workshop - regular council - oct 17 2019

TRANSCRIPT

AGENDA

Regular Council Meeting Meeting

Thursday, October 17, 2019 @ 5:30 PM

Council Chambers

Welcome to the City of Victoria Council Meeting. All information regarding the meeting process can be found by the front entrance.

Page

1. CALL TO ORDER

2. AGENDA ITEM

2.1.

Local Options Sales Tax

Staff Report, Local Option Sales Tax Public Input

10/14/2019 Staff Report

Slide deck from 10/14/19

White Paper: Local Option Sales Tax

2 - 85

3. ADJOURNMENT

Page 1 of 85

Request for Council Action Meeting Date: October 17, 2019 Subject: Local Option Sales Tax Public Input Staff Contact/Department: Dana Hardie/Administration Trisha Pollock/Finance Background: The City of Victoria is exploring potential implementation of a general local option sales tax as a potential funding source for parking solutions in the city’s vibrant downtown area or as a funding source for other large capital project(s). At the October 14, 2019 Council Workshop, staff presented an informational overview of local option sales tax to:

• inform the city council on general local option sales tax; • identify what cities currently impose a general local option sales tax on; • define the steps the city would need to take to implement a local option sales tax; • provide data on the estimated impact in Victoria should a local option sales tax be

imposed; and • examine the pros and cons of general local option sales tax in the community.

This meeting is the second of a three-part process to inform the council’s discussion on the topic. The three-part process includes:

1. Informational overview/presentation of white paper (Oct. 14, 2019) 2. Public comment – residents and businesses (Oct. 17, 2019) 3. Council dialogue and policy decision (Tentatively scheduled for December 16, 2019)

The October 17, 2019 meeting is a listening session and is an opportunity for businesses, residents, even visitors, to provide input and feedback on local option sales tax to the council. Commission/Committee/Citizen Comments: N/A Financial Impact: N/A Legal Review: N/A Recommendation: N/A Documents Attached: 1. October 14, 2019 staff report 2. Slide deck from Oct. 14, 2019 council workshop 3. White Paper: Local Option Sales Tax – A Comprehensive Overview for the City of Victoria

Proposed Motion: No action is requested.

Page 2 of 85

Request for Council Action Meeting Date: October 14, 2019 Subject: Local Option Sales Tax – Informational Overview Staff Contact/Department: Dana Hardie/Administration Trisha Pollock/Finance Background: The City of Victoria is exploring potential implementation of a general local option sales tax as a potential funding source for parking solutions in the city’s vibrant downtown area. To determine whether local option sales tax would be a reasonable public policy for the city, staff will present information to:

• inform the city council on general local option sales tax; • identify what cities currently impose a general local option sales tax; • define the steps the city would need to take to implement a local option sales tax; • provide data on the estimated impact in Victoria should a local option sales tax be imposed; and • examine the pros and cons of general local option sales tax in the community.

This workshop is the first of a three-part process to inform the council’s discussion on the topic. The three-part process includes:

1. Informational overview/presentation of white paper (Oct. 14, 2019) 2. Public comment – residents and businesses (Oct. 17, 2019) 3. Council dialogue and policy decision (Tentatively scheduled for December 16, 2019)

The Issue Over the years, the city council has been working with property owners, business owners and community members to identify potential solutions to help alleviate the parking issues. In 2018, the city council authorized a parking study which included resident and feedback input. In 2019, the city purchased and installed public parking signs throughout downtown and parking wayfinding signs off Hwy 5. Several business owners collaborated to offer valet parking service (which has since ceased). The city’s 2020 budget includes funding to hire a consultant to evaluate and make recommendations on the city’s parking-related ordinances and to accelerate the demolition of the city’s old public works facility to redevelop the site into a parking lot. There has also been discussion over the years on whether the city should build a parking structure. To date, however, there has not been consensus on how to move forward or how to fund the structure. To further assist council in understanding what tools beyond increasing the property tax levy are available to fund potential parking solutions or other capital projects, the city council is exploring implementation of a general local sales tax.

Proposed Motion: This is an informational item only.

Page 3 of 85

What is Local Option Sales Tax A local sales tax is an additional tax on sales. Local option sales tax is not imposed in all communities. Cities must gain special legislation and obtain voter approval to impose a local option sales tax. It is taxed at a different, lesser rate (generally between 0.25 percent and 1.00 percent). When it does apply, the local sales tax is in addition to the 6.875 percent state sales tax. It is applied to the same tax base with the same exemptions as the state sales tax. Likewise, a local use tax is required in all jurisdictions with a local sales tax. This has been in effect since Jan. 1, 2000 (M.S. 297A.99, subd. 6). A local use tax is collected on purchases that are taxable but were not taxed at the local sales tax rate. A use tax removes any disadvantage local businesses may suffer to competitors located outside the taxing area and not required to collect local taxes. One significant advantage of a local option sales tax is that the sales tax base is larger than the property tax base as it includes non-resident shoppers such as commuters and leisure visitors and tourists.

Legislation passed in 1971 prohibits cities from imposing any new tax or increasing local taxes on sales or income (M.S. 477A.016). The idea behind this restrictive law addressed legislator concerns that granting broad authority could result in the creation of “winners and losers” which could unintentionally open the door to increased aid or new equalization formulas. It also risks introduction of a “creep” effect that could lead to broad, general use of sales tax as a replacement of or to offset property taxes – something in which the legislature does not currently have the appetite to explore.

Over the years, there have been changes to the statutes governing local option sales tax. The most recent legislative change occurred in the 2019 legislative session. Today, before enacting a local option sales tax, cities must seek special legislation and then hold a voter referendum. (M.S. 297A.99 subd. 3). Seeking special legislation to enact a local option sales tax does not guarantee legislative approval. There is a lack of clear approval criteria in state statutes. Through the years, some proposals have received the necessary legislative authorization and some have not. Communities not granted legislative approval are left in the dark without guidance as to why or what did not meet the legislature’s approval.

Implementing Local Sales and Use Tax The process for implementing a local option sales tax is prescriptive. The city council must adopt a resolution indicating a desire to propose a local option sales tax for and must request special legislation by Jan. 31 of the year the city will seek special legislation. If a city is granted special legislation, residents must then vote to approve the tax in the next general election. If passed by a majority of the voters, the tax revenue can only be used for the specified project or improvements that were approved by the voters before the local option sales tax can be enacted. The specific steps outlined in state statute for implementing local sales and use tax follow:

Page 4 of 85

Statutory Language Statutory Reference

Adopt a resolution prior to the legislative request that includes: • Proposed tax rate • Amount of revenue anticipated for each project (up to 5) • Description of how the revenues will be used • Documentation of regional significance of project • Total revenue anticipated to be raised before tax expires • Duration of the tax

M.S. 297A.99, subds. 2, and 3(b) and (c)

Request special legislation that authorizes imposition of the tax (by January 31 of the year seeking special legislation)

M.S. 297A.99, subd. 3

Gain voter approval at a general election within 2 years after the special legislation is granted

M.S. 297A.99, subd. 3 (a)

File local approval with the Secretary of State before the start of the next legislative session

Pass an Ordinance imposing the tax

Inform the Commissioner of Revenue at least 90 days before the first day the tax will be imposed

M.S. 297A.99, subd. 12(b)

Display on the City’s website homepage a notification that residents and businesses may owe a local use tax on purchases of goods and services made outside of the city limits

M.S. 297A.99 subd. 12a

Send an annual notice in the water utility billing statement that residents and businesses may owe local use tax on purchases of goods and services made outside of the city limits

M.S. 297A.99 subd. 12a

The Current Landscape – Local Sales and Use Tax As of Jan. 1, 2019, 35 cities and three counties have imposed a general local option sales tax. Effective Oct. 1, 2019, nine new cities started collecting a local option sales tax. With the exception of Minneapolis and St. Paul, three cities (Elk River, Excelsior and Rogers) are the first cities in seven-county Twin Cities metropolitan area to impose a local option sales tax. Additionally, a fourth city, West St. Paul, will begin collecting a local option sales tax on January 1, 2020.

