54940566-mcommerce(1)(1) kjb

DESCRIPTION

IHS DFAI DFAIH P APSHF PAOAOJF POA JAP ODF JOA PFJPJOA SFHASF HAHFASJFPA ASFH PAHF APHFPAHFPA FHAPTRANSCRIPT

1

Lecture note of Intensive seminar on m-commerce Mar, 1st~Mar, 5th, 2004

Content: 1 Overview of m-commerce

1.1 M-commerce: definitions 1.2 M-commerce: components and market players 1.3 M-commerce: characteristics 1.4 M-commerce: generations

2 Framework for m-commerce 3 M-commerce: infrastructure

3.1 Wireless networking infrastructure 3.2 Security technologies

4 M-commerce: applications 4.1 Emerging applications 4.2 Functional platform of m-commerce applications 4.3 Impact of wireless infrastructure failures on m-commerce applications. 4.4 Scenarios for m-commerce applications

5 Mobile payment 5.1 Mobile payment methods 5.2 Mobile payment process 5.3 Mobile payment system

6 Issues in m-commerce

Key words: Mobile commerce, M-commerce application, Network infrastructure, Wireless infrastructure, Mobile payment, M-commerce issues.

2

1. Overview of m-commerce 1.1 M-commerce: definitions

Mobile e-commerce (also called mobile commerce or m-commerce) is defined as all activities related to a (potential) commercial transaction conducted through communications networks that interface with wireless (or mobile) devices. (Peter Tarasewich, Robert C. Nickerson and Merrill Warkentin, ISSUES IN MOBILE E-COMMERCE, Communications of the Association for Information Systems (Volume 8, 2002) 41-64)

Mobile electronic commerce (M-Commerce) is any type of transaction of an economic value having at least at one end a mobile terminal and thus using the mobile telecommunications network. (Aphrodite Tsalgatidou and Jari Veijalainen, Mobile Electronic Commerce: Emerging Issues, 1st International Conference on E-Commerce and Web Technologies, London, Greenwich, UK, September 4-6, 2000, Lecture Notes in Computer Science, pp. 477-486)

Mobile commerce is the buying and selling of goods and services through wireless hand-held devices such as mobile phones, personal digital assistants (PDAs), mp3 players, digital cameras, handheld gaming devices and computers. (Sojen Pradhan, Mobile Commerce in the Automobile Industry, Proceedings of the International Conference on Information Technology: Computers and Communications (ITCC.03))

Mobile commerce is defined as any transaction with a monetary value that is conducted via a mobile telecommunications network. (Xiaolin Zheng, Deren Chen, Study of Mobile Payments System, Proceedings of the IEEE International Conference on E-Commerce (CEC’03))

M-commerce is the use of mobile handheld devices to communicate, interact and conduct transactions via a mobile or wireless network. (Mylini Munusamy and Hiew Pang Leang, Characteristics of Mobile Devices and an Integrated M-Commerce Infrastructure for M-Commerce Deployment, Proceedings of the Second International Workshop on Internet Computing and E-Commerce (ICECE 2002), Florida, USA.)

M-commerce is all about wireless e-commerce that is where mobile devices are used to do business on the internet. (S. Schwiderski-Grosche and H. Knospe, Secure Mobile Commerce, Electronics & Communication Engineering Journal, October, 2002)

Mobile commerce is exchanges or buying and selling of commodities, service, or information on the internet by using mobile handheld devices. (Chung-wei Lee, Wen-Chen Hu, Jyh-haw Yeh , A System Model for Mobile Commerce, Proceedings of the 23rd International Conference on Distributed Computing Systems Workshops (ICDCSW'03))

3

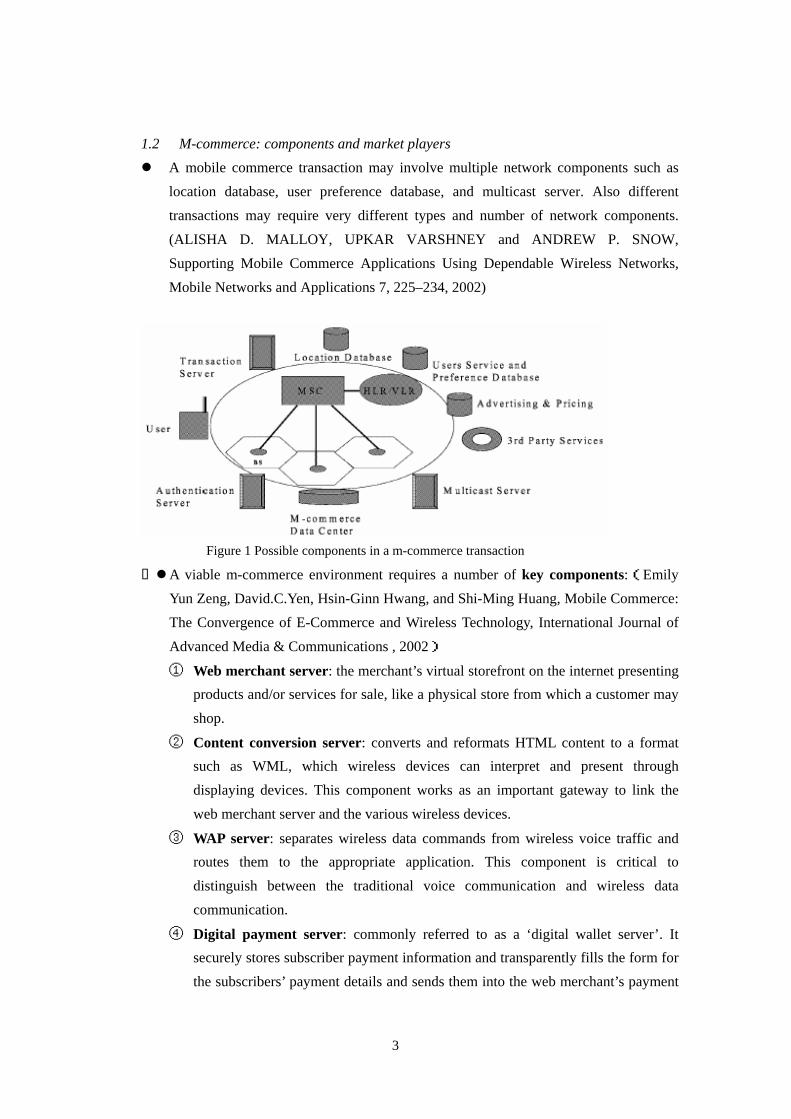

1.2 M-commerce: components and market players A mobile commerce transaction may involve multiple network components such as

location database, user preference database, and multicast server. Also different transactions may require very different types and number of network components. (ALISHA D. MALLOY, UPKAR VARSHNEY and ANDREW P. SNOW, Supporting Mobile Commerce Applications Using Dependable Wireless Networks, Mobile Networks and Applications 7, 225–234, 2002)

Figure 1 Possible components in a m-commerce transaction

A viable m-commerce environment requires a number of key components:(Emily Yun Zeng, David.C.Yen, Hsin-Ginn Hwang, and Shi-Ming Huang, Mobile Commerce: The Convergence of E-Commerce and Wireless Technology, International Journal of

Advanced Media & Communications , 2002)

① Web merchant server: the merchant’s virtual storefront on the internet presenting products and/or services for sale, like a physical store from which a customer may shop.

② Content conversion server: converts and reformats HTML content to a format such as WML, which wireless devices can interpret and present through displaying devices. This component works as an important gateway to link the web merchant server and the various wireless devices.

③ WAP server: separates wireless data commands from wireless voice traffic and routes them to the appropriate application. This component is critical to distinguish between the traditional voice communication and wireless data communication.

④ Digital payment server: commonly referred to as a ‘digital wallet server’. It securely stores subscriber payment information and transparently fills the form for the subscribers’ payment details and sends them into the web merchant’s payment

4

page.

⑤ Wireless payment proxy: converts wireless commands from mobile devices into commands that can be understood by digital payment servers.

⑥ Subscriber management system: maintains the mobile operators’ subscriber traffic, account and billing information and, by being cross-linked to digital payment servers, can act as private label account issuing systems.

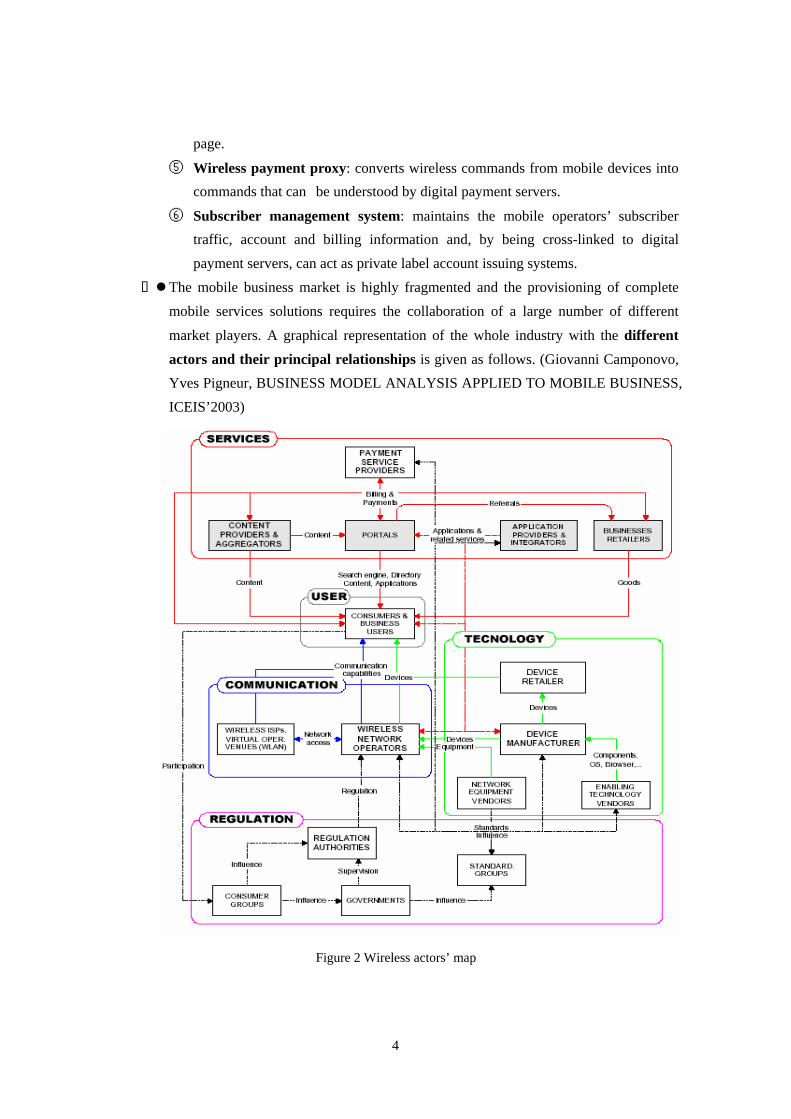

The mobile business market is highly fragmented and the provisioning of complete mobile services solutions requires the collaboration of a large number of different

market players. A graphical representation of the whole industry with the different actors and their principal relationships is given as follows. (Giovanni Camponovo, Yves Pigneur, BUSINESS MODEL ANALYSIS APPLIED TO MOBILE BUSINESS, ICEIS’2003)

Figure 2 Wireless actors’ map

5

1.3 M-commerce: characteristics The mobile business industry presents a certain number of peculiar economic

characteristics such as mobility, network effects and proprietary assets.

