“challenges & opportunities in the used car industry”. how to develop a healthy and...

TRANSCRIPT

“Challenges & opportunities in the used car industry”.

How to develop a healthy and sustainable remarketing

policy in present times as a leasing company”.

Managing Remarketing in a Changing Market

Bucharest, 12 November 2009

Rob M. Henneveld

Global Automotive ConsultancyThinking Global, Performing Local!

AL

B 2

00

9 c

on

fere

nce

Agenda for today

1. Introduction2. What drives the car manufacturer?3. Managing remarketing in an unstable new car

market4. Pricing pressure, sales barriers & -channels 5. Optimizing & managing the sales channels6. Conclusions

2© 2009 Global Automotive Consultancy, the Netherlands/Romania

AL

B 2

00

9 c

on

fere

nce

1. Introduction

3

In a variety of capacities: as an Independent International Business Consultant, Trainer, Coach, Interim- and Project manager, writer of articles and white-papers.

Mostly applied during strategic- & product development, in-depth market research and direct consultancy in areas such as, the (Financial) Service Industry, Aftermarket, Remarketing and IT.

More recently, co-founder and chairman of the Dutch Remarketing Council, objectives: promote Dutch cars throughout Europe, lower trade-barriers among car traders, create a knowledge-center used cars.

Background:Before founding Global Automotive Consultancy, an international in-depth knowledge and diversified automotive experience was acquired.

This developed into a well-balanced vision in a wide range of issues, covering: Car Leasing, Rental, Remarketing, Aftersales, Fleet Management and Insurance – involving a clientele in the wholesale, retail and end-user segments of the supplier-chain.

Active in several countries: the Netherlands, Germany, Belgium, France, Italy, Israel, Turkey, Poland, South-Africa, Spain, Poland and Romania.

© 2009 Global Automotive Consultancy, the Netherlands/Romania

AL

B 2

00

9 c

on

fere

nce

2. What drives the Car Manufacturer?

4© 2009 Global Automotive Consultancy, the Netherlands/Romania

AL

B 2

00

9 c

on

fere

nce

5

Commercial life-cycle shortens:

7-10 yr . => 5-7 yr. =>3-5 yr.

Additional 2x main threats: 1.single production platform & 2.(low) budget cars

Business model determines:

- Every 0,6 sec one car!

China produces mainly for its own use…. but for how long

Overproduction: +15-30%)

Scales of Economics drives production, not market

demand!

Source: AUTOFACTS Global Light Vehicle Assembly Outlook

© 2009 Global Automotive Consultancy, the Netherlands/Romania

AL

B 2

00

9 c

on

fere

nce

6

Per 1.000 inhabitants

In saturated markets: Change in purchase behavior:

Big car = OutSmall/Green car

= InEU /Governments car & cost: from fixed to variable

Low density: Need for mobility potential drives (1) used car market (2) production to CEE-countries

