idc predictions 2015

TRANSCRIPT

IDC Predictions 2015

Accelerating Innovation - and Growth - on the 3rd Platform

Frank Gens

SVP & Chief Analyst

December 2, 2014

and Q&A with the

IDC Predictions 2015 Team

IDC Predictions 2015 Team Larry Carvalho

Gary Chen

Ruthbea Clarke

Matt Davis

Marc DeCastro

Crawford DelPrete

Lynne Dunbrack

Matt Eastwood

Kitty Fok

Frank Gens

Al Gillen

Leslie Hand

Judy Hanover

John Jackson

Jialin Jiang

Keith Kmetz

Kimberly Knickle

Charles Kolodgy

Ramon Llamas

Carrie MacGillivray

Robert Mahowald

Tom Mainelli

Stephen Minton

Henry Morris

Courtney Munroe

Bob Parker

Melanie Posey

2

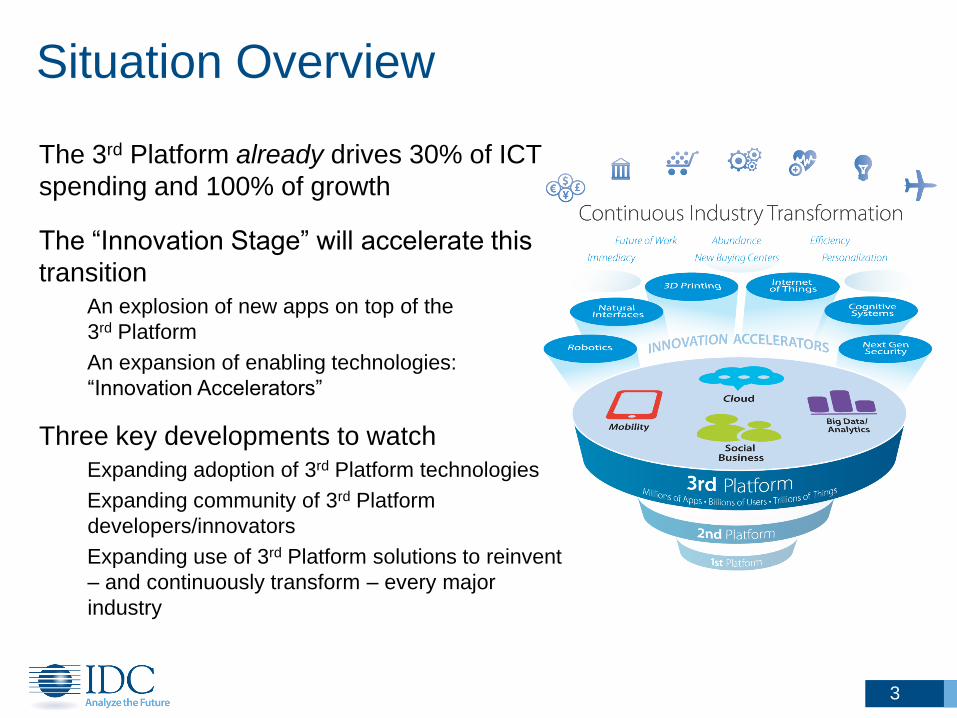

Situation Overview

The 3rd Platform already drives 30% of ICT

spending and 100% of growth

The “Innovation Stage” will accelerate this

transition

An explosion of new apps on top of the

3rd Platform

An expansion of enabling technologies:

“Innovation Accelerators”