① Mobility is the most important characteristic of mobile business, because it represents its only distinctive advantage upon which mobile services can build their value proposition.

a. Freedom of movement: services can be used while on the move.

b. Ubiquity: the possibility of using services anywhere, independent of the

user's location.

c. Reachability: users can be reached anywhere anytime, and they can restrict

it to particular persons and contexts

d. Convenience: as mobile devices are always at hand

e. Some constraints: limited and more expensive bandwidth

② Network effects: networks are composed of a set of components connected together by links. Since the provision of a service typically requires several components, they are complementary to each other. Because of this complementarity, networks exhibit a characteristic economic phenomenon known as network effects, an example of what economists call a positive consumption externality.

③ Exclusive control over important assets: the mobile business market is also characterized by the existence of important assets that are under the exclusive control of a firm. Network operators also have total control over a number of other important assets.

④ Implications: from these characteristics it follows that the provisioning of complete mobile services solutions requires the collaboration of a large number of market players, especially including network operators and device manufacturers.

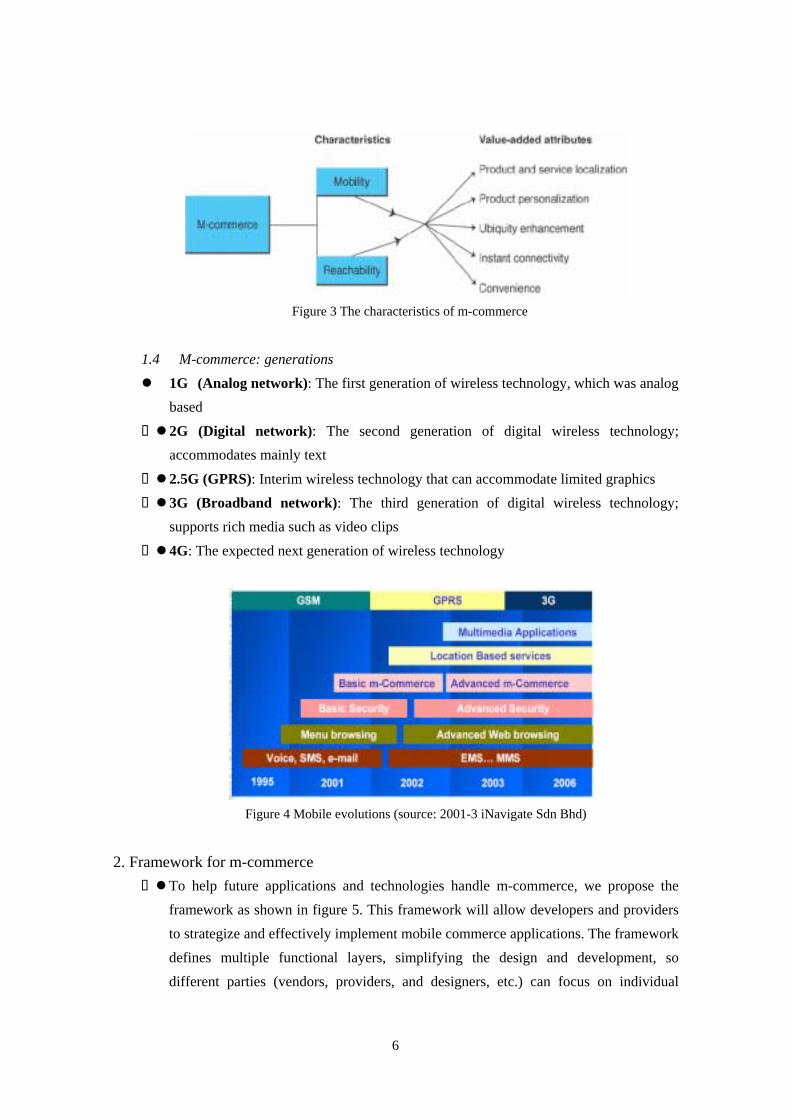

Mobile commerce: Attributes and Benefits

① Specific attributes of m-commerce (Mobility, Broad reach) ② Benefits of value-added attributes (Ubiquity, Convenience, Instant connectivity,

Personalization, Localization of products and services)

6

Figure 3 The characteristics of m-commerce

1.4 M-commerce: generations 1G (Analog network): The first generation of wireless technology, which was analog

based

2G (Digital network): The second generation of digital wireless technology; accommodates mainly text

2.5G (GPRS): Interim wireless technology that can accommodate limited graphics 3G (Broadband network): The third generation of digital wireless technology;

supports rich media such as video clips 4G: The expected next generation of wireless technology

Figure 4 Mobile evolutions (source: 2001-3 iNavigate Sdn Bhd)

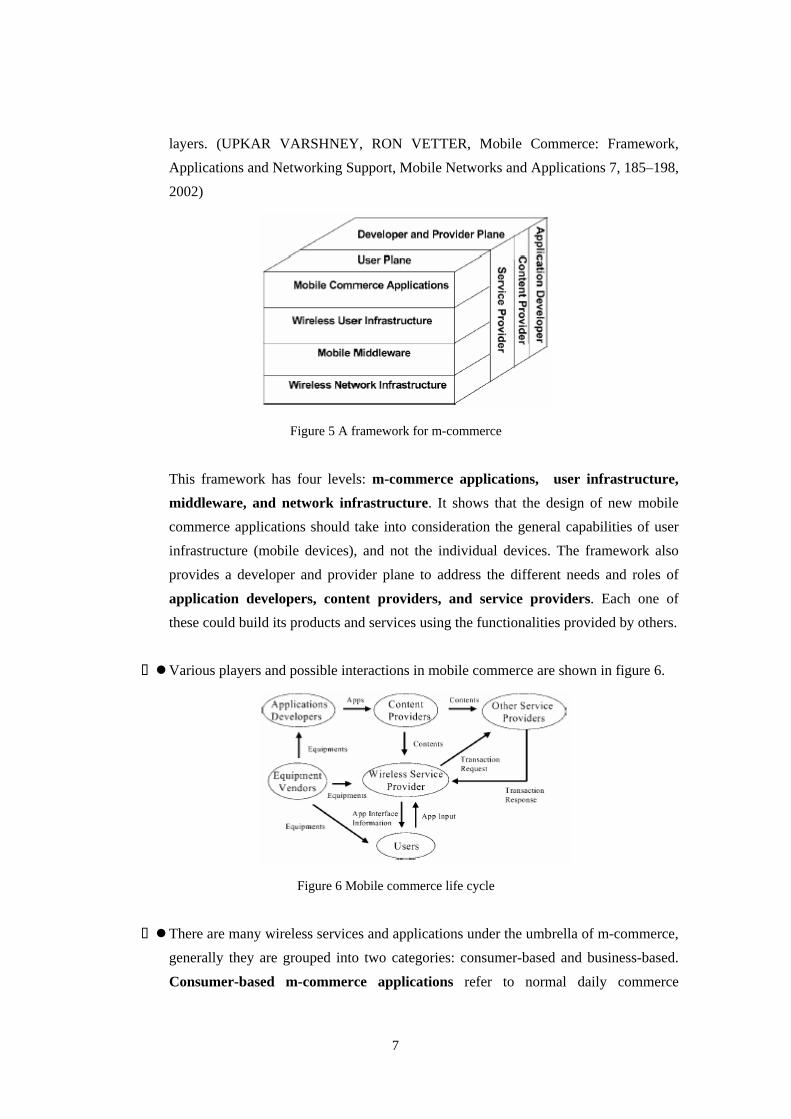

2. Framework for m-commerce To help future applications and technologies handle m-commerce, we propose the

framework as shown in figure 5. This framework will allow developers and providers to strategize and effectively implement mobile commerce applications. The framework defines multiple functional layers, simplifying the design and development, so different parties (vendors, providers, and designers, etc.) can focus on individual

7

layers. (UPKAR VARSHNEY, RON VETTER, Mobile Commerce: Framework, Applications and Networking Support, Mobile Networks and Applications 7, 185–198, 2002)

Figure 5 A framework for m-commerce

This framework has four levels: m-commerce applications, user infrastructure, middleware, and network infrastructure. It shows that the design of new mobile commerce applications should take into consideration the general capabilities of user infrastructure (mobile devices), and not the individual devices. The framework also provides a developer and provider plane to address the different needs and roles of

application developers, content providers, and service providers. Each one of these could build its products and services using the functionalities provided by others.

Various players and possible interactions in mobile commerce are shown in figure 6.

Figure 6 Mobile commerce life cycle

There are many wireless services and applications under the umbrella of m-commerce, generally they are grouped into two categories: consumer-based and business-based.

