chapter 9 technolog and industry

TRANSCRIPT

- -

Chapter 9

Technology and Industry

— —

ContentsPage

Importance of Information Technology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 307Findings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 307

Composition of Information Technology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 308Functions .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 308Examples of System Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 309

Characteristics of theU.S. Information Technology Industry . . . . . . . . . . . . . . . . . . . . . 316Employment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 317International Trade . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 317Industry Structure . . . . . . . . . ..., . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . , . . . . . . . . . . 320Small Entrepreneurial Firms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .......321

Where the Technology is Heading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 323Microelectronics. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 324Silicon Integrated Circuits. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 324Gallium Arsenide Integrated Circuits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 328The Convergence of Bio-technology and Information Technology . . . . . . . . . . . . . . . . 330Software . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 331The Changing Role of Software in Information Systems . . . . . . . . . . . . . . . . . . . . . . . 332The Software Bottleneck . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 333Software and Complexity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 334Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 335

TablesTable No. Page50. Functions, Applications, and Technologies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30951. Characteristics of Human Workers, Robots,

and Nonprogrammable Automation Devices. . . . . . . . . . . , . . . . . . , . . . . . . . . . , . 31252. Comparison of the U.S. Information Technology Industry

With Composite Industry Performance, 1978-82 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31753. Employment Levels in the U.S. Information Technology Industries . . . . . . . . . . . . 31854.U.S. Home Computer Software Sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32055.U.S. Office Computer Software Sales. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32156. Percentage of Total industry Sales and Employment

by Size of Small Businesses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32257. Venture Capital Funding and Information Technology Firms, 1983 . . . . . . . . . . . . . 32358. ICs Made With Lithographic Techniques . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32659. Software Sales by Use , . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 332

FiguresFigure No. Page52. Direct Broadcasting Satellite System . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31153. The Changing Structure and Growth of the

U.S. Information Technology Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31854. Balance of Trade, Information Technology Manufacturing Industry . . . . . . . . . . . . 31955. U.S. Trade Balance with Selected Nations

for R&D Intensive Manufactured Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31956. Historical Development of the Complexity of Integrated Circuits . . . . . . . . . . . . . . 32457. Read-Only Semiconductor Memory Component Prices by Type . . . . . . . . . . . . . . . . 32558. Median Microprocessor Price v. Time . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32559. Minimum Linewidth for Semiconductor Microlithography . . . . . . . . . . . . . . . . . . . . . 32660. A Schematic of an Electron Beam Lithography System, and Its Use to Make

LSI Logic Circuits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32761. Trends in Device Speed–Stage Delay

per Gate Circuit for Different Technologies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32862.The Relative Costs of Software and Hardware. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 332

Chapter 9

Technology and Industry

Importance of Information Technology

Information technology and the industriesthat advance and use its products are becom-ing increasingly important to America’s eco-nomic strength. Information technology is acore technology, contributing broadly to theNation’s trade balance, employment, and na-tional security. The information sector alreadyaccounts for between 18 and 25 percent of thegross national products of seven of the mem-ber nations of the Organization for EconomicCooperation and Development (OECD) and be-tween 27 and 41 percent of employment int h e s e c o u n t r i e s .12 2

An important characteristic of this technol-ogy is the rapidity with which research resultsare translated into “advanced” products andfrom there to the mainstream consumer market-place. This rapid transfer has been particularlyevident in semiconductor research leading tocheaper and more powerful microprocessors .

G i v e n t h e a c c e l e r a t e d m o v e m e n t f r o m t h eresearch laboratories to a worldwide market-place , i t i s natural that the at tent ion of thet r a d i n g n a t i o n s h a s f o c u s e d o n i n f o r m a t i o ntechnology research and development (R&D).Two basic building blocks of information tech-nology are:

● t h e m i c r o e l e c t r o n i c c h i p - t h e l a r g e s c a l eintegrated c ircuit that permits the stor-age , rapid retr ieval and manipulat ion ofvast amounts of information, and

● s o f t w a r e - t h e s e t s o f i n s t r u c t i o n t h a t d i -rect the computer in i ts tasks .3

As noted in chapter 2 , there i s no consen-sus on what composes the “ informat ion tech-

‘Information Activities, Electrom”cs and Tekwomtnum”cationsTechnologies: Impacts on Employment, Growth and Trade(OECD, Paris, 1981), pp. 22 and 24.

‘M. R. Rubin, Information Econom”cs and Policy in theUnited States, Libraries Unlimited, Littleton, CO, 1983,pp. 32-44.

3Software may also refer to the stored information.

nology industry. ” Because of the varyingdefinitions and the differing statistical anal-yses arising from them, it is impossible to pindown the size of the industry. A relatively con-servative estimate, discussed later in thischapter, places the annual sales of the U.S. in-dustry at over two hundred billion annuallyand growing. From another perspective: overone-half million jobs depend on computer in-dustry exports .4

Findings

In examining the composition of informa-tion technology, the characteristics of the U.S.industry, and where the technology is heading,several trends become apparent:1.

2.

3.

The U. S. information technology industryis large and growing rapidly; there is a worldmarket for its products and services as thedeveloped countries increasingly move intothe information age.The technology is pervasive, making pos-sible major productivity improvements inother fields, creating new industries, andenlarging the range of services available tothe public. The technology diffuses throughmost facets of life, including business, engi-neering and science, and government func-tions.With each level of technological advance inbasic information technology, the level ofcomplexity and cost increases for R&D, asdoes the demand for additional technicaltraining for R&D personnel.

‘Robert G, Atkins, The Computer Industry and InternationalTrade; A Summary of the U.S. Role, Information ProcessesGroup, Institute for Computer Sciences and Technology, Na-tional Bureau of Standards, December 1983, p. IX-1. Draft ofa report under joint development by ICST and the InternationalTrade Administration, as of February 1985.

307

308 • information Technology R&D: Critical Trends and Issues

4. Domestic and foreign competition for world 5.markets is both intensive and escalating.The stakes for the United States are greatin terms of corporate sales and competitiveness in world markets, and employment.

There will be continued rapid advances inthe capabilities of the industry’s underlyingbasic building blocks, microelectronics andsoftware.

Composition of Information TechnologyIndividual information technologies have

grown explosively in technical sophisticationand, at the same time, diminished in cost. Thatrare combination has propelled the new tech-nologies into the mass marketplace. As thetwo basic building blocks continue their ad-vances, the parade of new information tech-nology capabilities and applications will go on.

There is a recurrent pattern in which onetechnological advance makes possible stillother advances, often in a “bootstrap” fash-ion. For example, sophisticated computer-aided design (CAD) equipment is a tool usedin development of state-of-the-art random ac-cess memories and microprocessors; develop-ment of the next generation of super-comput-ers depends on use of today’s most advancedcomputers; “expert” systems— still in theirtechnological infancy-are already employedin configuring complex computer systems andcustom-designing integrated circuits.

Functions

For purposes of this report, the term “infor-mation technology” has been used to refer tothe cluster of technologies that provide the fol-lowing automated capabilities:

1.

2.

Data Collection. Examples of automateddata collection systems range from large-scale satellite remote-sensing systemssuch as weather satellites to medical ap-plications such as CAT-scans and elec-trocardiograms.Data Input. Input devices include the fa-miliar keyboard, optical character read-ers, video cameras, and so on. They arethe means by which data are inserted andstored, communicated, or processed.

3.

4.

5.

6.

Information Storage. The storage mediaassociated with the information industryare the electronic-based devices whichstore data in a form which can be read bya computer. They include film, magnetictape, floppy and hard disks, semiconduc-tor memories, and so on. The ability tostore increasingly vast amounts of datahas been essential to the information tech-nology revolution.Information Processing. Information proc-essing is the primary function of a com-puter. The information stored by acomputer can be numeric (used for com-putations), symbolic (rules of logic usedfor applications such as “expert” sys-tems), or image (pictorial representationsused in applications such as remote map-ping). The stored information–in what-ever form—is manipulated, or processed,in response to specific instructions (usu-ally encoded in the software). The increas-ing speed of information processing hasbeen another essential factor in the infor-mation technology revolution.Communications. Electronic communica-tions utilizes a variety of media-the airwaves (for broadcast radio and television),coaxial cable, paired copper wire (used,among other things, for traditional tele-phony), digital radio, optical fibers, andcommunications satellites. Communica-tions systems play a major role in broaden-ing the use of other facets of informationtechnology and make possible distributedcomputing, remote delivery of services,and electronic navigation systems, amongmany other applications.Information Presentation. Once the infor-mation has been sent, it must be “pre-

‘ ~

Ch, 9–Technology and Industry ● 309

sented” if it is to be useful. This can beaccomplished through a variety of outputdevices. The most common display tech-nology is the cathode ray tube or videodisplay terminal. Hard-copy output de-vices include the most commonly used im-pact printers as well as those using non-impact technologies such as ink-jet andxerography. There are also audio systemsthat permit the computer to “speak”-exemplified by the automobiles that ad-monish you to fasten your seat belts.

Table 50 shows some of the technologies andapplication areas that depend on these functions.

