chapter 2: the recording process act 201 lecture by: ms. adina malik

TRANSCRIPT

Chapter 2: The Recording Process

ACT 201 LectureBy: Ms. Adina Malik

The Account • Record of increases and decreases in a specific asset, liability

& owner’s equity item.• The format resembles the letter ‘T’, hence referred to as the T

Account• An Account consists of three parts:• A title• Left side, known as debit side• Right side, known as credit side

Title of Account

Debit Credit

Accounting custom/rule

Debits & Credits

Double-entry accounting system

• Commonly abbreviate Debit as ‘Dr.’ and Credit as ‘Cr.’

• Each transaction must affect two or more accounts to keep the basic accounting equation in balance.

• Recording done by debiting at least one account and crediting another.

• DEBITS must equal CREDITS.

Debits & Credits

Debit > Credit = Debit Balance

Title of AccountDebit/Dr. Credit/Cr.$10,000 $ 3,000$ 8,000$ 15,000

Credit > Debit = Credit Balance

Title of Account Debit/Dr. Credit/Cr.$ 10,000 $ 3,000

$ 8,000 $ 1,000

Balance Balance

13

2

Accounting Equation: Reminder

Basis Equation:Assets = Liabilities + Owner’s Equity

Expanded Equation:Assets = Liabilities + (Owner’s Capital Owner’s Drawings + Revenue Expenses)

• The equation must be in balance after every transaction.• For every Debit there must be a Credit.

Debit & Credit Procedure

ASSETS LIABILITIES

Chapter 3-23

AssetsAssets

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Chapter 3-24

LiabilitiesLiabilities

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Normal Balance is on the increase side

Debit & Credit Procedure: Owner’s Equity

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Owners’ EquityOwners’ Equity

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Owners’ CapitalOwners’ Capital

Chapter 3-23

Owners’ DrawingOwners’ Drawing

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Debit & Credit Procedure: Owner’s Equity

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Owners’ EquityOwners’ Equity

Chapter 3-26

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

RevenueRevenue

Chapter 3-27

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

ExpenseExpense

Normal Balance

‘Normal Balance is on the increasing side’ means that:

Normal Balance for Assets, Owner’s Drawings and Expenses is on the Debit side.

Normal Balance for Liabilities, Owner’s Capital and Revenue is on the Credit side.

Debit & Credit Rules

Summary

Question 1

Question 2

Steps in the Recording Process

Source documents, such as a sales slip, a check, a bill, or a cash register tape, provide evidence of the transaction.

Three basic steps generally in every business:• Analyze each transaction for its effects on the accounts.• Enter the transaction information in a journal.• Transfer the journal information to the appropriate accounts in the ledger.

Journal• It discloses in one place the complete effects of a transaction

(debit & credit effects)• It provides a chronological record of transactions.• As debit & credit amounts for each entry can be easily

compared, it helps to prevent or locate errors.• Also known as ‘General Journal’ or ‘The Book of Original

Entry’.

GENERAL JOURNAL

Date Account Titles and Explanation Ref. Debit Credit

Simple & Compound Entries

• Entering transaction data in the journal is known as journalizing.• It is important to use ‘correct’ & ‘specific account titles’ in

journalizing. • Simple Entry: entry which involves only two accounts, one debit and

one credit.• Compound Entry: entry that requires more than two accounts in

journalizing. E.g. Butler company purchases a delivery truck costing $14,000. ($8,000 paid in cash now and to pay the remaining $6,000 on account)

Date Ref. Debit Credit1 $14,000

$8,000$6,000

GENERAL JOURNALAccount Titles and Explanation

Delivery Truck Cash Accounts Payable(Purchased truck for cash with balance on account)