The types of projects local options sales tax revenue are funding throughout the state follow:

Page 5 of 85

Type of Projects Number of Cities Lake, water quality or shoreline improvements 3 Flood mitigation 2 Sewer, water infrastructure improvements 8 City facilities (rec center, fire/police station, city hall municipal airport, library, community center, or land)

18

Trail – new, connections, crossings 6 Park improvements (picnic shelters, bandshell, fishing pier, athletic field, pools, restrooms)

10

Roads 5 General economic development (neighborhoods, early educations centers, cultural economic development)

3

A summary of the projects that the four metro cities will use local option sales tax revenue to fund follow:

Elk River – 0.50% ($35 million)

• Recreational facility (ice arena, community activity space, turf field house) • Senior center facility improvements • Park facility improvements (athletic fields, picnic pavilion) • Dredging of Lake Orono • Citywide trail connections

Excelsior – 0.50% ($7 million)

• Funding source for the parks master plan include: o Parking o Park facilities (picnic pavilions, equipment rentals, restrooms, bandshell) o Playground equipment upgrades o Shoreline improvements o Enhanced neighborhood entries o Tree preservation o Boardwalk and trail connections

Rogers – 0.25% ($16.5 million)

• New trails and trail and pedestrian crossings and connections • Splash pad and school/community pool • Site improvements for future recreation facilities

West St. Paul – 0.5% ($28 million)

• Infrastructure

Page 6 of 85

Potential Impact of Local Sales and Use Tax in Victoria While state statute doesn’t restrict the tax rate, cities must specify the desired local tax rate that will be imposed in the special legislation request (M.S. 297A.99 subd. 5). Typically, local option sales tax rates are either 0.25, 0.50, or 1.00 percent. Of the local tax rates currently imposed 93 percent of the cities are 0.50 percent.

In looking at the latest available taxable sales data for the city, total taxable sales in Victoria averaged $27.6 million in from 2013-2017 (Minnesota Department of Revenue Tax Research Division). Based on this data, the chart that follows compares potential sales tax revenue to the additional property tax levy increase that would be needed to raise the same amount of revenue. Additional analysis would need to be done to determine how much of the sales tax burden is exported to non-residents and further breakdown of distribution burden.

Tax Rate Estimated Revenue Equivalent Property Tax Levy Increase in 2020

0.25% $69,000 1.32%

0.50% $138,000 2.64%

1.00% $276,000 5.29%

Commission/Committee/Citizen Comments: The public is invited to provide input/comment on local option sales tax at a special meeting of the council scheduled for Oct. 17, 2019 at 5:30pm Financial Impact: There is no financial impact at this time. Should the city seek special legislation and voter approval for enacting a local option sales tax, there are implementation costs. Staff estimate the cost to implement a local option sales tax in Victoria to range from $6,500 to $11,500 in an election year to $44,000 in a non-election year. The breakdown follows:

Activity Estimated Cost – Election Year

Estimated Cost - Non-Election Year

Referendum Expense at General Election $1,500 $30,000- 35,000

Drafting of Legislative Proposal & Lobbying Efforts $5,000 - $10,000 $5,000 - $10,000

TOTAL $6,500 - $11,500 $35,000 - $45,000

Page 7 of 85

Legal Review: N/A Recommendation: No action is being requested this evening. Staff will present an in-depth overview of local option sales tax at the workshop including current uses, how its evolved, the process for enacting a local option sales tax, common questions, and pros and cons of imposing local option sales tax. A detailed white paper is attached to this staff report with additional information.

Staff, however, recommend council hold a a special meeting of the council (currently scheduled for Oct. 17 at 5:30pm) to receive input and comment from businesses and residents. Staff also recommend that council hold a workshop on Dec. 16 at 5pm for a policy discussion and staff direction related to local option sales tax. Documents Attached:

1. White Paper – Local Option Sales Tax: A Comprehensive Overview for the City of Victoria

Page 8 of 85

FR Local Option Sales TaxC i t y C o u n c i l Wo r k s h o pO c t o b e r 1 4 , 2 0 1 9

Page 9 of 85

Agenda

2

• What is local option sales tax

• Cities with local option sales tax

• Process to enact a local option sales tax

• Potential impact of local option sales tax

• Pros and Cons of local option sales tax

www.ci.victoria.mn.us

Page 10 of 85

What is the Issue?

• Limited ability for cities to raise revenue

• Challenging to prioritize city services

• Investment in capital for growing city

www.ci.victoria.mn.us 3

Page 11 of 85

The Process

1. Learn• Overview

www.ci.victoria.mn.us 4

2. Listen 3. Discuss• Public Comment

• Businesses

• Residents

• Council Dialogue

• Policy Direction

Page 12 of 85

Local Option Sales Tax1 0 1

Page 13 of 85

Understanding General & Local Sales Tax

• Tax paid by the consumer at the time of purchase

• Revenue collected is submitted by the retailer to the state

www.ci.victoria.mn.us 6

Page 14 of 85

Understanding Local Option Sales Tax

Applies to:

• Retail sales of taxable service

• Tangible personal property made in Minnesota

Retail sale:

• Any sale, lease or rental of tangible personal property for any purpose other than resale, sublease or sub-rent

• Services for any purpose other than resale

www.ci.victoria.mn.us 7

Page 15 of 85

www.ci.victoria.mn.us 8

General State Sales Tax

General sales tax rate in Minnesota

• 6.875%

• Some special rates

Current sales tax rate in Victoria

• 7.375% (0.5% County Transit Tax)

Total sales and use tax revenue – FY2019

• Estimated $7.0 billion

Total taxable sales in Victoria

• Approximately $27.6 million

Page 16 of 85

Taxable Items

• Retail sales

• Most admission and amusement fees

• Building materials, supplies, equipment

• Cable TV services

• Candy and soft drinks

• Computer software

• Delivery charges

• Drugs (most over the counter)

• Fabrication and installation labor

• Lodging

www.ci.victoria.mn.us 9

• Machinery, equipment and tools

• Appliances

• Furniture and fixtures

• Meals and drinks

• Motor vehicles, leases and rentals*

• Utilities

• Vending machine sales

• Some services (building, cleaning, laundry, lawn care, towing, pet care)

*motor vehicle sales are exempt for local sales tax

Page 17 of 85

State Sales Tax Exemption Examples

Groceries: Exempt

www.ci.victoria.mn.us 10

Clothing: Exempt Prescription Drugs: Exempt

$100.00 Groceries

$0.00 Sales Tax

$100.00 Total

$100.00 Clothing

$0.00 Sales Tax

$100.00 Total

$100.00 Prescription Medication

$0.00 Sales Tax

$100.00 Total

Page 18 of 85

What is a Local Sales Tax

• Defined in M.S. 297A.99

• Not levied in all local municipalities

• A sales tax at the time of purchase on the same goods and services as state sales tax

• In addition to the 6.875% state sales tax

• Local sales tax rate is generally less than state rate

www.ci.victoria.mn.us 11

Shop Local.

Eat Local.

Spend Local.

Enjoy Local.Page 19 of 85

Calculating Local Sales Tax

www.ci.victoria.mn.us 12

City of Victoria Hypothetical Example:

6.875% State Sales Tax Rate+ 0.500% County Transit Tax+ 0.500% City General Local

7.875% Total Combined

City of Victoria Current Tax Rate:

6.875% State Sales Tax Rate+ 0.500% County Transit Tax

7.375% Total Combined

Page 20 of 85

State Sales Tax Example

Consumer Products: 6.875% Sales Tax + 0.50% County Transit + 0.50% Local Tax

www.ci.victoria.mn.us 13

$100.00 Consumer Products$6.88 State Sales Tax

$1.00 Local Sales Tax$107.88

Page 21 of 85

Sales Tax Rate Calculatorhttp://www.revenue.state.mn.us/businesses/sut/Pages/SalesTaxCalculator.aspx

www.ci.victoria.mn.us 14

Page 22 of 85

When is Local Sales Tax Paid?

State and local sales taxes are due.

www.ci.victoria.mn.us 15

A contractor buys and pick up materials in a city with local sales tax for use in an area without a local tax.

• Since materials are pick up in the city with a local sales tax, that city’s local sales tax applies.

