garanti bank corporate presentation januarynot … · garanti bank corporate presentation...

TRANSCRIPT

Investor Relations / Corporate Presentation

Garanti Bank Corporate Presentation January 2015

NOT A COINCIDENCE

Investor Relations / Corporate Presentation

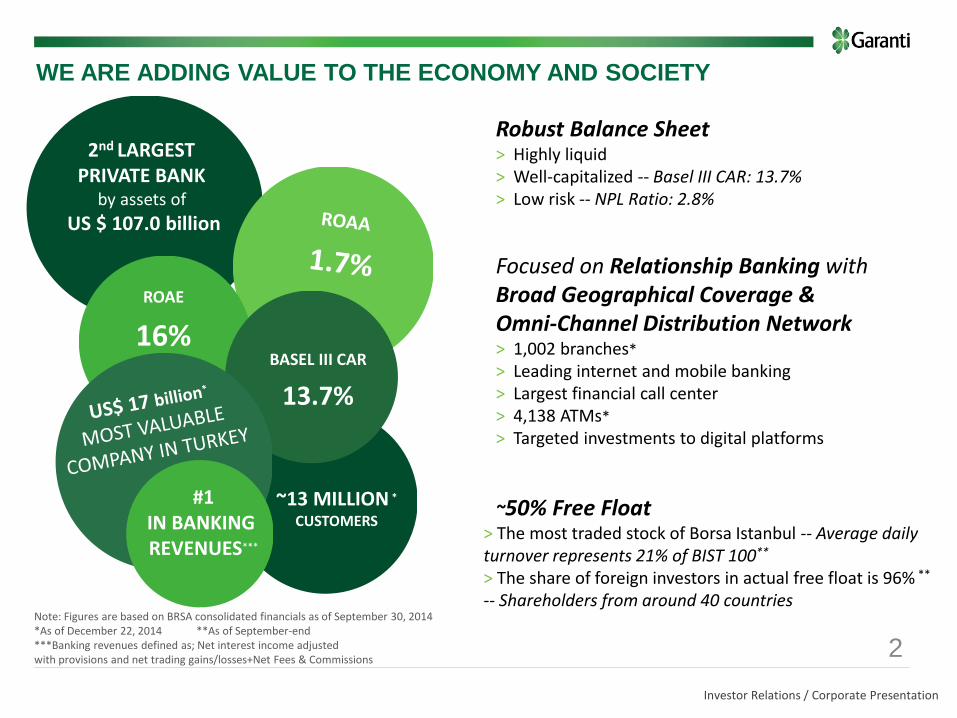

ROAE

16% BASEL III CAR

13.7%

~13 MILLION *

CUSTOMERS

2

WE ARE ADDING VALUE TO THE ECONOMY AND SOCIETY

2nd LARGEST PRIVATE BANK

by assets of

US $ 107.0 billion

Note: Figures are based on BRSA consolidated financials as of September 30, 2014 *As of December 22, 2014 **As of September-end ***Banking revenues defined as; Net interest income adjusted with provisions and net trading gains/losses+Net Fees & Commissions

Focused on Relationship Banking with Broad Geographical Coverage & Omni-Channel Distribution Network > 1,002 branches*

> Leading internet and mobile banking > Largest financial call center > 4,138 ATMs*

> Targeted investments to digital platforms

Robust Balance Sheet > Highly liquid > Well-capitalized -- Basel III CAR: 13.7% > Low risk -- NPL Ratio: 2.8%

#1 IN BANKING REVENUES***

~50% Free Float > The most traded stock of Borsa Istanbul -- Average daily turnover represents 21% of BIST 100**

> The share of foreign investors in actual free float is 96% ** -- Shareholders from around 40 countries

Investor Relations / Corporate Presentation

3

EMPOWERING

SUSTAINABLE

RESPONSIBLE

READY FOR FUTURE

Investor Relations / Corporate Presentation

RESPONSIBLE TOWARDS SOCIETY

Investor Relations / Corporate Presentation

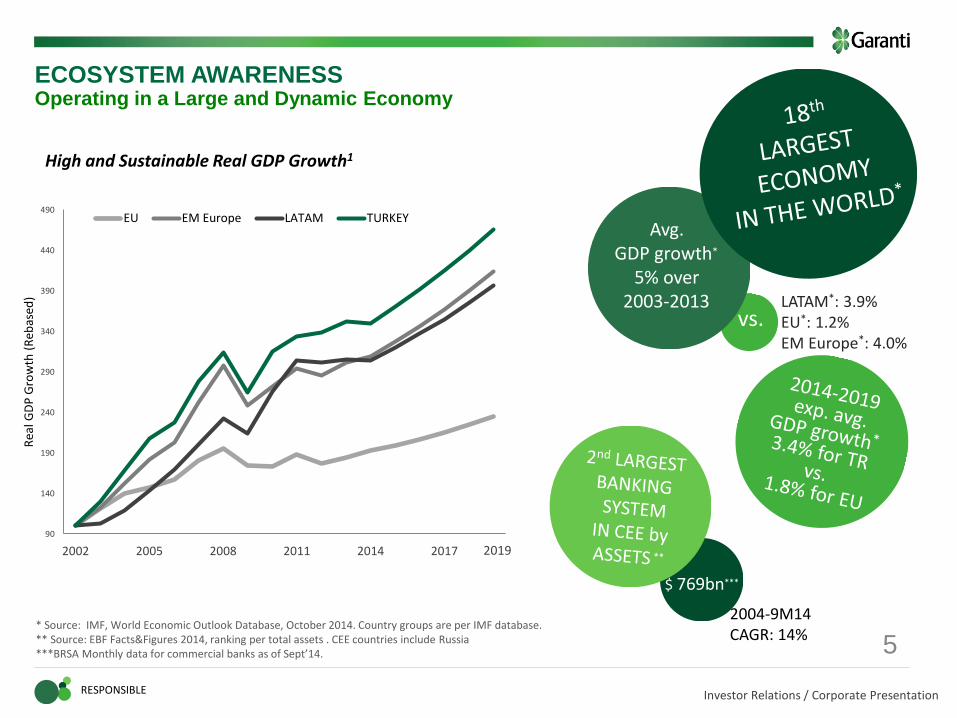

ECOSYSTEM AWARENESS

Operating in a Large and Dynamic Economy

5

High and Sustainable Real GDP Growth1

2004-9M14 CAGR: 14%

Avg. GDP growth*

5% over 2003-2013

* Source: IMF, World Economic Outlook Database, October 2014. Country groups are per IMF database. ** Source: EBF Facts&Figures 2014, ranking per total assets . CEE countries include Russia ***BRSA Monthly data for commercial banks as of Sept’14.

RESPONSIBLE

vs.

$ 769bn***

2019

90

140

190

240

290

340

390

440

490

2002 2005 2008 2011 2014 2017

Rea

l GD

P G

row

th (

Reb

ased

)