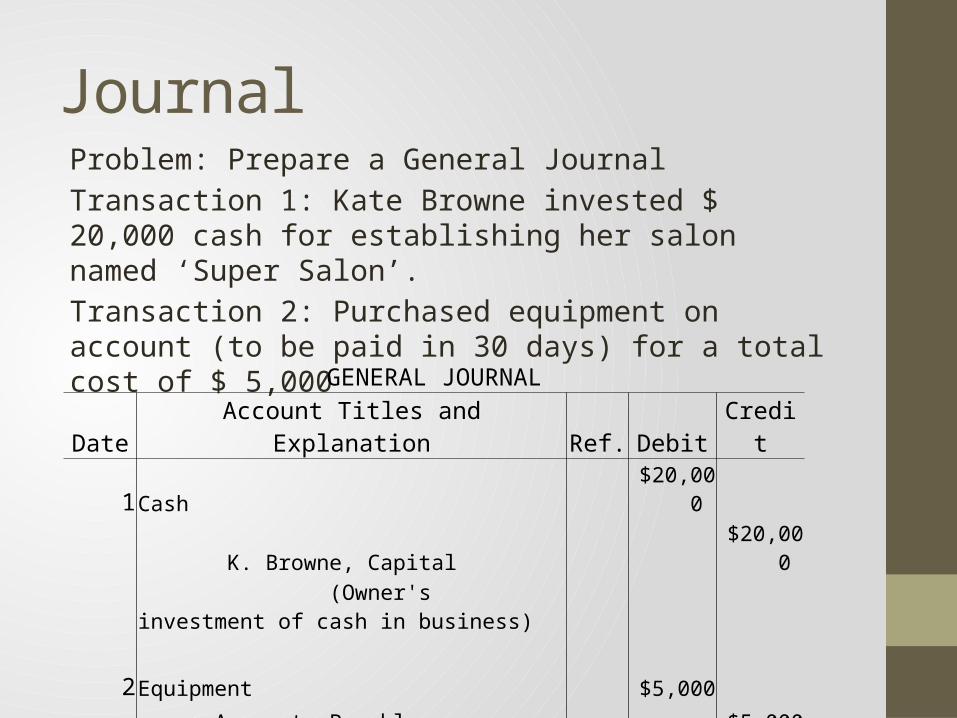

JournalProblem: Prepare a General JournalTransaction 1: Kate Browne invested $ 20,000 cash for establishing her salon named ‘Super Salon’.Transaction 2: Purchased equipment on account (to be paid in 30 days) for a total cost of $ 5,000

GENERAL JOURNALDate Account Titles and Explanation Ref. Debit Credit

1Cash $20,000 K. Browne, Capital $20,000 (Owner's investment of cash in business)

2Equipment $5,000 Accounts Payable $5,000 (Purchase of equipment on account)

The Ledger• It is the entire group of accounts maintained by a company.• It keeps in one place all the information about changes in

specific account balances.• A General Ledger contains all the asset, liability & owner’s

equity accounts.

Individual Assets Accounts

• Cash• Land• Equipment• Supplies• Etc.

Individual Liability Accounts

• Accounts Payable• Salaries Payable• Notes Payable• Interest Payable• Etc.

Individual Owner’s Equity Accounts

• Salaries Expense• Service Revenue• K. Browne,

Capital• K. Browne,

Drawings• Etc.

Posting ‘Journal Entry’ into ‘The Ledger’

Transaction 1:

Debit $ Credit $

K. Browne, Capital 20,000

Cash

Debit $ Credit $

Cash 20,000

K. Browne, Capital

Posting ‘Journal Entry’ into ‘The Ledger’

Transaction 2:

Debit $ Credit $ Accounts Payable 5,000

Equipment

Debit $ Credit $ Equipment 5,000

Accounts Payable

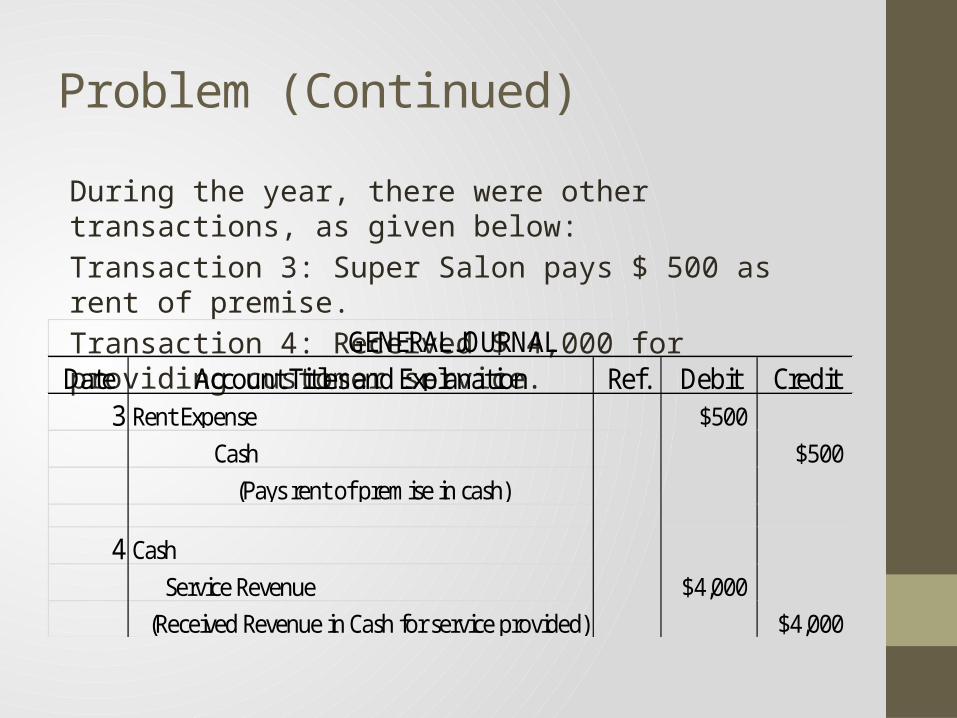

Problem (Continued)

During the year, there were other transactions, as given below:Transaction 3: Super Salon pays $ 500 as rent of premise. Transaction 4: Received $ 4,000 for providing customer service.

Date Ref. Debit Credit3 $500

$500

4$4,000

$4,000

Rent Expense Cash (Pays rent of premise in cash)

Cash Service Revenue (Received Revenue in Cash for service provided)

Account Titles and ExplanationGENERAL JOURNAL

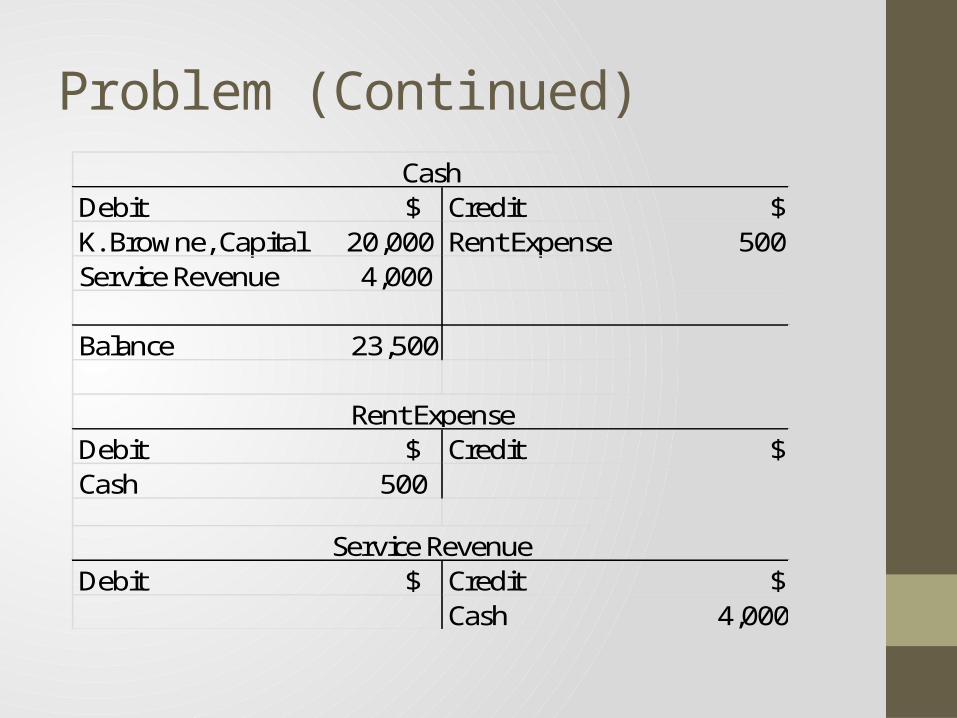

Problem (Continued)