• If the materials are delivered by the seller to the construction site, no local tax is due.

Page 23 of 85

When is Local Sales Tax Paid?

• City has a local sales tax.

• Seller lives outside of the city.

• Seller charges state and local tax.

www.ci.victoria.mn.us16

Page 24 of 85

What is a Local Use Tax?

Local use tax is collected on purchases that are taxable but were not taxed at the local sales tax rate

• Same tax rate applies

www.ci.victoria.mn.us 17

Page 25 of 85

Use Tax Example

www.ci.victoria.mn.us

You buy a taxable item online and the seller does not collect tax from you.

18

Page 26 of 85

General Minnesota Use Tax

How do you know you owe and how do you pay a use tax?

• Self assessed, paid by consumer directly to the State

• Individuals exempt from first $770 of use tax

• Cities required to notify public and provide information or links for paying the tax (M.S. 297A.99, subds. 6, 8, and 12a)

• Cities required to pos on main page of website

www.ci.victoria.mn.us 19

Page 27 of 85

Historical Timeline

www.ci.victoria.mn.us 20

Legislature prohibits cities from imposing

local sales tax

1971 1997

Legislature authorizes local

sales tax through special legislation

2008

Counties granted statutory authority

to impose local sales tax to fund

transportation

Carver County imposes 0.5% local

transit tax

2017Page 28 of 85

Types of Sales and Use TaxesTYPE OF SALES AND USE

TAX% AUTHORIZED RESTRICTIONS STATUTE

GENERAL LOCAL Up to 1.00%Specific capital improvement w/regional

benefit297A.99

SPECIAL PURPOSE

Lodging Up to 3.00% Tourism promotion 469.190

Lodging >3.00% Other than tourism promotion469.190297A.61

Entertainment 297A.61

Food & Beverage Up to 1.00% 297A.61

LOCAL TRANSPORTATIONUp to 0.50%

+ $20.00 excise tax

Tax on commercial sales of motor vehicles to fund transportation/transit project(s); transit

operations or safe routes to schools297A.993

www.ci.victoria.mn.us21

Page 29 of 85

Sales & Use Tax By the Numbers

Local Sales & Use Tax Status Cities Counties

Sales & Use Taxes Imposed 44 3

NEW Sales & Use Taxes (Effective Oct. 1, 2019) 9 0

Sales & Use Taxes Expired 3 0

Sales & Use Taxes Authorized but Not Imposed 1 2

www.ci.victoria.mn.us22

Page 30 of 85

Metro Cities – Types of Projects

Elk River – 0.50%

• Recreational facilities (ice arena, community activity space, turf field house)

• Senior center facility improvements

• Park facility improvements (athletic fields, picnic pavilion)

• Dredging of Lake Orono

• Citywide trail connections

www.ci.victoria.mn.us 23

Page 31 of 85

Metro Cities – Types of Projects

Excelsior– 0.50%

Revenue will fund $7 million of $20 million of improvements identified in the parks master plan such as:

• Parking

• New or improvements to park facilities (picnic pavilion, equipment rental shelter, restrooms, bandshell)

• Upgrades to existing playground equipment

• Shoreline improvements

• Enhanced neighborhood entries

• Tree preservation

• Boardwalk and trail connections

www.ci.victoria.mn.us 24

Page 32 of 85

Metro Cities – Types of Projects

Rogers– 0.25%

• New trails

• Trail and pedestrian crossings and connections

• Splash pad, community/school pool

• Site improvements for future recreational facilities

www.ci.victoria.mn.us 25

Page 33 of 85

Metro Cities – Types of Projects

West St. Paul – 0.50%

• Infrastructure

www.ci.victoria.mn.us 26

Page 34 of 85

Local Option Sales Taxes Imposed -Most Common Uses

27

• Public facilities construction or improvements

• Parks and trails construction or improvements

• Infrastructure

www.ci.victoria.mn.us

Page 35 of 85

Sales & Use Tax Types of ProjectsTypes of Projects Cities

City facilities Ex. rec/community center, city hall, airport, fire/police station, library, land

18

ParksEx. Picnic shelter, bandshell, fishing pier, athletic field, splash pad, pool, restrooms

10

Sewer, water infrastructure 8

Trails – new, connections, crossings 6

Street Infrastructure (including parking) 6

General economic developmentEx. Neighborhood improvements, cultural center, early education center

3

Lake, water quality, shoreline improvements 3

Flood mitigation 2

www.ci.victoria.mn.us28

Page 36 of 85

Victoria– Potential Projects

• Public parking facility – downtown Victoria

• Future parks

• Trail connections

• Future fire station land purchase

• Future water treatment plant land purchase and construction

• Dredging of water bodies

• Buckthorn removal program

• Water quality improvement programs – removing water bodies off the impaired waters list

• City-owned fiber to industrial area (CR10/CR11)

• Other?

www.ci.victoria.mn.us 29

Page 37 of 85

Estimated Revenue from General Local Option Sales Tax in Victoria

Average total taxable sales in Victoria 2013-2017:

$27,609,295

www.ci.victoria.mn.us 30

Tax Rate Estimated RevenueEquivalent % Levy

Increase (2020 budget)

0.25% $69,023 1.3%

0.50% $138,046 2.6%

1.00% $276,093 3.3%

Page 38 of 85

Tax Paid on Hypothetical Purchase

www.ci.victoria.mn.us 31

Purchase Amount7.375% Tax Rate

(Current Victoria Rate)7.875%

(0.50% LOST)Dif.

Current to 0.5%

8.375%(1.00% LOST)

Dif.Current to 1.00%

$25.00 $1.84 $1.97 $0.13 $2.09 $0.25

$50.00 $3.69 $3.94 $0.25 $4.19 $0.50

$100.00 $7.38 $7.88 $0.50 $8.38 $1.00

Page 39 of 85

Steps to Enact Local Option Sales Tax

1. Pass a resolution

• Proposed tax rate

• Description of how revenue will be used (up to 5 projects)

• Amount of revenue - each project

• Regional significance of each project

• Total revenue anticipated before expiration

• Anticipated duration of the tax

www.ci.victoria.mn.us

32

Page 40 of 85

Steps to Enact Local Option Sales Tax

2. Obtain special legislation that authorizes the tax

www.ci.victoria.mn.us 33

Page 41 of 85

Steps to Enact Local Option Sales Tax

3. Gain voter approval

• At a general election

• Within 2 years of legislative approval

www.ci.victoria.mn.us 34

Page 42 of 85

Process for Victoria

• Adopt a resolution supporting local option sales tax and its purpose by Jan. 27, 2020

• Request special legislation before Jan. 31, 2020

• Lobby for special legislation during the session (February – May 2020)

• Seek voter approval at 2020 general election via referendum

• Pass an ordinance imposing the tax

• File local approval with the Secretary of State before start of 2021 legislative session

• Inform the Commissioner of Revenue at least 90 days before the first day the tax will be imposed

www.ci.victoria.mn.us 35

Page 43 of 85

Estimated Costs for Implementation

ActivityEstimated Cost –

Election YearEstimated Cost –

Non-Election Year

Additional Referendum Expense at General Election $1,500 $30,000 - $35,000

Drafting of Legislative Proposal & Lobbying Efforts $5,000 - $10,000 $5,000 - $10,000

TOTAL $6,500 - $11,500 $35,000 - $45,000

www.ci.victoria.mn.us36

Page 44 of 85

Post-Authorization Steps

• Provide annual notification of use tax in utility bill

• Display public information on local option sales and use tax in website

• Provide links to forms for filing use tax

www.ci.victoria.mn.us 37

Page 45 of 85

State Statute Limits Communication to the Public

www.ci.victoria.mn.us 38

2011

Cities may hold referenda to impose

local option sales tax

2013

Cities can expend funds to provide public w/certain facts about local

option sales tax, and host public forums

M.S. 297A.99, subd. 1, para. (d)

Cities may not advertise, promote,

expend funds to support local option

sales tax

2008Page 46 of 85

Local Option Sales Tax in Victoria

• Why is the tax needed?

• How do I collect (businesses) or pay (residents) the local sales tax?

