quinta República (MVR), forms partof the ruling Polo Patriótico (PP) alliance; Proyecto Venezuela (PV) is allied in theNational Assembly with the PPOpposition parties: Acción Democrática (AD); the Comité de Organización PolíticaElectoral Independiente (COPEI); Movimiento al Socialismo (MAS); Patria Para Todos(PPT); Primer Justicia (PJ); La Causa Radical (LCR); Convergencia Nacional (CN)

President Hugo ChávezVice-president Adina Bastidas

Presidential secretary Diosdado Cabello

Defence José Vicente RangelEducation, culture & sport Héctor Navarro DíazEnergy & mines Alvaro Silva CalderónEnvironment & natural resources Ana Lisa OsorioFinance Nelson MerentesForeign affairs Luís Alfonso DávilaHealth & social development María Lourdes UrbanejaInfrastructure (transport, communications & urban development) General Eliécer Hurtado SucreInterior & justice Luís MiquilinaLabour Blancanieves PortocarreroPlanning & development Jorge GiordaniProduction & trade Luisa RomeroPrivatisation Antonio GinerScience & technology Carlos Genatio

Diego Luís Castellanos

Official name

Form of government

The executive

National legislature

Legal system

National elections

Main political organisations

Key ministers

Central Bank governor

Venezuela 5

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

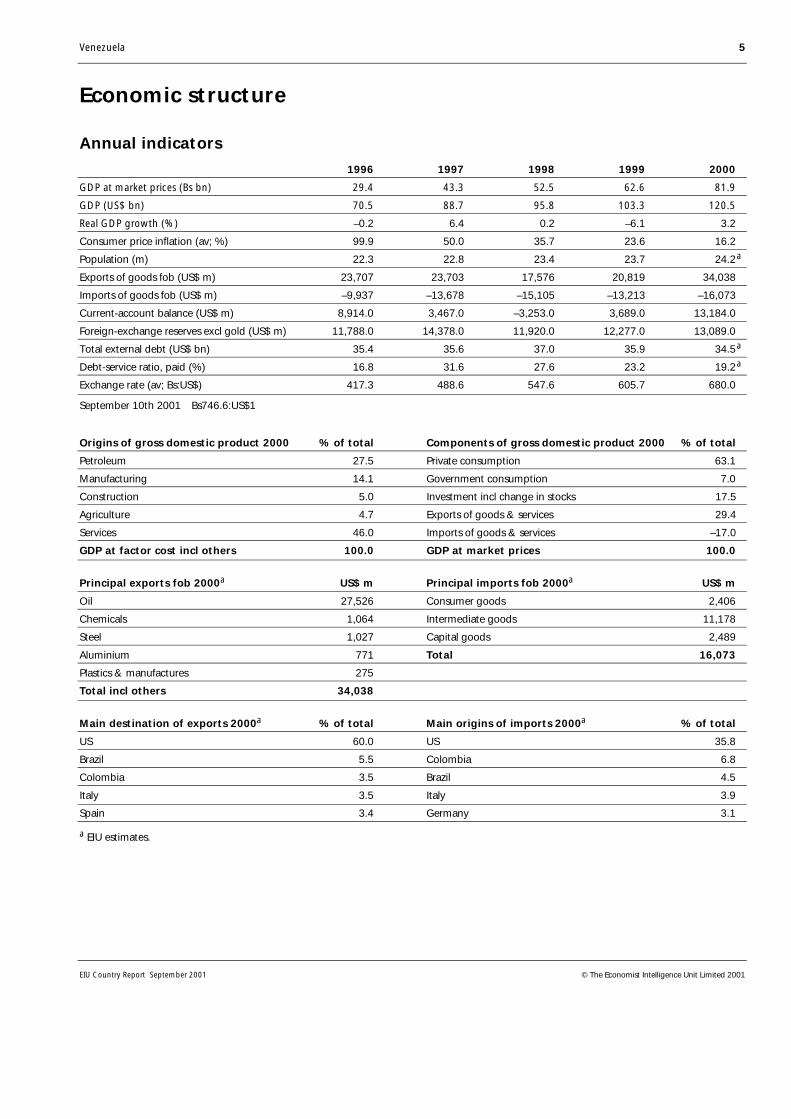

Economic structure

Annual indicators

1996 1997 1998 1999 2000

GDP at market prices (Bs bn) 29.4 43.3 52.5 62.6 81.9

GDP (US$ bn) 70.5 88.7 95.8 103.3 120.5

Real GDP growth (%) –0.2 6.4 0.2 –6.1 3.2

Consumer price inflation (av; %) 99.9 50.0 35.7 23.6 16.2

Population (m) 22.3 22.8 23.4 23.7 24.2a

Exports of goods fob (US$ m) 23,707 23,703 17,576 20,819 34,038

Imports of goods fob (US$ m) –9,937 –13,678 –15,105 –13,213 –16,073

Current-account balance (US$ m) 8,914.0 3,467.0 –3,253.0 3,689.0 13,184.0

Foreign-exchange reserves excl gold (US$ m) 11,788.0 14,378.0 11,920.0 12,277.0 13,089.0

Total external debt (US$ bn) 35.4 35.6 37.0 35.9 34.5a

Debt-service ratio, paid (%) 16.8 31.6 27.6 23.2 19.2a

Exchange rate (av; Bs:US$) 417.3 488.6 547.6 605.7 680.0

September 10th 2001

Bs746.6:US$1

Origins of gross domestic product 2000 % of total Components of gross domestic product 2000 % of total

Petroleum 27.5 Private consumption 63.1

Manufacturing 14.1 Government consumption 7.0

Construction 5.0 Investment incl change in stocks 17.5

Agriculture 4.7 Exports of goods & services 29.4

Services 46.0 Imports of goods & services –17.0

GDP at factor cost incl others 100.0 GDP at market prices 100.0

Principal exports fob 2000a US$ m Principal imports fob 2000a US$ m

Oil 27,526 Consumer goods 2,406

Chemicals 1,064 Intermediate goods 11,178

Steel 1,027 Capital goods 2,489

Aluminium 771 Total 16,073

Plastics & manufactures 275

Total incl others 34,038

Main destination of exports 2000a % of total Main origins of imports 2000a % of total

US 60.0 US 35.8

Brazil 5.5 Colombia 6.8

Colombia 3.5 Brazil 4.5

Italy 3.5 Italy 3.9

Spain 3.4 Germany 3.1

a EIU estimates.

6 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

Quarterly indicators

1999 2000 20013 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr

Central government finance (Bs bn)Ordinary revenue 2,888.2 3,183.3 3,212.2 3,199.4 3,329.5 4,915.4 3,652.2 4,864.6Ordinary expenditure 2,958.0 3,760.7 4,137.7 3,563.6 4,118.4 6,531.6 4,172.9 5,119.0Balance –69.8 –577.4 –925.5 –364.2 –788.9 –1,616.2 –520.7 –254.3Net extraordinary revenue 314.9 547.9 1,606.4 1.2 353.7 1,727.7 410.5 249.7

OutputGDP at constant 1984 market prices (Bs m) 141,564 144,510 139,196 146,015 145,731 153,312 144,367 150,281 % change, year on year –4.3 –4.1 1.1 2.7 2.9 6.1 3.8 2.9

Employment & PricesUnemployment rate (% of labour force) 14.5 14.5 14.6 14.6 13.2 13.2 14.6 n/aConsumer prices (1997=100) 171.5 178.7 185.7 191.9 198.1 204.1 209.1 215.7 % change, year on year 22.2 20.1 18.3 17.1 15.5 14.2 12.6 12.4Wholesale prices (1997=100) 140.3 143.1 147.2 151.5 154.8 158.4 160.1 162.8 % change, year on year 12.5 10.1 9.4 10.2 10.3 10.7 8.8 7.5Venezuelan crude basket (US$/barrel; spot) 18.31 21.84 25.30 25.09 27.92 27.58 21.96 22.39 % change, year on year 12.9 128.7 164.9 80.8 52.5 26.3 –13.2 –10.8