EU EM Europe LATAM TURKEY

LATAM*: 3.9% EU*: 1.2% EM Europe*: 4.0%

Investor Relations / Corporate Presentation

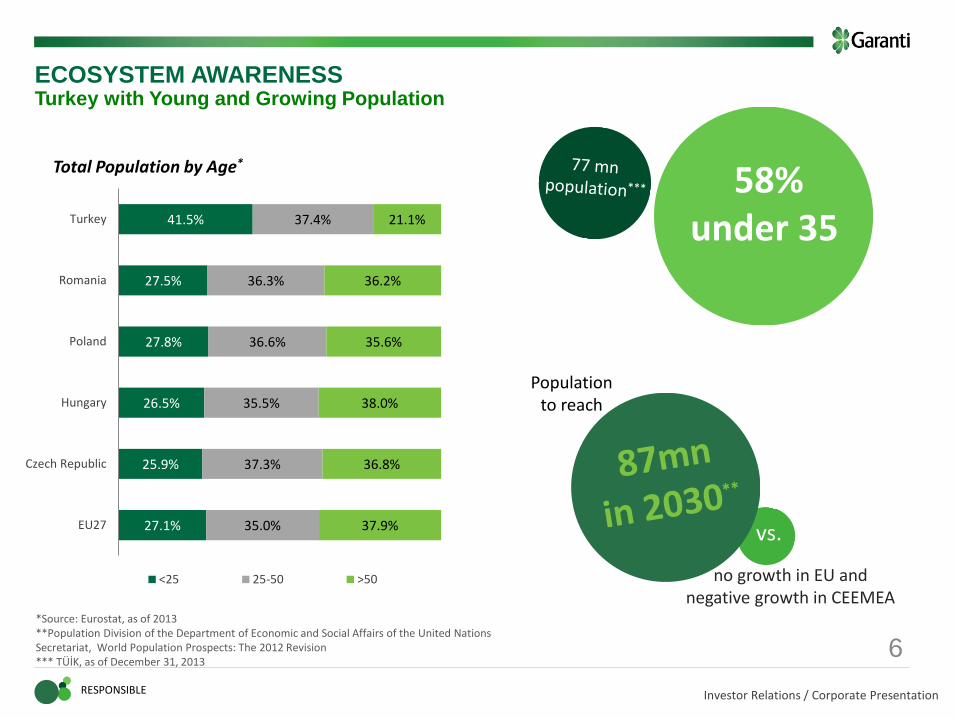

27.1%

25.9%

26.5%

27.8%

27.5%

41.5%

35.0%

37.3%

35.5%

36.6%

36.3%

37.4%

37.9%

36.8%

38.0%

35.6%

36.2%

21.1%

EU27

Czech Republic

Hungary

Poland

Romania

Turkey

<25 25-50 >50

6

Total Population by Age*

no growth in EU and negative growth in CEEMEA

Population to reach

*Source: Eurostat, as of 2013 **Population Division of the Department of Economic and Social Affairs of the United Nations Secretariat, World Population Prospects: The 2012 Revision *** TÜİK, as of December 31, 2013

ECOSYSTEM AWARENESS

Turkey with Young and Growing Population

vs.

58% under 35

RESPONSIBLE

Investor Relations / Corporate Presentation

ECOSYSTEM AWARENESS

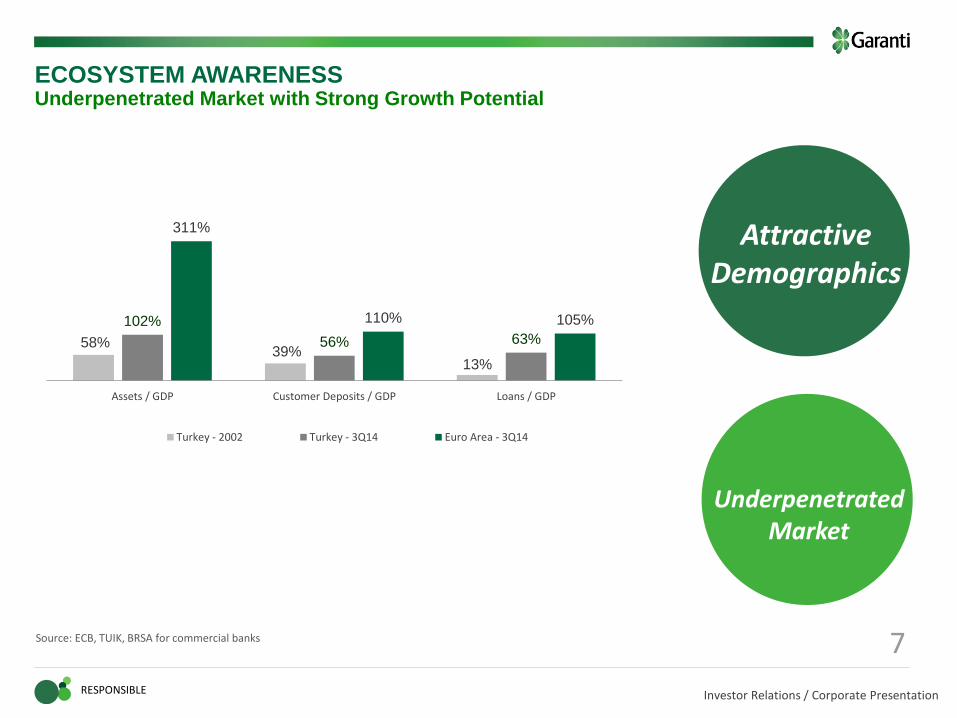

Underpenetrated Market with Strong Growth Potential

RESPONSIBLE

Attractive Demographics

Underpenetrated Market

7 Source: ECB, TUIK, BRSA for commercial banks

58% 39%

13%

102%

56% 63%

311%

110% 105%

Assets / GDP Customer Deposits / GDP Loans / GDP

Turkey - 2002 Turkey - 3Q14 Euro Area - 3Q14

Investor Relations / Corporate Presentation

8

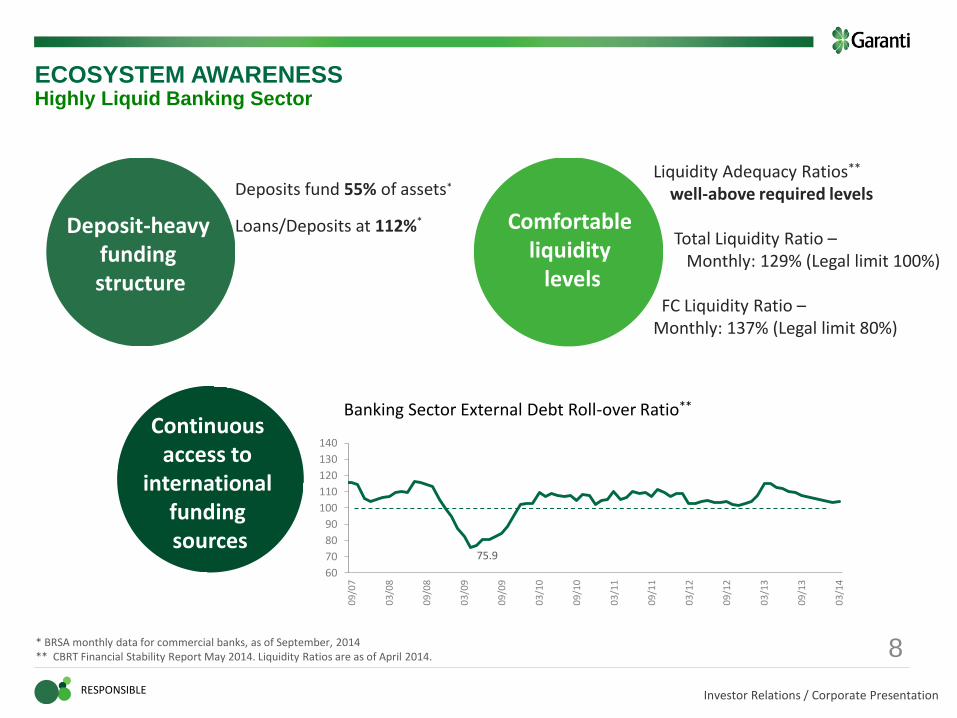

Deposits fund 55% of assets*

Loans/Deposits at 112%*

* BRSA monthly data for commercial banks, as of September, 2014 ** CBRT Financial Stability Report May 2014. Liquidity Ratios are as of April 2014.