• What are the revenues funding?

www.ci.victoria.mn.us 39

What the Public May Want to Know

Page 47 of 85

Local Option Sales Tax - Pros

• Everyone pays

• Improves accountability

• Provides more fiscal flexibility

• May improve economic vitality

www.ci.victoria.mn.us 40

Page 48 of 85

Local Option Sales Tax - Cons

• A tax is a tax

• Time and costs to implement

• Public perception of being taxed

• Uncertainty

• Lack of clear, objective criteria for approval

www.ci.victoria.mn.us 41

Page 49 of 85

Local Option Sales Tax - Cons

• Additional reporting for businesses and individuals

• Not deductible on federal income tax returns

• Potential harmful competition between local governments

• Inherently volatile revenue source

www.ci.victoria.mn.us 42

Page 50 of 85

Bits & Bobs

Page 51 of 85

Minnesota Tax Incidence Study

• Both mildly regressive

• Sales tax slightly more regressive

• Higher incomes spend less of their income on items subject to sales tax

www.ci.victoria.mn.us 44

Measured the progressiveness of property tax compared to sales tax

Page 52 of 85

Research – Common Themes

• Use on critical projects where property taxes are insufficient and the project would not otherwise be accomplished

• Projects have regional benefit (now required)

• Broad authority maty create “winners and losers” and result in increased aid or new equalization formulas

www.ci.victoria.mn.us 45

Local option sales tax plays a valuable but supporting role in the larger picture of state and local government financing

Page 53 of 85

www.ci.victoria.mn.us 46

Next Steps

Thursday, October 17, 2019

Public comment

Monday, December 16, 2019 Council policy discussion and staff direction

Monday, January 27, 2020Last day to pass a resolution for 2020 consideration

Page 54 of 85

Questions?

Page 55 of 85

State Sales Tax ExampleConsumer Products: Sale Subject to 6.875% Sales Tax

www.ci.victoria.mn.us 48

$100.00 Consumer Products$6.88 State Sales Tax$106.88

Page 56 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

City of Victoria 10/14/19 City Council Workshop

Page 57 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 1 of 28

Contents Section I: Introduction .................................................................................................................... 2

Section II: Background & Overview .............................................................................................. 3

Section III: Sales and Use Tax in Minnesota .................................................................................. 7

Section IV: Local Option Sales and Use Tax in Minnesota ........................................................... 9

Section V: Common Questions – Local Sales and Use Tax ......................................................... 18

Section VI: Pros and Cons of Imposing Local Sales and Use Tax ............................................... 19

Section VII: Conclusion ................................................................................................................ 22

Section VIII: Next Steps ............................................................................................................... 23

Works Cited .................................................................................................................................. 25

Page 58 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 2 of 28

Section I: Introduction Cities continue to face financial challenges to fund services and meet the needs and expectations of the community. Residents and non-residents depend on services such as public safety and other city services such as safe drinking water, sewage treatment, modern roadways, and park and recreation amenities to live and do business in the city. The costs of delivering such services to the public not only continue to increase, but also outpace inflation. As such, cities like Victoria are finding it more challenging to cover these increasing costs with current revenue sources. Recognizing that no one answer will alleviate the financial challenges cities face today, Victoria’s city council is exploring a general local option sales tax as a potential funding strategy for implementing parking solutions in the city’s vibrant downtown area which is the city’s current economic/commerce center. Having ample parking while maintaining the urban design and walkability of the downtown area could encourage and stimulate new economic development, attract investment, diversify the economic base with new opportunities for the community and the surrounding area, and encourage greater use of the downtown amenities by residents and visitors. The purpose of this comprehensive overview is to better inform the council and the public on local options sales tax so the council can determine whether local option sales tax would be a reasonable public policy for the city. Goals are to:

• inform the city council on general local option sales tax; • present information on cities that currently have imposed a general local option sales tax; • identify the steps the city would need to take to implement a local option sales tax; • provide data on the estimated impact in Victoria should a local option sales tax be

imposed; and • examine the pros and cons of general local option sales tax in the community.

This overview is the first of a three-part process to inform the council’s discussion on the topic. The three-part process includes:

1. Comprehensive informational overview (Oct. 14, 2019) 2. Public comment – residents and businesses (Oct. 17, 2019) 3. Council dialogue and policy decision (December 16, 2019)

Information on local sales and use tax was compiled from various professional journals, published reports, the Minnesota Department of Revenue, Minnesota State Statutes, the Minnesota House of Representatives House Research (House Research), various city ordinances and resolutions and council agendas and minutes.

Page 59 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 3 of 28

Section II: Background & Overview Balancing Needs and Costs Cities need revenue to provide services to their residents and businesses, and public officials are challenged to find ways to provide those services in a cost-effective manner. Like other cities, as the “cost of doing business” continues to rise, and the demand and expectation for service continues to increase, it is almost certain that Victoria will need to increase revenues in excess of the rate of inflation to maintain current levels of service as the city continues to grow. Minnesota statutes, however, limit the ability of cities to raise revenues. Funding sources such as state and federal aid, which help offset costs of providing various services, are becoming less dependable or in some cases eliminated altogether. In addition, artificial limitations on revenues such as levy limits or proposals to restrict fees also make it difficult for cities to recover costs. These trends in addition to the public’s general dissatisfaction with being taxed, have created a delicate balancing act driving city leaders to find the most cost-effective way to deliver services. Subsequently, cities have only two options; look to cut services or increase revenues. Current Revenues for the City of Victoria City revenues generally fall into one of three main categories: taxes, assessments, and fees and charges (Grundhoefer, October 2008). In Victoria, property taxes make up more than 80 percent of revenues. In 2019, the city levied $5.2 million in property taxes to fund general operations, capital improvements, and debt service. As a growing community with significant green field space (i.e. open space ready for development), the city’s property tax base continues to increase. In June 2019, the city council adopted its 2019-2020 Strategic Plan which included four strategic objectives. One of those objectives is to expand and enhance the local economy (City of Victoria, 2019). To that end, the council recognizes that initiatives and development that expand the tax base can provide long-term relief to existing taxpayers. For 2020, it is estimated that of the 13.1% percent total preliminary city and Economic Development Authority (EDA) levy increase, new construction will account for 43 percent of the increase leaving the existing tax base to absorb the balance of 57 percent. Cities, like Victoria, also use special assessments to finance different types of local improvements and to recover the costs of services or unpaid charges. Special assessments are charges that are imposed on properties for a specific improvement that benefits the specific property, or for certain services that were provided for and directly benefit the property owner.

Did You Know?

How residents rate their overall quality of life is an indicator on the overall health of a community… 94 percent of Victoria residents responding to a 2018 city survey rated Victoria as an excellent or good place to live. Nearly three quarters of residents felt the general value of city services was either excellent or good. (Victoria, MN Community Livability Report, 2018).

Page 60 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 4 of 28

These special assessments appear on the property tax bill. The authority for cities to impose special assessments is found in Minnesota Statutes (M.S.) Chapter 429. Common examples of special assessments include: construction or improvements to streets or sidewalks, nuisance abatements, and unpaid utility bills. In 2019, Victoria assessed $654,306. Cities also generate revenue by charging fees to provide services that benefit direct users of those services. The concept of fees and charges is that people benefiting from a particular service should bear the cost of providing that service. Examples include charging for the use of a park shelter or community room rental or charging a homeowner a permit fee for building an addition on his or her home. It is important to note that with the exception of specific fees allowed by state statutes, revenue raised through fees and charges only covers the cost of the service provided. It does not serve as a general source of funding for non-fee related services. In the City of Victoria, fees and charges account for 18 percent of the city’s revenue. While Minnesota Statutes limit the authority of cities to raise revenue, cities do have certain authorities to diversify how revenue is raised beyond property taxes, special assessments and fees and charges. For example, cities have authority to enter into franchise agreements with gas, electric, and cable television companies to charge utility franchise fees. Victoria has a cable franchise with Mediacom and through that franchise collects a cable franchise fee from cable subscribers. The city currently collects $1.29 per cable subscriber per month in cable franchise fee revenue. In 2016, the council also authorized utility franchise fees on electric and gas utility bills for both residential and commercial properties in the community. Of the 853 cities in Minnesota, 357 cities have implemented utility franchise fees. Additionally, 101 cities in the seven-county Twin Cities metropolitan area currently have franchise fees. While there is no cap on the fee rate and the fees collected can be used for any public purpose, many cities dedicate franchise fee revenue for a specific purpose such as: capital improvements, road maintenance, parks, sidewalks or trails (M.S. 216.36). In 2018, the City of Victoria collected $296,000 in utility franchise fee revenue. Victoria currently dedicates the utility franchise fee revenue to paying the bonds for utility undergrounding projects. For transparency purposes, all franchise fee revenue collected goes directly into this fund. Additionally, any city has authority to levy a lodging tax to market their community for tourism purposes. There are currently no lodging facilities in Victoria. Cities may also be granted special legislation to levy local option sales tax in their communities. The Current Challenge Downtown Victoria is comprised of restaurant, entertainment, retail, office, residential and other commercial uses. Even though 50 percent of the downtown’s land coverage is dedicated to parking or street rights-of-way, at times, parking can be challenging. A recent parking study reported that there are 445 parking spaces (on- and off-street) in downtown Victoria for both public and private use. Of these spaces, 68% (301 spaces) are for public use and 32% (144) are for private use (i.e. post office or bank customers, residents of The Flats) (Hoisington Koegler