Financial indicatorsExchange rate Bs:US$ (av) 616.75 635.90 659.04 677.36 688.06 695.37 702.60 713.57 Bs:US$ (end-period) 628.00 648.25 669.50 682.00 690.75 699.75 707.75 718.25Interest rates (av; %) Deposit 14.65 16.67 16.97 19.22 13.16 15.85 12.97 12.45 Lending 30.08 26.39 26.20 23.75 24.91 25.95 18.06 19.56 Money market 5.10 7.30 6.57 10.40 6.90 8.70 5.93 12.57M1 (end-period; Bs bn) 4,628 6,096 5,644 5,772 6,037 8,016 7,456 7,405 % change, year on year 10.4 23.4 32.7 29.9 30.4 31.5 32.1 28.3M2 (end-period; Bs bn) 10,606 12,741 12,524 12,926 13,410 16,285 15,278 14,862 % change, year on year 17.9 19.9 23.9 24.0 26.4 27.8 22.0 15.0BVC Caracas stockmarket index (end-period; Dec 1993=1,000) 5,818 5,418 5,496 7,033 6,864 6,825 7,357 7,560 % change, year on year 49.4 13.1 32.9 31.0 18.0 26.0 33.9 7.5

Sectoral trendsProduction Crude oil (m barrels/day) 2.73 2.75 2.80 2.87 2.92 2.99 3.00 2.82 % change, year on year –8.1 –7.7 –4.4 4.7 7.0 8.7 7.1 –1.7 Aluminium ('000 tonnes) 145.0 141.3 139.3 143.0 144.0 144.4 141.7 143.9 % change, year on year 0.8 –0.8 –0.3 –1.0 –0.6 2.2 1.7 0.6 Iron ore (‘000 tonnes) 3,620 5,000 5,466 5,662 4,610 4,312 5,062 5,269 % change, year on year –25.4 35.5 50.4 47.2 27.3 –13.8 –7.4 –6.9Foreign trade & paymentsa (US$ m)Exports fob 5,991 6,552 7,733 8,182 8,540 9,583 7,297 7,111 Petroleum & products 4,919 5,393 6,500 6,864 7,276 8,076 6,028 5,805Imports fob –3,741 –3,683 –3,346 –4,181 –4,249 –4,297 –3,954 –4,470Merchandise trade balance 2,250 2,869 4,387 4,001 4,291 5,286 3,343 2,641Services –649 –521 –682 –779 –895 –953 –799 –767Income balance –269 –401 –229 –309 –264 –361 –53 –78Net transfer payments 2 44 –6 –64 –36 –37 –75 –133Current-account balance 1,334 1,991 3,470 2,849 3,096 3,935 2,416 1,663Reserves excl gold (end-period) 11,135 12,277 11,412 12,153 13,686 13,089 12,045 10,460

a Balance-of-payments basis.Sources: IEA, Monthly Oil Market Report; IMF, International Financial Statistics; Banco Central de Venezuela, Indicadores Econúmicos; VenEconomy Monthly.

Venezuela 7

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

Outlook for 2001-02

Political outlook

Industrial relations are expected to remain fractious in the short term as unionsattempt to mobilise support ahead of the internal elections of the main,opposition-dominated union confederation, the Confederacíon de Trabajadoresde Venezuela (CTV, the Venezuelan Workers’ Confederation). The significanceof the elections, which are now scheduled for October 25th, is underscored bythe decision of the pro-government Frente Bolivariana de Trabajadores (FBT, theBolivarian Workers’ Front) to participate. The participation of the FBT in theCTV elections represents a significant climbdown for the FBT, which PresidentHugo Chávez had hoped would become the leading force in union politics.Under the terms approved in a popular referendum in December 2000, theunion movement will be unified. The government had anticipated that thiswould mark the end of the CTV, as it would be integrated into an FBT-dominated confederation. However, the failure of the organisationallyinexperienced FBT to build a significant presence in the labour force has meantthat it is likely to accept participation in the CTV elections, leading to a de factovictory for the CTV over the government and the FBT.

A strong showing by the opposition-dominated unions in the CTV elections mayprolong union conflict, as it could be interpreted as an endorsement of theconfederation’s current anti-government position. The CTV’s position at theforefront of workers’ demands for improved pay and conditions has resulted in asharp increase in support, a strategy that pro-government unions will finddifficult to replicate. Mr Chávez’s response to a poor showing by the FBT is opento question, and his unpredictability remains a source of political risk. Theescalation of protests may pressure the administration to drop its prudent line onsalaries and to undermine fiscal management. The performance of the ConsejoNacional Electoral (CNE, the National Electoral Council) will also be subject toscrutiny. Perception of electoral fraud would do little to enhance the legitimacyof the institution and would prove damaging for Mr Chávez.

While the CTV had emerged as an umbrella organisation for anti-governmentprotests, incorporating opponents of the administration’s land, education,union and economic policies, the forthcoming elections will force the con-federation to focus specifically on union-related issues. This will not under-mine the opposition forces outside the legislature, which have grown incoherence and numbers since the end of 2000. The second half of the year willbe politically difficult for the administration, with interest groups ready tomobilise against a number of contentious bills yet to be approved owing to alegislative backlog.

Although Mr Chávez remains popular, opinion polls point to a slow deter-ioration in his support, although at 53%, it remains high and he continues toenjoy a prolonged honeymoon period. This owes much to the disrepute inwhich the opposition parties are held and the popular rejection of their strategyof mobilising international opinion against Mr Chávez, a tactic that has

Domestic politics

8 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

provoked a backlash of nationalist sympathy for the president. Mr Chávez isparticularly vulnerable on crime, which he pledged to reduce, and job creation.With little progress so far on either front, the president may become increasinglyreliant on the military, both on the streets and in the cabinet, to overcome theperceived incompetence of regional and municipal police and the inertia of thestate bureaucracy. A sharp downturn in his popularity would be destabilising.

Mr Chávez’s strategy of regional political and economic integration continuesto face setbacks, with recent resolutions by the Caribbean Community(Caricom) at the Heads of State Summit underlining the organisation’s sus-picion of the economic intentions and territorial ambitions of the Venezuelangovernment. Relations with Peru are on the mend, as its new president,Alejandro Toledo, has played down the antagonism between the two countriescaused by the events surrounding the arrest and deportation from Venezuela ofthe former head of Peruvian intelligence, Vladimiro Montesinos.

Economic policy outlook

A far-reaching reform of labour and social security legislation is finallyexpected to be submitted to Congress in 2001. Progress on reducing unemploy-ment remains painfully slow. Open unemployment fell only slightly in thesecond quarter of 2001, to 13.3%, down from 14.2% at the end of the firstquarter but up from 12.1% at the end of 2000. The proportion of the labourforce employed in the informal sector was little changed, at 52%. Public-sectorinvestment programmes will provide only partial and temporary solutions.Such programmes also remain hampered by weak implementation capacity.Entrenched administrative inefficiency, which has hampered the investmentambitions of successive governments, has been made worse under Mr Chávezby the stand-off between the administration and the traditional elite, whichstarves government departments of much potential technical expertise. TheLey de Tierras (Land Law) has been a focus of concern in recent months asrumours have abounded over the risks of expropriation and the imposition oflimits on the size of landholdings.

According to the former finance minister, José Rojas (recently replaced by NelsonMerentes), Venezuela recorded a public-sector deficit of 2% of GDP in the first halfof 2001, well below the 3% target for the year. This was mainly the result ofhigher-than-budgeted oil revenue owing largely to dividend revenue fromPetróleos de Venezuela (PDVSA, the state-owned oil monopoly). However, the factthat the government accounts were in deficit despite rising petroleum-relatedrevenue and surprisingly conservative expenditure highlights the deep underlyingimbalances in the fiscal accounts. Moreover, pressure on government spending isset to increase in coming years, while oil revenue will decline as prices soften.Growing fiscal liabilities include wage and social security arrears inherited fromprevious administrations, officially estimated to total at least US$20bn, and amuch-needed increase in social investment. The structural reforms needed toplace the fiscal accounts on a sustainable path in the longer term, includingsocial security reform and rationalisation of bureaucracy, will also be costly.