ECOSYSTEM AWARENESS

Highly Liquid Banking Sector

Deposit-heavy funding structure

Comfortable liquidity

levels

Liquidity Adequacy Ratios** well-above required levels Total Liquidity Ratio – Monthly: 129% (Legal limit 100%) FC Liquidity Ratio – Monthly: 137% (Legal limit 80%)

Banking Sector External Debt Roll-over Ratio**

Continuous access to

international funding sources

RESPONSIBLE

75.9

60

70

80

90

100

110

120

130

140

09

/07

03

/08

09

/08

03

/09

09

/09

03

/10

09

/10

03

/11

09

/11

03

/12

09

/12

03

/13

09

/13

03

/14

Investor Relations / Corporate Presentation

9 * Source: Latest data from the IMF-FSI database. Most of figures are based on 2Q14 figures ** BRSA monthly data as of September 2014, commercial banks only

ECOSYSTEM AWARENESS

Well-Capitalized and Underleveraged

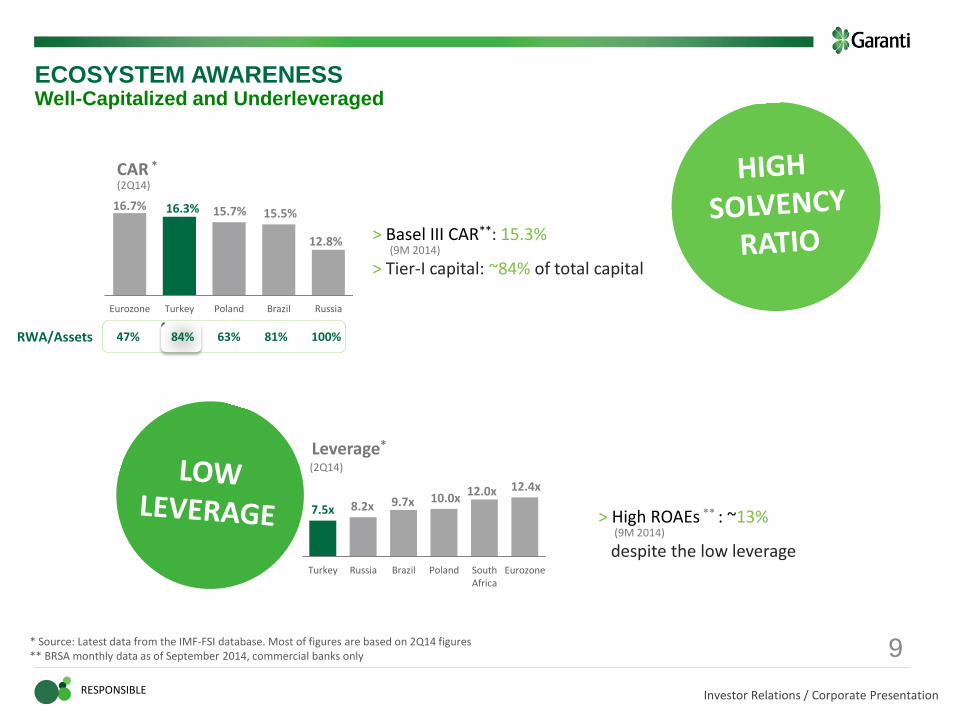

> High ROAEs ** : ~13% (9M 2014)

despite the low leverage

RESPONSIBLE

CAR *

(2Q14)

> Basel III CAR**: 15.3% (9M 2014)

> Tier-I capital: ~84% of total capital

Leverage*

(2Q14)

16.7% 16.3% 15.7% 15.5%

12.8%

Eurozone Turkey Poland Brazil Russia

RWA/Assets 47% 84% 63% 81% 100%

7.5x 8.2x 9.7x 10.0x 12.0x 12.4x

Turkey Russia Brazil Poland SouthAfrica

Eurozone

Investor Relations / Corporate Presentation

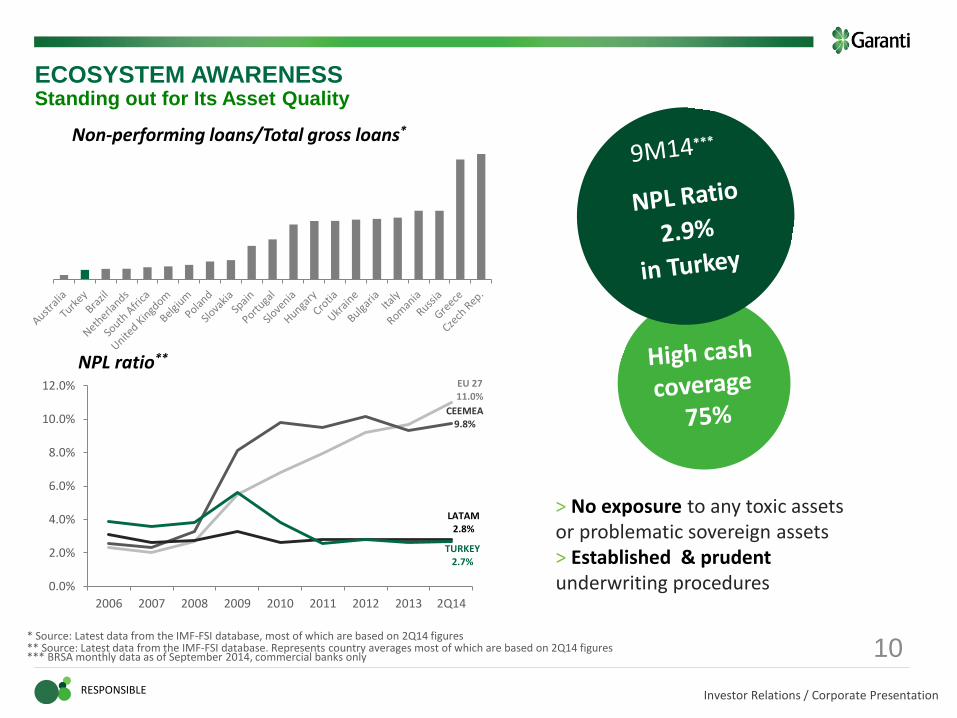

ECOSYSTEM AWARENESS

Standing out for Its Asset Quality

10

Non-performing loans/Total gross loans*

* Source: Latest data from the IMF-FSI database, most of which are based on 2Q14 figures ** Source: Latest data from the IMF-FSI database. Represents country averages most of which are based on 2Q14 figures *** BRSA monthly data as of September 2014, commercial banks only

NPL ratio**

> No exposure to any toxic assets or problematic sovereign assets > Established & prudent underwriting procedures

RESPONSIBLE

EU 27 11.0%

CEEMEA 9.8%

LATAM 2.8%

TURKEY 2.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2006 2007 2008 2009 2010 2011 2012 2013 2Q14

Investor Relations / Corporate Presentation

11

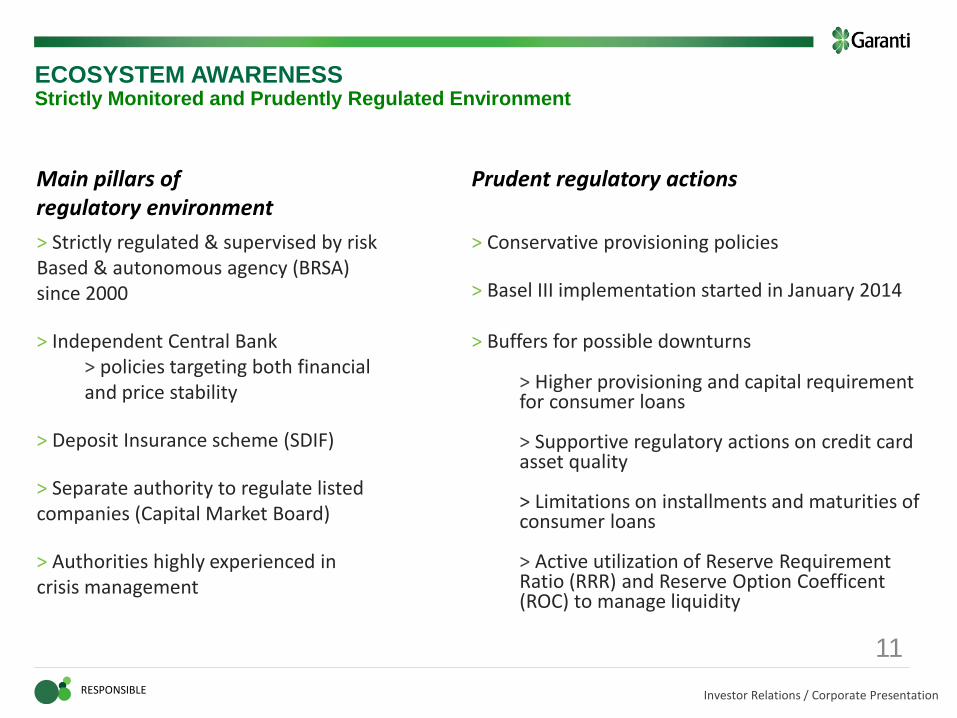

ECOSYSTEM AWARENESS

Strictly Monitored and Prudently Regulated Environment

Main pillars of regulatory environment

> Strictly regulated & supervised by risk Based & autonomous agency (BRSA) since 2000