Page 61 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 5 of 28

Group, February 2019). Parking challenges are most evident during evening and weekend hours with the city’s many recreational, entertainment and restaurant options. The study, however, concluded that the data does not support a need for additional parking as a modest level of parking is available during the evening hours and substantial amount of parking is available during the morning and afternoon hours. The study suggested that the city explore other parking solutions before adding supply (Hoisington Koegler Group, February 2019). To that end, the city has been working to implement solutions to help alleviate the parking challenges. In spring 2019, the city purchased and installed public parking signs throughout downtown and parking wayfinding signs off of Hwy 5. Several business owners also coordinated and paid for valet service for all downtown patrons. Unfortunately, low usage ended the service by summer. Additionally, the city’s 2020 budget includes funding to hire a consultant to evaluate and make recommendations on the city’s parking-related ordinances and to accelerate the demolition of the city’s old public works facility to redevelop the site into a parking lot for downtown patrons. Even with these solutions in play, the city periodically receives complaints from residents and visitors who wanted to eat, shop or recreate in downtown Victoria but could not find parking. Additionally, downtown business owners have continued to express to city officials a strong desire to construct a parking structure in the core downtown area to provide additional parking. Some business owners have even reported a downward trend in business citing lack of parking as the primary reason. For order of magnitude, a new parking structure can range between $20,000 and $30,000 per stall, and $100 to $150 per stall to maintain and operate on a monthly basis (Hoisington Koegler Group, February 2019). Additionally, the city does not currently own land in the downtown core that could accommodate such use, so a land purchase would be an additional cost to consider. A survey of 10 task force members (made up of two members council, two planning commission members, three residents and three business owners) provided input into the parking study and recommended the city further explore the location and feasibility of additional parking. As a result, the city’s 2020 budget reflects accelerated demolition and redevelopment of the city’s old public works facility into a parking lot to serve downtown patrons. This work is now expected to begin in 2020 rather than 2023. Additionally, a summary of the questions and task force member responses related to a parking structure follow:

Should a public parking ramp be built and who should pay for the construction: a) City ‐ 2 b) Downtown property owners ‐ 0 c) Some combination of City and downtown property owners – 6

If the City participating in financing a public parking ramp, should the City:

a) Use general funds – 0

Page 62 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 6 of 28

b) Only use TIF funds – 4 c) TIF and other funds ‐ 4 d) Not participate financially at all ‐ 2

Should a public parking ramp be built, who should pay for the maintenance:

a) City ‐ 2 b) Downtown property owners ‐ 0 c) City and downtown property owners – 6

Cities may use eminent domain to acquire property for a public use. When using eminent domain a judge determines the fair market price for the property. Should the City consider using eminent domain to construct a parking ramp?

a) Yes, only if a property owner is willing to sell ‐ 3 b) Yes, even if a property owner is unwilling to sell ‐ 2 c) No – 4

An excerpt from the 2019 parking study further discusses considering balancing parking needs with economic development.

The City of Victoria has seen a growing interest in downtown redevelopment projects (e.g., the Flats, the Victoria Burrow and the Creamery Site). These interests mirror development trends that are shifting towards urban centers that are located within walking distance to jobs and entertainment use. However, one of the ongoing challenges cities and developers face in these new markets is the ability to demonstrate to a lender that there is enough parking (surplus) available in an urban setting to meet their needs. Lenders are reluctant to approve loans if a plan does not adequately meet their parking requirements. Developers are also concerned about the long‐term marketability of their property if parking is not provided on‐site. To help alleviate these concerns, a parking generation model was developed to demonstrate the potential parking surplus available to accommodate future needs or to determine the breaking point when an alternative strategy should be explored. (Hoisington Koegler Group, February 2019)

As the city looks at future development and redevelopment to the west and east of the core downtown area, it will be important to continue to think about how parking would factor into any development or redevelopment. Solutions that maximize the existing parking supply and reduce the demand to build additional spaces strengthen the urban design that helps make Victoria desirable. If a larger redevelopment or infill opportunity presents itself, the city could consider working with the property owner or developer to determine their parking needs and the potential of developing additional public parking spaces in a parking structure. To further assist council in understanding what tools are available to fund potential parking solutions (short and long term) or large capital projects beyond increasing the property tax levy, levying special assessments or utilizing Tax Increment Financing (TIF), the city council is exploring a general local sales tax within the city.

Page 63 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 7 of 28

Section III: Sales and Use Tax in Minnesota Understanding Sales and Use Tax Before one can understand what local sales tax is, one must understand what state general sales tax is. Minnesota Statutes, chapters 297A and 297B provide that sales and purchases of tangible personal property and certain services are subject to the sales and use tax. Sales tax is simply a tax paid by the consumer at the time of purchase. The tax is added on to the purchase by the retailer who then submits the sales tax to the state. In Minnesota, sales tax applies to retail sales of taxable services and/or tangible personal property made in the state. Most retail sales are taxable in Minnesota. The general sales tax rate for the state of Minnesota is 6.875 percent. However, there are some additional special rates:

• Short-term rental of motor vehicles – 21.075% • Motor vehicle sales tax: 6.50% • Manufactured housing and park trailers: 6.875% on

65 percent of the cost In Minnesota, a corresponding use tax is required in all jurisdictions with a local sales tax. This has been in effect since Jan. 1, 2000 (M.S. 297A.99, subd. 6). A use tax is a tax charged on goods or services where the tax was not collected at the time of purchase. The general use tax rate is the same as the state’s general sales tax rate. A use tax removes any disadvantage local businesses may suffer to competitors located outside the taxing area and not required to collect local taxes.

The sales tax and the use tax are "mutually exclusive," which means either sales tax or use tax applies to a single transaction, but not both. The tax rate is the same for both sales and use tax, and the same exemptions apply. For purposes of this white paper and council discussion, local option sales tax refers to both the local sales tax and the local use tax as appropriate. Total sales tax revenue in Minnesota for Fiscal Year 2019 (FY2019) was forecasted at $7 billion. Motor vehicle sales and leases were projected to make up $795 million of the $7 billion (House Research and Fiscal Analysis Departments, Jan. 16, 2019). Net general sales tax receipts for FY2019, which ended on June 30, 2019 were $68 million or 1.2 percent greater than forecasted (Minnesota Management and

Examples of When Use Tax is Due

• You buy an item outside of

the city and the seller doesn’t charge local sales tax and you use or store this item in the city

• You buy a taxable item from an out of state seller who does not charge local sales tax

Online Sales The June 2018 Supreme Court case South Dakota v. Wayfair allows states to require remote sellers to collect sales taxes if certain conditions are met. Most remote sellers were required to collect Minnesota tax beginning October 1, 2018.