Examples of System Applications

A few examples of the many informationtechnology applications are provided below.They have been chosen to illustrate the diver-sity of applications, and in most cases reflectcapabilities that have only become feasible ona significant scale in recent years. The ex-amples include: cellular mobile radio commu-

table 50.—Functions, Applications, and Technologies”

RepresentativeFunction Typical application areaa information technology

Data collection Weather prediction

Medical diagnosis

Data input Word processingFactory automationMail sorting

Storage ArchivesAccounting systemsScientific computation

Information processing

Ecological mappingLibrariesSocial Security payments

Traffic controlDistributed inventory control

Medical diagnosesEngineering designScientific computation

Communications

Ecological mappingFactory automation

Office systems

TeleconferencingRescue vehicle dispatchInternational financial

transactions

Data output and presentation Word processing

Management informationPedestrian traffic control

Radar, infra-red object detection equipment,radiometers

CAT-scanners, ultrasonic cameras

Keyboards, touch-screensVoice recognizes (particularly for quality control)Optical character readers

Magnetic bubble devices, magnetic tapeFloppy disksWafer-scale semiconductors (still in research phase),

very-high-speed magnetic coresCharge-coupled semiconductor devices, video disksHard disksGeneral purpose “mainframe” computers, COBOL

programsMinicomputersMulti-user super-micros, application software

packages“Expert” systemsSpreadsheet application packages, microcomputersSupercomputers: multiple instruction-multiple data

(MI MD) processors, vector processors, data drivenprocessors, FORTRAN programs

Array processors, associative processorsRobotics, artificial intelligenceLocal area networks, private branch exchanges (PBX),

editor applications packagesCommunications satellites, fiber opticsCellular mobile radiosTransport protocols, data encryption, Integrated

Services Digital Networks (ISDN)

Personal computers, printers (impact, ink jet,xerographic)

Cathode ray tubes, computer graphicsVoice synthesizers

aThi~ list is not ~xhau~tive; any given technology may also be used for some of the other applications mentioned.

SOURCE Office of Technology Assessment.

310 . Information Technology R&D: Critical Trends and Issues

nications, direct broadcast satellites, robotics,computer simulation, a biomedical applicationin heart pacemakers, and financial services.

Cellular Mobile Radio CommunicationsFor decades, use of mobile telephone serv-

ice has been limited by over-crowding of theelectromagnetic spectrum; major cities havehad only some few hundred subscribers be-cause of spectrum constraints. Demand for ad-ditional mobile voice service has been grow-ing at a 12 percent rate annually for the past20 years. A new technology-cellular mobileradio communications—holds promise forvastly increasing the number of potentialsubscribers (to more than 100,000 in particu-lar geographic areas),’ while providing serv-ice of improved quality compared to that availa-ble previously. What is most significantabout the cellular concept is that it permitsconservation of the electromagnetic spectrum—a limited natural resource.

The older technology provided service froma single antenna to the area served. The cel-lular concept is based on dividing the servicearea into a number of geometric shapes, orcells, each served with its own antenna. Thecell antennas are interconnected with leasedtelephone lines. When a vehicle leaves a cell,that cell passes control to the next cell, andso on. The number of subscribers is muchgreater with the cellular concept because thetransmission frequencies can be reused re-peatedly in nonadjacent cells. Thus the impactof increasing demands on the spectrum is min-imized.

According to some estimates, cellular radiowill be a $4 billion U.S. industry by 1990 andcould reach $6 billion by the mid-1990s. Cel-lular mobile telephones recently cost about$3,000 but prices are likely to fall rapidly be-cause of competition among vendors.

Other countries are also finding considerabledemand for mobile radio services. In Japan,

60peration of cellular mobile radio systems in dozens of U.S.cities has been approved by the Federal Communications Com-mission.

mobile telephone services are now available inTokyo. In Spain, some 20,000 subscribers areanticipated by 1990. The Netherlands reachedapproximately 50,000 inhabitants by 1984.Saudi Arabia introduced cellular mobile radiocommunications in 1981 in three cities; by1982, there were 19,000 subscribers, and theSaudis have now extended coverage to 32cities.

Direct Broadcast SatellitesThe use of direct broadcast satellites (DBS)

has recently become feasible. With DBS, over-the-air signals (e.g., TV, radio) can be receiveddirectly by small rooftop antennas (see fig. 52).These new, commercial, geostationary sys-tems may have widespread use in the UnitedStates and in other countries, primarily pro-viding entertainment, but also with potentialfor education, advertising and other businessuses. As of early 1985, nine applications had

Photo credit: Motorola

Mobile cellular radiotelephone

Ch. 9—Technology and Industry ● 311

Figure 52.—Direct Broadcasting Satellite System

, Indoor unit

been approved by the Federal Communica-tions Commission (FCC) for subscription serv-ices to the public, some of which may becomeoperational.

DBS services will compete with other mediasuch as multiple distribution systems, STV(subscription TV), and cable TV (CATV) forserving television viewers. DBS services mayprove especially valuable for providing serv-ice to sparsely populated geographical areasthat are not economical to reach by othermeans, as well as to densely populated citieswhere new cable installations are prohibitivelyexpensive.

Among the technical improvements thatmake DBS systems feasible are higher powerand more efficient on-board power amplifiers;solar power generation equipment; more ac-curate satellite station-keeping control; im-proved ground receiver sensitivity; the use ofhigher frequencies; and better transmitterdownlink beam control. Higher power andhigher frequencies also make practical the useof small (about 1 meter or less) rooftop an-tennas. Some of the early U.S. experimentalsatellite communications systems, along withparallel advances in solid-state electronics andnew materials processing techniques, havecontributed significantly to the improvements

in components and subsystems availabletoday.

DBS systems had their genesis when NASA’sATS-6 satellite was launched in 1974—a sys-tem having a multiplicity of payloads, two ofwhich included TV broadcast capabilities. Anumber of countries have DBS systems inplace or in planning stages. Included amongthese are: Canada’s medium-powered ANIKC-2, which is serving Canadian audiences aswell as providing five channels of televisionentertainment to the Northeastern UnitedStates; Japan’s modified BS-2 satellite, launchedin early 1984; and France’s TDF-1 and WestGermany’s TV-SAT, which are expected to beoperational in 1986.

RoboticsRobots are mechanical manipulators which

can be programmed to move workplaces ortools along various paths. They are one of thefour tools employed in computer-aided manu-facturing (i.e., robots, numerically controlledmachine tools, flexible manufacturing sys-tems, and automated materials handlingsystems).6

Robotics emerged as a distinct disciplinewhen the century-old industrial engineeringautomation technologies converged with themore recent disciplines of computer scienceand artificial intelligence. The convergenceproduced the growing field of robotics, whichhas had wide factory applications in areas thatinclude (but are not limited to) materials han-dling, machine loading/unloading, spray paint-ing, welding, machining, and assembling. Therobots are most often used in performing par-ticularly hazardous and monotonous jobswhile offering enough flexibility to be easilyadapted to changes in product models.

Neither today’s robots, nor those likely tobe available in the next decade, look likehumans nor do they have more than a fractionof the dexterity, flexibility, or intelligence ofhumans. A simple “pick and place” machine

‘See Computerized Manufacturing Automati”on: Employment,Education, and the Workplace (Washington, DC: U.S. Congress,Office of Technology Assessment, OTA-CIT-235, April 1984.

38-8o2 0 - 85 - 21

312 ● Information Technology R&D: Critical Trends and Issues

with two or three degrees of freedom may costroughly between $5,000 and $30,000, whilemore complex progr ammable models, oftenequipped with microcomputers, begin at about$25,000 and may exceed $90,000.

Human workers, robots, and nonprogram-mable automation devices each have certaincharacteristics which offer advantages for themanufacturing process. Table 51 comparessome of the salient characteristics.

Table 51 .—Characteristics of Human Workers,Robots, and Nonprogrammable Automation Devicesa

Non programmableHuman Automation

Characteristic Worker Robot Device

Flexibility . . . . . . . . . . 1Consistency. . . . . . . . 3Endurance . . . . . . . . . 3Ability to tolerate

hostileenvironments. . . . . . 3

cost . . . . . . . . . . . . . . n/aSpeed . . . . . . . . . . . . . 2-3Intelligence/

programmability . . 1Sensing . . . . . . . . . . . 1Judgment. . . . . . . . . . 1Ability to adapt

to change. . . . . . . . 1Dexterity. . . . . . . . . . . 1

22

1-2

1-22

2-3

222

22

31

1-2

1-211

333

33

aNumerical ranking indicates relative advantage, With “l” Indicating the greatestadvantage.

SOURCE: Computerized Manufacturing Automation: Employment, Education,and the Workp/ace, (Washington, DC: U.S. Congress, Office ofTechnology Assessment, 1964). This table was derived from the fore-going report

At the end of 1983 Japan had about 43,000operating robot installations-by far the larg-est number in any country. The United States,where the original patents for robots were ob-tained, had about 9,400 installations (v. about13,000 in early 1985 and 6,300 in 1982), fol-lowed by West Germany (4,800), and France(3,600). Some projections indicate that by 1990there will bean installed base of nearly 90,000robots in the United States. *

As reported by OTA6a, significant roboticsresearch is being conducted in over a dozenuniversities, about three dozen industrial firmsand independent laboratories, and in FederalGovernment labs at the National Bureau ofStandards (NBS), NASA, and DOD. The re-port further noted that the research was in-tensively addressing several problem a r e a s :improved positioning and accuracy for the ro-bot’s arms; increased grace, dexterity, andspeed; sensors, including vision, touch, andforce; model-based control systems; software;mobility; voice recognition; artificial intelli-gence; and interface standards. The interfacearea is critical to widespread use of automatedmanufacturing. NBS has created an Auto-mated Manufacturing Research facility in partto perform research on the interfaces betweendifferent computerized devices in a factory.

Computer Simulation

“Computer simulation” is a process thatemploys a computerized model of certain sig-nificant features of some physical or logicalsystem which is undergoing dynamic change.We therefore find computers used in applica-tions such as economic modeling and wargames where “what if” scenarios can be playedout to test suggested social policies or militarystrategies. As relatively inexpensive computermemories grow in size and integrated circuitsgrow in speed, increasingly complex opera-tions are being modeled. Software advanceshave also played a large part in the growinguse of computer simulations.

*worldwide Robotics Survey ~d D&toW, 1984, to ~ pub-lished, Robotics Industries Association, Dearborn, MI. Thisdata is based on the RIA’s definition for robots which excludesthe simpler, nonreprogr amrnable machines.

@Compute~~ M~ufactufl-ng Automation: Employment,Education and the Workplace, op. cit.