> Independent Central Bank > policies targeting both financial and price stability

> Deposit Insurance scheme (SDIF)

> Separate authority to regulate listed companies (Capital Market Board)

> Authorities highly experienced in crisis management

Prudent regulatory actions

> Conservative provisioning policies

> Basel III implementation started in January 2014 > Buffers for possible downturns

> Higher provisioning and capital requirement for consumer loans > Supportive regulatory actions on credit card asset quality > Limitations on installments and maturities of consumer loans > Active utilization of Reserve Requirement Ratio (RRR) and Reserve Option Coefficent (ROC) to manage liquidity

RESPONSIBLE

Investor Relations / Corporate Presentation

12

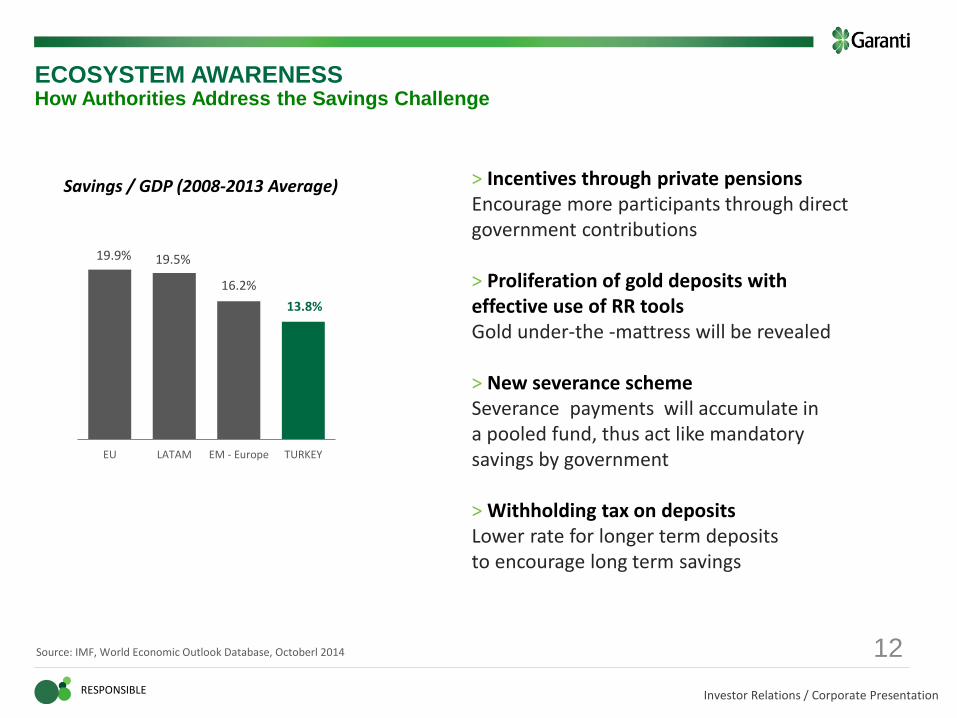

Savings / GDP (2008-2013 Average)

Source: IMF, World Economic Outlook Database, Octoberl 2014

ECOSYSTEM AWARENESS

How Authorities Address the Savings Challenge

> Incentives through private pensions Encourage more participants through direct government contributions

> Proliferation of gold deposits with effective use of RR tools Gold under-the -mattress will be revealed

> New severance scheme Severance payments will accumulate in a pooled fund, thus act like mandatory savings by government

> Withholding tax on deposits Lower rate for longer term deposits to encourage long term savings