Three key developments to watch

Expanding adoption of 3rd Platform technologies

Expanding community of 3rd Platform

developers/innovators

Expanding use of 3rd Platform solutions to reinvent

– and continuously transform – every major

industry

3

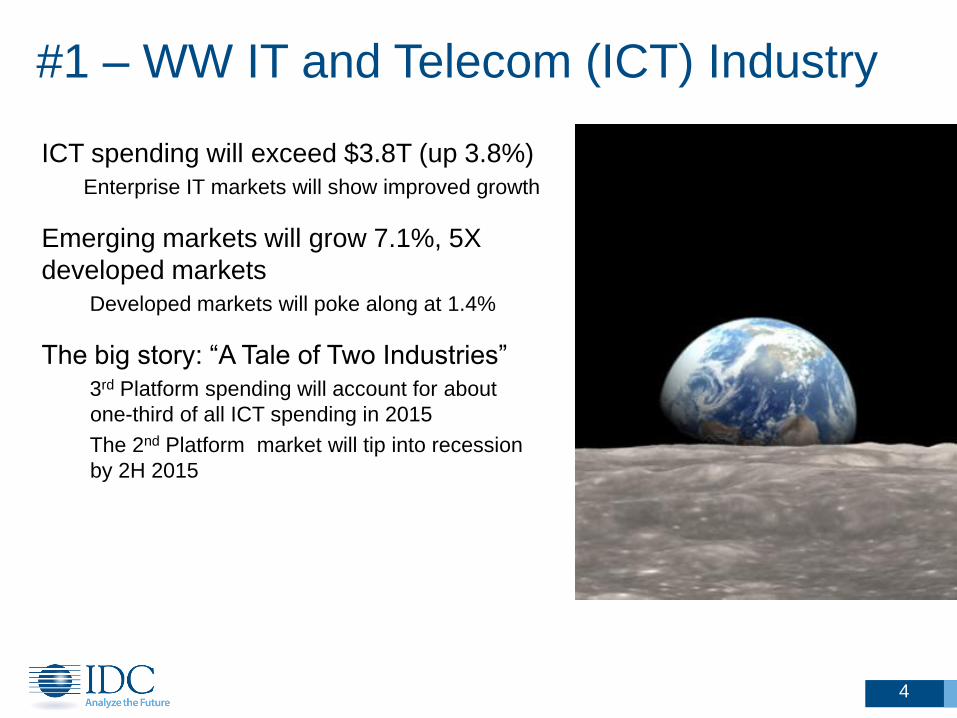

#1 – WW IT and Telecom (ICT) Industry

4

ICT spending will exceed $3.8T (up 3.8%)

Enterprise IT markets will show improved growth

Emerging markets will grow 7.1%, 5X

developed markets

Developed markets will poke along at 1.4%

The big story: “A Tale of Two Industries”

3rd Platform spending will account for about

one-third of all ICT spending in 2015

The 2nd Platform market will tip into recession

by 2H 2015

#2 – Telecom Services

5

Wireless data will be the biggest ($536B)

and fastest-growing (13%) Telecom Services

sector

Eroding margins will drive faster innovation

Expanding portfolios of high-value, API-based

services

Rapprochement with major over-the-top (OTT)

service providers

Net neutrality will be mandated in the U.S.

A “hybrid” approach will leave room for mutually-

beneficial Telco/OTT deals

#3 – Mobile Devices & Apps

6

Smartphones and Tablets will generate 40% of

all IT growth (excludes telecom services)

Phablet sales will grow 60%, cannibalize tablet sales

Chinese smartphone OEMs’ market share will surge

Wearables unit sales will underwhelm in 2015

A wrist-phone will ship, and flop

Mobile app download growth will slow, hit

150B

Apple, Google will account for almost 80%

Chinese independent apps stores: 18%

Enterprise mobile app development will more

than double

#4 – Cloud Services

7

Public cloud services sales will near $70B

The “greater cloud market” – including public, private

clouds, and enabling IT and services – will hit $118B

IaaS competition will intensify

Amazon under attack, will hold/gain share

Many 2nd tier public IaaS clouds will drop out; Google,

Microsoft, IBM, China SPs will gain share

PaaS Wars will expand

# of apps in leading marketplaces will double

% of SaaS vendors using PaaS will hit 15%; 50% by

2018

Container adoption will disrupt VMware, Microsoft

IoT, Cognitive/Machine Learning new PaaS hot spots

“Strange bedfellow” partnerships multiply

Facebook, HP, Salesforce.com, et al.

#5 – Big Data & Analytics

8

Big data & analytics market will reach $125B

Rich media analytics will at least triple in

2015

Video, Audio, and Image analytics and search:

expanding use cases in many industries

“Data supply chains” will be a top priority for

PaaS and analytics vendors

25% of top IT vendors will offer Data-as-a-Service

IoT will be the next critical focus for

data/analytics services

30% CAGR over the next five years

The “Year of Cognitive/Machine Learning”

Growing number of apps and competitors

#6 – The Internet of Things

9

IoT spending will exceed $1.7T, up 14%

1/3 of spending for intelligent/embedded devices

outside of the ICT industry

Cisco, IBM, Intel will form an IoT solutions

company

Challenging IT industry players (like Pivotal) and

industry-focused players (like Bosch, Schneider

Electric and GE)

“IoT Backend as a Service” will emerge from

PaaS and Industry Platform players

Predictive maintenance will lead the IoT solutions

category

#7 – 3rd Platform Data Centers

10

Data center growth will accelerate toward SPs

By 2016, over 50% of compute, 70% of storage

capacity will be installed in hyperscale data centers

Cloud SPs will drive a new renaissance in IT

hardware innovation

Lots of new workload-specialized system designs will

emerge from Cloud SPs in 2015/2016 and beyond

Consolidation will continue among OEMS

Across server, storage, and networking silos

Look for increasing number of OEM/ODM

strategic partnerships, M&A

#8 – 3rd Platform Industries

11

1/3 of market share leaders in every industry

will be disrupted by 3rd Platform competitors

Expanded customer reach, faster offering launch,

expanded supply/distribution networks, transformed

cost model

The number of Industry Platforms/

Communities will double in 2015

At least 60 by year end; over 100 by YE2016

Numerous 3rd Platform-driven industry

disruptions emerge in 2015

Financial Services: Alternative payment systems

Government: Cities will play big roles in IoT roll-out

Retail: Location-based services will increase same

shopper sales through engagement; real-time

competitive pricing is next.