Ch. 9–Technology and Industry ● 313

When combined with other informationtechnologies, some startling simulations arepossible. In flight simulators, for example,computer-generated imagery techniques areused to create background, images, sounds,and sensations, and to position discrete ele-ments in a scene—elements which have beenobtained from video images of real trees,buildings, clouds, aircraft, and other charac-teristics of the environment to be simulated.The flight simulator is placed in the dynam-ically changing recreated environment and thepilot then “flies through” in the simulator,which duplicates the performance of the actualairplane. Realistic simulations are made pos-

sible by the rapid calculation and implemen-tation of flight characteristics related to theknown aerodynamic and engine properties ofthe craft, air speed, altitude, attitude, and lift.Some systems use 10,000 variables associatedwith a single-engine jet fighter. In order toachieve visual accuracy, simulator systemscalculate the aircraft’s position between 25and 60 times per second.

The Federal Aviation Administration per-mits 100 percent simulation training for ex-perienced pilots who are upgrading their flightcertifications to more advanced aircraft. Simu-

314 . /formation Technology R&D: Critical Trends and Issues

lated dogfight training at Williams Air ForceBase is so realistic that some F-4 pilots havebecome airsick.7

Computer simulation is proving effective forimproving the quality of training in a varietyof jobs—e.g., operating a locomotive, control-ling a supertanker, operating a space shut-tle—while reducing the cost, time, and riskassociated with conventional training.

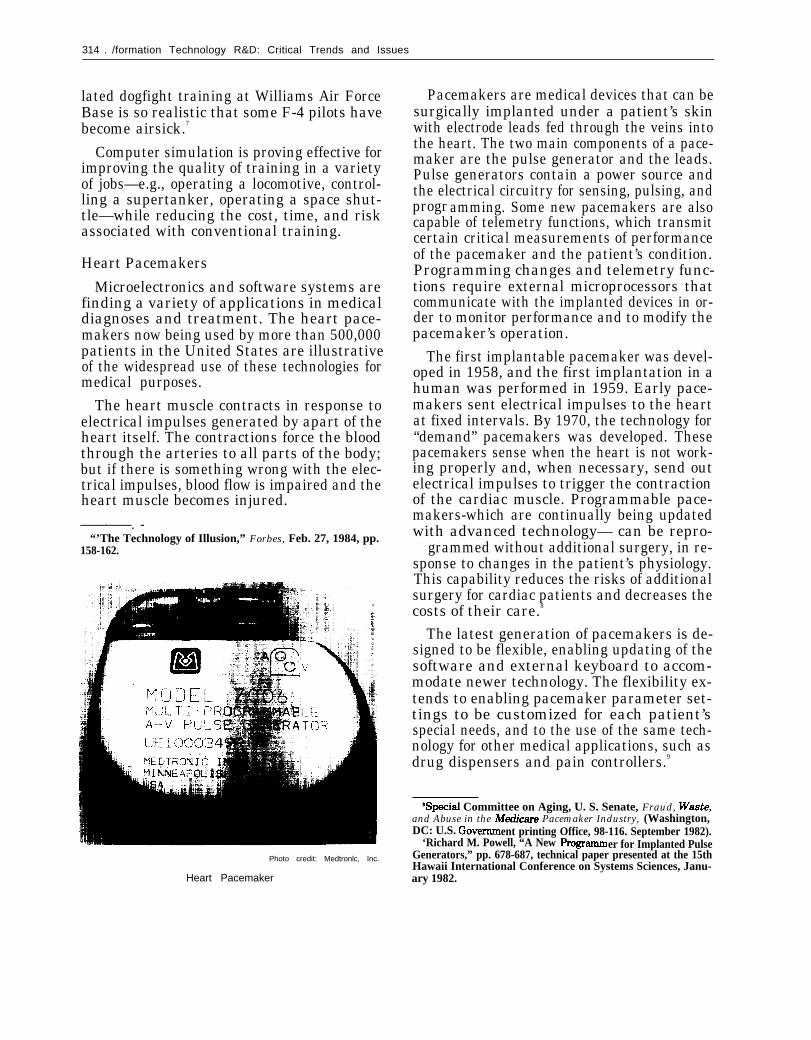

Heart Pacemakers

Microelectronics and software systems arefinding a variety of applications in medicaldiagnoses and treatment. The heart pace-makers now being used by more than 500,000patients in the United States are illustrativeof the widespread use of these technologies formedical purposes.

The heart muscle contracts in response toelectrical impulses generated by apart of theheart itself. The contractions force the bloodthrough the arteries to all parts of the body;but if there is something wrong with the elec-trical impulses, blood flow is impaired and theheart muscle becomes injured.

——-——. -“’The Technology of Illusion,” Forbes, Feb. 27, 1984, pp.

158-162.

Photo credit: Medtronlc, Inc.

Heart Pacemaker

Pacemakers are medical devices that can besurgically implanted under a patient’s skinwith electrode leads fed through the veins intothe heart. The two main components of a pace-maker are the pulse generator and the leads.Pulse generators contain a power source andthe electrical circuitry for sensing, pulsing, andprogr amming. Some new pacemakers are alsocapable of telemetry functions, which transmitcertain critical measurements of performanceof the pacemaker and the patient’s condition.Programming changes and telemetry func-tions require external microprocessors thatcommunicate with the implanted devices in or-der to monitor performance and to modify thepacemaker’s operation.

The first implantable pacemaker was devel-oped in 1958, and the first implantation in ahuman was performed in 1959. Early pace-makers sent electrical impulses to the heartat fixed intervals. By 1970, the technology for“demand” pacemakers was developed. Thesepacemakers sense when the heart is not work-ing properly and, when necessary, send outelectrical impulses to trigger the contractionof the cardiac muscle. Programmable pace-makers-which are continually being updatedwith advanced technology— can be repro- grammed without additional surgery, in re-sponse to changes in the patient’s physiology.This capability reduces the risks of additionalsurgery for cardiac patients and decreases thecosts of their care.8

The latest generation of pacemakers is de-signed to be flexible, enabling updating of thesoftware and external keyboard to accom-modate newer technology. The flexibility ex-tends to enabling pacemaker parameter set-tings to be customized for each patient’sspecial needs, and to the use of the same tech-nology for other medical applications, such asdrug dispensers and pain controllers.9

%pecisl Committee on Aging, U. S. Senate, Fraud, Waste,and Abuse in the Medz”care Pacemaker Industry, (Washington,DC: U.S. Govemxnent printing Office, 98-116. September 1982).

‘Richard M. Powell, “A New Programm er for Implanted PulseGenerators,” pp. 678-687, technical paper presented at the 15thHawaii International Conference on Systems Sciences, Janu-ary 1982.

—

Ch. 9—Technology and Industry . 315

Financial ServicesThe financial service industry would not pro-

vide the level of service it does without infor-mation technologies. 10 The numbers of checks(over 37 billion annually), credit card drafts(over 3.5 billion annually), and securities trades(over 30 billion shares traded annually) aresimply too much for any manual system tohandle. In the 1960s, for example, before thefinancial service industry was substantiallyautomated, there were days when the NewYork Stock Exchange suspended operationsbecause the broker/dealers were unable to han-dle the workload.

Both users and providers of financial serv-ices have made use of virtually every categoryof informat ion technology . Banks and otherfinancial service providers have been longtimeu s e r s o f c o m p u t e r s . H o w e v e r , a n i n c r e a s i n gn u m b e r o f r e t a i l e r s - l a r g e a n d s m a l l - a r e i n -s ta l l ing the hardware and us ing the te lecom-munications networks to verify checks and toauthorize and complete credit transact ions .

Applications software packages for financialservices can process market data and gener-a t e i n f o r m a t i o n u s e d f o r p o r t f o l i o m a n a g e -ment. They can also generate and analyze loaninformat ion, and process bank card appl ica-t ions . The spread of remote terminals inter-connected with central computers i s becom-ing ubiquitous, and expanding the number ofservices avai lable to the publ ic .

T h e v i d e o - r e l a t e d t e c h n o l o g i e s - v i d e o t e x ( atwo-way information service) and te letext (ao n e - w a y i n f o r m a t i o n s e r v i c e ) — a r e n o t y e twidely used in the delivery of financial serv-ices, but experiments are under way and it isl ike ly that they ul t imate ly wi l l gain accept-a n c e . O n e v i d e o t e x s y s t e m , c u r r e n t l y b e i n gmarketed in Flor ida, uses an AT&T terminalattached to a television set to link the finan-cial service provider with the customer.

— . —‘°For detailed discussion, see Effects of Information Tech-

nology on Financial Service Systems, (Washington, DC: U.S.Congress, Office of Technology Assessment, OTA-CIT-202, Sep-tember 1984).

There are also several card technologies. Theembossed plastic card with its strip of mag-netic tape provides the primary means foraccessing credit and debit services that are de-livered through both paper-based and elec-tronic systems. Laser cards-not yet used bythe financial service industry–can store dig-ital data signifying the bearer’s fingerprints.Electron cards combine three encoding tech-nologies-the banking industry’s magnetictape, the retai l industry’s opt ical characterrecogni t ion , and the UPC bar code .

Document and currency readers have hadsome acceptance, part icularly for the readingof checks encoded with magnetic ink. Systemsthat process credit and debit card transactionsalready truncate the paper f low at the earl i -est pract ical t ime. The data are recorded onmagnetic media and transferred electronicallyfor processing by the card issuer.

Together, these technologies have resultedin a financial service industry that is offeringan increasing number of services such as auto-mated redemption of money market funds. Atthe same t ime these services are being pro-v ided in an increas ing number of ways , in-c luding the use of automated te l ler machinesand telephone bill payers.