International relations

Fiscal policy

Policy trends

Venezuela 9

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

The government is struggling to raise non-oil tax collection by improvingefficiency and curbing evasion. However, the Servicio Nacional Integrado deAdministración Aduanera y Tributaria (Seniat, the tax authority) remains indisarray, lacking both qualified personnel and effective institutional autonomy.

Economic forecast

The external climate is unfavourable for Venezuela, which is sensitive toeconomic growth in the US, its largest export market, and global oil pricedevelopments. In 2001 the world economy will experience its sharpest slow-down since the 1974 oil price shock. World growth will recover in 2002, but astrong rebound now looks unlikely. Moreover, the risks to the EconomistIntelligence Unit’s forecast are significant, owing to the imbalances in the USeconomy, in particular stretched equity valuations, a large current-accountdeficit and low rates of private-sector savings. If these imbalances were to beunwound suddenly, the US could enter a protracted recession. Given thecurrent weaknesses in Japan, the world’s second largest economy, this outcomecould tip the rest of the world into recession.

OPEC’s decision in July to cut production by 1m barrels/day from Septemberwill take OPEC supply to its lowest level in more than two years. The cut, thethird in 2001, brings the combined OPEC reduction to 3.5m b/d. In theory,this cut could push the oil market back into deficit in the fourth quarter,although we believe a small wind-down of inventories, followed by a return tosurplus early in 2002, is more likely than a serious shortage accompanied by aprice spike. We expect that Brent oil prices will average US$26.6/barrel in 2001,falling only marginally in 2002, to US$26/1/b.

International assumptions summary(% unless otherwise indicated)

1999 2000 2001 2002

Real GDP growthWorld 3.6 4.6 2.7 3.6OECD 3.1 3.7 1.4 2.4EU 2.5 3.4 1.9 2.4

Exchange rates (av)¥:US$ 113.9 107.8 122.7 123.5US$:€ 1.07 0.92 0.88 0.96SDR:US$ 0.731 0.758 0.791 0.768

Financial indicators¥ 2-month private bill rate 0.27 0.24 0.18 0.10US$ 3-month commercial paper rate 5.18 6.32 4.04 4.75

Commodity pricesOil (Brent; US$/b) 17.9 28.5 26.6 26.1Gold (US$/troy oz) 278.8 279.3 263.0 255.0Food, feedstuffs & beverages

(% change in US$ terms) –18.6 –6.1 1.2 15.0

Industrial raw materials (% change in US$ terms) –4.6 13.4 –3.9 3.9

Regional aggregate GDP growth rates weighted using purchasing power parity exchange rates.

International assumptions

10 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

Forecast summary(% unless otherwise indicated)

1999a 2000a 2001b 2002b

Real GDP growth –6.1 3.2 2.9 3.4

Gross agricultural production growth –2.1 1.4 2.5 2.5

Unemployment rate (av) 14.9 13.9 14.0 13.8

Consumer price inflation Average 23.6 16.2 12.7 14.6 Year-end 20.0 13.4 13.0 15.4

Short-term interbank rate 32.1 25.2 23.9 22.7

Central government balance (% of GDP) –2.9 –1.7 –2.6 –1.4

Exports of goods fob (US$ bn) 20.8 34.0 32.3 32.7

Imports of goods fob (US$ bn) 13.2 16.1 18.1 19.4

Current-account balance (US$ bn) 3.7 13.2 8.9 7.5 % of GDP 3.6 10.9 6.8 5.3

External debt (year-end; US$ bn) 35.9 34.5c 34.3 34.7

Exchange rates Bs:US$ (year-end) 648.3 699.8 740.9 813.5 Bs:¥100 (av) 531.8 631.0 587.8 631.0 Bs:€ (year-end) 651.2 657.0 670.5 821.6 Bs:SDR 889.7 911.7 940.4 1,081.4

a Actual. b EIU forecasts. c EIU estimate.

Venezuela’s economy will grow faster than that of most other countries in theregion, but it is facing strong downward pressures nevertheless. Sliding oil pricesare reducing state revenue, unemployment remains high and the global eco-nomy is slowing. Moreover, pressure on the bolívar has triggered correctivemeasures that are squeezing liquidity, further limiting growth. Public invest-ment, the most likely source of growth this year, is struggling with delays inimplementation. As the contribution from net trade is faltering and governmentconsumption is reigned in, investment—boosted by public projects—and privateconsumption will be the main engines of growth, though neither will be strong.

Our GDP growth forecast for 2001 of 3% was reinforced by second-quarter data,which showed GDP up by 2.9% year on year. This followed an upward revisionof the first-quarter growth rate to 3.8%, bringing the first-half average to 3.4%.The first-half expansion was largely fuelled by the non-oil sector, which rose by5.9% on the back of a rise in government spending, particularly construction.Oil-related GDP actually contracted by 2.3%—reflecting the constraints imposedby adherence to OPEC quotas. The government has not adjusted its official 4.5%growth target, although the Banco Central de Venezuela (the Central Bank) hashinted that it regards an outcome of 3.5-4% as more likely.

The comparatively low rate of average monthly inflation of 1% posted in thefirst eight months of 2001 indicates that the strength of the bolívar is helpingto offset increased price pressures stemming from the continuing recovery ofdemand. With a further real appreciation of the exchange rate expected in2001-02, the government should be able to restrain average inflation to below15% per year. Mr Chávez’s desire to contain wage growth was reflected in the

Economic growth

Inflation

Venezuela 11

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

moderate 10% increase in the minimum wage announced in July. However,political expediency in the approach to union elections in October could yetcause this award to be revised upwards, increasing inflationary pressures.Ultimately, the main risk to price inflation in the coming years stems from therisk of a sharp exchange-rate correction. A strong reserves position andbuoyant prospects for oil earnings make this unlikely in 2001-02, but the riskwould grow if oil prices were to fall below US$20/barrel, which would exposestructural weaknesses in the fiscal finances more starkly.

Despite the bolívar’s recent weakening to Bs746.6:US$1, the currency hascontinued to appreciate in real terms against a strong US dollar, with themonthly nominal depreciation averaging 0.3% in January-August and monthlyprice inflation averaging 1%. We expect the currency to continue to appreciatein real terms in 2001-02, keeping inflationary pressures in check. The strongexchange rate has been a central tool in the government’s battle to controlinflation, but it is incompatible with its aims of promoting the development ofsmall and medium-sized enterprises (SMEs) and agriculture. In 2001-02 firm oilprices will keep reserves strong, supporting the government’s strong exchange-rate policy, but as fiscal weaknesses become increasingly evident, speculativepressure on the currency will build. The fact that reserves have been decliningin a year of firm oil prices is indicative of the high level of capital flight.

In August one of the directors of the Central Bank, Domingo Maza Zavala, con-firmed that the Bolívar would remain on its 7% devaluation curve this year, butadded that it could be pegged to the US dollar in 2002 if oil prices and economicconditions were favourable. Mr Maza Zavala also indicated that the rise in USdollar demand had led the authorities to study policy alternatives to reduce suchdemands—hence capital controls could still be on the agenda. Such controlscould be introduced if the latest liquidity measures, the discount rate increase,the selling of US dollars and import controls prove insufficient to prevent furtherpressure on the bolívar.

Second-quarter current-account data reinforced the weakening trend in theexternal accounts. They show a current-account surplus of US$1.7bn, down fromUS$2.4bn in the first quarter of 2001 and US$2.8bn in the second quarter of 2000.The deterioration is largely a result of the narrowing of the trade surplus toUS$2.6bn, reflecting the decline in oil export revenue and rising import spending.The current-account surplus will narrow from 2001 as softening oil prices andrising imports associated with a strengthening of the economic recovery and astrong exchange rate cause the trade surplus to shrink. The impact on the currentaccount will be exacerbated by a growing invisibles deficit, driven by increasedspending by Venezuelans abroad and, from 2002, by rising interest payments onthe external debt, reflecting the forecast rise in US interest rates from 2002.Outright capital flight and negative portfolio flows will exacerbate these outflows.However, the authorities are introducing measures to combat outflows. The firstpackage, tightening banks’ liquidity requirements, has come into force, while thesecond package, introducing new import restrictions, has still to be announced indetail. At this stage, it is difficult to assess how much this will affect the balance ofpayments, other than to slow the deterioration in the trade account.