Consumer-based m-commerce applications refer to normal daily commerce

8

activities that are most likely to be conducted by anyone who is a user of a wireless device. Examples include receiving stock prices, finding restaurants, getting driving

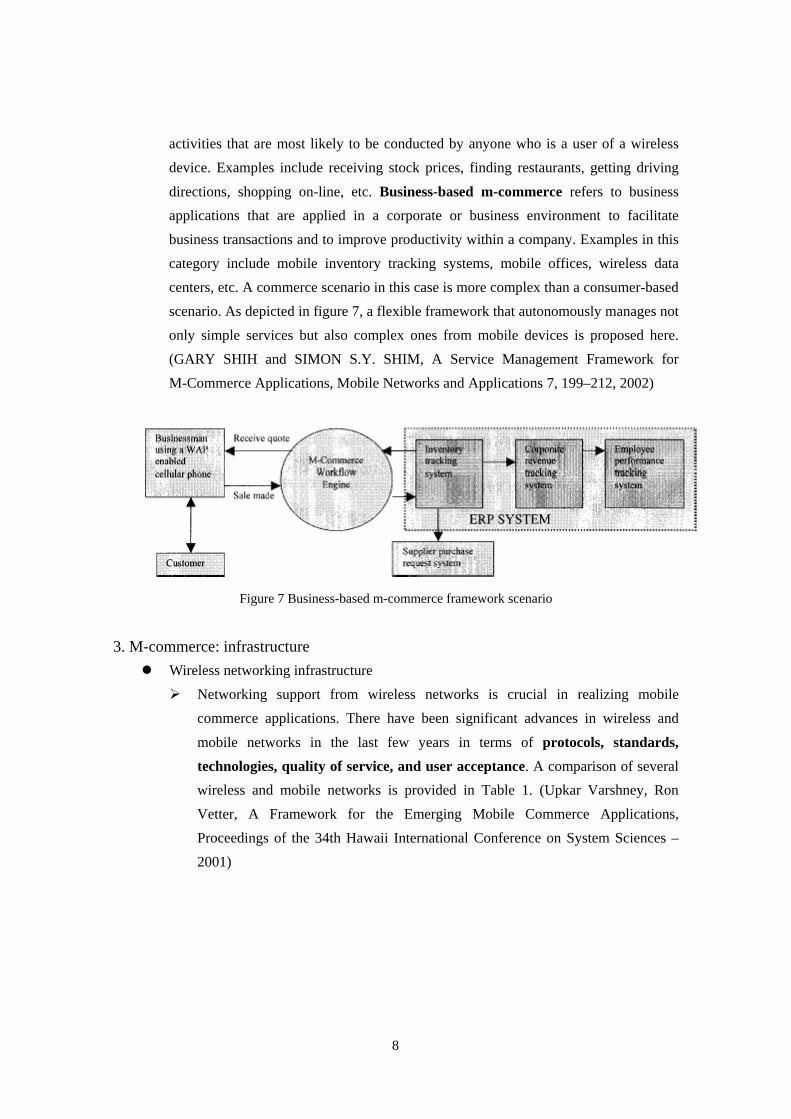

directions, shopping on-line, etc. Business-based m-commerce refers to business applications that are applied in a corporate or business environment to facilitate business transactions and to improve productivity within a company. Examples in this category include mobile inventory tracking systems, mobile offices, wireless data centers, etc. A commerce scenario in this case is more complex than a consumer-based scenario. As depicted in figure 7, a flexible framework that autonomously manages not only simple services but also complex ones from mobile devices is proposed here. (GARY SHIH and SIMON S.Y. SHIM, A Service Management Framework for M-Commerce Applications, Mobile Networks and Applications 7, 199–212, 2002)

Figure 7 Business-based m-commerce framework scenario

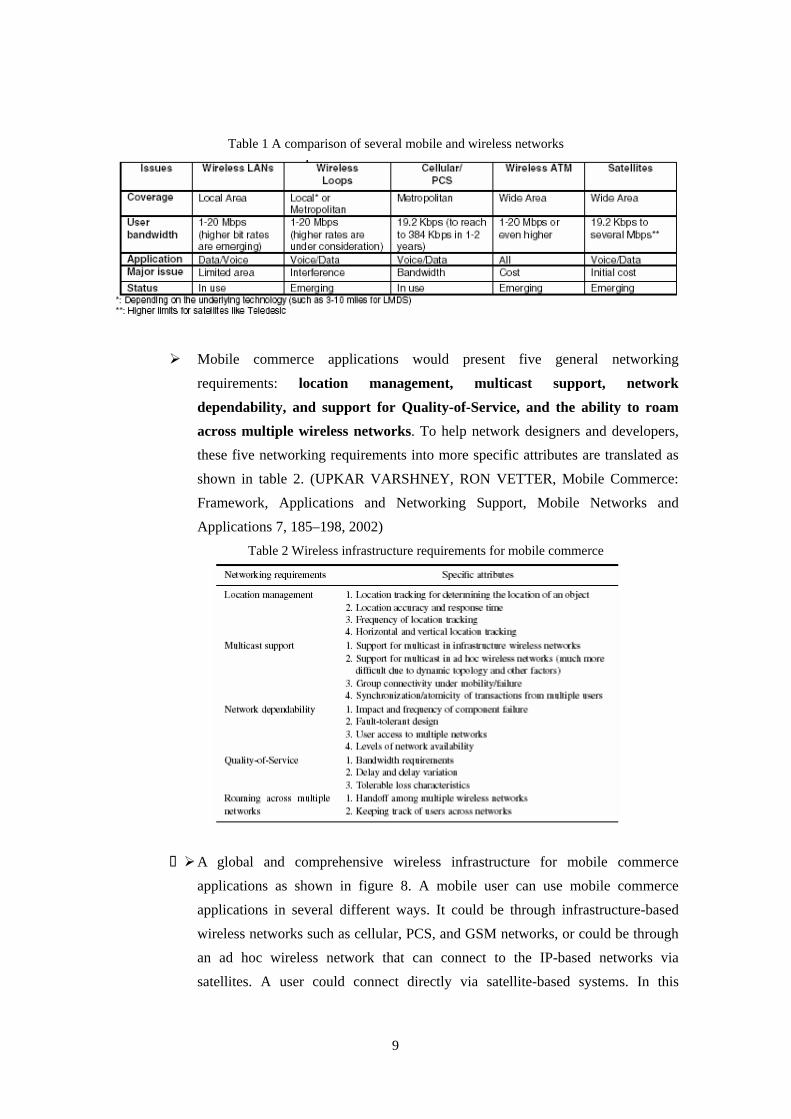

3. M-commerce: infrastructure Wireless networking infrastructure

Networking support from wireless networks is crucial in realizing mobile commerce applications. There have been significant advances in wireless and

mobile networks in the last few years in terms of protocols, standards, technologies, quality of service, and user acceptance. A comparison of several wireless and mobile networks is provided in Table 1. (Upkar Varshney, Ron Vetter, A Framework for the Emerging Mobile Commerce Applications, Proceedings of the 34th Hawaii International Conference on System Sciences – 2001)

9

Table 1 A comparison of several mobile and wireless networks

Mobile commerce applications would present five general networking

requirements: location management, multicast support, network

dependability, and support for Quality-of-Service, and the ability to roam across multiple wireless networks. To help network designers and developers, these five networking requirements into more specific attributes are translated as shown in table 2. (UPKAR VARSHNEY, RON VETTER, Mobile Commerce: Framework, Applications and Networking Support, Mobile Networks and Applications 7, 185–198, 2002)

Table 2 Wireless infrastructure requirements for mobile commerce

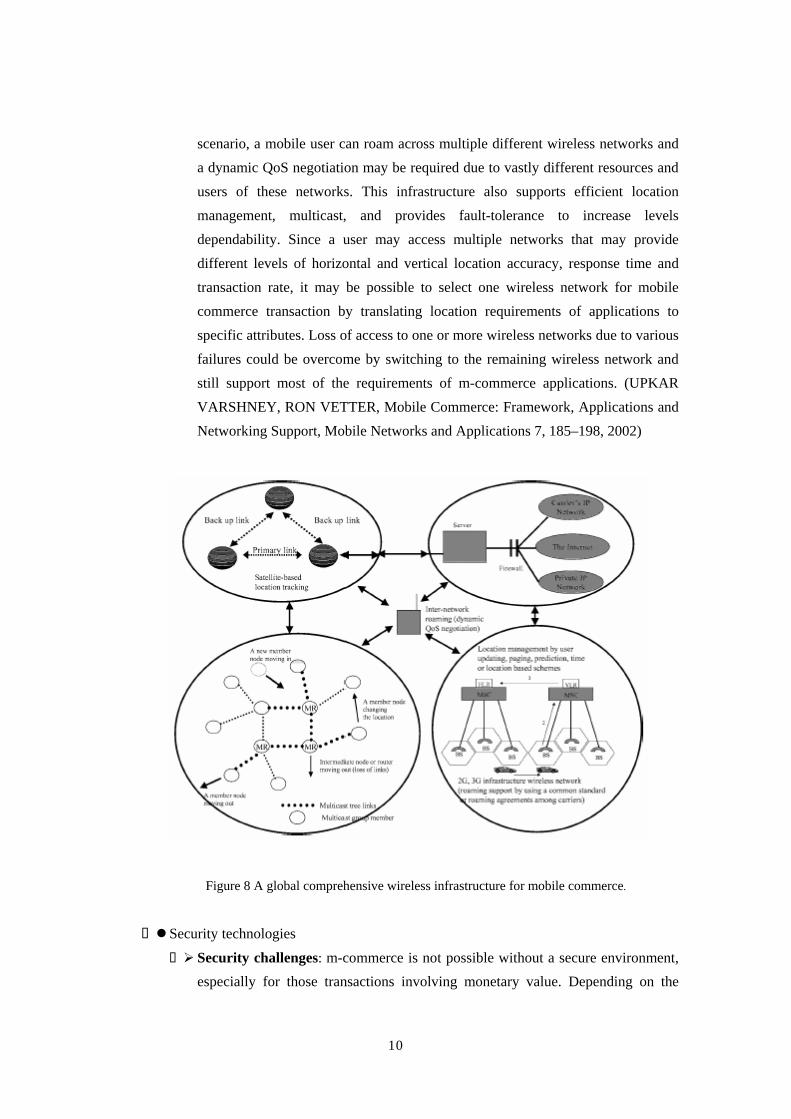

A global and comprehensive wireless infrastructure for mobile commerce applications as shown in figure 8. A mobile user can use mobile commerce applications in several different ways. It could be through infrastructure-based wireless networks such as cellular, PCS, and GSM networks, or could be through an ad hoc wireless network that can connect to the IP-based networks via satellites. A user could connect directly via satellite-based systems. In this

10

scenario, a mobile user can roam across multiple different wireless networks and a dynamic QoS negotiation may be required due to vastly different resources and users of these networks. This infrastructure also supports efficient location management, multicast, and provides fault-tolerance to increase levels dependability. Since a user may access multiple networks that may provide different levels of horizontal and vertical location accuracy, response time and transaction rate, it may be possible to select one wireless network for mobile commerce transaction by translating location requirements of applications to specific attributes. Loss of access to one or more wireless networks due to various failures could be overcome by switching to the remaining wireless network and still support most of the requirements of m-commerce applications. (UPKAR VARSHNEY, RON VETTER, Mobile Commerce: Framework, Applications and Networking Support, Mobile Networks and Applications 7, 185–198, 2002)

Figure 8 A global comprehensive wireless infrastructure for mobile commerce.