With all this, there is the possibility ofredistribution of functions among traditionalsuppliers as well as potential new entrants.Whereas in the past the payment system hasbeen reserved largely to banks, because theyhad access to facilities for clearing and settle-ment, movement of funds electronically makesit possible to avoid the traditional paymentsystem and to settle directly between tradingpartners. Alternative means of distributing in-formation could diminish the role of brokersfor such products as securities, real estate, andinsurance. Cash-oriented businesses, such asgas stations and supermarkets, already use on-site automated teller machines to relieve therequirement to cash checks while minimizingthe amount of currency that is held at eachstore location.

316 ● Information Technology R&D: Critical Trends and Issues

Characteristics of the U.S. InformationTechnology Industry

The information technology industry is acomposite of several industries both in man-ufacturing and services. There is no single,generally accepted definition of the industry.The definitions in use by the Information In-dustry Association, for example, are too broadfor the purposes of this report, while defini-tions used by the Computer and BusinessEquipment Manufacturer’s Association andby the Association of Data Processing Serv-ice Organizations are too restricted.

Despite the ambiguities, this section at-tempts to characterize the industry in termsof size and structure, growth, employment, in-vestment in R&D, and other areas of specialconcern. The part of the information technol-ogy industry portrayed here includes primar-ily manufacturers of: electronics; informationprocessing equipment, including computers,office equipment, and peripherals and services;semiconductors; and telecommunicationsequipment.

Table 52 is a summary of the key indicatorsfor the composite 30 industry categories cov-ered by Business Weekll for the period 1978to 1982, compared with aggregated data forpart of the information technology industry.”A point of contrast worth noting is that infor-mation technology firms’ business perform-ance during the period outpaced the compos-ite industry average significantly as measuredby the following criteria:

●

●

growth in sales revenues: 40 percent forthe composite industry groups vs. 66 per-cent for the information technology sector.growth in profits: 6.4 percent for the com-posite vs. 36.4 percent for the informationtechnology sector.

llBu~jne~~ W=k, R&D Scoreboard, June 20, 1983, PP. 122-

153. See also Business Week, July 9, 1984, pp. 64-77, whichshows a continuation of the trends through 1983.

‘zData shown by Business Week for national composite in-dustry R&D expenditures correlates closely with NSF data inScience Resources Stud-es “Highlights,” June 11, 1982.

●

●

●

●

profits/sales ratios ranging between 4.2to 5.7 percent for the composite vs. 7.9to 9.7 percent for the information technol-ogy sector.growth in the number of employees: a de-crease of 7.8 percent for the composite vs.an increase of 11.8 percent for the infor-mation technology industry.growth in R&D expenditures: 81 percentfor the composite vs. 111 percent for theinformation technology sector. The infor-mation technology sector’s R&D expend-itures per employee were higher than thecomposite by about 20 percent annuallyfor the period, and both groups increasedtheir R&D investments in spite of a reces-sion.13

investments in R&D as a percentage ofsales: averaging 2.1 for the composite vs.4.2 for the information technology sector;and, as a percentage of profits, 42 vs. 48,respectively.

The above statistics are incomplete becausefirms whose primary business is not informa-tion technology do not appear as part of theindustry—despite the fact that their informa-tion technology activities may be significant.Among the firms not represented are GeneralElectric, Rockwell International, and West-inghouse.

The above data for the information technol-ogy manufacturing industry, when combinedwith related sectors such as the software andcomputer services, and telephone and tele-graph services sectors of the economy, hadtotal revenues of $229 billion for 1982, up from$180 billion in 1980, for a 27 percent increase.Figure 53 illustrates the increasing portion of

‘Klf the four sectors-industry, Federal Governrnent, collegesand universities, and other nonprofit organizations-only in-dustry increased its funding for R&D in constant 1972 dollarsduring the 1978-82 period. Probable Levels of R&D Expench”-tures in 1984: Forecast and Analysis, Battelle, December 1983.

Ch. 9—Technology and Industry . 317

Table 52.—Comparison of the U.S. Information Technology Industry withComposite Industry Performance, 1978-82

Percent1978 1979 1980 1981 1982 change— —.

C o m p o s i t e

Infotech

C o m p o s i t e

Infotech

C o m p o s i t e

Infotech

C o m p o s i t e

Infotech

C o m p o s i t e

I n f o t e c h

C o m p o s i t e

Infotech

C o m p o s i t e

Infotech

C o m p o s i t e

Infotech

Sales (mill Ions of dollars) . . . . . 1,085,291

131,872

1,277,764149,783

1,421,551

174,449

1,586,510

193,921

1,520,313218,862

4066

P r o f i t s ( m i l l i o n s o f d o l l a r s ) . . 59,57812,780

72,50513,821

73,49315,474

81,75716,056

63,36517,436

6.436.4

Profits/sales (percent) . . . . . . . . . . 5.59.7

5.79.2

5.28.9

5.18.3

4.27.9

Employees (thousands) . . . . . . . . . . 15,1332,952

15,5423,099

15,4983,226

15,0453,252

13,9593,301

– 7.811.8

R & D ( m i l l i o n s o f d o l l a r s ) . . . . 20,6104,961

24,6745,885

28,9847,221

33,2858,531

37,17910,473

81111

R&D $/sales (percent) . . . . . . . . . . . 1.93.8

1.93.9

2.04.1

2.14.4

2.54.8

R&D $/profits (percent) . . . . . . . . . . 34.638.8

34.042.6

39.446.7

40.753.1

59.080.1

R&D $/employee ... . . . . . . .

R&D expendi tures per employee

lnfotech/Composite (percent) . . .

1,3621,680

1,5881,899

1,8702,238

2,2122,623

2,6673,173

120123 120 121 119Business Week “Scoreboard” Numbers Notes:

A This IS a sample of R&D spending in information technology by U.S. corporations, It is based on total R&D expenditures for those companies that are publiclyheld, have annual revenues over $35 million, and R&D expenses of $1 million or 1 percent of revenue. Only that spending by companies whose primary businessis Information technology (electronics, computers, office equipment, computer services and peripherals, semiconductors, and telecommunications) is included.

B Sales, R&D spending, and R&D spending per employee figures have been adjusted to reflect the numbers from Western Electric and other AT&T subsidiariesthat are not included in the “Scoreboard” numbers, This adjustment involves:1 addition of revenues received from Western Electric to the total operating revenues figures in the AT&T Annual Reports for the years covered,2 use of the total AT&T spending figures for R&D which include spending by Western Electric and other AT&T subsidiaries as provided in Business Week for

the years 1980-82 and as estimated from a chart in the 1983 AT&T Annual Report for the years 1978 and 1979.3 use of total AT&T employment figures provided in Forbes each May for the years 1978-82.

C Employment numbers for all sectors have been calculated from the R&D spending per employee and the R&D spending figures provided in Business Week andmay reflect rounding errors,

SOURCE. Data obtained, or calculated from Business Week, Scoreboard, June 30, 1983 the U.S. Commerce Department; Forbes, May 1979 throuah 1983; 10K formsfiled by AT&T and Western Electric Corp

s e r v i c e s c l o s e l y m a t c h e s t h a t o f c o m p u t e rm a n u f a c t u r i n g , b o t h g r o w i n g b y a b o u t 1 4 0percent between 1972 and 1982 .

International Trade

Technology-intensive products have impor-tant implications for the balance of trade.Studies on U.S. trade and the influence of tech-nology have generally concluded that technol-o g y s e r v e s a s a n i m p o r t a n t d e t e r m i n a n t o fcomparative advantage in manufactured goodst r a d e . 14 15

“C. Mi~el Aho and Howard F. Rosen, “Trends in Technol-ogy-Intensive Trade: With Special Reference to U.S. Competi-tiveness, ” Office of Foreign Economic Research, Bureau of In-ternational Labor Affairs, U.S. Department of Labor, p. 11.

“T. C, Lowinger, “Human Capital and Technological Deter-minants of U.S. Industries Revealed Comparative Advantage, ”Quarterly Review of Econozzu”cs and Business (1974), winter1977, pp. 91-102, as reported in Aho and Rosen, pp. 11, 12.

total sales due to services, which are approach-ing 50 percent of total industry revenues.

Employment

Employment in information technologymanufacturing increased significantly between1972 and 1982 in most segments of the indus-try (table 53), experiencing employment growthranging between 9 and 142 percent. Only theconsumer products (radio and TV sets) showeda decline (28 percent). Total employment in in-formation technology manufacturing grew by51 percent , in spi te of economic recess ions .

Employment in information technologyservices i s about equal to that of the manu-facturing segment , with some 1 .6 mi l l ion em-ployees . The employment level in computing

318 ● Information Technology R&D: Critical Trends and Issues

Figure 53.—The Changing Structure and Growth of the U.S. Information

300

200

-

100

0

Technology IndustryInformation industry revenues; 1980-83 (dollars in billions)

Software 180na n d c o m p u t e r . servicesl’2

Telephoneand telegraph 34.3%

service2

Informationtechnology

manufacturing

229

258

34.7%

1980 1981 1982 1983

YearsSOURCES: IADAfJSO; 2U.S. Industrial Outlook, 1983, 1984.

Table 53.—Employment Levels in the U.S. Information Technology IndustriesEmployees (in thousands)

Percent change1972 1982 1972-1982

Manufacturing a

Computers . . . . . . . . . . . . . . . . . . . . . . . . . . . . 145 351 + 142Office equipment. . . . . . . . . . . . . . . . . . . . . . . 34 51 +50Radio and television receiving sets . . . . . . . 87 63 –28Telephone and telegraph equipment . . . . . . 134 146 + 9Radio and television communications

equipment . . . . . . . . . . . . . . . . . . . . . . . . . . . 319 454 +42Electronic components. . . . . . . . . . . . . . . . . . 336 528 +57

Totals, manufacturing . . . . . . . . . . . . . . . . . 1,055 1,593

ServicesTelephone and telegraph . . . . . . . . . . . . . . . . 949 1,131 +11Computing b. . . . . . . . . . . . . . . . . . . . . . . . . . . . 149 360 + 141Radio and television broadcast . . . . . . . . . . 68 81 +19Cable television . . . . . . . . . . . . . . . . . . . . . . . 40 52 +30

Totals, services . . . . . . . . . . . . . . . . . . . . . . . . . . 1,206 1,624aEstimates provided by the U..S. Department of Commerce, Bureau of Industrial Economics.bF\gures are for 1974 and 1983. Source: U.S. Industrial Outlook, 1984.CFigures are for 1979 and 1983, Source: Federal Communication Commission in telephone interview with OTA staff, May 1984,

dF\gures are for 1981 and 1982. Ibid. (FCC).