External sector

Exchange rates

12 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

The political scene

The main union confederation, the historically unpopular Confederacíon deTrabajadores de Venezuela (CTV, the Venezuelan Workers’ Confederation),encountered a setback in mid-August when the Consejo Nacional Electoral(CNE, the National Electoral Council) announced its intention to suspend theSeptember 25th CTV election. The Supreme Justice Tribunal allowed thepostponement of the election to October 25th as the CNE could not guaranteethe completion of union and voter registration requirements nor the trans-parency of the election process. The opposition-dominated unions condemnedthe move, specifically the Frente Unitario de Trabajadores (FUT), whosecandidate for the CTV presidency, Carlos Ortega, is considered a frontrunner.

Within days of the announcement, the pro-government union, the FrenteBolivariana de Trabajadores (FBT, the Bolivarian Workers’ Front), finallyreached an agreement with the former allies of the ruling Polo Patriótico (PP)coalition, Patria Para Todos (PPT), to field a joint candidate for the CTVpresidency. A PPT member and a former mayor of Caracas, Aristóbulo Istúriz,was selected as the unity candidate, as the FBT objected to Pablo Medina, theoriginal PPT candidate. The FBT’s reliance on the PPT for a strong candidate isindicative of the FBT’s limited organisational and leadership experience. Thesubsequent decision by the Movimiento al Socialismo (MAS), another formerPP member, to support Mr Istúriz will encourage the emergence of a two-horse race.

The selection of Mr Istúriz, a popular former teacher with strong links to thegrassroots of the union movement, will pose a challenge to Mr Ortega,especially as Mr Istúriz has succeeded in uniting the diverse left-wing and pro-government unions. The personal endorsement of Mr Istúriz by the president,Hugo Chávez, has raised protests that Mr Chávez’s use of his radio programmeto promote the FBT candidate has provided an unfair advantage. Moreover, ithas increased speculation that the CNE’s decision to reschedule the elections

FBT runner enjoysMr Chávez’s open support

Government-backed FBTfields a unity candidate

Union elections postponed

Venezuela 13

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

was intended to increase the campaigning time available to Mr Istúriz. Despitethe FBT’s preliminary objections to the rescheduling, the organisation’s leader-ship announced that it would accept the date change in order to preclude thethreat of government intervention.

Since December 2000’s union reform referendum—which saw Mr Chávez winpopular backing for union elections, but based on a very low voter turnout—the union movement has mounted an unexpectedly strong challenge againstthe government. Labour strife has increased and the CTV has beentransformed into an important vehicle for anti-government protest. Thedevelopment of the FBT has been hindered by the revival of the politicalfortunes of the CTV, which has placed itself at the forefront of an escalationin workers’ demands for improved pay and conditions. The FBT has struggledto recruit its target 1m members and the government’s strategy of absorbingthe CTV into a single, FBT-dominated confederation has backfired: theopposition-dominated unions that control the CTV have extensive organ-isational experience and, given the CTV’s current popularity among thelabour force, look set to retain control of the confederation.

Although the government has found its authority seriously challenged by theCTV, the union movement has failed to achieve significant concessions fromthe administration. The administration did not compromise its fiscally prudentstance when it raised the minimum wage by 10% in July. The increase takesthe minimum wage to Bs158,400 (US$220) per month. Given yearly inflationlevels above 12%, this rise implies a contraction of the minimum wage in realterms. In fact, in real terms the minimum wage is just below the 1997 level. Noincrease was decreed for workers earning more than the minimum salary andthe government emphasised that it respected the right of private companies tonegotiate wage increases with its workers without the intervention of thegovernment. This represents a break with industrial relations tradition inVenezuela, where the government has traditionally decreed wage increasesacross both the private and public sector.

Although there has been an unprecedented concentration of power in theexecutive since Mr Chávez took office, the president has passed only eight of the44 bills planned for the year, with just four months of his fast-track authorityremaining—granted for a period of one year ending in November 2001 underthe Ley Habilitante (Enabling Law), which permits the introduction of legislationin a range of areas without debate in the National Assembly.

Progress through the legislative timetable has been similarly slow in theNational Assembly. The transition to unicameral arrangements under the 1999constitution and a ruling party majority has not altered the slow pace that hastraditionally characterised congressional approval of legislation. Of the 80pieces of legislation placed on the assembly’s agenda for 2001, only five havebecome law. The backlog has been criticised by leading private-sectororganisations as a deterrent to investment, and the opposition has found iteasy to spread concern regarding the likely content of legislation.

Unions fail to attain majorgovernment compromises

Adoption of new laws slow

14 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

The National Assembly’s failure to complete its agenda before the summer recessof August 15th prompted the launch of extraordinary sessions to deal with 31pieces of legislation. These included the Central Bank Law, the reforms of incomeand capital gains tax, value-added tax (VAT), budgetary laws, Treasuryrequirements, taxation laws, education law, agricultural law, comptrollerregulations, and the Penal Process Code—deemed essential to tackle crime andimprove co-ordination of the police services. The Central Bank Law was passedin late August and the majority of financial legislation has had a preliminaryreading. The Ley de Tierras (Land Law) required modification ahead of its firstreading. The new Social Security Law will be discussed in late September. TheMovimiento Quinta República (MVR) has tried to build a consensus oneducation law, which would modify the controversial education decreeintroduced by Mr Chávez at the end of 2000 (March 2001, page 15).

Mr Chávez has complained that bills central to the administration’s economicand social policy programme are stalled in the assembly and that the backlogof legislation is holding up the executive’s policy work. While this is true inpart, Mr Chávez’s tendency to become involved in every aspect of governmentand politics has contributed to the legislative delay. The centralisation of poweraround the executive has reversed earlier efforts at the decentralisation ofpolicymaking, adding to the backlog of promised legislative initiatives fromthe cabinet. Moreover, the dominance of the executive has weakened otherstate institutions, including the National Assembly, where the polarisationbetween supporters and opponents of Mr Chávez has reduced productivity andexacerbated partisan conflict. The majority of assembly representatives fromthe ruling MVR lack political experience, and the opposition has found it easyto determine the pace of events in the legislature.

The poor performance of the MVR in the National Assembly underlines theorganisational weakness of Mr Chávez’s political base, leaving the govern-ment’s popularity and legitimacy overwhelmingly dependent on the pres-ident’s personal charisma. In contrast to the opposition parties, which boast along history and tight organisational structure, the MVR was only formed in1996. An influx of opportunists and the centralisation of political authorityaround Mr Chávez have undermined its coherence, both ideologicaland organisational.

Aware of the MVR’s limited political penetration at the grassroots level ofVenezuelan society, Mr Chávez announced plans in June to develop circles ofpolitical activitists under the direction of the Movimiento BolivarianoRevoluciónario 200 (MBR-200), the civil-military alliance organisation thatacted as the forerunner of the MVR (June 2001, pages 13-14). The governmenthas also publicly criticised corruption within the MVR, and the links betweenthe president and his political party have become increasingly fragile in theabsence of routine meetings and policy discussions. Senior figures in the partyhave expressed concern that Mr Chávez and the interior and justice minister,Luís Miquilena, one of the president’s leading advisers, are seeking to sidelinethe party and focus on rebuilding MBR-200 at the expense of the MVR.Deprived of influence in the government and increasingly perceived as corrupt

Mr Chávez complains aboutlegislative backlog

Mr Chávez seeks to rebuildhis grassroots support base

Venezuela 15

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

and unrepresentative, the MVR has started to fall apart. Factionalism hasincreased and the departure of individual assembly members from the partycannot be ruled out.

Increasing divisions within the MVR could further reduce the government’smajority in the assembly. The PP alliance, which supported Mr Chávez’spresidential bid in 1998, intially grouped the MVR with two left-wing parties,the PPT and MAS. These parties have left the alliance following policydifferences and personality clashes with Mr Chávez. Their departure hasreduced the MVR’s leverage in the National Assembly and deprived the rulingparty of the solid network of experienced activists and supporters that MASand the PPT brought with them. Although the contribution made by MAS andthe PPT to Mr Chávez’s political and electoral success has largely been playeddown by the government since 1998, the absence of these parties from thecoalition has amplified the organisational frailties of the MVR.