RESPONSIBLE

19.9% 19.5%

16.2%

13.8%

EU LATAM EM - Europe TURKEY

Investor Relations / Corporate Presentation

13

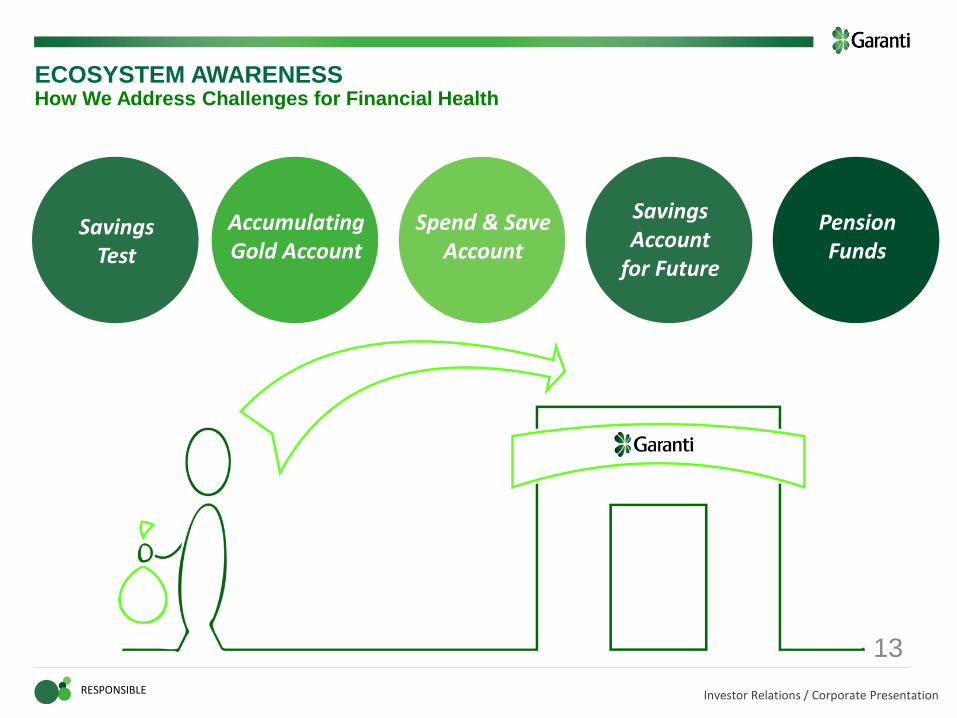

ECOSYSTEM AWARENESS

How We Address Challenges for Financial Health

RESPONSIBLE

Savings Test

Accumulating Gold Account

Spend & Save Account

Savings Account

for Future

Pension Funds

Investor Relations / Corporate Presentation

14

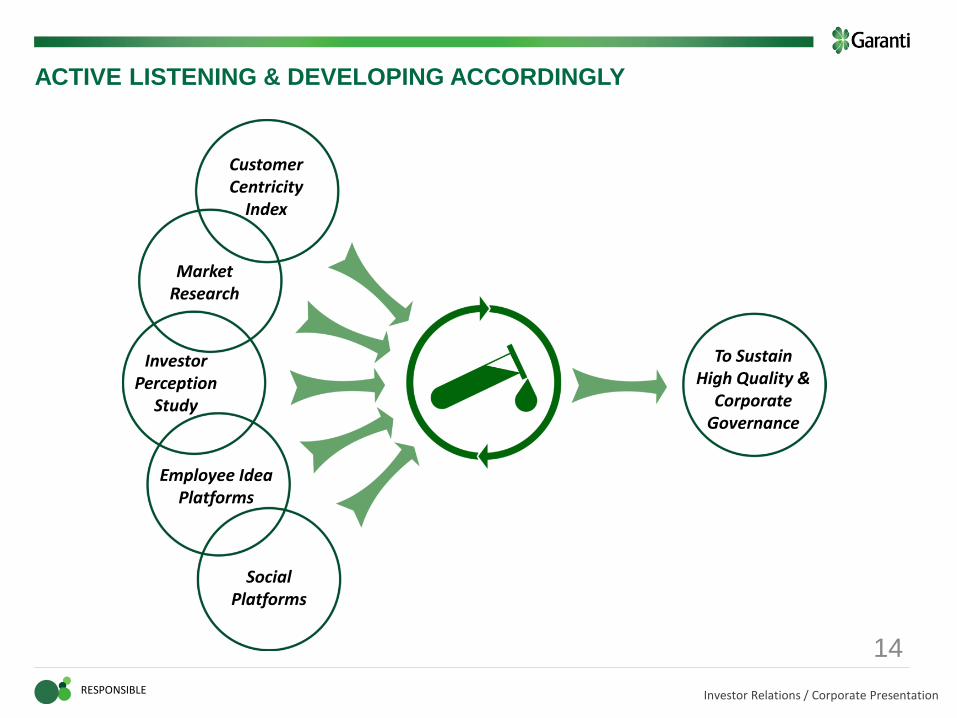

ACTIVE LISTENING & DEVELOPING ACCORDINGLY

RESPONSIBLE

Social Platforms

Customer Centricity

Index

Market Research

Investor Perception

Study

Employee Idea Platforms

To Sustain

High Quality & Corporate

Governance

Investor Relations / Corporate Presentation

EMPOWERING IN ALL POSSIBLE DIMENSIONS

Investor Relations / Corporate Presentation

16

SINGLE POINT OF CONTACT FOR ALL FINANCIAL NEEDS

EMPOWERING

Commercial

Payment Systems

Digital Banking

SME

Corporate

Consumer

Note: Asset contribuions are calculated based on BRSA Consolidated Financials as of September 30, 2014

Asset Contribution: 5.2%

Asset Contribution: 2.3%

Asset Contribution: 0.4%

Asset Contribution: 1.6%

Asset Contribution: 1.0%

Asset Contribution: 2.8%

Asset Contribution: 0.0%

Asset Contribution: 0.0%

Investor Relations / Corporate Presentation EMPOWERING

17

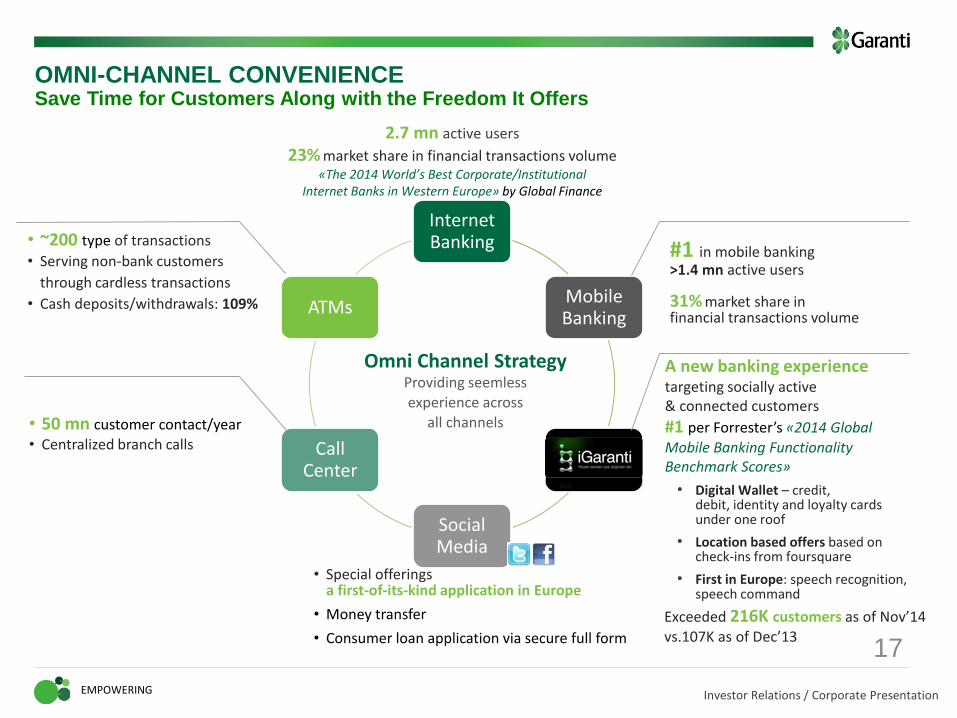

OMNI-CHANNEL CONVENIENCE

Save Time for Customers Along with the Freedom It Offers

Internet Banking

Mobile Banking

Social Media

Call Center

ATMs

Omni Channel Strategy Providing seemless experience across

all channels

2.7 mn active users

23% market share in financial transactions volume «The 2014 World’s Best Corporate/Institutional

Internet Banks in Western Europe» by Global Finance

• ~200 type of transactions

• Serving non-bank customers

through cardless transactions

• Cash deposits/withdrawals: 109%

• 50 mn customer contact/year • Centralized branch calls

• Special offerings a first-of-its-kind application in Europe

• Money transfer

• Consumer loan application via secure full form

#1 in mobile banking >1.4 mn active users 31% market share in financial transactions volume

A new banking experience targeting socially active & connected customers

#1 per Forrester’s «2014 Global

Mobile Banking Functionality Benchmark Scores»

• Digital Wallet – credit, debit, identity and loyalty cards under one roof

• Location based offers based on check-ins from foursquare

• First in Europe: speech recognition, speech command

Exceeded 216K customers as of Nov’14 vs.107K as of Dec’13

Investor Relations / Corporate Presentation

18

CULTURE OF PARTICIPATION & SHARING IN DECISION MAKING

Management Information

at all levels for performance monitoring

> Bank level

> Business line level

> Region level

> Branch level

> Sales person level

> Customer level

A single source of data & common understanding

> Single data dictionary

> Standardized management reports

> Consolidated data into MR platform

Platform for management and legal reporting

> Transparency

> Accountability

> Governance

EMPOWERING

Performance Management

Successful Decision Making

Investor Relations / Corporate Presentation

SUSTAINABLE FOR A BETTER LIFE

Investor Relations / Corporate Presentation

20

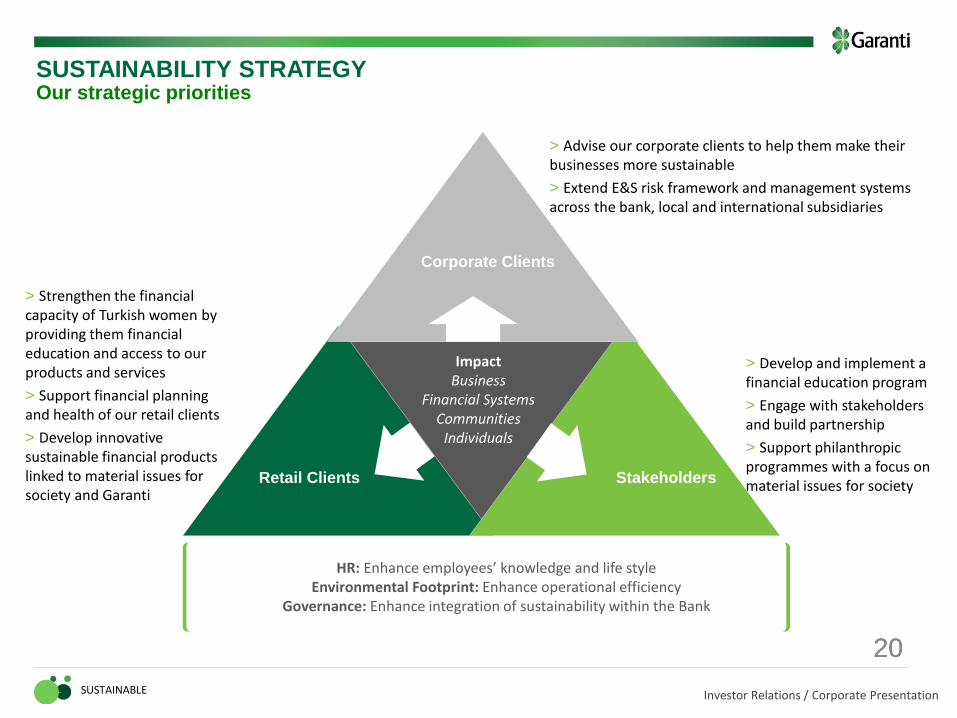

SUSTAINABILITY STRATEGY Our strategic priorities

20

SUSTAINABLE

Performance Management Performance Management

Corporate Clients

Impact Business

Financial Systems Communities

Individuals

Retail Clients

> Advise our corporate clients to help them make their businesses more sustainable