—

Ch. 9—Technology and Industry ● 319

The U.S. merchandise trade balance hasbeen negative in recent years: deficits of $42.7billion in 1982; $69.4 billion in 1983; and over$100 billion in 1984. In 1980, advanced tech-nology products showed a positive trade bal-ance of $31 billion, compared with a deficit ofm o r e t h a n $ 5 0 b i l l i o n f o r a l l m a n u f a c t u r e dgoods.”

Information technology manufactured prod-ucts17 usually made positive contributions tothe U.S. balance of trade between 1972 and1982 (fig. 54), led by sales of computer equip-m e n t . H o w e v e r , 1 9 8 3 a n d 1 9 8 4 s a w t r a d edeficits of $0.8 and 2.3 billion according to De-p a r t m e n t o f C o m m e r c e e s t i m a t e s .18 T h e d e f i -cits would have been much greater withoutabout $6 billion in exports of computer equip-ment in each of those years (see f ig . 55) .— . — —

“International Competitiveness in Advanced Technology:Decisions for Aznen”ca, National Research Council (Washing-ton, DC: National Academy Press, 1983, pp. 23-24.

“The products include: computer equipment, SIC 3573; of-fice equipment, SIC 3579; radio and TV sets, SIC 3651;telephone and telegraph equipment, SIC 3661; radio and TVcommunications equipment, SIC 3662; and electronic comp~nents, SIC 367.

‘aU.S. Industn”d Outlook, 1978 through 1984.

Figure 54. —Balance of Trade, InformationTechnology Manufacturing Industry

(dollars in billions)

6 -

equipment (SIC 3573)4

2

o

,-6 Radio and TV Communications

equipment,

1972 1974 1976 1978 1980 1982 1984Years

SOURCE: U.S. Industrial Outlook for years 1978 through 1984.

est

Figure 55.— U.S. Trade Balancea With SelectedNations for R&D Intensive Manufactured Products

$30

28

26

24

22

20

18

16

14

12

4

2

0

-2

-4

-6

●✍

Developing nations

1966 67 68 69 70 71 72 73 74 75 76 77 78 79 80Years

aExports less imports.blncludes West Germany,

SOURCE: Science Indicators— 1982, National Science Board, Na-tional Science Foundation, 1983.

Although the United States holds the ma-jor market share of the industrialized coun-t r i e s ’ e x p o r t s o f h i g h - t e c h n o l o g y p r o d u c t s ,t h a t s h a r e h a s d e c l i n e d f r o m 3 0 p e r c e n t i n1962 to 22 percent in 1978, and has increasedonly marginal ly s ince . In absolute terms, theU.S. positive trade balance in high-technologyproducts increased over e ightfold from 1962to 1980. During that same period West Ger-m a n y , a n d e s p e c i a l l y J a p a n , s t a r t i n g f r o msmaller bases , have had impress ive gains int h e i r s u r p l u s e s o f e x p o r t s o v e r i m p o r t s — aninefold increase for West Germany and two-hundredfold increase for Japan.1 9

19U+S. Dep~ment of Commerce, International made Admin-istration, as reported in “An Assessment of U.S. Competitiveness in High-Technology Industries, ” prepared for the Work-ing Group on High Technology Industries of the CabinetCouncil on Commerce and Trade, final draft, May 19,1982.

—— —

320 . Information Technology R&D: Critical Trends and Issues

Industry Structure

Information technology companies in theUnited States are heterogeneous in dollarvalue of sales, breadth of product lines, num-ber of employees, and degree of vertical in-tegration. Competing for those markets arethousands of firms ranging in size from thevertically integrated multinational companiessuch as IBM, ITT, and the still-large, post-divestiture AT&T to the more typical, smallercompanies that produce a narrow cluster ofproducts with a large technology content.While the majority of sales dollars are concen-trated in the large companies, the vast ma-jority of companies are relatively small.

The diversity in the sizes of the businessesthat populate the information technology fieldis important for reasons that include the bene-fits of competition; the impetus to innovationdue to firms’ willingness to take risks and totry new directions; and the tendency to fillniche market demand for specialized products.The U.S. telecommunications, electronics, andsoftware industries provide three illustrationsof the contrasts in the breadth of that di-versity.

The telecommunications services industryis simultaneously both a mature industrydating back to the 19th century and a grow-ing industry marked by limited competitionin some markets and diversity in others. Whilelocal public telecommunications services arelargely dominated by regulated monopolies,long-distance services are now offered in acompetitive market. New services, such aspaging, cellular mobile radio services, bypassservices and direct broadcast satellite services,are not dominated by the established carriers,but are being offered by a variety of firms.

Table 54.—U.S. Home

The telecommunications equipment provid-ers are exceptionally diverse and competitive.There are hundreds of firms in this field, rang-ing from a few U.S. and foreign multinationalcompanies manufacturing a full range ofequipment to dozens of medium size, andmany hundreds of small companies concen-trating on a more limited range of products—e.g., speech compression products, multiplex-ers, modems, data terminals and local areanetworks.

The electronics industry is even more di-verse. The thousands of electronic systemsand equipment providers, as well as consultingfirms, range in size from those with billionsof dollars in annual sales to small, start-upventures such as the Apple Computer’s garageoperation of a few years ago. For those seg-ments of the industry undergoing rapid tech-nological change, diversity is often acceleratedby spin-offs from rapidly growing companies,and other new entries into the field.

The U.S. microcomputer software industryis an example of rapid change, growth, anddiversity. Future Computing, Inc. estimatesthat the U.S. market for home computer soft-ware grew by 168 percent from 1982 to 1983,and projects an 85 percent growth from 1983to 1984, with the growth rate declining to 26percent by 1988 in a projected $5 billion an-nual market by then (table 54). Software unitsales for office use are projected to enjoy com-parable growth. Table 55 indicates growthrates of 87 percent between 1982 and 1983,and 58 percent from 1983 to 1984, graduallytapering off to 24 percent in 1988 in a $6.7 bil-lion annual market.20 Like the electronics in-dustry, software firms number in the thou-

2 0 F u t u r e c o m p u t i n g , ~ r g on ~ c o m m u n i c a t i o n , Mmch 1984.

Computer Software Salesa

1981 1982 1983 1984 1985 1986 1987 1988Software units (millions) . . . . . . . . . . 1.1 6.9 19.0 37.0 58.0 82.0 112.0 144.0Percent growth (units) . . . . . . . . . . . . 486 168 85 52 42 32 26Revenue (millions of dollars). . . . . . . 48 282 757 1,400 2,100 3,000 4,000 5,000aData for 19u.M are estimates by Future cOrnPUllW.SOURCE: Future Computing, Richardson, TX, by OTA staff telephone interview, March 1964,

Ch. 9—Technology and Industry . 3 2 1

Table 55.—U.S. Office Computer Software Salesa

1981 1982 1983 1984 1985 1986 1987 1988

Software units (millions) . . . . . . . . . . 3.2 6.1 11.0 17.0 25.0 35.0 46.0 59.0Percent growth (units) . . . . . . . . . . . . 111 87 58 44 36 30 24Revenue (millions of dollars) . . . . . . . 343 724 1,351 2,100 3,100 4,200 5,400 6,700aData for lgsd.aa are estifnates by Future Computln9

SOURCE Future Computing, Richardson, TX, by OTA staff telephone interview, March 1984

sands. Although no hard data are available,it is the impression of industry analysts thatthe rapid pace of startups in the software in-dustry seen in recent years now appears to beslackening.

An important trend in industry structure istoward concentration in the software and dataservices industries, where larger firms have ac-quired hundreds of smaller ones. Among theselarger firms are Automatic Data Processing,Electronic Data Systems, and General Electric.

Larger firms are also integrating their prod-uct lines-some moving into subsystems andcomponents, and others, such as semiconduc-tor manufacturers, moving into subsystemand computer manufacturing. AT&T, TexasInstruments, Intel, and Northern Telecom-munications Corp. are examples of companiesrecently expanding into computers and relatedproducts.

There is also an active trend toward affilia-tions between information producers and dis-tributors. Among these are publishers of news-papers, books, and magazines and broadcast,cable TV, and interactive computer networkcompanies.

Geographic diversification is taking place ata rapid pace as foreign-primarily European—companies acquire U.S. firms. Among theEuropean firms are: Olivetti, CAP Gemini,Racal Electronics, Schlumberger, Thomson-CSF, and Agfa-Gevaert.

A number of U.S. firms are expanding theirmarkets by establishing joint ventures or byacquiring foreign outlets—e.g., IBM, AT&T,and Datapoint.

Small Entrepreneurial Firms

Small businesses play a central role in U.S.industry in general, accounting for:

● thirty-eight percent of the Nation’s grossnational product;

● two-thirds of all new jobs;● two-and-a-half times as many innovations

per employee as large firms;21andŽ a tendency to produce more ‘‘leapfrog’

creations compared to large companiesand to introduce new products morequickly than large firms.22

The contributions of small businesses to theinformation technology industry are signifi-cant. Small businesses with less than 500 em-ployees account for 33 percent of sales in elec-tronic components and 34 percent of theNation’s employment in this sector. In thecomputer services sector, small businesses ac-count for 69 percent of the industry’s sales and67 percent of its employees. These firms alsomake contributions in sectors where largecompanies dominate, such as in office com-puting equipment, consumer electronics, andcommunications equipment (table 56).