Security technologies

Security challenges: m-commerce is not possible without a secure environment, especially for those transactions involving monetary value. Depending on the

11

points of view of the different participants in an m-commerce scenario, there are different security challenges. These challenges related to:

The mobile device: confidential user data on the mobile device as well as the

device itself should be protected from unauthorized use The radio interface: access to a telecommunication network requires the

protection of transmitted data in terms of confidentiality, integrity, and

authenticity

The network operator infrastructure: security mechanisms for the end user

often terminate in the access network. This raises questions regarding the

security of the user’s data within and beyond the access network.

The kind of m-commerce application: m-commerce applications, especially

those involving payment, need to be secured to assure customers, merchants, and

network operators

Security of network technologies GSM (Global System for Mobile Communications)

UMTS (Universal Mobile Telecommunications System)

WLAN (Wireless Local Area Networks)

Bluetooth (Wireless technology developed by the Bluetooth Special Interest

Group. This defined protocol stack that permits ad hoc piconets and connections

to peripheral devices.)

4. M-commerce: applications 4.1 Emerging applications

(Various classes of m-commerce applications have been defined.) Be classified as mobile financial services, mobile advertising, mobile shopping,

mobile entertainment, mobile office, mobile inventory management, mobile education, mobile telematics, and mobile information management. Within these classifications, various services may be identified, for example, mobile financial services includes services such as mobile banking, mobile broking, mobile cash, mobile payment, mobile e-billing and mobile e-salary. Mobile shopping would involve services such as mobile retailing, mobile auctions, mobile ticketing, mobile reservations and even mobile postcards. (Mylini Munusamy and Hiew Pang Leang, Characteristics of Mobile Devices and an Integrated M-Commerce Infrastructure for M-Commerce Deployment, Proceedings of the Second International Workshop on Internet Computing and E-Commerce (ICECE 2002))

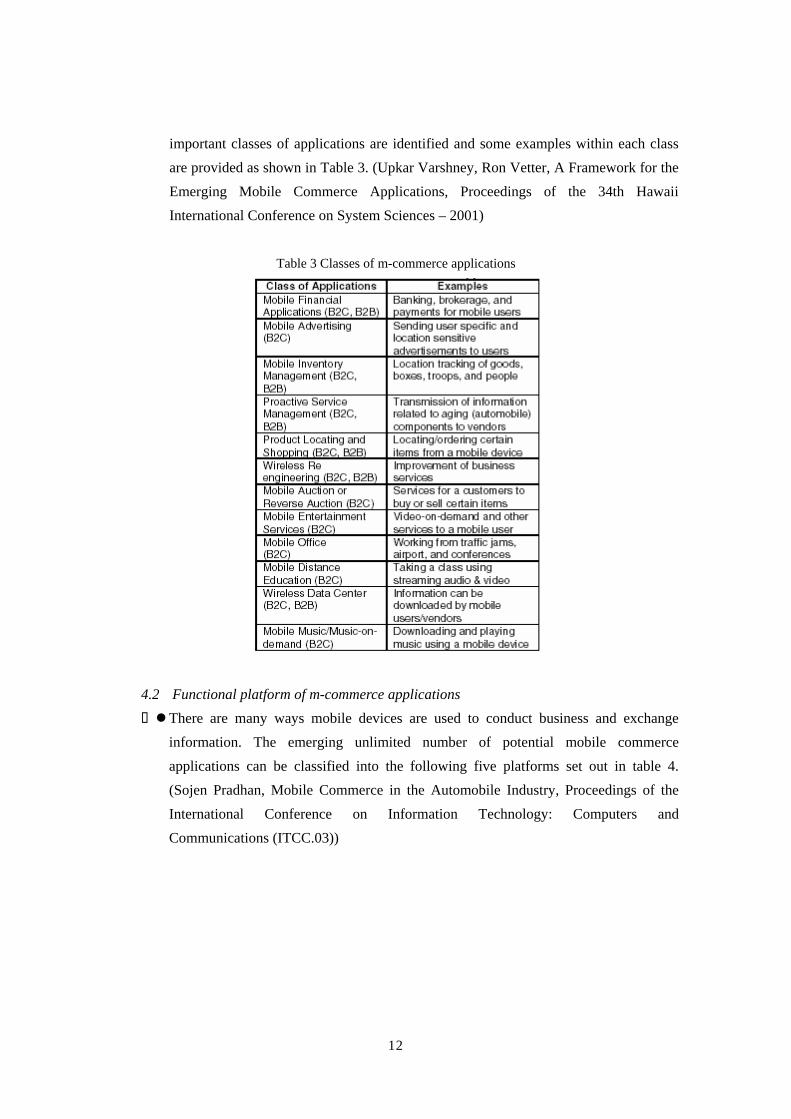

There are potentially an unlimited number of mobile commerce applications, a few

12

important classes of applications are identified and some examples within each class are provided as shown in Table 3. (Upkar Varshney, Ron Vetter, A Framework for the Emerging Mobile Commerce Applications, Proceedings of the 34th Hawaii International Conference on System Sciences – 2001)

Table 3 Classes of m-commerce applications

4.2 Functional platform of m-commerce applications

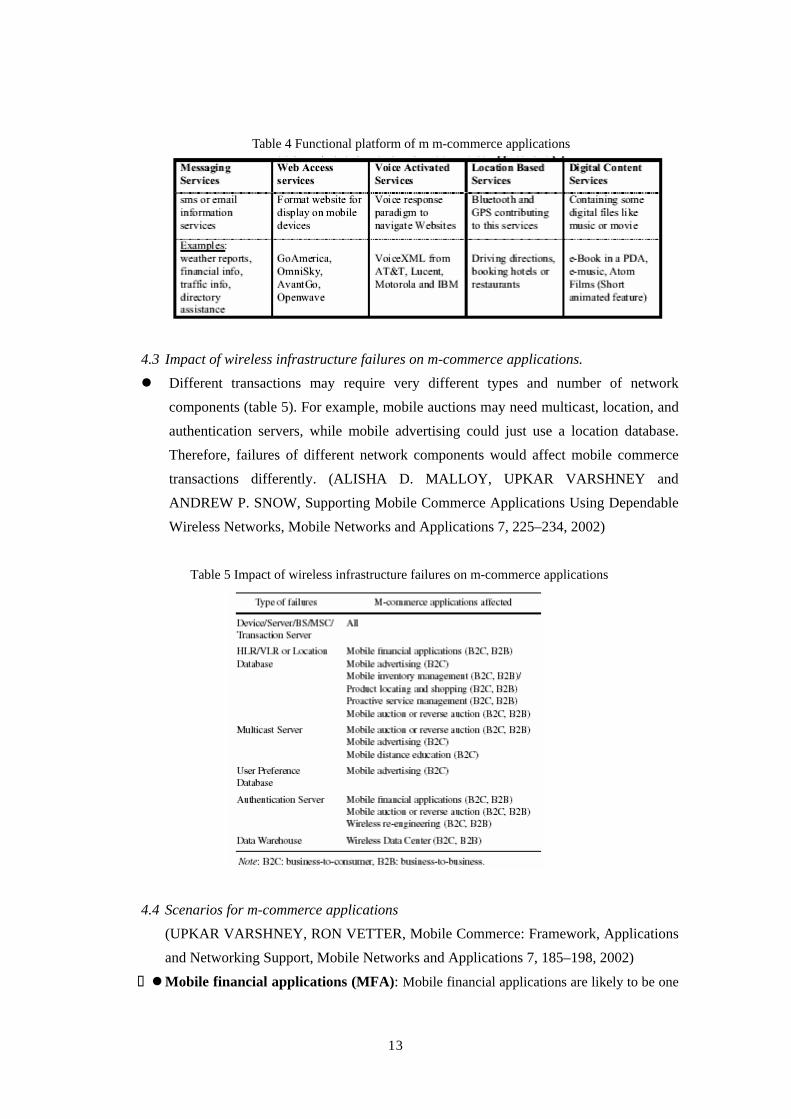

There are many ways mobile devices are used to conduct business and exchange information. The emerging unlimited number of potential mobile commerce applications can be classified into the following five platforms set out in table 4. (Sojen Pradhan, Mobile Commerce in the Automobile Industry, Proceedings of the International Conference on Information Technology: Computers and Communications (ITCC.03))

13

Table 4 Functional platform of m m-commerce applications

4.3 Impact of wireless infrastructure failures on m-commerce applications. Different transactions may require very different types and number of network

components (table 5). For example, mobile auctions may need multicast, location, and authentication servers, while mobile advertising could just use a location database. Therefore, failures of different network components would affect mobile commerce transactions differently. (ALISHA D. MALLOY, UPKAR VARSHNEY and ANDREW P. SNOW, Supporting Mobile Commerce Applications Using Dependable Wireless Networks, Mobile Networks and Applications 7, 225–234, 2002)