Despite the tensions within the MVR, Mr Chávez himself remains extremelypopular, with the support of around 53% of the population according to recentopinion polls. However, this will diminish if the government fails to addressissues cited by Venezuelan citizens as crucial. Critical in this respect are jobcreation and a reduction in the rising level of crime, both central elements ofMr Chávez’s pre-election manifesto. The administration is particularly vulnerableon crime, which has increased dramatically in recent years. Despite the deploy-ment of the National Guard in the most dangerous areas, the weekend murderrate in the capital, Caracas, has now reached triple-digit figures, while the annualnational murder rate has doubled since 1991 and kidnap risk has increased.

The potential shift in opinion was illustrated in a poll conducted byMercanálisis in August clearly reflecting the population’s continued concernover public security. In the poll, 65% of respondents felt that Mr Chávez hadbeen ineffective in confronting the rising crime problem. Responses in the pollreflect mounting support for the small Primero Justicia (PJ) party—derided bythe government as a “yuppie organisation”. While 26% of respondents claimedto support the MVR, the PJ emerged in second place with the endorsement of21% of voters. Acción Democrática (AD) and the Comité de OrganizaciónPolítica Electoral Independiente (COPEI), historically the largest two parties inthe country, trailed in the poll, with support of 7% and 2% respectively. Theimproving fortunes of the PJ were further reflected in a poll on futurepresidents, with the PJ leader, Julio Borges, trailing the MVR mayor of Caracas,Alfredo Peña, by just 1 percentage point, with 25% support. Francisco AriasCardenas, a former ally of Mr Chávez who challenged him for the presidencyin July 2000, received the support of 17% of respondents.

The government’s attempts to deal with the problem of personal security havebeen undermined by the failure of the National Assembly and the executive tomeet the legislative schedule. Core pieces of legislation relating to security andhuman rights have been held up in the National Assembly. This, combinedwith Mr Chávez’s reluctance to work with local government officials, hasimpeded the creation of an effective anti-crime strategy.

Rising crime could dentMr Chávez’s poll ratings

Tension in MVR couldreduce president’s support

Crime levels constitute amajor issue with electorate

16 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

In May Mr Chávez publicly debated the declaration of a state of emergency inorder to clamp down on crime and corruption. The proposal caused a mediabacklash and allegations from the opposition that the government was under-mining Venezuelan democracy. Although the suggestion was dropped byMr Chávez, the murder of a prominent businessman and the increasinglydamaging implications of the high crime levels for investor confidence haveled the private sector to revise its earlier opposition to emergency measures. InJuly the president of the Federación Venezolana de Cámaras y Asociaciones deComercio y Producción (Fedecámaras, the federation of trade and industrychambers) met the president of the National Assembly to lobby the govern-ment to introduce a 30-day state of emergency on the grounds of public safety.Although a state of emergency would boost the government’s ability to dealwith crime, it could undermine the legislative and institutional channels.

The government has been acutely embarrassed by events surrounding theentry and arrest in Venezuela of Vladimiro Montesinos, the head ofintelligence under the disgraced former Peruvian president, Alberto Fujimori.Mr Chávez’s triumphant announcement of the capture of Mr Montesinos inJune was rapidly subsumed by allegations from the opposition and Peru’sinterim foreign minister that the Venezuelan government had secretly allowedMr Montesinos entry into Venezuela in December 2000. The swift deportationof Mr Montesinos was accompanied by a diplomatic rift that saw bothcountries withdraw their ambassadors.

Four separate investigations into the entry and arrest of Mr Montesinos wereset up in Venezuela. These included one by the attorney-general, a second bythe Military Intelligence Directorate (DIM), which captured Mr Montesinos, athird by the Interior Committee of the National Assembly and a fourth by aTruth Commission established by opposition members of the assembly andformed in protest at their exclusion from the legislature’s official investigation.A number of unsavoury allegations linking the foreign and interior ministersand the former head of the Dirección de Servicios de Inteligencia y Prevención(Disip, the security services) to Mr Montesinos were made by the TruthCommission. The investigations of the three other bodies pointed in contrastto a plot to discredit Mr Chávez by his political opponents, including theformer president Carlos Andrés Pérez, against whom Mr Chávez launched amilitary coup attempt in 1992.

In light of the arrest of Mr Montesinos and evidence of the involvement ofDisip officers in hiding him, the new head of the Disip introduced an edictrequesting all previous employees to return their credentials and weaponslicences. While the truth behind Mr Montesinos’s presence in Venezuela hasyet to be revealed, the ongoing investigations served to demonstrate thepresence of officials opposed to and working against Mr Chávez in the securityforces and links between the domestic opposition and expatriot Venezuelansliving in the US.

Diplomatic relations between Venezuela and Peru saw a marked improve-ment following the inauguration of the new Peruvian president, AlejandroToledo, at the end of July. At his swearing-in ceremony—attended by

Private sector revisits state-of-emergency issue

Montesinos affairembarrasses government

But diplomatic row withPeru proves temporary

Venezuela 17

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

Mr Chávez—the Peruvian president emphasised the importance ofnormalising diplomatic relations between Venezuela and Peru and prioritisedintegration between Andean nations.

Relations between Venezuela and the 15 members of the CaribbeanCommunity (Caricom) have deteriorated, despite Mr Chávez’s stated objectiveof deepening ties with the regional group. At its 12th Heads of State Summitheld in the Bahamas in July, Caricom emphasised its support for Guyana in thecountry’s ongoing territorial dispute with Venezuela. The disagreement centreson the Essequibo delta, a 160,000-km stretch of land on the Venezuela-Guyanaborder. Caricom also rejected Venezuela’s sovereignty claim over the Isla LasAves, a 4-ha wildlife reserve 300 miles north of the Venezuelan mainland. Theorganisation recognised the island as territory of the Dominican Republic andexpressed concern that Venezuela’s claim represented a 200-mile extension ofits economic sea limits.

The organisation’s statement follows the decision by Barbados, a Caricommember, to purchase petroleum from Trinidad, as opposed to Venezuela, whichoffers more favourable terms under the Caracas Energy Accord. A formerdefence and foreign minister from Venezuela criticised the hostility of theEnglish-speaking Caribbean countries towards Venezuela.

Economic policy

Despite the headline improvement in the overall budget, which recorded adeficit equivalent to 2% of GDP in the first half of 2001 according to theMinistry of Finance—well below the full-year 3% target—detailed quarterlyaccounts give cause for thought. In the central government accounts, taxrevenue increased by 15% in the first quarter, mostly a result of higher incometax revenue. However, income tax revenue will struggle to keep up in the restof the year owing to the contraction in oil-related GDP in the second quarterand the importance of oil for income tax revenue. So far this year revenue fromvalue-added tax (VAT) has consistently been below target. Non-tax revenue fellby 4% in the first quarter, with oil-related royalty payments down by 5%.Excluding interest payments, current spending expanded by 4% in the sameperiod, implying a contraction in real terms.

The consolidated public-sector accounts, in contrast, saw a 5% year-on-year fall inrevenue in the first quarter, largely caused by a fall in non-tax revenue,particularly a decline in earnings from state enterprises. In real terms, totalspending fell slightly. Capital spending increased, in line with other data onpublic spending, especially construction spending, as it spurred economic growth.

According to the Banco Central de Venezuela (the Central Bank) the centralgovernment produced a small fiscal surplus of Bs35.8bn (US$50m) in April.Non-oil revenue rose marginally (up by 1.3% on March), but oil revenue rosesharply (up by 75.8%) in April as Petróleos de Venezuela (PDVSA, the state-owned oil monopoly) paid dividends totalling Bs600bn. Although total

Strained relations withCaricom

Budget still showsstructural weaknesses

PDVSA dividend paymentflatters April-May revenue

18 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

revenue jumped by 36.2% month on month in April, the increase is unlikelyto be repeated in the short term. Total spending rose by 3.2% in April, or 2% inreal terms. In January-April the central government deficit amounted toBs489bn, with revenue up by 37.8% year on year, largely owing to thesignificant dividend payments.