Opportunities for innovation based on ad-vances in information technology have beennumerous. Consequently, hundreds of marketniche applications have been created that

“Advocacy: A Voice for Small Businesses, Office of Ad-vocacy, U.S. Small Business Administration, 1984. p. 1.

22Stroemann, 1977. Karl A. Stroetmann “Innovation in Smalland Medium Sized Firms.” Working paper presented at InstitutFur Systemchnik und Innovations forschung, Karlsruhe, WestGermany, August, 1977. See Vesper (Entrepreneurship).

322 • Information Technology R&D: Critical Trends and Issues

Table 56.—Percentage of Total Industry Sales andEmployment by Size of Small Businesses

Companies with Companies withunder 100 employees under 500 employees

Sales Employment Sales Employment

Office computing machinesand computer auxiliaryequipment . . . . . . . . . . . . . . . 2.6 2.6 6.0 6.3

Consumer electronics . . . . . . . 5.4 5.9 9.3 10.1Communications equipment. . 4.7 5.2 9.9 10.8Electronic components . . . . . . 18.3 17.2 32.7 33.7Computer services . . . . . . . . . . 51.2 47.7 68.6 67.1SOURCE: Small Business Administration, 19S4.

small firms are quick to fill-niches too nar-row or specialized to attract large firms.23 Thedevelopment of the computer in the 1940s andthe subsequent invention of the transistor ledto an explosion of new applications and to op-portunities for then small companies whosenames are now familiar in the informationtechnology industry: IBM, Fairchild, Intel,Texas Instruments, DEC, Data General,Wang, and Computervision. One market re-search company’s listing of the fastest-grow-ing niche markets shows that about 90 percentof the top 50 entries are in information tech-nology,24 and many of these technologies arerelatively new.

As the successful firms in this industrygrow, they tend to generate spin-off companiesthat often specialize initially in a narrow rangeof innovative products or processes. Fairchildis such a company, having begun with onlyeight employees and now accounting for over80 spin-off enterprises.25

Venture capital funding is extremely impor-tant to the small entrepreneurial firms. In-.— — ———

231n a July 1981 study, the General Accounting Office foundthat in concentrated industries, such as the information tech-nology industry, small businesses are likely to perform special-ized innovative functions and develop products or processes tobe used or marketed by other, usually larger firms in that in-dustry, For example, in the semiconductor industry there aremany small companies that manufacture diffusion furnaces, ionimplantation machines, epitaxia.1 growth systems, and mask-making systems—all part of a necessary supporb structure forthe semiconductor industry.

‘421st Century Research, Supergrowth Technology U. S. A.,newsletter as published in EDP News Service, Inc., ComputerAge-EDP Weekly, Feb. 28, 1983, p. 9.

“Carl H. Vesper, Entrepreneursiu”p and National Policy,Heller Institute for Small Business Policy Papers, p. 27.

vestments through organized venture capitalinvestment businesses in 1983 amounted to$2.8 billion, up 55 percent from $1.8 billion in1982.26 It is improbable that this growth ratewill be sustained for very long.27

The supply of U.S. venture capital financ-ing has grown at least eightfold since the mid-1970s, helping to fund the more than 5,500U.S. small startup and expanding firms. Thesefirms tend to operate in innovative marketniches where the risks are high and the poten-tial payoffs much higher.

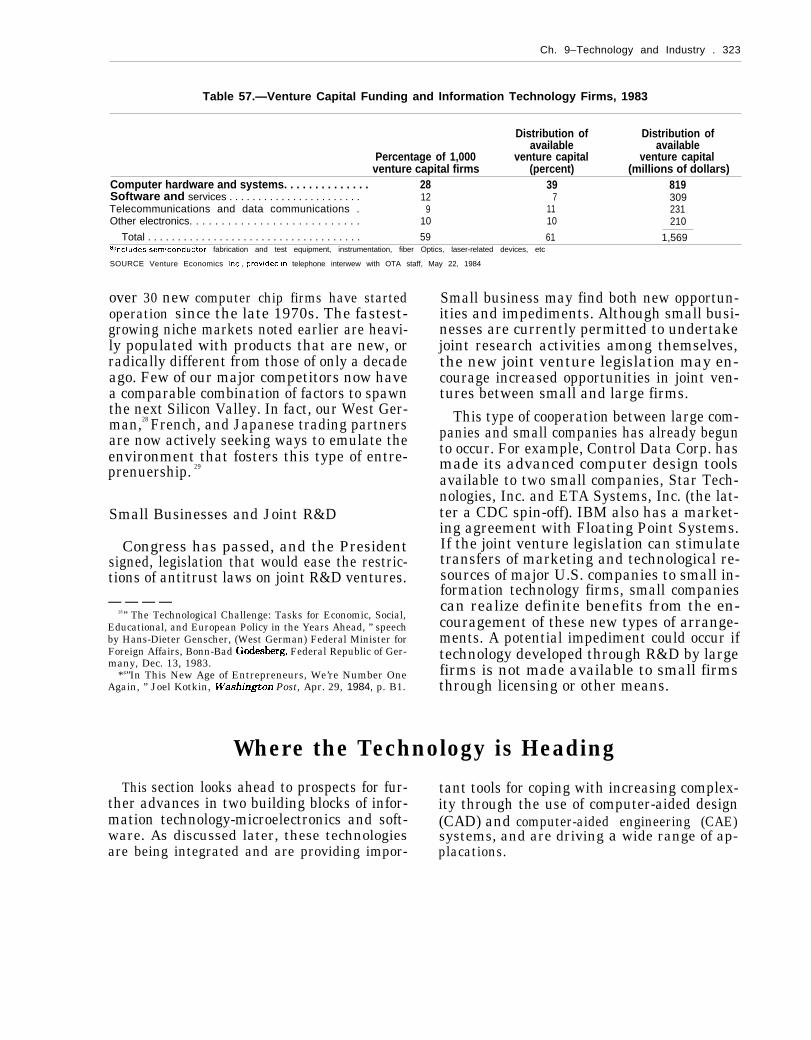

Information technology firms supported byventure capital funds numbered in excess of1,000 in 1983, and received about $2.1 billionfrom organized venture capital investmentbusinesses. These funds were used for bothstartups and expansion of existing companies.The distribution of funds is shown in table 57.

These firms account for a significant num-ber of advances in the information technologyfield. Among the now-well known informationtechnology firms started or aided by venturecapital are: Intel, Apple Computer, Visicalc,DEC, and Data General. R&D limited partner-ships also contribute to this process (see ch. 2).

The existence of so many entrepreneurialfirms, the current abundance of venture capi-tal to fund their growth, and the strengthen-ing university-industry R&D relationshipsserve as a powerful source of strength for in-novation in the United States. For example,

“Data provided by Venture Economics, Inc., from its data-base covering organized venture capital investment companies.

“’’Scramble for Capital at Almost-Public Companies, ” For-tune June 25, 1984, p. 91.

Ch. 9–Technology and Industry . 323

Table 57.—Venture Capital Funding and Information Technology Firms, 1983

Distribution of Distribution ofavailable available

Percentage of 1,000 venture capital venture capitalventure capital firms (percent) (millions of dollars)

Computer hardware and systems. . . . . . . . . . . . . . 28 39 819Software and services . . . . . . . . . . . . . . . . . . . . . . . 12 7 309Telecommunications and data communications . 9 11 231Other electronics. . . . . . . . . . . . . . . . . . . . . . . . . . . 10 10 210

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59 61 1,569alncl”des semiconductor fabrication and test equipment, instrumentation, fiber Optics, laser-related devices, etc

SOURCE Venture Economics Inc , prowded In telephone interwew with OTA staff, May 22, 1984

over 30 new computer chip firms have startedoperation since the late 1970s. The fastest-growing niche markets noted earlier are heavi-ly populated with products that are new, orradically different from those of only a decadeago. Few of our major competitors now havea comparable combination of factors to spawnthe next Silicon Valley. In fact, our West Ger-man,28 French, and Japanese trading partnersare now actively seeking ways to emulate theenvironment that fosters this type of entre-prenuership. 29

Small Businesses and Joint R&D

Congress has passed, and the Presidentsigned, legislation that would ease the restric-tions of antitrust laws on joint R&D ventures.— — — —

28’’ The Technological Challenge: Tasks for Economic, Social,Educational, and European Policy in the Years Ahead, ” speechby Hans-Dieter Genscher, (West German) Federal Minister forForeign Affairs, Bonn-Bad Godesberg, Federal Republic of Ger-many, Dec. 13, 1983.

*g”In This New Age of Entrepreneurs, We’re Number OneAgain, ” Joel Kotkin, Wdu”ngton Post, Apr. 29, 1984, p. B1.

Small business may find both new opportun-ities and impediments. Although small busi-nesses are currently permitted to undertakejoint research activities among themselves,the new joint venture legislation may en-courage increased opportunities in joint ven-tures between small and large firms.

This type of cooperation between large com-panies and small companies has already begunto occur. For example, Control Data Corp. hasmade its advanced computer design toolsavailable to two small companies, Star Tech-nologies, Inc. and ETA Systems, Inc. (the lat-ter a CDC spin-off). IBM also has a market-ing agreement with Floating Point Systems.If the joint venture legislation can stimulatetransfers of marketing and technological re-sources of major U.S. companies to small in-formation technology firms, small companiescan realize definite benefits from the en-couragement of these new types of arrange-ments. A potential impediment could occur iftechnology developed through R&D by largefirms is not made available to small firmsthrough licensing or other means.

Where the Technology is HeadingThis section looks ahead to prospects for fur- tant tools for coping with increasing complex-

ther advances in two building blocks of infor- ity through the use of computer-aided designmation technology-microelectronics and soft- (CAD) and computer-aided engineering (CAE)ware. As discussed later, these technologies systems, and are driving a wide range of ap-are being integrated and are providing impor- placations.