> Extend E&S risk framework and management systems across the bank, local and international subsidiaries

> Strengthen the financial capacity of Turkish women by providing them financial education and access to our products and services

> Support financial planning and health of our retail clients

> Develop innovative sustainable financial products linked to material issues for society and Garanti

> Develop and implement a financial education program

> Engage with stakeholders and build partnership

> Support philanthropic programmes with a focus on material issues for society

HR: Enhance employees’ knowledge and life style Environmental Footprint: Enhance operational efficiency

Governance: Enhance integration of sustainability within the Bank

Stakeholders

Investor Relations / Corporate Presentation

SUSTAINABILITY STRATEGY Key Achievements

SUSTAINABLE 21

21

21

Performance Management

21

Performance Management

Corporate Clients

Stakeholders

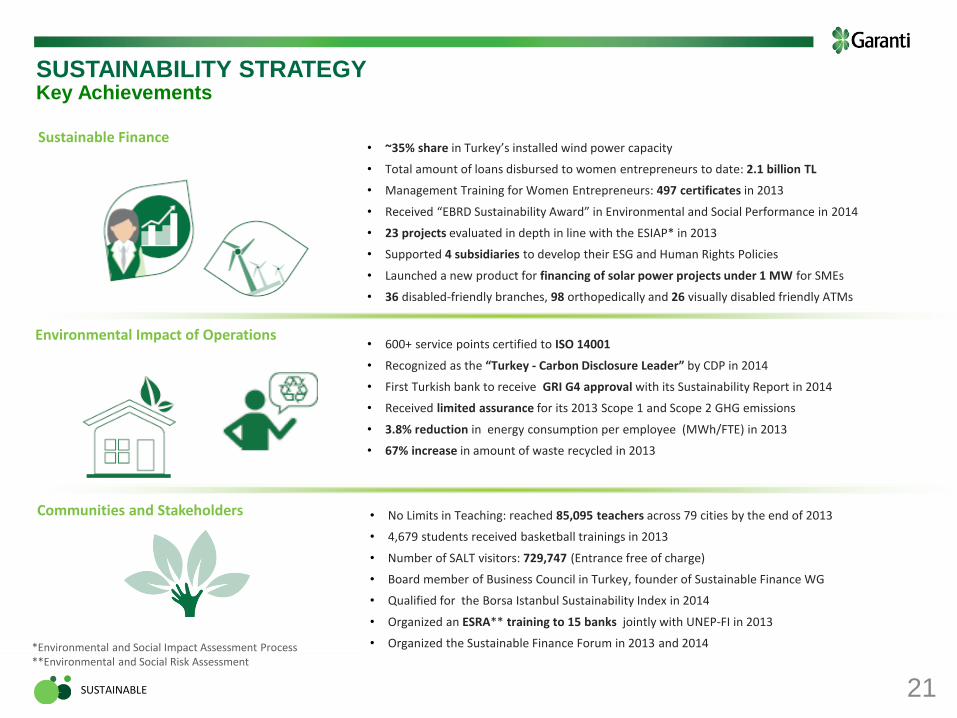

• 600+ service points certified to ISO 14001

• Recognized as the “Turkey - Carbon Disclosure Leader” by CDP in 2014

• First Turkish bank to receive GRI G4 approval with its Sustainability Report in 2014

• Received limited assurance for its 2013 Scope 1 and Scope 2 GHG emissions

• 3.8% reduction in energy consumption per employee (MWh/FTE) in 2013

• 67% increase in amount of waste recycled in 2013

Communities and Stakeholders

Environmental Impact of Operations

• No Limits in Teaching: reached 85,095 teachers across 79 cities by the end of 2013

• 4,679 students received basketball trainings in 2013

• Number of SALT visitors: 729,747 (Entrance free of charge)

• Board member of Business Council in Turkey, founder of Sustainable Finance WG

• Qualified for the Borsa Istanbul Sustainability Index in 2014

• Organized an ESRA** training to 15 banks jointly with UNEP-FI in 2013

• Organized the Sustainable Finance Forum in 2013 and 2014

Sustainable Finance

21

• ~35% share in Turkey’s installed wind power capacity

• Total amount of loans disbursed to women entrepreneurs to date: 2.1 billion TL

• Management Training for Women Entrepreneurs: 497 certificates in 2013

• Received “EBRD Sustainability Award” in Environmental and Social Performance in 2014

• 23 projects evaluated in depth in line with the ESIAP* in 2013

• Supported 4 subsidiaries to develop their ESG and Human Rights Policies

• Launched a new product for financing of solar power projects under 1 MW for SMEs

• 36 disabled-friendly branches, 98 orthopedically and 26 visually disabled friendly ATMs

*Environmental and Social Impact Assessment Process **Environmental and Social Risk Assessment

Investor Relations / Corporate Presentation

22

INNOVATIVE BUSINESS MODEL

SUSTAINABLE

Process Technology

People

Investor Relations / Corporate Presentation

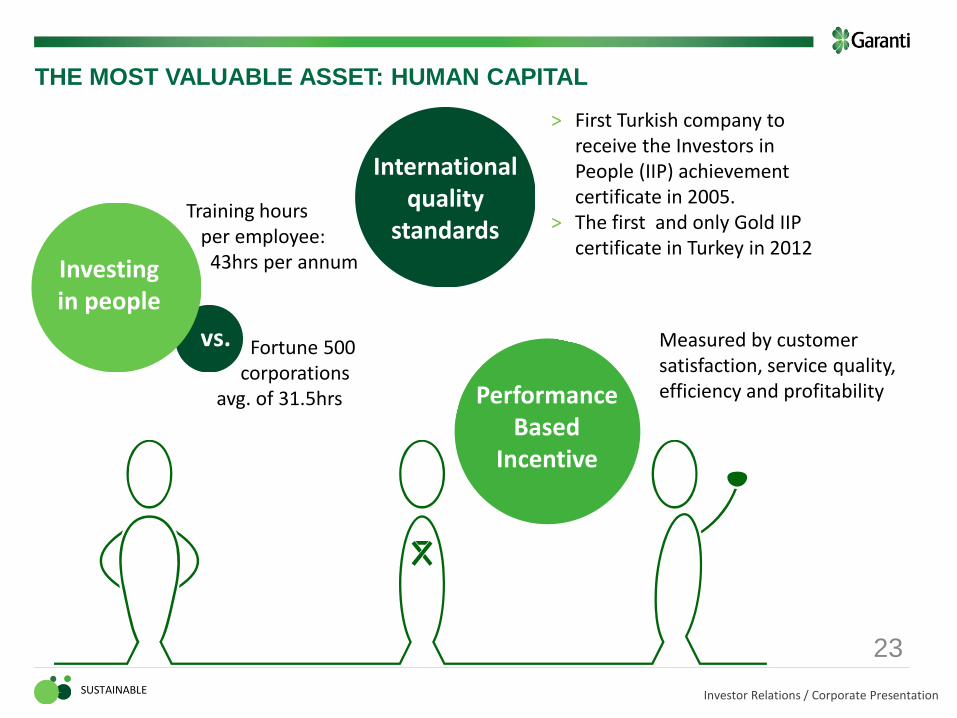

Training hours per employee: 43hrs per annum

23

THE MOST VALUABLE ASSET: HUMAN CAPITAL

SUSTAINABLE

I International

quality standards

Performance Based

Incentive

> First Turkish company to receive the Investors in People (IIP) achievement certificate in 2005. > The first and only Gold IIP

certificate in Turkey in 2012

Measured by customer satisfaction, service quality, efficiency and profitability

vs.