Table 5 Impact of wireless infrastructure failures on m-commerce applications

4.4 Scenarios for m-commerce applications (UPKAR VARSHNEY, RON VETTER, Mobile Commerce: Framework, Applications and Networking Support, Mobile Networks and Applications 7, 185–198, 2002)

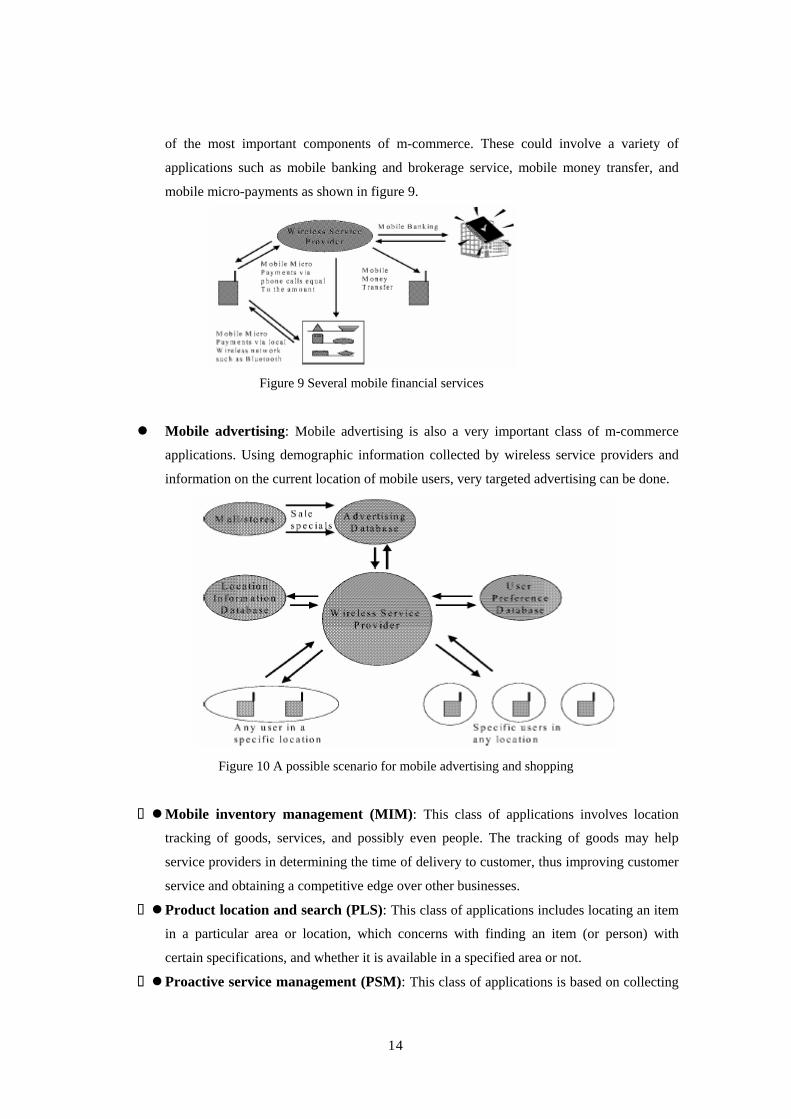

Mobile financial applications (MFA): Mobile financial applications are likely to be one

14

of the most important components of m-commerce. These could involve a variety of

applications such as mobile banking and brokerage service, mobile money transfer, and

mobile micro-payments as shown in figure 9.

Figure 9 Several mobile financial services

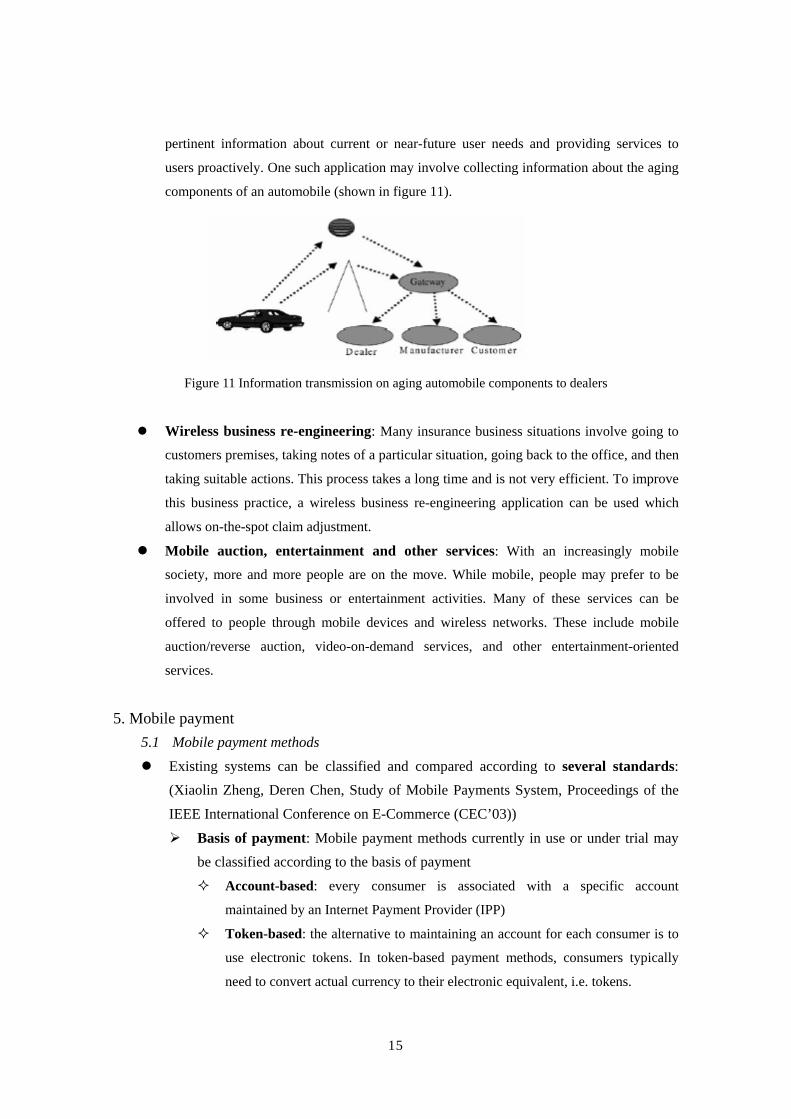

Mobile advertising: Mobile advertising is also a very important class of m-commerce

applications. Using demographic information collected by wireless service providers and

information on the current location of mobile users, very targeted advertising can be done.

Figure 10 A possible scenario for mobile advertising and shopping

Mobile inventory management (MIM): This class of applications involves location

tracking of goods, services, and possibly even people. The tracking of goods may help

service providers in determining the time of delivery to customer, thus improving customer

service and obtaining a competitive edge over other businesses.

Product location and search (PLS): This class of applications includes locating an item

in a particular area or location, which concerns with finding an item (or person) with

certain specifications, and whether it is available in a specified area or not.

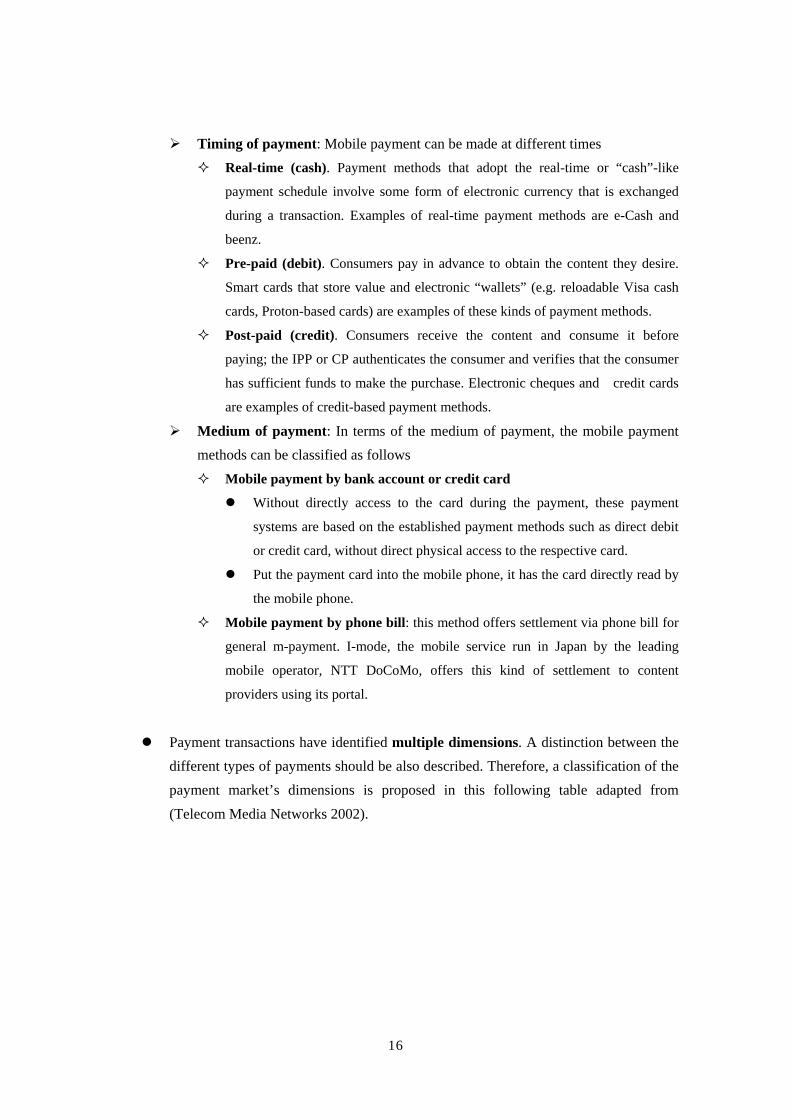

Proactive service management (PSM): This class of applications is based on collecting

15

pertinent information about current or near-future user needs and providing services to

users proactively. One such application may involve collecting information about the aging

components of an automobile (shown in figure 11).