Consumers are in an “ownership-motivation” crisis

© 2009 Global Automotive Consultancy, the Netherlands/Romania

AL

B 2

00

9 c

on

fere

nce

3. Managing remarketing in an unstable (new) car market

7© 2009 Global Automotive Consultancy, the Netherlands/Romania

AL

B 2

00

9 c

on

fere

nce

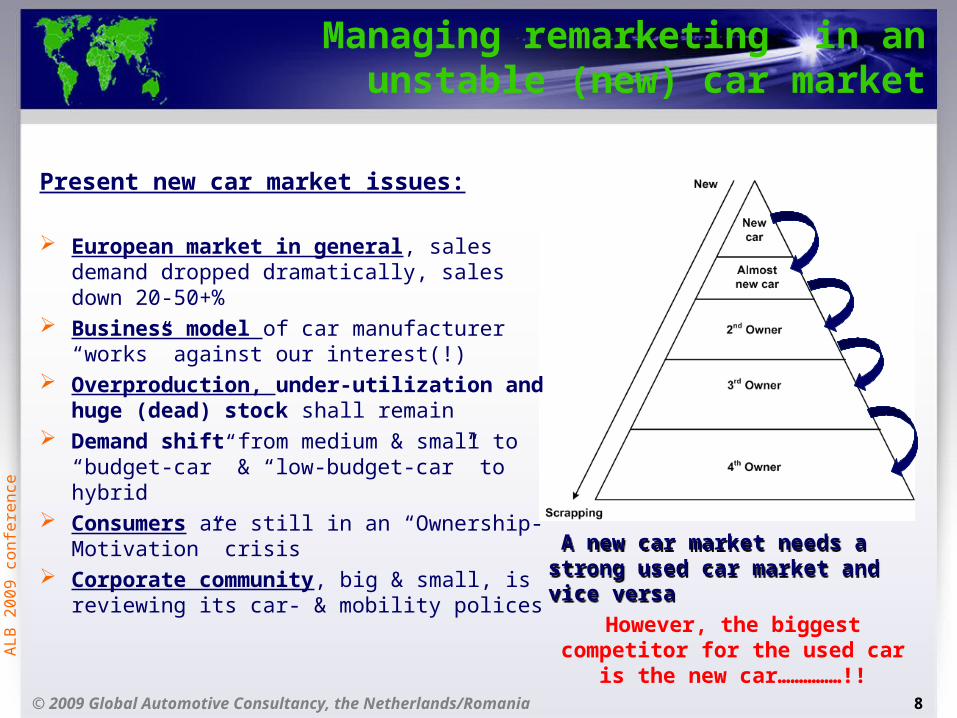

Managing remarketing in an unstable (new) car market

8

A new car market needs a strong used car market and vice versa A new car market needs a strong used car market and vice versa

© 2009 Global Automotive Consultancy, the Netherlands/Romania

Present new car market issues:

European market in general, sales demand dropped dramatically, sales down 20-50+%

Business model of car manufacturer “works” against our interest(!)

Overproduction, under-utilization and huge (dead) stock shall remain

Demand shift from medium & small to “budget-car” & “low-budget-car” to hybrid

Consumers are still in an “Ownership-Motivation” crisis

Corporate community, big & small, is reviewing its car- & mobility polices

However, the biggest competitor for the used car is the new

car……………!!

AL

B 2

00

9 c

on

fere

nce

Used car transaction volumes in Europe

9© 2009 Global Automotive Consultancy, the Netherlands/Romania

Some conclusions:

Volume changes car producing countries

Bigger-volume-countries: value-determining

Romania: no influence on EU-pricing used car

Focus on quality & transparancy is key-factor

As a product, used cars are more stable than the new car…………

Mainland Europe:

Increasingly becomes one market with a pan-European pricing…….

AL

B 2

00

9 c

on

fere

nce

2008-2009: Pricing pressure & power shift

10

A new used car segment!

• Putting extra pressure on the used car value• Usually supplied by the brand-dealer• But also through independent car-traders

Developments:Shift in consumer’s behavior: “ownership- motivation crisis” and more TCO-awareness

Market power shifted from sellers to the buyers

Stigmatizing the new car buyer (private-consumer)

Used car requirements changed during ’08/’09:

• More price orientated, from 10-11k => 5k

• Brand/model less important

• Trustable source (history) (Internet?)

• Fuel type

• etc.

During 2008 sellers’ power shifted to the buyers…

This means that the sellers have to revise their strategy!

© 2009 Global Automotive Consultancy, the Netherlands/Romania

AL

B 2

00

9 c

on

fere

nce

The (large) leasing companies

For the car leasing industry:

A shockwave went through the used car market

Shift of power in ‘08 was big surprise for the leasing industry, who were the first ones to start bleeding,

Consumer wanted a different car (cheaper!) Encountering very confrontational issues, such

as: No solid used car policy in place (afterall: “disposals”) Single sales channel orientated & mainly wholesale Strong process orientation (“allocating cars”) Not sales driven (not adding value) Lack of sales competence among staff Too short internal lead-times Wrong mix of fuel (95-diesel/5% petrol) AND NO CONTINGENCY PLAN

11© 2009 Global Automotive Consultancy, the Netherlands/Romania

Selling the cars within short lead-times, accelerates the drop in car value, making things worse…………

AL

B 2

00

9 c

on

fere

nce

4. Pricing pressure, sales barriers & -channels

12© 2009 Global Automotive Consultancy, the Netherlands/Romania

AL

B 2

00

9 c

on

fere

nce

Changing sales channels

13© 2009 Global Automotive Consultancy, the Netherlands/Romania

On the Internet: what is a good or a bad car?