#9 – Innovation Accelerators

12

3rd Platform-optimized Security

Securing the edge: 15% of mobile devices will be

accessed biometrically (over 50% by 2020)

Securing the core: 20% of regulated data will be

encrypted by YE2015 (80% by 2018)

Threat intelligence as a service: by 2017, 55% of

enterprises will receive customized threat intelligence

data feeds

3D Printing

By 2020, 10%+ of consumer products will be

available through “produce on demand” via 3D

printing

2015 spending will surge 27%, to $3.4B

Canon, Ricoh and Epson: prepping market entry

Stratsys and 3D Systems will continue to scale

through M&A

#10 – China

13

ICT spending of $465B+, growing over 11%

Accounting for 43% of total ICT industry growth

Domestic engines for 3rd Platform growth are

roaring

Mobile, Internet, Social, and Online Shopping

China’s cloud and ecommerce leaders will

challenge for global leadership

Alibaba, Tencent, Baidu

Chinese smartphone OEMs will grab 40% of

global share

Lenovo/Motorola, Xiaomi, Huawei, ZTE, and Coolpad

China’s 13th 5-Year Plan will be built on 3rd

Platform technologies, investments

Essential Guidance

14

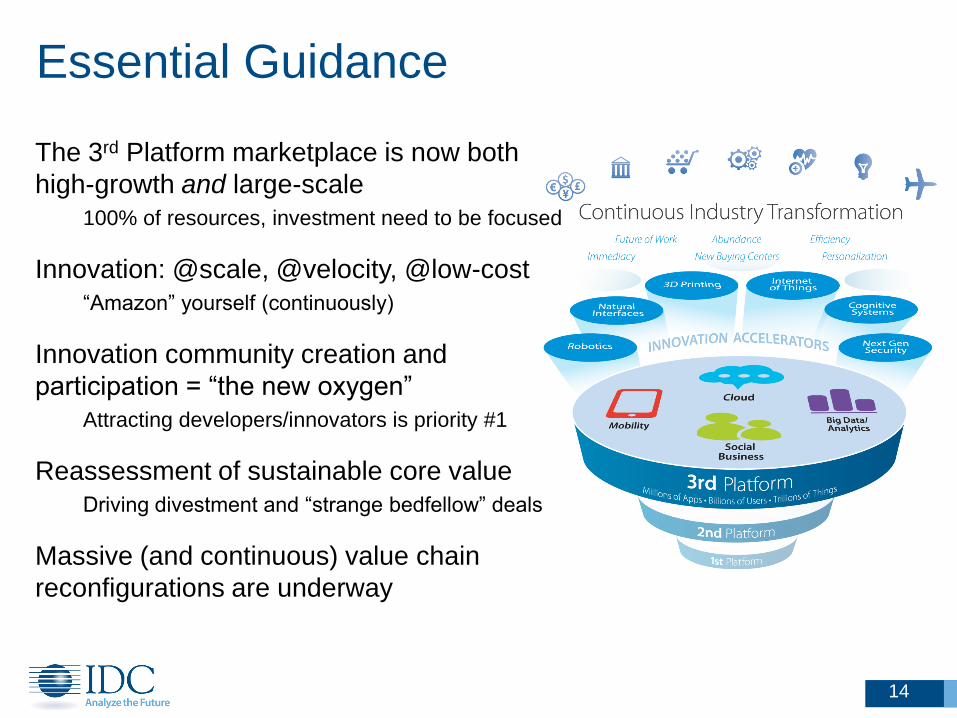

The 3rd Platform marketplace is now both

high-growth and large-scale

100% of resources, investment need to be focused

Innovation: @scale, @velocity, @low-cost

“Amazon” yourself (continuously)

Innovation community creation and

participation = “the new oxygen”

Attracting developers/innovators is priority #1

Reassessment of sustainable core value

Driving divestment and “strange bedfellow” deals

Massive (and continuous) value chain

reconfigurations are underway

idc.com/predictions2015

15

IDC doc#252700

Joining Us for Q&A

16

Larry Carvalho

Crawford DelPrete

Matt Eastwood

John Jackson

Keith Kmetz

Charles Kolodgy

Stephen Minton

Henry Morris

Courtney Munroe

Melanie Posey

Dave Schubmehl

Vernon Turner

Dan Vesset

Rick Villars

James Wester

Meredith Whalen