dover corporation presented by greysi burroughs rena huynh helen tse

TRANSCRIPT

Dover Corporation

Presented by Greysi Burroughs Rena HuynhHelen Tse

Agenda Company Overview – Rena

Financial Statement Analysis – Greysi

Firm Riskiness – Helen

Beta – Helen

Cost of Equity – Rena

Firm Valuation Discount Dividend Model (DDM) – Greysi Free Cash Flow Model (FCFM) – Helen Multiples (P/E ratio) – Rena

Final Valuation and Recommendations – Greysi

Company Overview

Brief History Founded: 1955

HQ: Downers Grove, Illinois

Diversified Global Manufacturer

Volume: > $8 Billion

Exchange: NYSE under “DOV”

Company Overview

4 Major Operating Segments

Industry-leading product innovation

Providing innovative

products & solutions that

serve drilling, production and

downstream markets

1. Global pump & fluid handling

markets

2. Refrigeration systems

Provides integrated printing,

coding, identification equipment

Provide acoustic components

for consumer electric markets

*serves life sciences,

aerospace, & telecom

markets

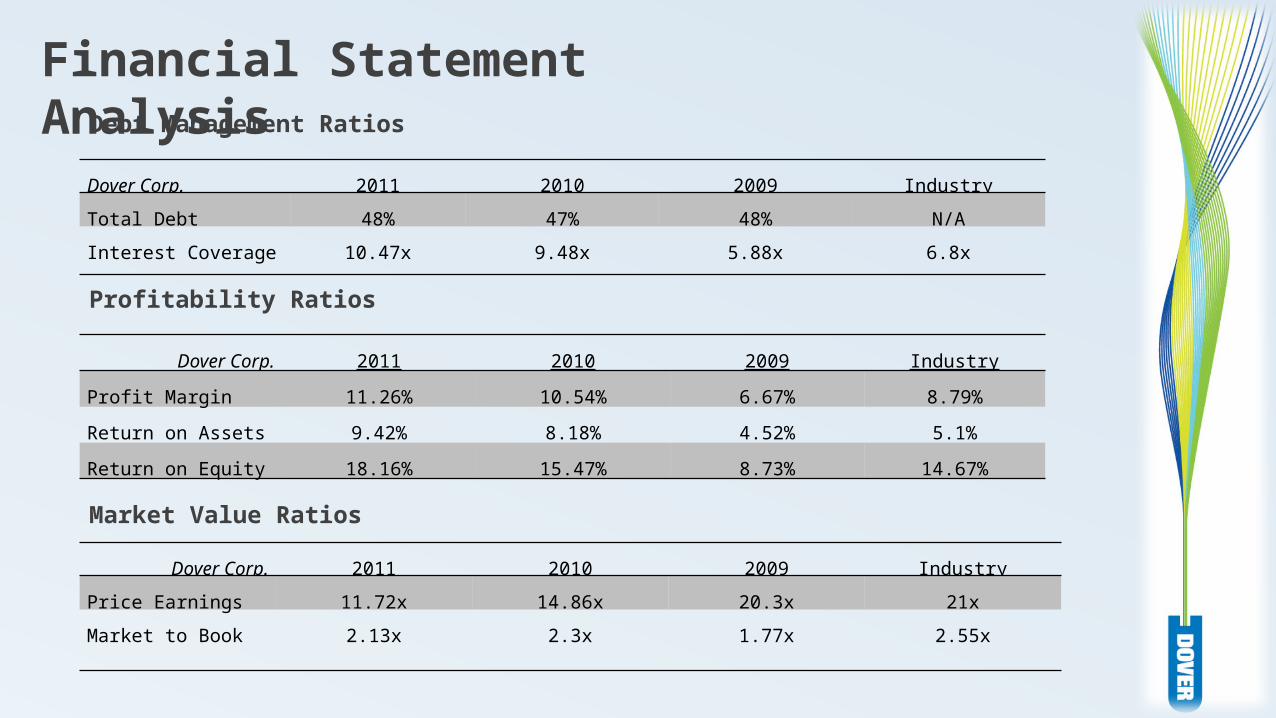

Financial Statement AnalysisLiquidity Ratios

Dover Corp. 2011 2010 2009 Industry

Current Ratio 2.82x 2.73x 2.60x 1.2x

Quick Ratio 2.16x 2.16x 2.01x 0.9x

Asset Management Ratios

Dover Corp. 2011 2010 2009 Industry

Inventory Turnover9.9x 10.09x 9.36x 5.8x

Day Sales Outstanding55 days 56 days 60 days N/A

Fixed Asset Turnover7.94x 8.45x 6.45x N/A

Total Asset Turnover0.84x 0.76x 0.68x 0.6x

Profitability Ratios

Market Value Ratios

Debt Management Ratios

Dover Corp. 2011 2010 2009 Industry

Total Debt 48% 47% 48% N/A

Interest Coverage 10.47x 9.48x 5.88x 6.8x

Dover Corp. 2011 2010 2009 Industry

Profit Margin 11.26% 10.54% 6.67% 8.79%

Return on Assets 9.42% 8.18% 4.52% 5.1%

Return on Equity 18.16% 15.47% 8.73% 14.67%

Dover Corp. 2011 2010 2009 Industry

Price Earnings 11.72x 14.86x 20.3x 21x

Market to Book 2.13x 2.3x 1.77x 2.55x

Financial Statement Analysis

Firm Riskiness Economic conditions and uncertainties

Competitive environment

Advanced technology

Increased price/unavailability of raw materials

Litigations

Foreign operations

Beta

Dover’s computed beta: 1.4

(Yahoo Finance) Dover beta: 1.5

Our beta will be used in the Capital Asset Pricing Model that will help calculate the expected return of Dover.

Cost of Equity

Cost of Equity = 9.9%

Risk-free rate = 3.1%

Market risk premium = 5%

β = 1.4

Valuation: Dividend Discount Model

Assumptions Non-constant growth rate: 12.8% Constant growth rate: 5.5% Cost of equity: 9.89%

Valuation for December 2011: $50.45

Stock Price as of 12/31/11: $56.51 per share

Valuation: FCFM

Assumptions Based on past 3 years (2011, 2010, 2009)

Created pro forma financial statement for next 10 years Forecasted unlevered free cash flow Dover’s value was estimated to be $244.25 per share

In comparison to $56.51 per share on December 2011

Valuation: Multiples

Stock Price as of 12/31/11: $56.51 per share

Method 1: Valuation = $54.04

Method 2: Valuation = $65.14

Method 3: Valuation = $140.32

Final Valuation Estimate and Recommendation

Dover’s value estimate for 12/11 is $56.54 per share

Stock price on 12/31/11 was $56.51 per share

Average of – DDM: $50.45 per share– Valuation by Multiples Method

1: $54.04 per share– Method 2: $65.14 per share

Recommendation: BUY!!!

Questions???