324 ● Information Technology R&D: Critical Trends and Issues

Advances in microelectronics and softwareare dependent on entirely different under-pinnings-e.g., physics, chemistry, materialsscience and electrical engineering for theformer, and computer and information science,psychology, and software engineering, amongothers, for the latter. Prospects for continua-tion of the explosive growth of informationtechnology during the past two decades willbe paced by advances in microelectronics andsoftware.

Microelectronics30

The rate of technological improvement insemiconductors has been phenomenal duringthe past quarter century, and has sparked newapplications and economic advances world-wide. This section reviews the growth ofintegrated circuit capabilities and seeks to pro-vide insight into future progress, its depend-encies and foreseeable limitations, and thelikely timeframe of that progress.

Probable trends include:●

●

●

Silicon is likely to remain the most impor-tant semiconductor material for the nextdecade and beyond, while gallium arse-nide is likely to come into wide use in cer-tain applications where its special prop-erties provide specific advantages. Theimpact of other innovative materials islikely to be marginal until after the turnof the century, when biotechnology maybegin to converge with information tech-nology.Prices for the main output of microelec-tronics technology, logic and memory, canbe expected to continue to decline on a perfunction basis, following the general pat-tern of the past two decades.Continued advances during the next twodecades in large-scale integration of sili-con and gallium arsenide will require the

——— .—.—.30A ~i~ficmt mount of data in this section is t~en from,

or based om 1) the Sixth Mountbatten Lecture, M2”c.melectmm”csProgress Prospects, delivered by Ian M. ROSS, President, AT&TBell Laboratories, Nov. 10, 1983, London, England; and 2) J.D. Meindl, Theoretical, Practical, and Analogical b“zm”ts toULLU, Technical Digest of the International Electron DevicesMeeting, December 1983, pp. 8-13.

●

continued advance of other sciences andtechnologies, particularly physics, chem-istry and materials science, and manufac-turing and software engineering.The R&D costs for incremental advancesin microelectronics technology are ex-pected by industry experts to increase asthe complexity of circuits increases andas the theoretical physical limits of micro-electronics are approached.

Silicon Integrated Circuits

Transistor Size and Density

Between 1972 and 1981, the number of tran-sistors that could be packed on a chip doubledeach year (11,000 in 1972 and 600,000 in 1981)(see fig. 56). Today, integrated circuit technol-

Figure 56.—Historical Development of theComplexity of Integrated Circuits

1 05

. ->

1 04

1 03

1970 1975 1980 1985

Introduction year

SOURCE: Arthur D. Little, Inc. estimatea.

Ch. 9—Technology and Industry ● 325

ogy is approaching the capability of packinga million components (mostly transistors) ona single silicon chip.31

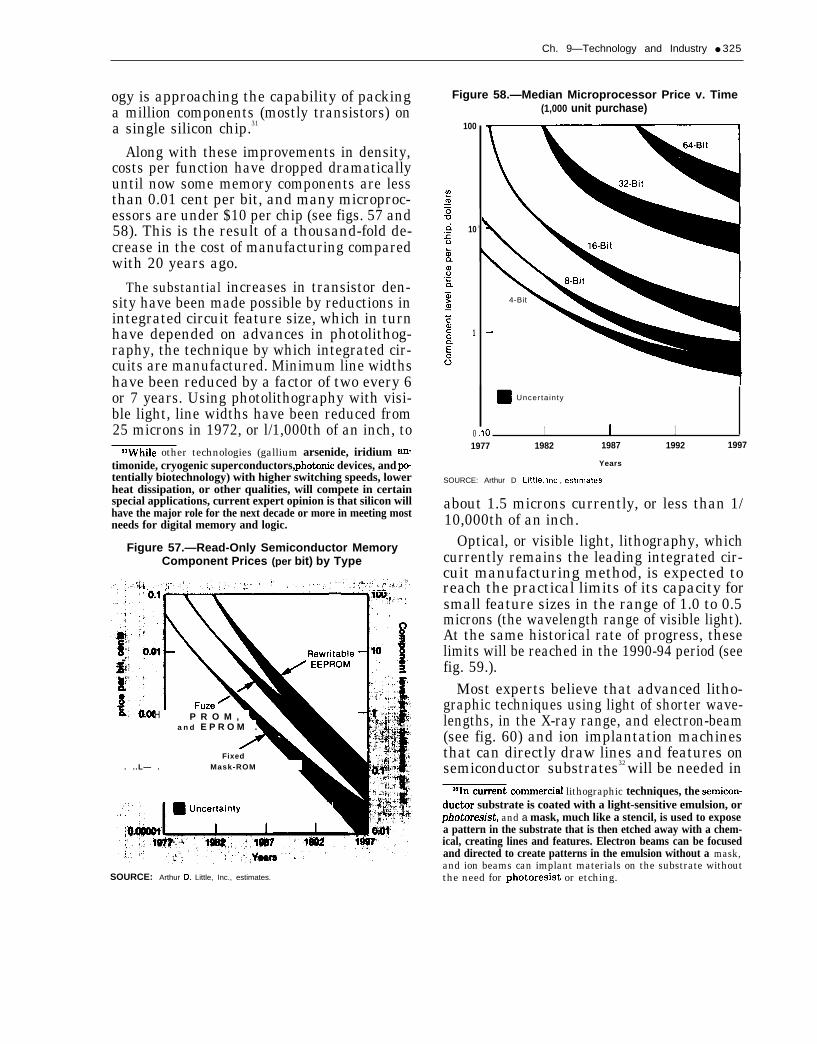

Along with these improvements in density,costs per function have dropped dramaticallyuntil now some memory components are lessthan 0.01 cent per bit, and many microproc-essors are under $10 per chip (see figs. 57 and58). This is the result of a thousand-fold de-crease in the cost of manufacturing comparedwith 20 years ago.

The substantial increases in transistor den-sity have been made possible by reductions inintegrated circuit feature size, which in turnhave depended on advances in photolithog-raphy, the technique by which integrated cir-cuits are manufactured. Minimum line widthshave been reduced by a factor of two every 6or 7 years. Using photolithography with visi-ble light, line widths have been reduced from25 microns in 1972, or l/1,000th of an inch, to

$lwhile other technologies (gallium arsenide, iridium ~-timonide, cryogenic superconductors, photonic devices, and POtentially biotechnology) with higher switching speeds, lowerheat dissipation, or other qualities, will compete in certainspecial applications, current expert opinion is that silicon willhave the major role for the next decade or more in meeting mostneeds for digital memory and logic.

Figure 57.—Read-Only Semiconductor MemoryComponent Prices (per bit) by Type

H P R O M , a n d E P R O M .

Fixed. ..L— . Mask-ROM

SOURCE: Arthur D. Little, Inc., estimates.

Figure 58.—Median Microprocessor Price v. Time(1,000 unit purchase)

100

10 i

1

Uncerta inty

,10 1 1 11977 1982 1987 1992 1997

Years

o

4-Bit

SOURCE: Arthur D Little, lnc , estimates

about 1.5 microns currently, or less than 1/10,000th of an inch.

Optical, or visible light, lithography, whichcurrently remains the leading integrated cir-cuit manufacturing method, is expected toreach the practical limits of its capacity forsmall feature sizes in the range of 1.0 to 0.5microns (the wavelength range of visible light).At the same historical rate of progress, theselimits will be reached in the 1990-94 period (seefig. 59.).

Most experts believe that advanced litho-graphic techniques using light of shorter wave-lengths, in the X-ray range, and electron-beam(see fig. 60) and ion implantation machinesthat can directly draw lines and features onsemiconductor substrates32 will be needed in

gZ1n Cwent co~erci~ lithographic techniques, the semicon-ductor substrate is coated with a light-sensitive emulsion, orphotoresist, and a mask, much like a stencil, is used to exposea pattern in the substrate that is then etched away with a chem-ical, creating lines and features. Electron beams can be focusedand directed to create patterns in the emulsion without a mask,and ion beams can implant materials on the substrate withoutthe need for photoresist or etching.

326 ● Information Technology R&D: Critical Trends and Issues

Photo credit: AT& T Bell Laboratories

Microprocessor WE 32100

order to achieve further advances.33 A num-ber of such machines are in use for experi-mental purposes and for production of circuitsto be used in-house at major companies suchas IBM and AT&T.

