it s showtime! digital drives the agenda, data delivers ... · it’s showtime! digital drives the...

TRANSCRIPT

It’s showtime!Digital drives the agenda,data delivers the insightsMedia & Entertainment

Global Media & Entertainment Center

For the first time since the great recession of 2008, media and entertainment (M&E) chief financial officers (CFOs) have shifted their primary focus from cost reduction and operational efficiencies to optimizing the organization for growth. Today’s priority for an overwhelming 74% of CFOs is the evolution of digital — using digital to drive their growth agenda and data to deliver the insights that enable game-changing decision-making.

In our sixth in a series of executive reports, 50 CFOs from leading M&E companies around the world share these and other views on the current and future direction of the industry. The CFOs we interviewed represent M&E companies with combined annual revenues exceeding US$475b globally, spanning eight media and entertainment industry sectors and 10 geographies.

About this reportFigure 1Company size — annual revenues (in US$)(numbers of participating companies*)

$500m–$999m

Less than $500m

$1b–$4.9b

$5b–$9.9b

$10b–$25b

Greater than $25b 6

4

8

14

6

9

5 10 15

face-to-face interviews completed with the world’s leading media and

entertainment CFOs

50

* If more than one division or subsidiary participated, consolidated parent company revenues have been included.

It’s showtime! Digital drives the agenda, data delivers the insights

Figure 2Headquarters of participating companies

United States52%

India12%

China8%

Australia8%

United Kingdom

6%

France4%

Russia4%

Canada2%

Japan2%

Brazil2%

Figure 3Companies by sub-sector

Publishing and

information services

20%

Filmed entertainment

18%

Broadcast and cable networks

16%

Media conglomerates

14%

Music/radio4%Cable/satellite

distributors8%

Internet and interactive media

10%

Advertising and measurement

10%

countriesrepresented

billion of media and entertainment revenue represented by participating

companies (approximately)

media and entertainment sectors represented

810Over

$475

Figure 4Geographic distribution of revenue of participating companies

North America48.1%

Europe14.9%

Japan9.3%

Asia Pacific7.2%

Latin America3.2%

Australia/New Zealand

1.8% ROW15.5%

To augment our interview findings, we have used proprietary EY analyses and secondary research to provide depth and context.

We promote an environment of openness and candor during the interview process. As such, none of the comments or quotes used in this report is attributed to any participant. We would like to take a moment to thank all participants for their time and the insights they generously provided. Their involvement was instrumental in the creation of this report.

Participating CFOs and executives*

Global Media & Entertainment Center

Howard M. AverillExecutive Vice President and CFOTime Warner Inc.

Jimmy BargeCFOLionsgate Entertainment Corp.

Manuel BelmarCFOGlobosat Programadora Ltda.

Gregoire CastaingCFOCanal+ Groupe

Nicholas ChongCFOAutohome Inc.

Lewis ColemanPresident and CFODreamworks Animation SKG, Inc.

Laurence DebrouxGroup CFOJC Decaux

Patrick T. DoyleExecutive Vice President and CFODIRECTV, Inc.

Bernard G. DvorakExecutive Vice President and Co-CFOLiberty Global, plc

James FolloCFOThe New York Times Company

Sambasivan GCFO Tata Sky Limited

Ian Griffi thsCFO ITV plc

Joseph GuCFO China Media Capital

Piyush GuptaCFO HT Media Ltd.

Andrew HeffernanCFOEros International plc

David C. HendlerSenior Executive Vice President and CFOSony Pictures Entertainment

Andrew HobsonSenior Executive Vice President and CFOUnivision Communications Inc.

David HousegoCFOFairfax Media Limited

Simon KellyChief Operating Offi cer and CFONine Entertainment Company

Steven E. KoberExecutive Vice President and CFOSony Corporation of America

Mitch KochCFO Interactive Entertainment BusinessMicrosoft Corporation

John LoSenior Vice President and CFOTencent Holdings Limited

Frank MergenthalerExecutive Vice President and CFOThe Interpublic Group of Companies

Patrick MilanoExecutive Vice President, CFO and Chief Accounting Offi cerMcGraw-Hill Education

It’s showtime! Digital drives the agenda, data delivers the insights

* Two CFOs asked to remain anonymous.