Preliminary figures from the finance ministry for the first five months of 2001show that 41% of total tax revenue stemmed from PDVSA. This amounted toBs3.5tr (US$4.9bn) by early June. PDVSA’s payments were roughly split inthirds between the above-mentioned dividends declared in tax year 2000 (nottaxed in 2000, when the government took recourse to internal debt issuanceinstead), fuel exploitation and property taxes.

Public finances, Jan-Mar 2001(Bs m unless otherwise indicated)

Consolidated Centralpublic sector % change government % change

Total revenue 5,569,818 –5.4 3,667,465 9.9Current revenue 5,528,351 –5.4 3,667,465 – Tax revenue 2,027,126 5.6 2,837,895 14.5 Income tax 504,971 30.8 – – Social security 164,891 6.7 – – Other 1,357,264 –1.6 – – Non-tax revenue 3,501,225 –10.8 829,570 –3.6Capital income 41,467 5.8 0 0

Total spending 4,772,556 10.8 3,720,736 9.6Current spending 3,087,189 –0.1 2,713,191 4 of which: remuneration 749,648 28.8 670,084 25 purchase of goods & services 282,666 4.1 192,831 79.4 interests & commissions 694,725 7.4 605,106 25.7 transfers 1,366,185 –2.7 1,275,183 –10.0 other –6,036 – –30,013 –Capital spending 1,522,181 47.8 856,745 41.1Off-budget spending 73,704 –26.9 73,704 –26.9Concessions (net of loans) 89,482 3.5 77,096 0.7

Financial balance 797,263 –49.5 –53,271 –5.6

Current balance 2,441,162 –11.5 954,274 31.1

Primary balance 1,491,988 –31.2 551,835 29.8

Note. Preliminary data.Sources: Oficina de Estadísticas de las Finanzas Publicas; Ministerio de Finanzas, EIU.

Analysis of the public finances is complicated owing to a serious lack oftransparency. The financial services group PwC recently found Venezuelanaccounting the most opaque among Latin America’s eight largest economies. Agood example of this complexity is the Fondo de Inversión para laEstabilización Macroeconómica (FIEM, the Macroeconomic StabilisationInvestment Fund). Its governing principles would suggest a total accumulationof US$12bn by the end of the year, as the fund absorbs 50% of government oiltax revenue above budgeted levels. So far, it only contains US$6.6bn. Althoughthis is in part a result of administrative delays as the procedures are veryconvoluted, the government’s pledge of further payments has yet to be

Lack of transparency slowsanalysis of public accounts

Venezuela 19

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

realised. It has also rebuked Central Bank allegations that the funds are beingused to fund current budget expenditure, claiming such money is only used tofund investment projects.

The basket oil prices for Venezuelan crude have stayed steadfastly above thebudgeted US$20/barrel since the start of 2001, recording in mid-August a year-to-date average of US$21.9/b. Crude prices have softened in response toweakening global demand, giving rise to concerns that PDVSA might not meetits revenue targets this year, affecting fiscal revenue. OPEC has reduced outputtargets for the third time this year. From September, Venezuela’s quota hasbeen reduced to 2.67m barrels/day. Oil production accounts for about one-third of GDP, one-half of government income and three-quarters of exports.

OPEC quotas(‘000 b/d unless otherwise indicated)

Apr Sep Production abovequota quota % change quota (Jun; %)

Venezuela 2,786 2,670 –4.2 2

Total (excl Iraq) 24,201 23,201 –4.1 7

Source: Middle East Economic Survey (MEES).

According to the head of the Servicio Nacional Integrado de AdministraciónAduanera y Tributaria (Seniat, the internal revenue service), Trino Alcides, thetax collection target for 2002 is Bs12tr, up by 46% on this year’s target ofBs8.2tr, which was itself 22% above last year’s official target of Bs6.7trn.However, the revenue target was missed by 21% in 2000. The authorities aretrying to improve their performance this year by increasing tax efficiency—both the VAT and income tax laws will be adjusted. Contrary to earliersuggestions, VAT exemptions will not be dropped. Instead, Seniat willstrengthen collection efforts. Additionally, a new income tax amnesty law willallow those with tax arrears to pay their debts over a period of up to two years.Seniat expects that this will raise a further Bs1bn in overdue payments, but it isnot clear how much of the estimated Bs1bn will actually benefit this year’saccounts. Although amnesty laws have a positive short-term impact on taxrevenue, they often have the opposite medium-term effect as people wait topay their taxes until the next reprieve deal is announced.

Tax targets and results(Bs bn)

Results Target (% of target) % change

1 Qtr 2 Qtr Jan-Jun 3 Qtr 4 Qtr Year 1 Qtr Jan-Jun Jan-Jun

Income tax 534 503 1,037 428 453 1,918 114 110 41.7

VAT 1,062 1,004 2,066 1,151 1,171 4,389 87 93 15.5

Customs duties 283 330 613 308 339 1,261 94 95 5.5

Excise & other taxes 117 152 269 164 199 631 107 n/a n/a

Total 1,996 1,989 3,985 2,051 2,163 8,198 96 99 20

Note. Payments exclude those made directly to the Treasury.Source: Servicio Nacional Integrado de Administración Aduanera y Tributaria.

Ambitious tax revenuetargets

Production cuts could hitfiscal oil revenue

20 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

Specific fiscal measures will weigh on the deficit this year. The government’sdecision in August to forego a Bs2/litre wholesale tax on gasoline to supportwholesalers, service stations and transportation companies will cost theauthorities Bs30bn in lost tax revenue. The recently announced 10% minimumwage increase will require spending of Bs711bn. Part of this relates to pensionpayments, which are tied to the level of the minimum wage. About one-thirdof those public workers entitled to an earlier announced 10% pay rise are stillawaiting payment.

Total budgetary impact of minimum wage risea

(Bs m)

Wage increases 427,584 Central government 224,105 Decentralised entities 203,478

Pension increasesb 284,002 IVSS 151,610 Other pension regimes 132,392

Total 711,586

a Data includes the National Assembly’s proposal to make the decree retroactive to May 1st.b Pension payments are linked to the minimum wage level.Source: Oficina de Asesoría Económica y Financiera.

Moreover, by the Central Bank’s own admission, public spending is behind target.It is expected to provide a larger boost to growth in the second half of the year,when historically most of the actual money transfers take place. Therefore,spending is likely to rise more rapidly in the second half than in the first half of2001, when the authorities prided themselves in remaining well within theirtargets. Moreover, during the first six months of 2001 off-budgetary spending—inthe form of additional credits from the legislature requested by the executive—appeared subdued. This is, however, an entrenched historical practice. With crimelevels and labour unrest rising and the oil sector struggling, the government couldstill resort to this type of financing in the second half of the year.

After several readings the National Assembly finally approved the new CentralBank Law at the end of August. Although Mr Chávez has claimed that the lawincreases the Central Bank’s autonomy, the opposition has criticised the bill forallowing too much government interference. The bill states that the NationalAssembly can nominate two of the directors on the Bank’s board and thepresident the remaining three members. Directors can only be removed by atwo-thirds majority in the assembly or if they have committed a crime againstthe nation. The Central Bank also has the authority to regulate prices offinancial services and to set interest rates—the only one on the continent withinterest-rate setting powers.

The Central Bank has been forced to intervene in the foreign-exchange markets,selling US dollars to stem the Bolívar’s slide, particularly in May-June, whenrumours that the government was considering both imposing a state ofemergency and applying interest-rate caps fuelled market fears about the possibleimposition of exchange controls. On August 14th it introduced further measures

Unexpected costs to weighon the budget

Central Bank Lawapproved

Central Bank tightensliquidity

Venezuela 21

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

to tighten liquidity and arrest the sliding currency. The ceiling on banks’ netforeign currency holdings was reduced from 15% to 12% of net capital. Themaximum daily variation in banks’ net foreign currency holdings was loweredfrom 15% to 12%. The Central Bank prohibited foreign-exchange operators fromselling foreign currency to companies domiciled outside the country. OnSeptember 10th the Central Bank raised its discount rate from 32% to 37% in afurther attempt to halt currency speculation. A strong exchange rate has been acentral tool in the government’s battle to control inflation. On September 10ththe bolívar stood at Bs746.6:US$1, down by 6.3% in nominal terms since thestart of the year but still up by an estimated 1.8% in real terms.