Figure 11 Information transmission on aging automobile components to dealers

Wireless business re-engineering: Many insurance business situations involve going to

customers premises, taking notes of a particular situation, going back to the office, and then

taking suitable actions. This process takes a long time and is not very efficient. To improve

this business practice, a wireless business re-engineering application can be used which

allows on-the-spot claim adjustment.

Mobile auction, entertainment and other services: With an increasingly mobile

society, more and more people are on the move. While mobile, people may prefer to be

involved in some business or entertainment activities. Many of these services can be

offered to people through mobile devices and wireless networks. These include mobile

auction/reverse auction, video-on-demand services, and other entertainment-oriented

services.

5. Mobile payment 5.1 Mobile payment methods

Existing systems can be classified and compared according to several standards: (Xiaolin Zheng, Deren Chen, Study of Mobile Payments System, Proceedings of the IEEE International Conference on E-Commerce (CEC’03))

Basis of payment: Mobile payment methods currently in use or under trial may be classified according to the basis of payment

Account-based: every consumer is associated with a specific account

maintained by an Internet Payment Provider (IPP)

Token-based: the alternative to maintaining an account for each consumer is to

use electronic tokens. In token-based payment methods, consumers typically

need to convert actual currency to their electronic equivalent, i.e. tokens.

16

Timing of payment: Mobile payment can be made at different times Real-time (cash). Payment methods that adopt the real-time or “cash”-like

payment schedule involve some form of electronic currency that is exchanged

during a transaction. Examples of real-time payment methods are e-Cash and

beenz.

Pre-paid (debit). Consumers pay in advance to obtain the content they desire.

Smart cards that store value and electronic “wallets” (e.g. reloadable Visa cash

cards, Proton-based cards) are examples of these kinds of payment methods.

Post-paid (credit). Consumers receive the content and consume it before

paying; the IPP or CP authenticates the consumer and verifies that the consumer

has sufficient funds to make the purchase. Electronic cheques and credit cards

are examples of credit-based payment methods.

Medium of payment: In terms of the medium of payment, the mobile payment methods can be classified as follows

Mobile payment by bank account or credit card

Without directly access to the card during the payment, these payment

systems are based on the established payment methods such as direct debit

or credit card, without direct physical access to the respective card.

Put the payment card into the mobile phone, it has the card directly read by

the mobile phone.

Mobile payment by phone bill: this method offers settlement via phone bill for

general m-payment. I-mode, the mobile service run in Japan by the leading

mobile operator, NTT DoCoMo, offers this kind of settlement to content

providers using its portal.

Payment transactions have identified multiple dimensions. A distinction between the different types of payments should be also described. Therefore, a classification of the payment market’s dimensions is proposed in this following table adapted from (Telecom Media Networks 2002).

17

Table 6 The different payment dimensions

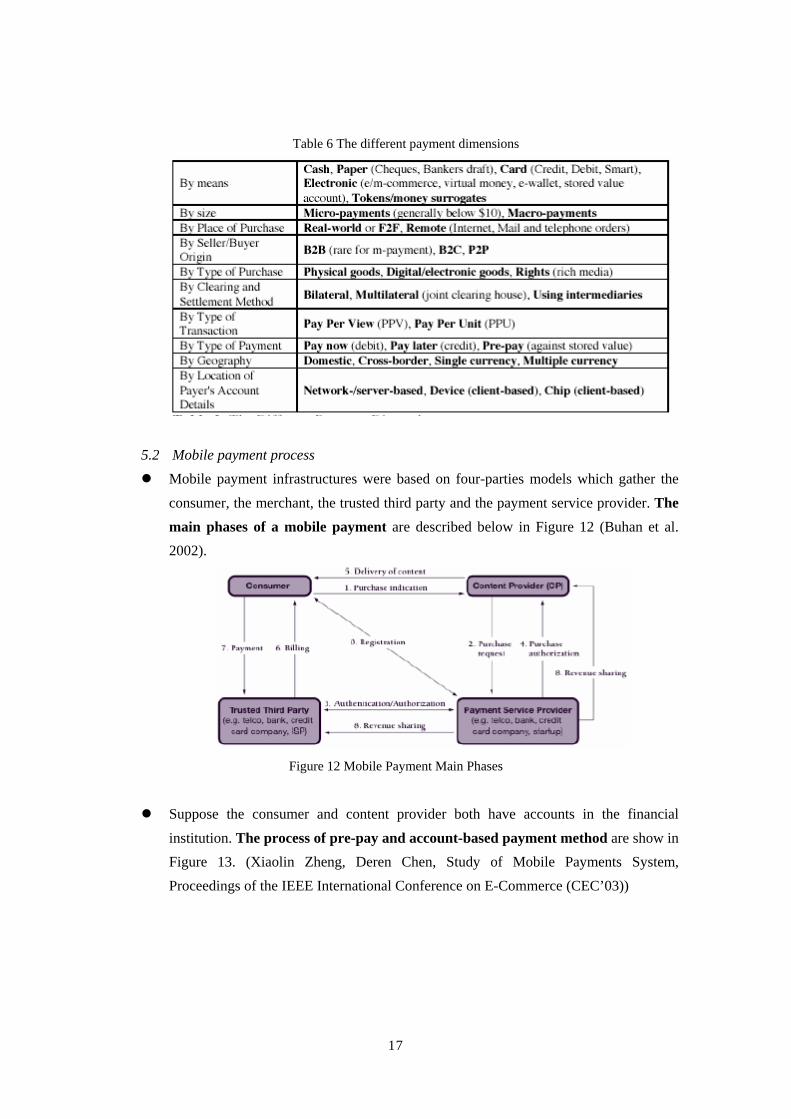

5.2 Mobile payment process Mobile payment infrastructures were based on four-parties models which gather the

consumer, the merchant, the trusted third party and the payment service provider. The main phases of a mobile payment are described below in Figure 12 (Buhan et al. 2002).

Figure 12 Mobile Payment Main Phases

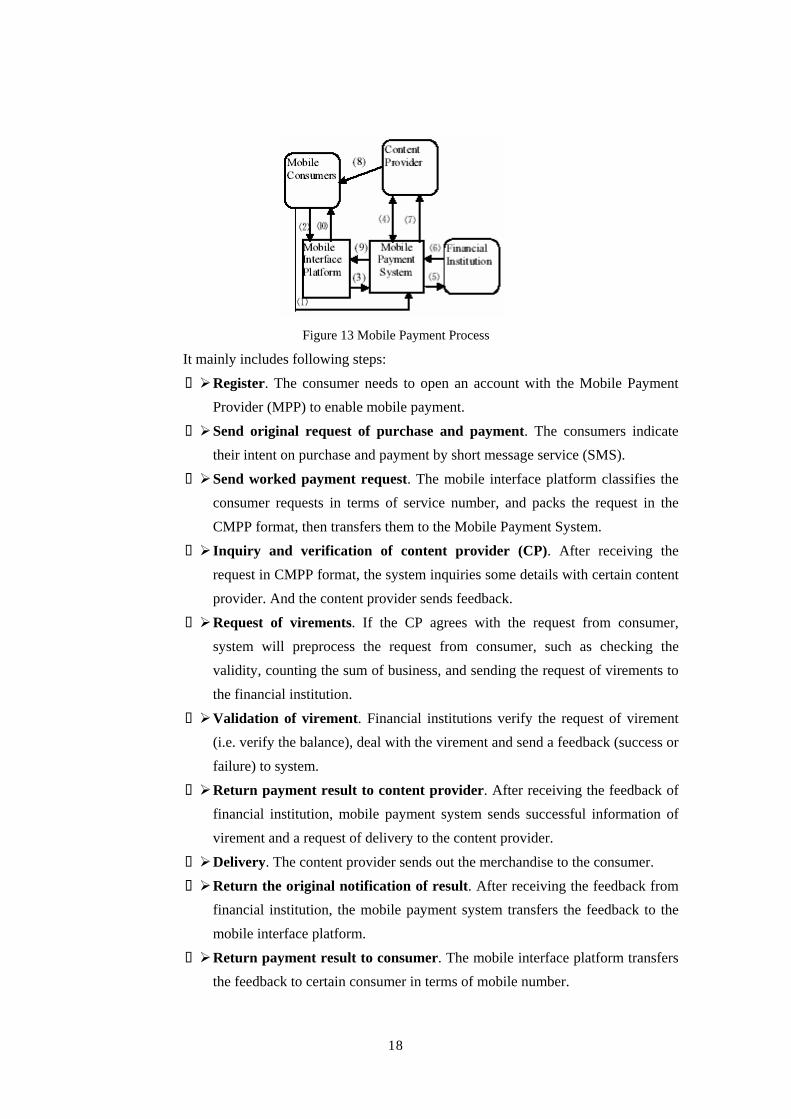

Suppose the consumer and content provider both have accounts in the financial

institution. The process of pre-pay and account-based payment method are show in Figure 13. (Xiaolin Zheng, Deren Chen, Study of Mobile Payments System, Proceedings of the IEEE International Conference on E-Commerce (CEC’03))

18

Figure 13 Mobile Payment Process

It mainly includes following steps:

Register. The consumer needs to open an account with the Mobile Payment Provider (MPP) to enable mobile payment.

Send original request of purchase and payment. The consumers indicate their intent on purchase and payment by short message service (SMS).

Send worked payment request. The mobile interface platform classifies the consumer requests in terms of service number, and packs the request in the CMPP format, then transfers them to the Mobile Payment System.

Inquiry and verification of content provider (CP). After receiving the request in CMPP format, the system inquiries some details with certain content provider. And the content provider sends feedback.

Request of virements. If the CP agrees with the request from consumer, system will preprocess the request from consumer, such as checking the validity, counting the sum of business, and sending the request of virements to the financial institution.

Validation of virement. Financial institutions verify the request of virement (i.e. verify the balance), deal with the virement and send a feedback (success or failure) to system.

Return payment result to content provider. After receiving the feedback of financial institution, mobile payment system sends successful information of virement and a request of delivery to the content provider.

Delivery. The content provider sends out the merchandise to the consumer. Return the original notification of result. After receiving the feedback from

financial institution, the mobile payment system transfers the feedback to the mobile interface platform.

Return payment result to consumer. The mobile interface platform transfers the feedback to certain consumer in terms of mobile number.