Shoichi NakamotoDirector, Senior Executive Vice President and CFODENTSU INC.

John P. NallenSenior Executive Vice President and CFO21st Century Fox America Inc.

Shankar NarayanCFOBennett Coleman & Co. Ltd

Maureen O’ConnellChief Accounting Offi cer, CFO and Executive Vice PresidentScholastic Inc.

Thomas C. PeddieExecutive Vice President and CFOCorus Entertainment Inc.

David PendletonChief Operating Offi cerAustralian Broadcasting Company

Nick PridayCFO, Dentsu Aegis Network & Aegis MediaDentsu Aegis Network Limited

Julie RaffeFinance DirectorVillage Roadshow Limited

Paul RichardsonGroup Finance DirectorWPP

Mitchell ScherzerSenior Vice President and CFOHearst Corporation

Peter SeymourExecutive Vice President and CFODisney ABC Television Group

Chris SheanSenior Vice President and CFOLiberty Media Corporation

Paul ShurgotSenior Vice President and CFOThe Walt Disney Studios

Bedi A. SinghCFONews Corporation

Dene StrattonCFOMetro-Goldwyn-Mayer Inc.

Ganapathy SubramaniamCFOHathway Cable and Datacom

N. SubramanianCFOEntertainment Network (India) Limited

Thomas SummerCFOAdvance Publications, Inc.

Nikolay SurikovCFOCTC Media, Inc.

Elena VermanCFOProf-Media Management

Larry WassermanCFODreamworks Studios

David WellsCFONetfl ix, Inc.

Kathy WillardExecutive Vice President and CFOLive Nation Entertainment, Inc.

Zhang Jazy YingCFOGiant Interactive Group, Inc.

Global Media & Entertainment Center

The methodologyWe met with each of the CFOs who participated in the study, asking them 12 questions focused on the industry as a whole, as well as on specific areas within each CFO’s organization, and asked the CFOs to rank their top three responses in order of importance. We have summarized their responses in this report, highlighting the key themes that emerged from our discussions.

If you would like to see the complete results of the study, please contact your local EY representative.

1It’s showtime! Digital drives the agenda, data delivers the insights

Contents

2 Overview

4 Digital isn’t the future — it’s already here

8 Data analytics deliver insights that improve decision-making

12 Transactions focus on what companies already know

16 Better tax planning accelerates performance

18 Capturing today’s talent will fuel tomorrow’s growth

20 Conclusion

2 Global Media & Entertainment Center

After six years of driving cost reductions and business efficiencies to first survive and then thrive amid economic uncertainty and disruptive markets, CFOs are changing gears. In our 2012 CEO report,1 62% of CEOs cited economic uncertainty as their top challenge. Of the 50 M&E CFOs we interviewed for our 2014 CFO study, only 26% highlighted economic uncertainty as a concern. This shift away from retract and retrench reflects the sentiment of CFOs across sectors.

Overview

“As M&E companies look to grow, CFOs are focusing on being strategic partners to the business, providing leadership and insight, and helping to ensure the business is moving fast enough to adapt to and innovate in today’s digital world.”

John NendickGlobal Media & Entertainment LeaderEY

Figure 5Economic uncertainty is no longer the greatest challenge

of CFOs identified economic uncertainty as a challenge for their organization

of CEOs identified economic uncertainty as a challenge for their organization

Instead, organizations around the world are turning their attention to growth. M&E CFOs are no exception. And they see digital and data analytics as the means to achieve it.

For organizations seeking to accelerate their growth trajectory, transactions are making a comeback. For companies that are looking to grow through acquisitions, a majority of CFOs say their organizations are focused on expanding the geographic footprint for existing businesses. Nearly half report a willingness to take a risk on new business ventures, such as games, social media and online entertainment.