Page 64 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 8 of 28

Budget, July 10, 2019). While FY2019 exceeded the state’s revenue projections, long-term economic growth is expected to be low. This is consistent with what’s happening at a national level. The Federal Open Market Committee (FOMC) released a statement in July 2019 indicating that economic activity has been rising at a moderate rate and growth of household spending has picked up from earlier in the year (Federal Reserve Press Release, July 31, 2019). However, with economists arguing that healthy economic growth should range between two and three percent (2-3%), the national GDP growth for 2020 is projected to fall below this range to 1.8 percent (1.8%). Long-term growth is expected to continue to fall tapering off to 1.6 percent (1.6%) by 2022 (Minnesota Management and Budget, July 10, 2019). Taxable Sales and Tax-Exempt Sales in Minnesota As we look to determine what Victoria’s projected revenue could be from enacted a local option sales tax, it is important to understand what is taxable and exempt from sales tax. This is key in the local sales tax discussion because the same tax base and the same exemptions apply to local sales and use taxes. While there are some exceptions to what is taxable in the state (e.g. clothing, food for home consumption), a general list of what is taxable follows: Figure 1 - Taxable Items List

Taxable Items – Minnesota Sales Tax Retail Sales Furniture and fixtures Admission and amusement fees Meals and drinks Building materials, supplies, equipment Utilities Cable and satellite TV services Vending machine sales Candy and soft drinks Cigarettes Fabrication and installation labor Computer software Delivery charges Drugs (most over the counter) Lodging Machinery, equipment, tools Appliances Motor vehicles, leases and rentals (motor

vehicle sales are exempt from local sales tax but not State sales tax)

Some services (building, cleaning, laundry, lawn care, towing, landscaping, pet care)

It should be noted that services performed will also be subject to the local tax if more than half of that service is performed within that local taxing jurisdiction. Likewise, exemptions from sales tax for individuals in Minnesota follow:

Page 65 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 9 of 28

Figure 2 - Sales Tax Exempt List of Items

Items Exempt from Minnesota Sales Tax Food for home consumption All drugs for human consumption Clothing Newspaper and subscription magazines Home heating fuels Cigarettes (subject to in-lieu tax instead) Motor fuels (subject to the gas tax)

Business and farms sales also have several exemptions from the state sales tax. Major business and farm sales tax exemptions include:

• Capital equipment • Farm machinery • Certain direct inputs to agricultural and industrial production • Certain direct inputs for some taxable services

Other major sales tax exemptions for the state include:

• Most sales to the federal government and local governments (sales to the state government are still taxable)

• Many sales to nonprofit charitable, religious, educational and youth organizations • Certain sales by nonprofit charitable organizations

A full list and explanation of what is taxable and what is exempt from taxes is available through the Minnesota Department of Revenue at: https://www.revenue.state.mn.us/guide/minnesota-sales-and-use-tax-business-guide

Section IV: Local Option Sales and Use Tax in Minnesota The remainder of this paper will explore local option sales and use tax – what it is, how it has evolved over time, the steps a city would need to take to levy a local sales and use tax in its community, the projected impact of local option sales and use tax in Victoria, and the pros and cons of imposing such tax. Local Authority to Impose Tax As noted previously, state statutes limit the authority of cities to raise revenue. Cities do, however, have some additional revenue-related authorities in addition to property taxes, fees and charges, state and federal aid monies, franchise fees, and special assessments. For example, cities have authority to levy a local lodging tax (M.S. 469.190), gambling tax (M.S. 349.213), and to establish special taxing districts such as storm sewer improvements districts (M.S. 444.16) or housing improvement districts (M.S. 428A.13) – to name a few. Additionally, cities may work with entities who are exempt from property taxes but are heavy users of city services (such as churches or colleges) to negotiate voluntary payment of some amount to the City. This is referred to as “payment in lieu of taxes,” also known as PILOT or PILT.

Page 66 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 10 of 28

Carver County now levies a 0.50 percent (0.50%) transit sales and use tax as well as a $20 vehicle excise tax which became effective on Oct. 1, 2017 (Minnesota Depatment of Revenue, July 20, 2017). Revenues from the county’s local transit tax will fund projects identified in the Carver County 20-Year Transportation Tax Implementation Plan (2018-2037) as adopted in the Carver County Resolution 25-17 (Carver County, May 2, 2017). Special purpose local sales taxes such as: lodging (greater than three percent), entertainment, and food and beverage taxes - as well as local transportation/transit sales and use taxes - are beyond the scope of this white paper. Understanding Local Sales and Use Tax A local sales tax is an additional tax on sales. Local sales and use tax is not imposed in all communities. Cities must gain special legislation and obtain voter approval to impose local sales and use taxes. It is taxed at a different, lesser rate generally between 0.25 percent and 1.00 percent with the majority of local option sales tax rates at 0.50 percent. When it does apply, the local sales tax is in addition to the 6.875 percent state sales tax. It is applied to the same tax base with the same exemptions as the state sales tax. Likewise, a local use tax is collected on purchases that are taxable but were not taxed at the local sales tax rate. One significant advantage is that the sales tax base is larger than the property tax base as it includes non-resident shoppers such as commuters and leisure visitors and tourists. Up until 2019, Minneapolis and St. Paul were the only two cities in the seven-county Twin Cities metropolitan area with a general local option sales tax enacted. Effective, Oct. 1, 2019, three cities began collecting a local option sales tax in the metro: Elk River (0.50%), Excelsior (0.50%) and Rogers (0.25%). The City of West St. Paul received authorization and voter approval and will begin collecting a half percent (0.50%) local option sales tax on Jan. 1, 2020. With such few metro cities collecting a local option sales tax, local data is more difficult to ascertain. However, the following excerpt from a study conducted by the Minnesota Department of Revenue examines the distribution of state and local tax burdens on Minnesotans in 2014. It should be noted, that projected distributions for 2019 remain about the same. (2017 Minnesota Tax Incidence Study, p. 27):

The following [chart] show[s] that some taxes are borne by Minnesotans in much greater proportions than are others. Of the large state taxes, the income tax is borne almost entirely by [Minnesotans], who pay 94 percent of total collections. [They] bear a smaller share of the

Calculating Local Sales Tax

• Combine the state tax rate and the

local rates.

• Apply the combined rate to the taxable sales price

• Round to the nearest full cent

Page 67 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 11 of 28

general sales tax burden (79 percent). At the other end of the scale, Minnesotans are estimated to bear only 25 percent of the burden of property taxes on industrial property. Minnesotans are estimated to bear 62 percent of the burden of the total tax imposed on business. [The following chart] assigns each tax to one of three broad categories. Each tax is either a tax on income, a tax on consumption, or a tax on property. [The following chart] shows each category’s share of the total state and local tax burden for Minnesotans. It also distinguishes state taxes from local taxes. Over 72 percent of the total burden is from state taxes; less than 28 percent is from local taxes. By tax category, 41 percent of the burden is from taxes on income, 29 percent from taxes on property, and 30 percent from taxes on consumption. Local taxes are primarily taxes on property, with a relatively small portion on consumption (local sales taxes). State taxes are primarily on income or consumption, with a relatively small portion on property.

Figure 3 - 2014 Distribution of State and Local Tax Burdens Pie Chart

Historical Overview – Local Sales and Use Tax in Minnesota Legislation passed in 1971 prohibits cities from imposing any new tax or increasing local taxes on sales or income (M.S. 477A.016). The idea behind this restrictive law addressed legislator concerns that granting broad authority could result in the creation of “winners and losers” which could unintentionally open the door to increased aid or new equalization formulas. It also risks

Page 68 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 12 of 28

introduction of a “creep” effect that could lead to broad, general use of sales tax as a replacement of or to offset property taxes – something in which the legislature does not currently have the appetite to explore.