19

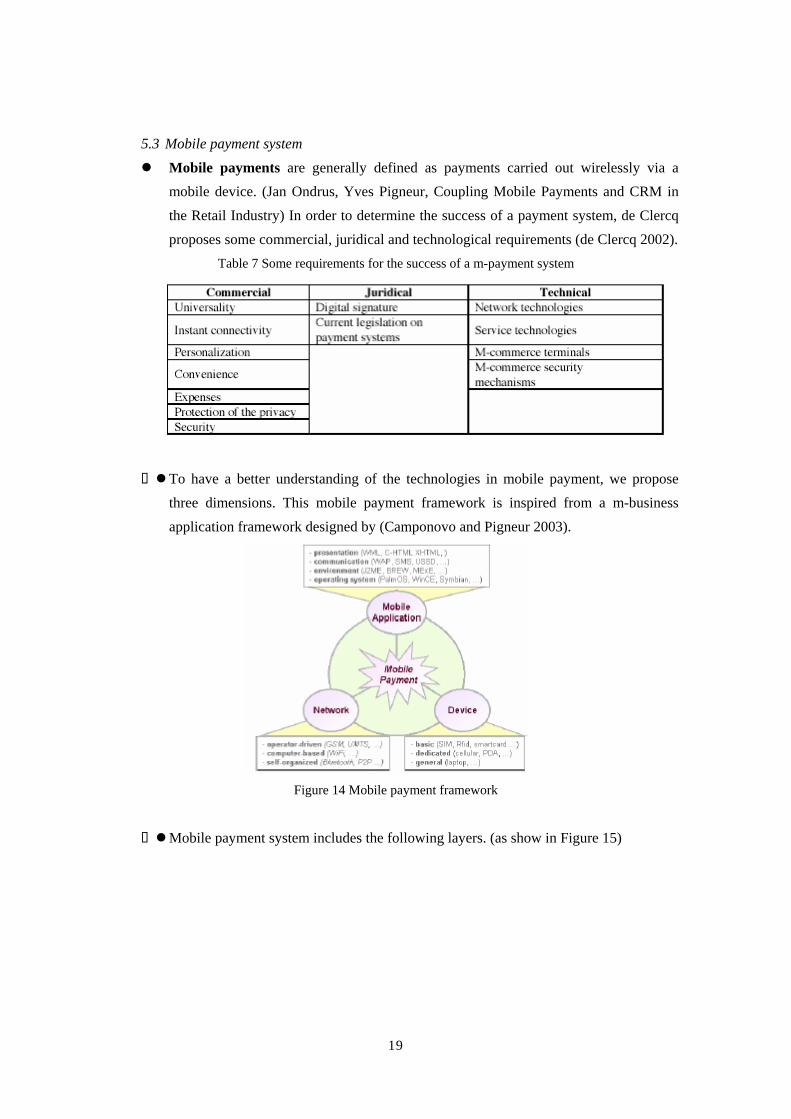

5.3 Mobile payment system Mobile payments are generally defined as payments carried out wirelessly via a

mobile device. (Jan Ondrus, Yves Pigneur, Coupling Mobile Payments and CRM in the Retail Industry) In order to determine the success of a payment system, de Clercq proposes some commercial, juridical and technological requirements (de Clercq 2002).

Table 7 Some requirements for the success of a m-payment system

To have a better understanding of the technologies in mobile payment, we propose three dimensions. This mobile payment framework is inspired from a m-business application framework designed by (Camponovo and Pigneur 2003).

Figure 14 Mobile payment framework

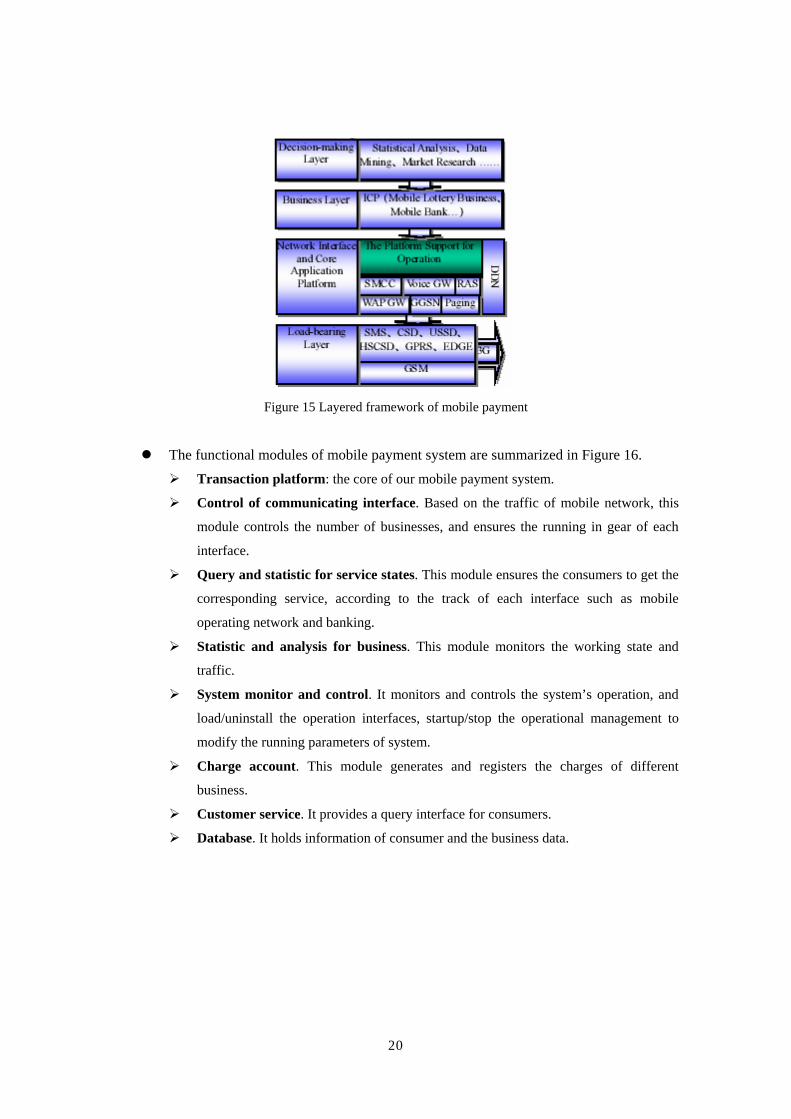

Mobile payment system includes the following layers. (as show in Figure 15)

20

Figure 15 Layered framework of mobile payment

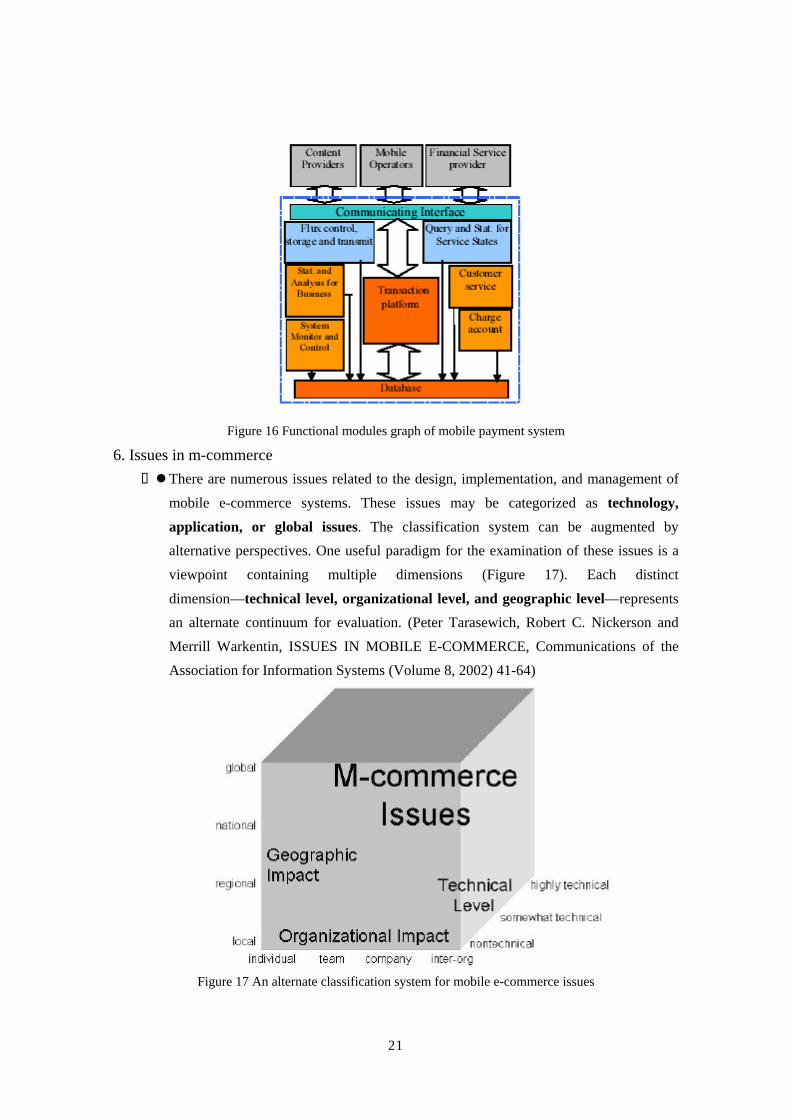

The functional modules of mobile payment system are summarized in Figure 16. Transaction platform: the core of our mobile payment system.

Control of communicating interface. Based on the traffic of mobile network, this

module controls the number of businesses, and ensures the running in gear of each

interface.

Query and statistic for service states. This module ensures the consumers to get the

corresponding service, according to the track of each interface such as mobile

operating network and banking.

Statistic and analysis for business. This module monitors the working state and

traffic.

System monitor and control. It monitors and controls the system’s operation, and

load/uninstall the operation interfaces, startup/stop the operational management to

modify the running parameters of system.

Charge account. This module generates and registers the charges of different

business.

Customer service. It provides a query interface for consumers.

Database. It holds information of consumer and the business data.