Although growth is now the number one priority, CFOs are still seeking cost reductions and business efficiencies. And they see integrated tax planning as a ripe opportunity, particularly as organizations expand their geographic footprint into emerging markets.

Although cost reduction and business efficiencies have played a role for several years, as growth becomes the priority, CFOs are looking to digital and data analytics to shift them into high gear.

3It’s showtime! Digital drives the agenda, data delivers the insights

As CFOs look to the future, they perceive recruiting, developing and retaining the right talent as critical to their organization’s success. Investments in digital talent specifically are high priorities across M&E subsectors.

Digital transformation, data analytics to improve decision-making, transactions to accelerate growth, optimizing tax planning opportunities, and recruiting and retaining the right talent — these are the priorities CFOs identified when we interviewed them, and they are the themes we explore in this report.

Study highlightsDigital isn’t the future, it’s already hereDigital is transforming the M&E landscape. M&E companies’ best advantage is to manage from within the digital and technology disruptions that are transforming the market.

Data analytics deliver insights that improve decision-makingTo effectively align their organization for digital growth, CFOs are placing significant emphasis on data analytics to improve decision-making, systems and processes.

Transactions focus on what companies already knowAs M&E companies look to grow, CFOs are most focused on deals in core markets and geographies. But new opportunities are a tempting option.

Better tax planning accelerates performanceIntegrating tax planning that aligns to business and operational strategy is more important than ever for CFOs as tax planning moves into the digital age.

Capturing today’s talent will fuel tomorrow’s growthCFOs recognize the importance of attracting and retaining top talent, and they’re pinning their success, in part, on their ability to do it.

4 Global Media & Entertainment Center

Study participant says:“Online and digital distribution is not the future anymore — it’s already happening.”

Digital technology today pervades every aspect of our lives. It’s no wonder then that 74% of M&E CFOs see digital and online distribution as a top priority for their organization. Reading, television, film, games, music — it’s all online, available across multiple platforms and eminently consumable. The difference between today and years past is the intensity and the pace at which the digital landscape is changing. It seems that each day we wake up to a new device, platform or app that will transform how we think, work and live in the world.

EY’s digital media platform saturation index suggests a 17% compound annual growth rate (CAGR) between 2010 and 2017. In the same time frame, while worldwide device penetration is growing at 20% annually, data consumption is growing at 25%.

Average broadband penetration speed, which has doubled globally from 1.9 megabits per second (Mbps) to 3.8 Mbps between 2010 and 2013, is one factor. Consumers having more devices and doing more with them is another.

see the evolution of digital and online distribution as a priority for the organization

74%selected the evolution of digital and online distribution as their #1 priority

25%Figure 6The evolution of digital and online distribution

Study participants say:“Without digital, we cannot survive.”

“Media companies are still grappling with getting a digital monetization model in place.”

“M&E CFOs no longer see digital as a new media play. They see it as an essential and fundamental component of their organization in every dimension.”

Howard Bass Global Media & Entertainment Advisory Services LeaderEY

Digital isn’t the future —it’s already hereDigital is transforming the M&E landscape. M&E companies’ best advantage is to manage from within the digital and technology disruptions that are transforming the market.

5It’s showtime! Digital drives the agenda, data delivers the insights

Figure 7Rise in connected devices is outpaced by higher consumer levels2

Worldwide consumer internet-enabled device growth index

Worldwide consumer IP data traffic growth index

0

1

2

3

4

5

6

7

Index is based on the household penetration of fixed and wireless broadband connections and consumer internet-enabled devices.

Index = (broadband penetration + consumer device penetration) / 200%

Index is based on the growth rates for consumer internet-enabled devices and consumer internet data traffic.

50

100

150

200

250

300

350

400

450

500

2010 2011 2012 2013 2014e 2015e 2016e 2017e

2010

2.77

2011 2012 2013 2014e 2015e 2016e 2017e

3.53

4.22

4.825.33

5.726.01

6.63

1.291.61

1.992.30

2.733.11

3.48

3.96

Worldwide US

100127

162

206

255

313

384

468

100126

163189

230

268

304

356

Between 2010 and 2014, the average broadband speed globally doubled from 1.9 Mbps to 3.8 Mbps.