Electron beam lithography and ion implan-tation34 may become the ultimate semiconduc-tor manufacturing techniques, with minimumline widths possible in the range of 0.1 to 0.01micron. The latter widths are comparable tofeature spacing on the order of 20 to 200——————

~~~me en~nWr9 have begun to question the premise thatmore densely packed circuits are necessary. See “Solid State, ”IEEE Spectrum, January 1984, p. 61.

WI’he Defense Department’s Very High Speed Integrated Cir-cuits (VHSIC) program supports research on electron-beam andion-beam manufacturing techniques. Discussion of both of thesecan be found in IEEE Spectrum, January 1984, pp. 61-63.

Figure 59.— Minimum Linewidth for SemiconductorMicrolithography

10

1

0.11977 1982 1987 1992 1997

Years

SOURCE: Arthur D. Little, Inc., estimates.

atoms. The major drawback of such systemsis that they are much slower than mask lithog-raphy; they are now used only in producingcustom chips of low production volume. Elec-tron-beam and ion implantation technologyare expected to be in use on commercial in-tegrated circuit production lines by 199435 (seetable 58).

Research is under way in the United Statesand Japan that is striving to achieve moredensely packed circuit components by stack-ing chips into three dimensional structures. Anumber of problems need to be solved to real-ize 3-D circuits, among them is the difficultyof making connections with elements buriedwithin layers of semiconductor material. Ion-beam equipment is seen as critical to produc-ing the complex microscopic structures re-quired for such 3-D chips.36

—. .—.—351EEE Swtnn.n, January 1984, p. 63.‘6’’3-D Clups, ” The Econonu”st, Feb. 12, 1983, p. 84.

Table 58.—ICs Made with Lithographic Techniques(percent)

Technique 1983 1985 1987

optical scanner. . . . . . . . . . . . . 85 58 38Optical stepper . . . . . . . . . . . . . 15 40 52Electron beam . . . . . . . . . . . . . . 0 1 8X-ray . . . . . . . . . . . . . . . . . . . . . . 0 1 2Ion beam . . . . . . . . . . . . . . . . . . 0 0 0SOURCE: IEEE Spectrum, January 1984, p. 80,

Ch. 9–Technology and Industry ● 327

Figure 60.—A Schematic of an Electron Beam Lithography System,and its Uses to Make LSI Logic Circuits

Compu te r

(G)

Beam on-off control I(F) I I I ICI I a~e

. . . . . , I. .

analog circuits

Electrostatic deflection(p)

’ on a w x o r

SOURCE Mosaic, SS//MS//LVLSMJLSJ,S/, VOI 15, No. 1, p 15.

In devices with such subminiature dimen-sions, other limitations become significant,e.g., the dielectric strength, electronic isola-tion, and heat dissipation of the silicon mate-rial-some of which may represent more se-vere limitations than the theoretical limitsimposed by the most advanced manufactur-ing techniques. Transistors with critical di-mensions of 0.1 micron have been demonstratedto operate by Bell Telephone Laboratories.These dimensions would theoretically lead tosome billion components on a square centi-meter of silicon. A more realistic, practicallimit for silicon may be 100 million compo-nents per square centimeter.37

Increasing the physical dimensions of thechip may also contribute to increasing thecomponent count per chip. Chip sizes are—

“ROSS, op. cit., p. 6.

determined by manufacturing control–theability to minimize the number of impuritiesand defects in the semiconductor substratematerial and in finished circuits. Today’stypical chip size is about 1 square centimeter.There are development efforts under waytoward wafer-scale integration38 which couldprovide a factor of 100 increase in integratedcircuit chip size, to 100 square centimeters orlarger. This factor, coupled with componentdensities of 100 million transistors per squarecentimeter made possible with the advancedmanufacturing techniques noted above, couldresult in component counts of 1 billion tran-sistors per integrated circuit.39

. —SsChips me cut from 3 to 6-inch-diameter wafers which are

currently manufactured with some 100 separate integrated cir-cuits per wafer.

“ROSS, op. cit., p. 7.

38-802 0 - 85 - 22

328 ● Information Technology R&D: Critical Trends and Issues

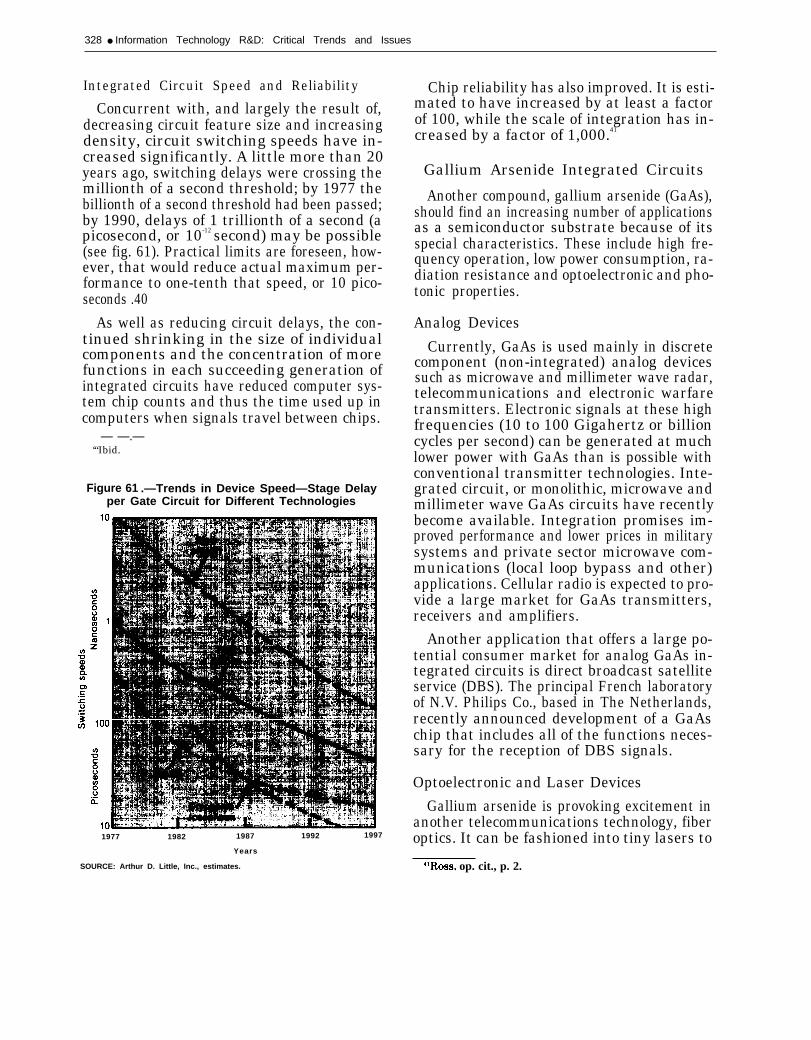

Integrated Circuit Speed and Reliability

Concurrent with, and largely the result of,decreasing circuit feature size and increasingdensity, circuit switching speeds have in-creased significantly. A little more than 20years ago, switching delays were crossing themillionth of a second threshold; by 1977 thebillionth of a second threshold had been passed;by 1990, delays of 1 trillionth of a second (apicosecond, or 10-12 second) may be possible(see fig. 61). Practical limits are foreseen, how-ever, that would reduce actual maximum per-formance to one-tenth that speed, or 10 pico-seconds .40

As well as reducing circuit delays, the con-tinued shrinking in the size of individualcomponents and the concentration of morefunctions in each succeeding generation ofintegrated circuits have reduced computer sys-tem chip counts and thus the time used up incomputers when signals travel between chips.

— —.—‘“Ibid.

Figure 61 .—Trends in Device Speed—Stage Delayper Gate Circuit for Different Technologies

1977 1982 1987 1992 1997

Years

SOURCE: Arthur D. Little, Inc., estimates.

Chip reliability has also improved. It is esti-mated to have increased by at least a factorof 100, while the scale of integration has in-creased by a factor of 1,000.41

Gallium Arsenide Integrated Circuits

Another compound, gallium arsenide (GaAs),should find an increasing number of applicationsas a semiconductor substrate because of itsspecial characteristics. These include high fre-quency operation, low power consumption, ra-diation resistance and optoelectronic and pho-tonic properties.

Analog Devices

Currently, GaAs is used mainly in discretecomponent (non-integrated) analog devicessuch as microwave and millimeter wave radar,telecommunications and electronic warfaretransmitters. Electronic signals at these highfrequencies (10 to 100 Gigahertz or billioncycles per second) can be generated at muchlower power with GaAs than is possible withconventional transmitter technologies. Inte-grated circuit, or monolithic, microwave andmillimeter wave GaAs circuits have recentlybecome available. Integration promises im-proved performance and lower prices in militarysystems and private sector microwave com-munications (local loop bypass and other)applications. Cellular radio is expected to pro-vide a large market for GaAs transmitters,receivers and amplifiers.

Another application that offers a large po-tential consumer market for analog GaAs in-tegrated circuits is direct broadcast satelliteservice (DBS). The principal French laboratoryof N.V. Philips Co., based in The Netherlands,recently announced development of a GaAschip that includes all of the functions neces-sary for the reception of DBS signals.

Optoelectronic and Laser DevicesGallium arsenide is provoking excitement in

another telecommunications technology, fiberoptics. It can be fashioned into tiny lasers to

“ROSS, op. cit., p. 2.

Ch. 9—Technology and Industry ● 329

function as light sources for fiber optic trans-mission, into optoelectronic photodetectors toreceive optical signals and translate them intoelectrical signals, and into signal processingcomponents for fiber optic system amplifiersand repeaters (see Fiber Optics Case Study).Recent work at Bell Labs has developed large-scale integrated (LSI) GaAs signal processingcircuits that are scheduled for production.42

Heretofore, separate devices have been re-quired for fiber optic light generation, recep-tion and signal processing. Communicationamong these separate devices introduces de-lays in fiber optic transmission systems.Lasers have been particularly difficult to inte-grate with the other circuit components onsingle chips because of their complex structureand the large amount of heat that is generatedby their operation.

Fujitsu, the Japanese electronics giant, hasconducted GaAs R&D funded by that govern-ment as part of a $74 million, 7-year projectamong a number of Japanese companies. In1983, it announced development of a processthat integrates a laser light source and thesignal processing transistors necessary for fi-ber optic transmission, all on a single GaAschip that operates at room temperature. Asimilar integrated optoelectronic photoreceiv-er is in the works.

American researchers at Honeywell andRockwell International have also announcedthe development of integrated GaAs opticaltransmitters. 43 The Rockwell device in particu-lar is reported to be adaptable to well-knownLSI circuit manufacturing techniques, promis-ing low production costs.”

— .— .-.— ——‘zl??~ectrom”cs, Oct. 6, 1983, p. 154.“Honeywell announced an integrated optical transmitter in

1982, but it originally required special cooling. The Honeywelldevice has since been improved. See C. Cohen, “Optoelectronicchip integrates laser and pair of FETs, ” Electrom”cs, June 30,1983, pp. 89-90. See also The Econonu”st, Feb. 5, 1983, pp. 82-83.

441, Waler, ‘lG~s Optical IC Integrates Laser, Drive Tra-nsistors, ” Electronics, Oct. 6, 1983, pp. 51-52.

Digital Devices