21

Figure 16 Functional modules graph of mobile payment system

6. Issues in m-commerce There are numerous issues related to the design, implementation, and management of

mobile e-commerce systems. These issues may be categorized as technology, application, or global issues. The classification system can be augmented by alternative perspectives. One useful paradigm for the examination of these issues is a viewpoint containing multiple dimensions (Figure 17). Each distinct

dimension—technical level, organizational level, and geographic level—represents an alternate continuum for evaluation. (Peter Tarasewich, Robert C. Nickerson and Merrill Warkentin, ISSUES IN MOBILE E-COMMERCE, Communications of the Association for Information Systems (Volume 8, 2002) 41-64)

Figure 17 An alternate classification system for mobile e-commerce issues

22

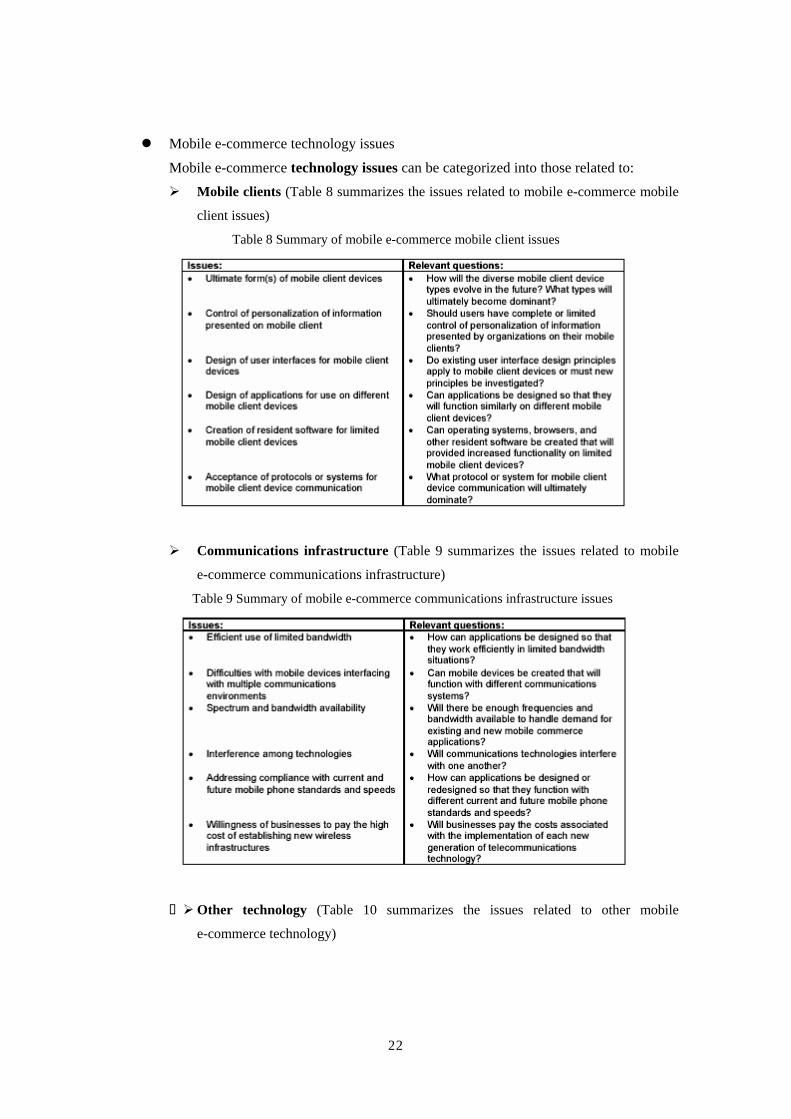

Mobile e-commerce technology issues

Mobile e-commerce technology issues can be categorized into those related to: Mobile clients (Table 8 summarizes the issues related to mobile e-commerce mobile

client issues)

Table 8 Summary of mobile e-commerce mobile client issues

Communications infrastructure (Table 9 summarizes the issues related to mobile

e-commerce communications infrastructure)

Table 9 Summary of mobile e-commerce communications infrastructure issues

Other technology (Table 10 summarizes the issues related to other mobile

e-commerce technology)

23

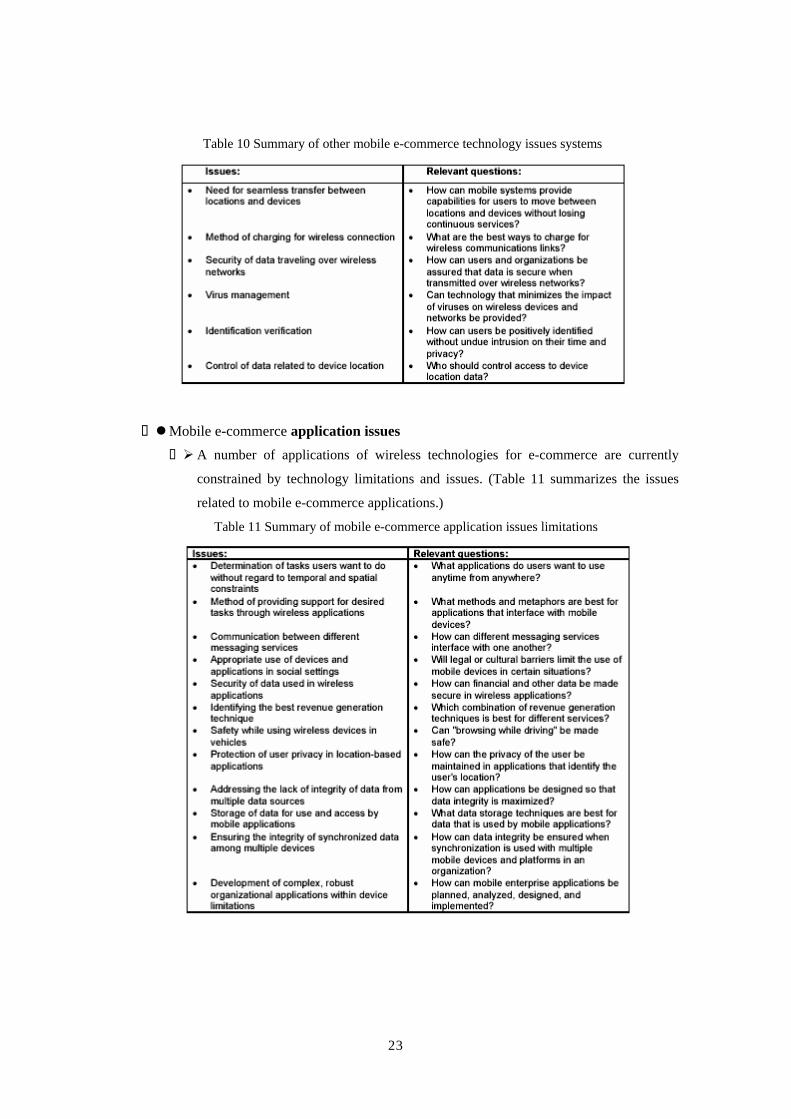

Table 10 Summary of other mobile e-commerce technology issues systems

Mobile e-commerce application issues A number of applications of wireless technologies for e-commerce are currently

constrained by technology limitations and issues. (Table 11 summarizes the issues

related to mobile e-commerce applications.)

Table 11 Summary of mobile e-commerce application issues limitations

24

Mobile e-commerce global issues The global use of wireless technologies and applications adds another layer of

complexity to the issues in m-commerce. This complexity derives from the legal,

cultural, social, political, and technical differences among countries. (Table 12

summarizes the global issues related to mobile e-commerce.)

Table 12 Summary of mobile e-commerce global issues

25

References: ALISHA D. MALLOY, UPKAR VARSHNEY and ANDREW P. SNOW, Supporting Mobile

Commerce Applications Using Dependable Wireless Networks, Mobile Networks and

Applications 7, 225–234, 2002 Aphrodite Tsalgatidou and Jari Veijalainen, Mobile Electronic Commerce: Emerging Issues,

1st International Conference on E-Commerce and Web Technologies, London, Greenwich, UK,

September 4-6, 2000, Lecture Notes in Computer Science, pp. 477-486 Chung-wei Lee, Wen-Chen Hu, Jyh-haw Yeh , A System Model for Mobile Commerce,

Proceedings of the 23rd International Conference on Distributed Computing Systems

Workshops (ICDCSW'03) Emily Yun Zeng, David.C.Yen, Hsin-Ginn Hwang, and Shi-Ming Huang, Mobile Commerce:

The Convergence of E-Commerce and Wireless Technology, International Journal of Advanced

Media & Communications , 2002 GARY SHIH and SIMON S.Y. SHIM, A Service Management Framework for M-Commerce

Applications, Mobile Networks and Applications 7, 199–212, 2002 Giovanni Camponovo, Yves Pigneur, BUSINESS MODEL ANALYSIS APPLIED TO

MOBILE BUSINESS, ICEIS’2003 Jan Ondrus, Yves Pigneur, Coupling Mobile Payments and CRM in the Retail Industry Mylini Munusamy and Hiew Pang Leang, Characteristics of Mobile Devices and an Integrated

M-Commerce Infrastructure for M-Commerce Deployment, Proceedings of the Second

International Workshop on Internet Computing and E-Commerce (ICECE 2002), Florida, USA Peter Tarasewich, Robert C. Nickerson and Merrill Warkentin, ISSUES IN MOBILE

E-COMMERCE, Communications of the Association for Information Systems (Volume 8,

2002) 41-64 Sojen Pradhan, Mobile Commerce in the Automobile Industry, Proceedings of the International

Conference on Information Technology: Computers and Communications (ITCC.03) S. Schwiderski-Grosche and H. Knospe, Secure Mobile Commerce, Electronics &

Communication Engineering Journal, October, 2002 UPKAR VARSHNEY, RON VETTER, Mobile Commerce: Framework, Applications and

Networking Support, Mobile Networks and Applications 7, 185–198, 2002 Upkar Varshney, Ron Vetter, A Framework for the Emerging Mobile Commerce Applications,

Proceedings of the 34th Hawaii International Conference on System Sciences – 2001 Xiaolin Zheng, Deren Chen, Study of Mobile Payments System, Proceedings of the IEEE

International Conference on E-Commerce (CEC’03)