Debit $ Credit $ K. Browne, Capital 20,000 Rent Expense 500Service Revenue 4,000

Balance 23,500

Debit $ Credit $ Cash 500

Debit $ Credit $ Cash 4,000

Cash

Rent Expense

Service Revenue

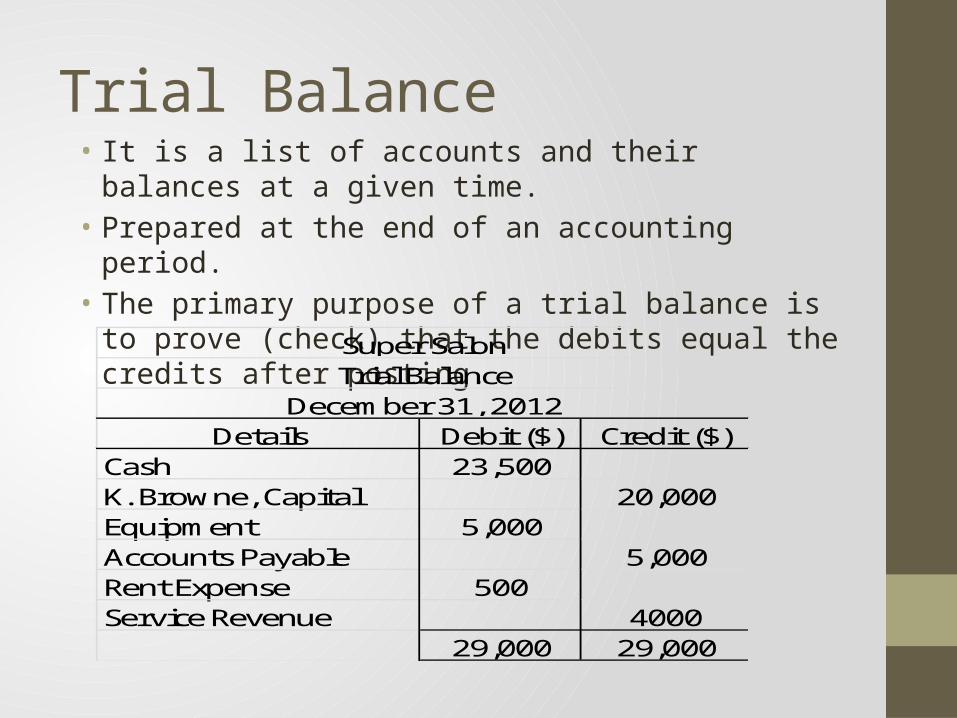

Trial Balance• It is a list of accounts and their balances at a given time.• Prepared at the end of an accounting period.• The primary purpose of a trial balance is to prove (check) that

the debits equal the credits after posting.

Details Debit ($) Credit ($)Cash 23,500K. Browne, Capital 20,000Equipment 5,000Accounts Payable 5,000Rent Expense 500Service Revenue 4000

29,000 29,000

Super SalonTrial Balance

December 31, 2012

Limitations of a Trial Balance

The trial balance may balance even when:

• A transaction is not journalized

• A correct journal entry is not posted

• A journal entry is posted twice

• Incorrect accounts are used in journalizing or posting, or

• Offsetting errors are made in recording the amount of a transaction

Question

QuestionBob Sample opened the Campus Laundromat on September 1, 2010. During the first month of operations, the following transactions occurred.Sept.1 Bob invested $20,000 cash in the businessSept.2 The company paid $1,000 cash for store rent for Sept.Sept.3 Purchased washers & dryers for $25,000, paying

$10,000 in cash and $15,000 on accountSept.4 Received a bill from the Daily News for advertising the

opening of the Laundromat $200Sept.10 The company owes employee salaries of $2,000 and

pays them in cashSept.20 Bob withdraw $700 cash for personal useSept.30 The company determined that cash receipts for

laundry services for the month were $6,200

(a) Journalize the September transactions(b) Open ledger accounts and post the September transactions(c) Prepare a trial balance at September 30, 2010