Meanwhile, capital flight and the related drain of deposits, as well as the newliquidity requirements for banks and the higher discount rate, are generatingupward pressure on interest rates in the marketplace. Overnight rates roseabove 40% in July owing to a liquidity crunch and again in mid-August asbanks scrambled to meet the new liquidity measures. This prompted the largestbanks to raise interest rates on corporate loans by more than 5 percentagepoints in July and August, to more than 25%. This is of particular concernbecause those loans are mostly taken up only by large corporates. Small andmedium-sized enterprises (SMEs) had limited access to funding even before thislatest liquidity crunch tightened conditions further. Liquidity is likely toremain tight as long as it is unclear whether the new measures imposed onbanks are of a temporary or (semi-) permanent nature. The only rate that hasbucked the trend, and one of the most important rates for the retail sector, therate on car loans, has come down from 30% per year to 18-19% per year, owinglargely to government intervention. However, the recent rise in the discountrate is likely to put pressure on car loan rates before long.

After imposing stricter liquidity requirements on the banks the production andtrade minister, Luisa Romero, announced that the government was alsoworking on a package of measures to reduce import spending by at least 20%this year, and more in 2002. The measures are intended to reduce the outflowof capital and boost domestic production. No final details have been releasedyet, but the package could include import restrictions on agricultural goods,shoes and clothing as well as industrial items and car parts. Import restrictions,new quotas, suspensions of existing licences and subsidies are all beingdiscussed, while trade agreements could be revised.

The Ley de Hidrocarburos (Hydrocarbons Law), which is currently under dis-cussion in the National Assembly, will tackle the tax system for the oil sector.At the moment, Venezuela’s government receives 67% income tax on allpetroleum exports and 34% income tax on profits derived from upgrading,offshore gas and boiler fuel Orimulsion projects. The regime of royalties appliesa number of different rates, incentives and discounts according to the type ofactivity or project in question, although in theory royalties are set at 16.7%.Proposals in the new law include a reduction in income tax from 67% to 34%,but an increase in royalties from 16.7% to 30%. This would be one of thehighest levels in any oil-producing country. The rate has triggered oppositionfrom officials, industry experts, and domestic and foreign oil companies alike.

Concern about new law foroil sector

Interest rates rise

Import controls to back upcurrency support

22 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

The government has backed away from privatisation plans for the electricitysector, deciding instead to provide the necessary investment to restructure thecompanies involved. According to the Federación Venezolana de Cámaras yAsociaciones de Comercio y Producción (Fedecámaras, the federation of tradeand industry chambers), the electricity industry will need US$12bn to meet itsten-year projected expansion plan. The government believes that only US$5bnwill be needed to expand and upgrade energy provision, but the CongresoVenezolano de Ingeniería Eléctrica, (CVIE, the electricity industry organisation)has warned that this could result in an energy crisis and pose an additionalthreat to the country’s medium-term prospects. A track record ofunderinvestment in the electricity sector in the past decade has left manygenerators and substations in poor states of repair. An estimated US$330m ininvestment is required in 2001-03 to rehabilitate deteriorating generators andtransmission systems in western states, where poor maintenance and thefailure of installed capacity to keep up with growth in demand has led tofrequent power cuts and recurrent rationing.

The Comisión Nacional de Telecomunicaciones (Conatel, the telecommun-ications regulator), announced a delay in the auction of radio frequencies forhigh-speed telecoms services to the first half of 2002. The regulator cited thedownturn in the global telecoms markets, as a result of which interestedcompanies would not be able to finance investments this year. The auction forthe 11 licences for local multipoint distribution systems (LMDS) will also bepostponed until next year. The auctions in 2000 of 14 fixed-line telephonylicences generated US$20.4m. Third-generation (3G) auctions will not takeplace before late 2002 or early 2003.

The domestic economy

Economic trends

According to preliminary data, GDP expanded by 2.9% year on year in thesecond quarter of 2001. Growth was fuelled by the non-oil sector, whichexpanded by 5.9%; oil-related GDP contracted by 2.3%. GDP growth in thefirst quarter was revised upwards to 3.8%, from 3.5%. This brings first-half GDPgrowth to 3.4%. The non-oil economy—particularly the construction sector,which was up by 20.9% year on year in the second quarter—benefited from arise in government spending. Telecommunications expanded by 12.9%, manu-facturing by 5.3% and commerce by 4.9%. Mining and financial serviceslagged substantially, growing by just 1% and 0.7% respectively.

The growth upturn has been checked by the private sector’s reluctance to raiseinvestment spending. Only the basic consumer goods sectors (food and drinks)and services sectors (telecoms, utilities and banking) have seen an increase ininvestment. The trend was highlighted in a recent survey of 100 companies byan opinion-research firm, Datanalisis, which showed that 40% of companies inVenezuela have frozen their investment plans because of political concerns.

A slow recovery

Private-sector investmentlacking

Cancelled electricity salecould cause energy crisis

Radio frequencies auctiondelayed

Venezuela 23

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

Although there can be little doubt that car sales performed robustly during thefirst half of 2001, this is not necessarily a good indicator of rising consumerconfidence, as conflicting reports show. Rather, the car sale surge is a result ofspecific factors including cheaper car loans and the government’s “family car”programme, which exempts cars bought under the scheme (31% of total salesin July) from the 14.5% value-added tax (VAT). Total car sales rose by 70% yearon year in July, leaving total sales for the first half of 2001 up by 58% year onyear according to the Cámara Automotriz de Venezuela (Cavenez, theVenezuelan Automotive Chamber). Imported vehicles accounted for 40% ofthe total, comparable to 39% in the year-earlier period.

Car sales(units unless otherwise indicated)

Jul Jan-Jun 2000 2001 % change 2000 2001 % change

Domestic cars 6,417 10,524 64 46,163 69,601 51

Imported cars 4,422 7,911 79 28,003 47,334 69

Total 10,839 18,435 70 74,166 116,935 58

Source: Cámara Automotriz de Venezuela.

Two other recent retail sales reports offer conflicting data on the consumermarket. According to the Consejo Nacional del Comercio y los Servicios(Consecomercio, the council for trade and services) retail sales fell by 2.5% inJanuary-June 2001. However, its numbers are boosted by the inclusion of carsales—which rose by 15%, underpinning statements from car dealers—and thetrue state of the retail market is worse than suggested in the figures. Clothing andfootwear sales were the worst hit sectors. According to Consecomercio, amajority of those polled are confident about the outlook for the third quarter.

However, the Central Bank’s inflation-adjusted retail sales records disagree withthis report, showing that overall sales rose by more than 30% year on year inMarch, April and May. However, most of the increase is owing to hardware,construction and machinery sales, with sales in traditional retail sectors (healthand beauty, clothing and food, and beverages and tobacco) lagging. Moreover,many of the products sold are imports.

Mixed retail sales picture

24 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

Retail sales(real % change, year on year)

2000 Jan 2001 May 2001

Food, beverages & tobacco 30 35 15

Clothing 5 17 23

Health & beauty 24 23 1

Hardware 20 34 31

Construction 19 30 36

Transport 36 61 59

Machinery 29 48 68

Household 48 93 64

General index 29 40 33

Source: Banco Central de Venezuela.

Consumer price inflation increased by 0.6% in August, leaving prices up by12.9% year on year. This halted the steady increase in the 12-month inflationrate since April, which reflected large price increases for communications andeducation services and food—owing to a shortage of meat and a prolongeddrought. Officially approved increases for telephone tariffs and matriculationpayments pushed up communications and education prices. Moreover, as thebolívar has weakened in recent months, fears of a devaluation will also haveweighed on prices. Reducing inflation has been one of the government’sprincipal economic achievements to date. In his resolution to keep inflationunder control, the president, Hugo Chávez, announced in May that hewas sticking to a modest 10% rise in public-sector wages in 2001 (seeEconomic policy).