However, modifications to state statute have been made over time in response to increasing pressures at the local government levels to look beyond property taxes and local government aid for additional revenue. With the exception of being able to impose up to a three percent lodging tax, new local sales taxes are now limited to those authorized under special legislation and that received voter approval. Legislation passed in 1997 granted cities who obtained special legislation the authority to collect local sales and use tax to fund a specific capital improvement(s). The 1997 legislation also clarified the process for cities seeking local sales tax approval. The clarifications provided that:

• A political subdivision may impose a general sales tax if permitted by special law • The political subdivision shall adopt a resolution prior to the legislation request • Imposition after approval is subject to voter approval in the political subdivision • the local tax base be the same as the state tax base • A complementary local use tax be enacted • Exemptions for the local tax parallel the state exemptions • Quarterly ‘begin’ and ‘end’ dates be used (Minnesota Department of Revenue, February

2004). Prior the 1997 legislation, few communities throughout the state had significant revenue sources other than property tax. In 1998, the statute was modified again to require cities seeking special legislation for local option sales tax to pass a resolution that included information on the proposed tax rate, the amount of revenue expected to be raised, the intended use of the revenue, and an expiration date (M.S. 297A.99, subd. 2). Statutory changes in 1999 expanded the requirements. Cities were now required to hold a local referendum at a general election before a local sales tax could be imposed in a community. The 1999 law, however, was ambiguous to the timing of such referendum. It wasn’t until 2011 that clarifying language was added to address the timing. Between 2011 and 2019, cities were required to hold referenda prior to requesting special legislation for local sales and use tax (M.S. 297A.99 subd. 3). In 2019, the law changed again and cities are to hold referenda within two years after being granted special legislation. In 2008, language was added to the statute to prohibit cities from advertising, promoting, expending funds or even holding referenda to impose local sales and use taxes. Although, a temporary prohibition, this language was in effect through May 31, 2010 and effectively eliminated any new local sales tax proposals coming before the legislature during that time. In 2011, the law changed, and while cities could once again hold referenda to impose the local sales tax, cities were still prohibited from advertising or expending funds to promote the tax.

Page 69 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 13 of 28

It wasn’t until 2013 that legislators agreed to loosen provisions. Under the 2013 legislative changes, cities were authorized to spend money to provide the public with ‘certain facts’ about a proposed local sales tax and to host public forums on the topic as long as those ‘for’ and ‘against’ would be given equal time to speak (M.S. 297A.99. subd. 1, paras. (d) and (e)). The most recent legislative change occurred in the 2019 legislative session. In addition to requiring cities to seek special legislation before holding a voter referendum, the law requires revenue to go solely to the construction and rehabilitation costs and associated bonding costs related to the specific capital improvement approved by the voters (M.S. 297A.99 subd. 3). There is one exception to this; the city of Duluth has collected local sales tax since 1970 for general operating purposes. Having gained authority for local sales tax prior to the 1971 act, which prohibited cities from imposing a new tax or increasing an existing tax, and later restrictions that apply to local sales tax, Duluth is the only city that may use the tax collected for general operating purposes. Some cities, however, have historically managed to gain legislative approval to dedicate excess revenues for a specific improvement or capital project to either their general or capital funds. The legislative changes in 2019 make this more difficult as cities are required to terminate the local tax once the project is paid. Any revenue collected beyond the project cost and before the tax terminates at the end of the quarter is retained by the commissioner for the general fund (M.S. 297A.99 subd. 3(f)). Implementing Local Sales and Use Tax Once a city council adopts a resolution indicating a desire to propose a local options sales tax for their community, the city must request special legislation by Jan. 31 of the year the city will seek special legislation. If a city is granted special legislation, residents must vote to approve the tax in the next general election. If passed by a majority of the voters, the tax revenue can only be used for the specified project or improvements that were approved by the voters before the local option sales tax can be enacted. The specific steps outlined in state statute for implementing local sales and use tax follow: Figure 4 - Steps for Implementing Local Sales and Use Tax in Minnesota

Statutory Language Statutory Reference

Adopt a resolution prior to the legislative request that includes: • Proposed tax rate • Amount of revenue anticipated for each project (up to 5) • Description of how the revenues will be used • Documentation of regional significance of project • Total revenue anticipated to be raised before tax expires • Duration of the tax

M.S. 297A.99, subds. 2, and 3(b) and (c)

Request special legislation that authorizes imposition of the tax (by January 31 of the year seeking special legislation)

M.S. 297A.99, subd. 3

Page 70 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 14 of 28

Statutory Language Statutory Reference

Gain voter approval at a general election within 2 years after the special legislation is granted

M.S. 297A.99, subd. 3 (a)

File local approval with the Secretary of State before the start of the next legislative session

Pass an Ordinance imposing the tax

Inform the Commissioner of Revenue at least 90 days before the first day the tax will be imposed

M.S. 297A.99, subd. 12(b)

Display on the City’s website homepage a notification that residents and businesses may owe a local use tax on purchases of goods and services made outside of the city limits

M.S. 297A.99 subd. 12a

Send an annual notice in the water utility billing statement that residents and businesses may owe local use tax on purchases of goods and services made outside of the city limits

M.S. 297A.99 subd. 12a

Seeking special legislation to enact a local option sales tax does not guarantee legislative approval. There is a lack of clear approval criteria in state statutes. Through the years, some proposals have received the necessary legislative authorization and some have not. Communities not granted legislative approval are left in the dark without guidance as to why or what did not meet the legislature’s approval. For example, the City of Excelsior pursued legislative approval for five years before finally receiving the authority to enact the tax in 2019. There is no easy way to ascertain the number of proposals that did not receive legislative approval for implementing, or in some cases modifying existing local sales tax authority. That being said, a staff review of 2017-2018 bill summaries from the legislative session, found that all seven requests to authorize new local option sales taxes were granted. However, of the five proposals requesting modification to existing local option sales tax authority (e.g. increasing the sales tax rate, redirecting revenue to additional or different projects), only one of the five proposals were granted modification (Minnesota Senate, 2018). A staff review of 2018-2019 bill summaries from the legislation session and first special session found that of all of the 17 requests for new or increased local option sales taxes were approved and the one request to modify an existing local option sales tax was also authorized. (Minnesota House Research, May 24, 2019) The most current information on local general sales taxes authorized by special legislation can be found on the Minnesota House Sales and Use Tax webpage (Minnesota House of House of Representatives House Research Department, 2019).

Page 71 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 15 of 28

The Current Landscape – Local Sales and Use Tax As of Jan. 1, 2019, 35 cities and three counties have imposed a general local option sales tax. Effective Oct. 1, 2019, nine new cities started collecting a local option sales tax. With the exception of Minneapolis and St. Paul, three cities (Elk River, Excelsior and Rogers) are the first cities in seven-county Twin Cities metropolitan area to impose a local option sales tax. Additionally, a fourth city, West St. Paul, will begin collecting a local option sales tax on January 1, 2020. Looking more broadly, three other Minnesota cities had imposed local option sales tax that have since expired, and one city and two counties have received special legislation for a general local option sales tax but have not imposed the tax1. Figure 5 - Local Sales and Use Tax Count