Investing in people

Fortune 500 corporations

avg. of 31.5hrs

Investor Relations / Corporate Presentation

24

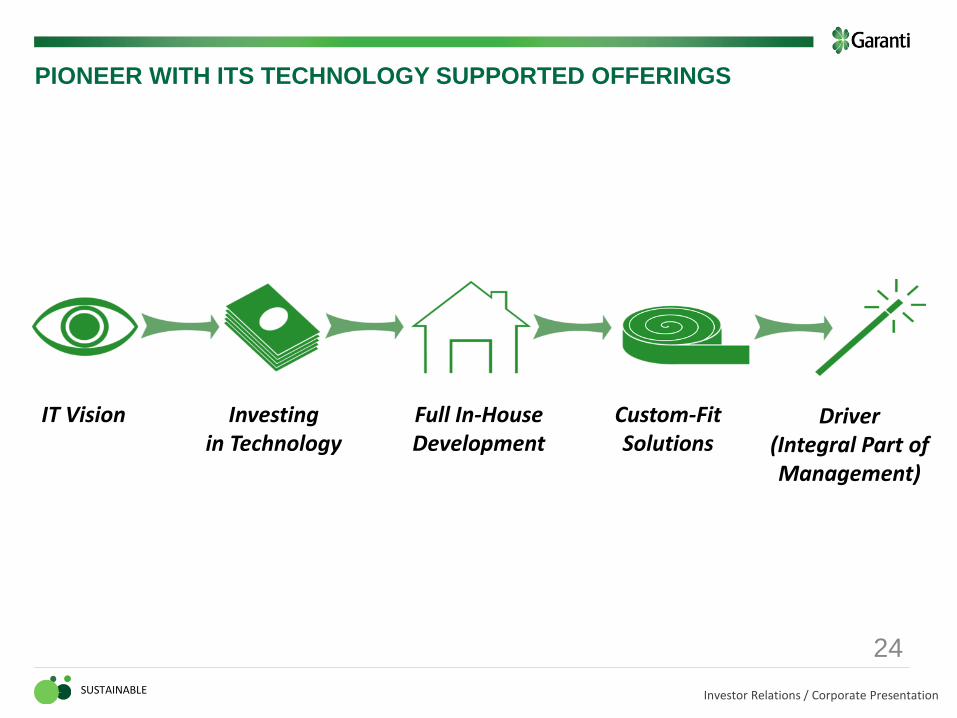

PIONEER WITH ITS TECHNOLOGY SUPPORTED OFFERINGS

SUSTAINABLE

IT Vision Investing in Technology

Full In-House Development

Custom-Fit Solutions

Driver (Integral Part of Management)

Investor Relations / Corporate Presentation

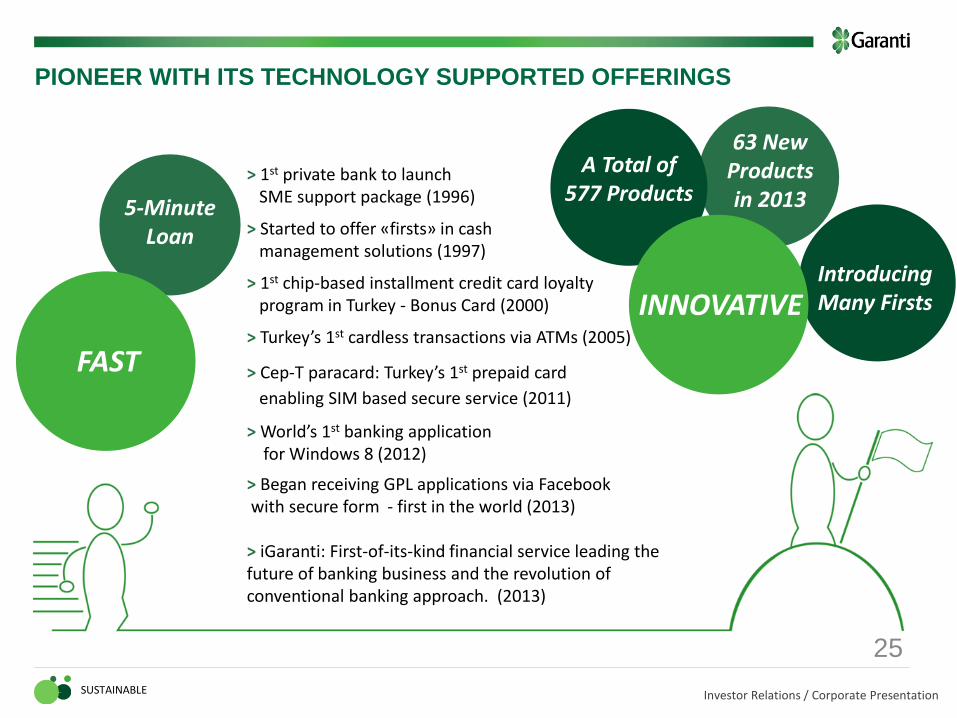

63 New Products in 2013

25

SUSTAINABLE

PIONEER WITH ITS TECHNOLOGY SUPPORTED OFFERINGS

5-Minute Loan

FAST

INNOVATIVE

A Total of 577 Products

Introducing Many Firsts

> 1st private bank to launch SME support package (1996)

> Started to offer «firsts» in cash management solutions (1997)

> 1st chip-based installment credit card loyalty program in Turkey - Bonus Card (2000)

> Turkey’s 1st cardless transactions via ATMs (2005)

> Cep-T paracard: Turkey’s 1st prepaid card

enabling SIM based secure service (2011)

> World’s 1st banking application for Windows 8 (2012)

> Began receiving GPL applications via Facebook with secure form - first in the world (2013) > iGaranti: First-of-its-kind financial service leading the future of banking business and the revolution of conventional banking approach. (2013)

Investor Relations / Corporate Presentation

26

SUSTAINABLE

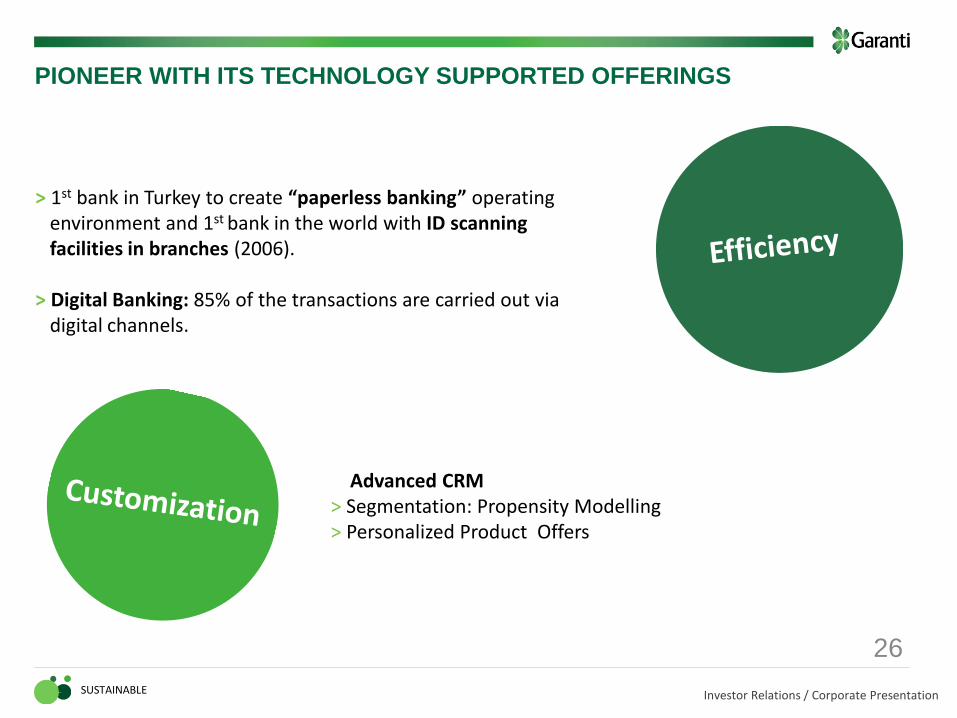

PIONEER WITH ITS TECHNOLOGY SUPPORTED OFFERINGS

> 1st bank in Turkey to create “paperless banking” operating environment and 1st bank in the world with ID scanning facilities in branches (2006). > Digital Banking: 85% of the transactions are carried out via digital channels.