AL

B 2

00

9 c

on

fere

nce

Optimizing & Basic Remarketing Requirements

Basics: Develop a strategy, with a plan and objectives (core-business??)Create a flexible and Collaborative Platform (Internet) => Apply Virtual

RemarketingIntegrated processing, preferably with back-office systemAll-interaction with stakeholders (service suppliers, buyers, etc.)Lead-time management (incl. transaction benchmarking approach)Drive for uniformity, creates reliability and trustIntake process: Fair, Consistent & Transparent

Some additional objectives:Utilize pre-remarketing period & collect Internet-search behavior ransparent description & uniform presentation of the carPrevent uncertainties of the car’s external & internal conditionEvaluate the “brand-value” of the Internet portalsCreate a Lease Car Standard => Quality-standard of the Car Lease IndustryIssue a “Lease-Voucher” => new owner receives aftersales

discount/service, etc.

14

Optimizing

Remarketing

transactions

has become

crucial!

© 2009 Global Automotive Consultancy, the Netherlands/Romania

AL

B 2

00

9 c

on

fere

nce

Multi-channel sales strategy

15© 2009 Global Automotive Consultancy, the Netherlands/Romania

It is about optimizing transaction result and spreading the risk

AL

B 2

00

9 c

on

fere

nce

Required: purchase barriers

16© 2009 Global Automotive Consultancy, the Netherlands/Romania

Purchase barriers pan-European & local market:

Correct and complete description of the car Insight in the technical state of the car:

Optical, outside & inside Repair/Maintenance history, Inspection: MOT Body repair history Tyre condition, in mm’s, sparewheel? Number of owners (private/company)

Knowledge navigation system (import/export) Countries & language settings

VAT-number buyer & seller Local taxations by import Administration by im- & export

Missing the Certificate of Conformity (CoC)

These barriers are alike for the private-consumer and the professional car trader

By taking them away, you add value to the used car proposition.

Make sure the prospect buyer recognises the good points of your car………..

AL

B 2

00

9 c

on

fere

nce

5. Optimizing & Managing the sales channels

17© 2009 Global Automotive Consultancy, the Netherlands/Romania

AL

B 2

00

9 c

on

fere

nce

5. Managing the Sales Channels

18

•Logistics! •Intake process•Channel allocation!

Pre-Remarketing period & Asset-evaluation

Multi-Channel Remarketing Approach

Wholesales Export Retail Direct

• Auction method: Online & Physical

• Tenders: Open & Closed

• Independent car traders

• Drivers &

• Relatives

• Private sales

•Franchised network

•Dealers

• Independent used car outlets

• Car Supermarkets

• Auctions: Online & Physical

• Independent traders

•Re-lease….•Pre-runner…•Short-rental…• ???

Time

© 2009 Global Automotive Consultancy, the Netherlands/Romania

AL

B 2

00

9 c

on

fere

nce

6. Some conclusions

Business model of car manufacturer “works” against our interest!

Huge stock & under-utilization shall remain Shift from medium & small to “budget-car” & “low-

budget-car” Biggest competitor for the used car is the new car Consumers are entering an “Ownership-Motivation”

crisis Sales management approach is needed Multi-channel strategy is justified, to spread the risk Introduction of “Virtual Remarketing” (Smart-Internet) Reducing traditional purchase barriers is vital to

optimize sales transaction

19© 2009 Global Automotive Consultancy, the Netherlands/Romania

AL

B 2

00

9 c

on

fere

nce

20

Thank You!

Rob M. Henneveld

+31 654921409 or +40 751254551

www.globaucon.com

© 2009 Global Automotive Consultancy, the Netherlands/Romania