Local Sales and Use Tax Status Cities Counties

Sales and Use Taxes Currently Imposed

35 3

Sales and Use Taxes Effective Oct. 1, 2019 9 0 Sales and Use Taxes Expired

3 0

Sales and Use Taxes Authorized but not Imposed

1 2

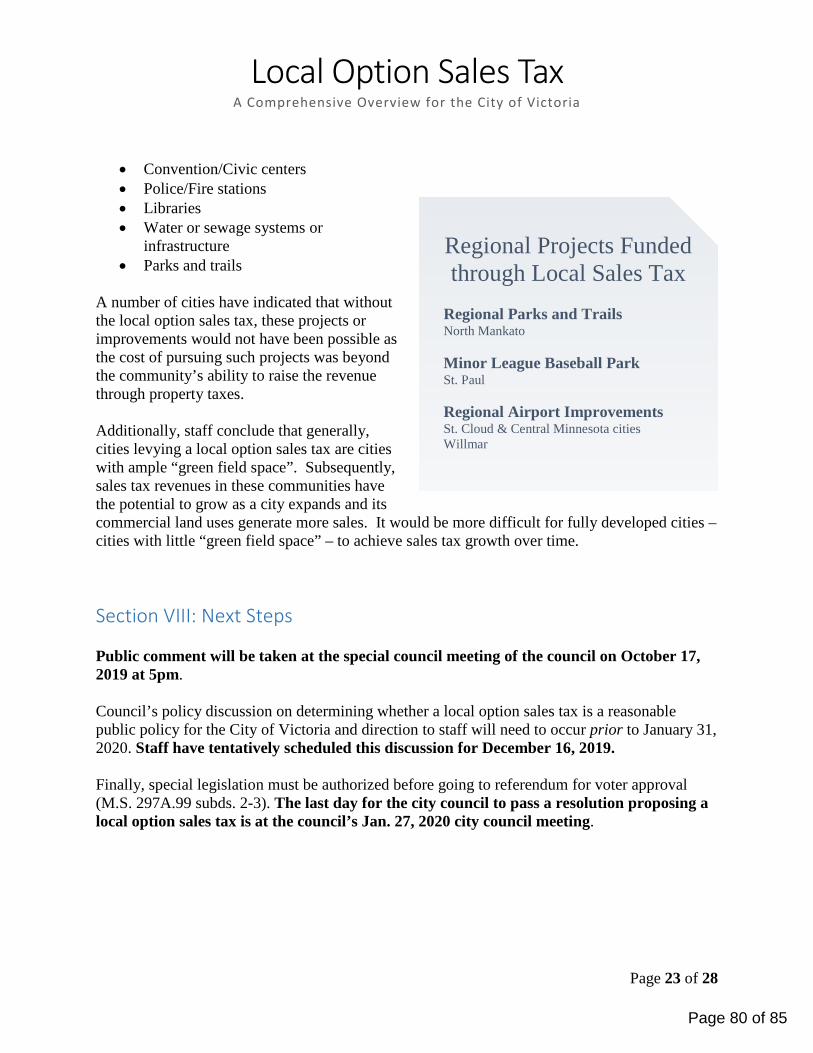

A summary of the projects that the four metro cities will use local option sales tax revenue to fund follow:

Elk River – 0.50% ($35 million) • Recreational facility (ice arena, community activity space, turf field house) • Senior center facility improvements • Park facility improvements (athletic fields, picnic pavilion) • Dredging of Lake Orono • Citywide trail connections

Excelsior – 0.50% ($7 million)

• Funding source for the parks master plan including: o Parking o Park facilities (picnic pavilions, equipment rentals, restrooms, bandshell) o Playground equipment upgrades o Shoreline improvements o Enhanced neighborhood entries o Tree preservation

1 This chart reflects general local option sales tax only and does not include a count of cities or counties with other local sales taxes such as transportation/transit, entertainment, lodging, liquor, etc.

Page 72 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 16 of 28

o Boardwalk and trail connections Rogers – 0.25% ($16.5 million)

• New trails and trail and pedestrian crossings and connections • Splash pad and school/community pool • Site improvements for future recreation facilities

West St. Paul – 0.5% ($28 million)

• Infrastructure Again, looking more broadly, the types of projects local options sales tax revenue are funding throughout the state follow: Type of Projects Number of Cities Lake, water quality or shoreline improvements 3 Flood mitigation 2 Sewer, water infrastructure improvements 8 City facilities (rec center, fire/police station, city hall municipal airport, library, community center, or land)

18

Trail – new, connections, crossings 6 Park improvements (picnic shelters, bandshell, fishing pier, athletic field, pools, restrooms)

10

Roads 5 General economic development (neighborhoods, early educations centers, cultural economic development)

3

Potential Impact of Local Sales and Use Tax in Victoria While state statute doesn’t restrict the tax rate, cities must specify the desired local tax rate that will be imposed in the special legislation request (M.S. 297A.99 subd. 5). Typically, local option sales tax rates are either 0.25, 0.50, or 1.00 percent. Of the local tax rates currently imposed 93 percent of the cities are 0.50 percent.

As a reminder, local sales tax is levied on anything that is currently subject to the sales tax. The statute also requires a compensating use tax to be applied at the same tax rate as the local sales tax (M.S. 297A.99 subd. 6).

Sales tax is inherently volatile. While not as volatile as income tax, studies do show that personal wealth (income), consumer confidence (economic outlook and forecasting errors) contributes to this volatility (Povich, 2014). If consumers are not spending as much, sales tax revenue will decline. If states or even cities with local sales tax are dependent on that revenue to meet bond obligations or for capital projects, the decrease is likely coming at a challenging time. When the revenue goes down, cities don’t necessarily have a corresponding decrease in the number of residents or businesses in which it needs to provide services. Cities have to provide services and pay debt even when revenue falls off dramatically.

Page 73 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 17 of 28

The tax burden of levying a local sales tax on Victoria residents is an important consideration. In looking at the latest available taxable sales data for the city, total taxable sales in Victoria averaged $27.6 million from 2013-2017 (Minnesota Department of Revenue Tax Research Division). Based on this data, the chart that follows, compares potential sales tax revenue to the additional property tax levy increase that would be needed to raise the same amount of revenue. Additional analysis would need to be done to determine how much of the sales tax burden is exported to non-residents and further breakdown of distribution burden. Figure 6 - Potential Sales Tax Revenue and Equivalent Property Tax Levy Increase Needed to Raise Same Amount of Revenue

Tax Rate Estimated Revenue Equivalent Property Tax Levy Increase in 2020

0.25% $69,000 1.32%

0.50% $138,000 2.64%

1.00% $276,000 5.29%

Estimated Costs to Implement Local Option Sales and Use Tax in Victoria Staff estimate the cost to implement a local option sales tax in Victoria to range from $6,500 to $11,500 in an election year to $44,000 in a non-election year. The breakdown follows: Figure 7 - Estimated Cost to Implement Local Option Sales Tax in Victoria

As illustrated in Figure 7, there are some inherent cost savings in an election year as the city is already utilizing precincts, election judges, ballots, etc. as part of the general election. Subsequently, election year costs reflect the incremental cost for adding the referendum question to the ballot. In a non-election year, however, the city would bear the entire costs of

Activity Estimated Cost – Election Year

Estimated Cost - Non-Election Year

Referendum Expense at General Election $1,500 $30,000- 35,000

Drafting of Legislative Proposal & Lobbying Efforts $5,000 - $10,000 $5,000 - $10,000

TOTAL $6,500 - $11,500 $35,000 - $45,000

Page 74 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 18 of 28

administering an election for the one referendum question. Because the same efforts are required for drafting the proposal and lobbying, that cost estimate is the same regardless of an election or non-election year.

Section V: Common Questions – Local Sales and Use Tax Despite limited use in the Twin Cities metropolitan area, many communities throughout the state have either imposed or attempted to impose a local option sales tax in their communities. Common questions that have been raised in other communities regarding local option sales tax follow: How much revenue collected would come from local residents vs. non-residents? Based on state sales tax data, it is noted that a portion of these sales (3.5 – 4.0 percent) are paid by non-residents. At the local level, however, most communities are not collecting this data. However, The City of Elk River did do this level of analysis and contracted with the University of Minnesota Extension Center for Community Vitality to look at estimated contributions of residents and non-residents for local option sales tax. As a commuter city and regional center, the report estimates that 70 percent of sales are to non-residents (University of Minnesota Extension Center for Community Vitality, May 2018). Elk River received legislative authority and voter approval and subsequently started collecting a local option sales tax in October 2019. Other studies suggest that communities with local sales taxes in place experience a loss in gross sales of 1.5 to five percent within the community (Minnesota Department of Revenue Tax Research Division, 2017). Expending resources to gather city-level survey data about who is spending money in the community to determine how much of the tax burden is exported to non-residents could strengthen a community’s proposal to secure special legislation of a new local sales tax request (Minnesota Department of Revenue, February 2004). How will the local sales tax be collected? By statute, the Minnesota Department of Revenue collects the sales tax on behalf of cities with local option sales tax imposed. The state is entitled to recover administrative costs for collection. Minnesota Statutes, section 297A.99, subd. 11 requires the tax be remitted to cities at least quarterly. If a resident from a city that has a local sales tax in place makes a purchase from outside the city limits, must that resident pay the local sales tax? No. Local option sales tax applies to a sale made or services performed within the city limits only. Vehicle purchases are specifically exempt from any local sales taxes. If a vendor operates within a local taxing district, the vendor must collect the general local sales tax and submit it to the state with its sales and use tax report.

Page 75 of 85

Local Option Sales Tax A Comprehensive Overview for the City of Victoria

Page 19 of 28