Advanced CRM > Segmentation: Propensity Modelling > Personalized Product Offers

Investor Relations / Corporate Presentation

27

LESS IS MORE

SUSTAINABLE

> 1st Bank to set up centralized operations in Turkey > 99% Operational Centralization Ratio

> Electronic Data Warehousing > Highest per branch efficiencies in terms of assets, loans and ordinary banking income

Smarter Touch-Points for All

Investor Relations / Corporate Presentation

28

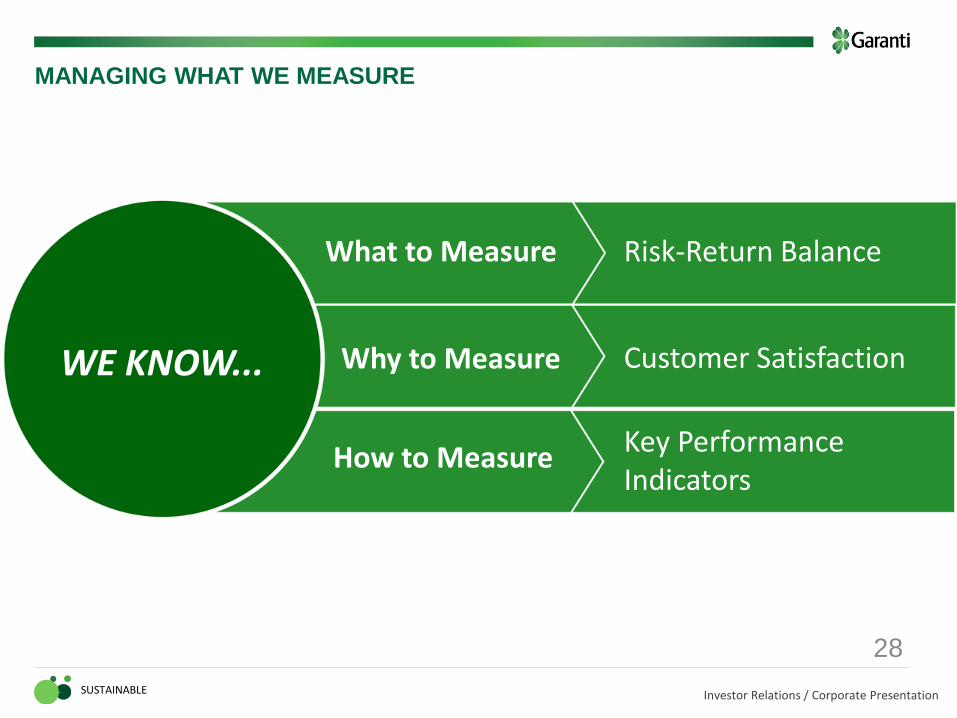

MANAGING WHAT WE MEASURE

SUSTAINABLE

WE KNOW...

What to Measure

Why to Measure

How to Measure

Risk-Return Balance

Customer Satisfaction

Key Performance Indicators

Investor Relations / Corporate Presentation SUSTAINABLE

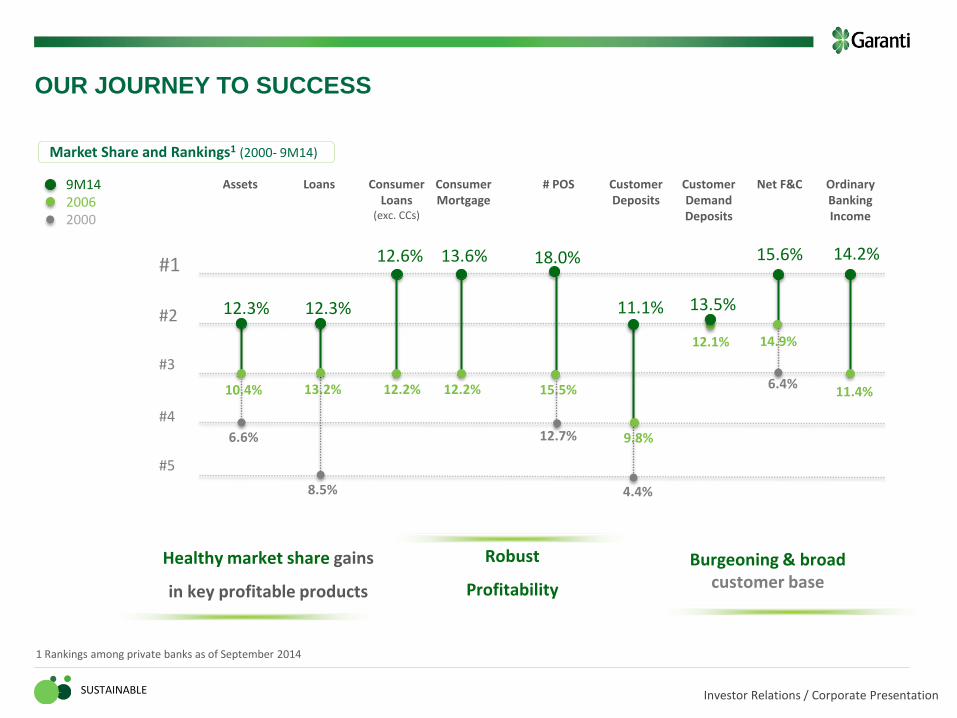

OUR JOURNEY TO SUCCESS

Assets Loans Consumer Loans

(exc. CCs)

ConsumerMortgage

# POS Customer Deposits

Customer Demand Deposits

Net F&C Ordinary Banking Income

12.3%

#1

#2

#3

#4

13.2%

12.3%

12.2%

12.6%

9M14 2006 2000

9.8%

11.1%

15.5%

18.0%

13.5%

12.1%

15.6%

14.9%

14.2%

11.4%

Market Share and Rankings1 (2000- 9M14)

Healthy market share gains

in key profitable products

Robust

Profitability

Burgeoning & broad customer base

10.4%

6.6%

#5

8.5% 4.4%

12.7%

6.4% 12.2%

13.6%

1 Rankings among private banks as of September 2014

Investor Relations / Corporate Presentation

READY FOR FUTURE

Investor Relations / Corporate Presentation

DISCLAIMER STATEMENT

Türkiye Garanti Bankasi A.Ş. (the “TGB”) has prepared this presentation document (the “Document”) thereto for the sole purposes of providing information which include forward looking projections and statements relating to the TGB (the “Information”). No representation or warranty is made by TGB for the accuracy or completeness of the Information contained herein. The Information is subject to change without any notice. Neither the Document nor the Information can construe any investment advise, or an offer to buy or sell TGB shares. This Document and/or the Information cannot be copied, disclosed or distributed to any person other than the person to whom the Document and/or Information delivered or sent by TGB or who required a copy of the same from the TGB. TGB expressly disclaims any and all liability for any statements including any forward looking projections and statements, expressed, implied, contained herein, or for any omissions from Information or any other written or oral communication transmitted or made available.

Investor Relations Levent Nispetiye Mah. Aytar Cad. No:2 Beşiktaş 34340 Istanbul – Turkey Email: [email protected] Tel: +90 (212) 318 2352 Fax: +90 (212) 216 5902 Internet: www.garantiinvestorrelations.com

/garantibankasi