Consumer price inflation(% change; Caracas metropolitan area price index)

2000 2001 Monthly Year on year Cumulative Monthly Year on year Cumulative

Jan 1.7 19.3 1.7 0.9 12.6 0.9

Feb 0.4 17.9 2.1 0.5 12.7 1.4

Mar 0.9 17.5 3.0 0.8 12.5 2.2

Apr 1.5 18.0 4.6 1.1 12.1 3.3

May 1.0 16.9 5.7 1.5 12.6 4.9

Jun 1.1 16.4 6.8 1.0 12.5 5.9

Jul 1.0 15.8 7.9 1.5 13.0 7.5

Aug 0.8 15.0 8.8 0.6 12.9 8.2

Sep 1.7 15.9 10.6 – – –

Oct 0.8 15.1 11.6 – – –

Nov 0.6 14.2 12.3 – – –

Dec 1.0 13.4 13.4 – – –

Source: Banco Central de Venezuela.

Inflation proving slightlystubborn

Venezuela 25

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

Despite improvements, unemployment remains high. According to the OficinaCentral de Estadística e Informática (OCEI, the Central Statistics Office) thelevel of unemployment fell to 13.3% at the end of the second quarter, downfrom 14.2% at the end of the first quarter, but nevertheless up from the 12.1%registered at the end of 2000. Of the total workforce, 52.4% of workers wereemployed in the informal sector, more than 1 percentage point higher than atthe end of the first quarter. The government expects a further fall inunemployment to about 11% by the end of the year.

However, private unemployment estimates have consistently put the level ofunemployment 1-2 percentage points higher than official figures. According toDatanalisis polls, the unemployment rate in July was 14.5%, down from 15%in June. The polls also suggest that about 55% of the workforce is active in theinformal sector—data supported by evidence from the Federación Venezolanade Cámaras y Asociaciones de Comercio y Producción (Fedecámaras, thefederation of trade and industry chambers). The unions, meanwhile, claim thatunemployment exceeds 20% of the active population and that 59% of theworkforce is now in the informal sector.

Onerous labour regulations and an overvalued currency are deterringpotential employers and form a disincentive to some foreign investment. Theonly likely short-term spur to employment growth could be state infra-structure spending. In that light, the government’s national employmentplan, also dubbed the Simon Rodríguez Plan—expected to generate an extra238,838 jobs between July and December 2001, equivalent to a reduction inthe unemployment rate of 2 percentage points—should provide some relief.However, details of this programme are scarce, and given the delaysexperienced in other public projects, employment growth will probably pickup much more slowly than expected.

Oil and gas

The proposed Ley de Hidrocarburos (Hydrocarbons Law) currently under dis-cussion in the National Assembly has been criticised for potentially deterringforeign investment in the sector (see Economic policy). It will confirm thestate’s exclusive ownership rights over Petróleos de Venezuela (PDVSA, thestate-owned oil monopoly) and all its daughter companies. Under the law, theprimary activities of exploration, extraction and storage will be exclusivelyreserved for state-owned enterprises or those companies in which the state is amajority shareholder. Moreover, all these joint ventures will require legislativeapproval and the National Assembly will have the right to modify the venture’sconditions. This will limit the sector’s attractiveness to foreign investors, whoare likely to balk at the idea of financing government-controlled projects. It isnot clear whether the law will apply to existing ventures. Under the law,privately owned companies will be allowed to operate in the refining sector butthe government will have the right to set prices of refined products sold in thedomestic market.

Unemployment declines

Hydrocarbons Law likely tocurb foreign investment

26 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

In the first eight months of 2001 prices for the Venezuelan oil basket of crudesaveraged US$21.9/barrel. As crude oil prices softened in response to weakeningglobal demand, OPEC moved to for the third time this year to cut supplies further.As a result, from September 1st Venezuela’s quota output level is 2.67m barrels/day,down from 2.79m b/d. However, according to the Middle East Economic Survey(MEES), in June Venezuela was producing 2% above its April quota level. Oilproduction accounts for about a one-third of GDP, one-half of government incomeand three-quarters of exports.

PDVSA’s profits dropped to US$980m in the first four months of 2001, fromUS$1.9bn in the year-earlier period. The decline was attributed to a rise ininvestment spending and a new labour contract signed by the former PDVSApresident, Héctor Ciavaldini, in October 2000 which will cost US$4bn in total.The Ministry of Finance has expressed concern that PDVSA’s annual resultscould come in under budget, resulting in lower tax revenue for the govern-ment. According to the current PDVSA president, General GuaicaipuroLameda, expenditure rose by 30% and investments increased by 50% year onyear in the first half of 2001. However, he did not add that investment levelswere still below planned budget levels. At the company’s annual assembly inDecember 2000 an investment budget of Bs4.2trn (US$5.8bn) and a spendingbudget of Bs5.2trn were approved.

PDVSA profits down

Production cuts bite

Venezuela 27

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001

Texaco (US) announced at the end of June that nearly US$1.1bn in financinghad been raised by the partners in the Hamaca project, an ambitious heavycrude production and upgrading operation in the Orinoco Belt. Texaco andPDVSA each have a 30% stake in the project, while Phillips Petroleum (US)owns the remaining 40%. The field is estimated to contain over 30bn barrels ofoil, of which 2.1bn could be recoverable during the project’s 34-yearproduction life—generating about 190,000 barrels/day of extra-heavy 8.6degree API crude. The crude will be upgraded into 180,000 b/d of 26-degree APIcrude for sale in the international markets.

The government has finally awarded development and exploration licences forthe Yucal Placer gas fields to an international consortium. TotalFinaElf leadsthe consortium with a stake of 69.5%, followed by Repsol YPF (15%) and twoVenezuelan partners, Inepetrol and Otepi (with 10.2% and 5.3% respectively).The field is expected to produce some 300m cu ft/day of gas by 2007. Thecompanies involved are studying investments approximating US$380m overthe next three years.

Industry

Production trends in individual sectors varied widely in the first five monthsof 2001. Aluminium output suffered from a two-day walkout in June byworkers demanding higher salaries and improved social benefits. Productionof crude oil and oil derivatives is also in decline, as is that of steel andcement, although monthly growth rates vary widely for the last two sectors.Production of iron ore, electricity, sugar and fertilisers is struggling as a resultof structural problems.

La Siderúrgica de Orinoco de Venezuela (Sidor) is expecting to sell 3m tonnesof steel by the end of the year, a historical record for the company and abovethe 2.8m tonnes sold in 2000. The company envisages further growth in 2002.Although upgrading its production sites will enable the company to increasesupply—it is investing US$90m this year and US$80m next year—its optimisticforecasts could be hampered by the slowdown in global demand. The companyis Venezuela’s largest private exporter and relies heavily on foreign demand. Aslight recovery of steel prices will, however, support the company’s revenue.The Economist Intelligence Unit expects steel prices to drop from an averageUS$344.8/tonne in 2000 to US$276.1/tonne this year, but is forecasting a riseto US$291/tonne in 2002.

Physical production trends in key sectors, 2001(% change, year on year)

Crude Oil derivatives Iron ore Steel Aluminium Cement Electricity Sugar Fertilisers

Jan 6.8 7.0 7.6 25.1 9.3 –16.1 8.8 –2.0 –50.4

Feb 2.5 2.0 –28.9 –1.4 –0.9 –6.9 0.6 –30.3 –54.1

Mar 3.9 –0.1 –7.2 13.3 0.9 16.3 8.5 –31.0 –20.1

Apr 1.3 –7.4 1.7 14.7 5.2 19.3 6.9 –43.2 –15.1

May –0.4 –1.8 3.8 –58.4 –13.7 –11.1 3.1 –66.3 –35.6

Source: Banco Central de Venezuela.

Good news for Hamaca andYucal projects

Industrial productionvaries widely across sectors

Sidor paints a positivepicture

28 Venezuela

EIU Country Report September 2001 © The Economist Intelligence Unit Limited 2001