2010–2017e CAGRWorldwide: 17%US: 13%

2010–2017e CAGRIT traffic: 25%Devices: 20%

EY digital media platform saturation index EY worldwide digital media consumption growth index

In the US, between 2010 and 2013, consumers increased their use of social networking by 37% and online video by 94%. Over the same time period, traditional media continued to decline, with newspapers and magazines down 16% and 11%, respectively.

6 Global Media & Entertainment Center

The speed at which digital technology is evolving, combined with voracious consumer consumption rates, is fundamentally changing the business landscape for M&E companies. The telephone, a ground-breaking communications tool invented amid a wave of innovation during the industrial revolution, took 75 years to connect 50 million people globally. Imagine presenting a business case today that suggested a 75-year

time frame for reaching 50 million customers. The business case would never be approved. Four years ago, from the time it was introduced in 2010, it took Apple’s iPad less than two years to reach the same number of customers. Rovio Entertainment’s game Angry Birds reached 50 million customers in about 30 days.

Figure 8Disruptive technology is changing the M&E landscape3

10 200 30 40 50 60 70 80

Number of years to reach 50m global customers

75.0

38.0

13.0

6.5

4.0

3.6

3.0

3.0

2.9

2.8

2.5

2.3

1.8

0.2

0.1Angry Birds

Google+

iPad

Snapchat

AOL

iPhone

MySpace

iPod

www

Television

Radio

Telephone

It took about 75 years for the telephone to connect 50 million people. Today, technologies reach that milestone in around a month.

7It’s showtime! Digital drives the agenda, data delivers the insights

Study participant says:“It’s unknown where technology is going and how disruptive it will be, thus, the need for a flexible business model.”

of CFOs cite platform and technology disintermediation as the greatest challenge64%

58% of CFOs cite the inability to persuade consumers to pay “fair value” for content

Given that M&E organizations are unable to predict the direction or the speed of the next wave of digital innovation, their best advantage is to create flexibility across the organization to adapt and capitalize on the digital and technology disruptions that are transforming the market.

In addition to platform and technology disintermediation, 58% of M&E CFOs cite losing control of the customer relationship and persuading consumers to “pay fair value” for content as another significant challenge. Part of the issue is that fair value is in the eye of beholder. Looking through the lens of the consumer, fair value means something quite different from what content producers or creators see. As celebrities and other consumers continue to produce “free” content, M&E companies are having to prove that their content is worth its price.

Figure 9M&E’s greatest challenges

The ability to achieve mass scale in a matter of weeks or months instead of years represents an enormous and enticing opportunity for M&E companies. Yet it also means that a new slew of competitors can be just around the corner. It’s also important to note that mass scale in the short term does not guarantee long-term success. The speed at which a company’s star rises can also be the speed at which it falls. It is for these reasons that 64% of CFOs cite platform and technology disintermediation as their greatest challenge over the next three years.

“Fair value is tough to address because consumers and content producers have very different perspectives on what ‘fair value’ means.”

Jean-Benoit Berty UK Technology, Media & Telecommunications Market LeaderEY

8 Global Media & Entertainment Center

Data analytics deliver insights that improve decision-making

Study participant says:“We’re confident we can win when we understand and can predict the rules.”

Figure 10Top priorities for the finance team

60% of CFOs feel it is a top priority to improve their decision analytics capabilities

54% of CFOs feel it is a top priority to improve efficiency of systems and processes

To effectively align their organization for digital growth, CFOs are placing significant emphasis on data analytics to improve decision-making, systems and processes.

9It’s showtime! Digital drives the agenda, data delivers the insights

To enrich existing data strategies and drive insights into the business, CFOs are focusing on four components:

Simplify rear-view reporting. Companies are now using modern tools and data analytics techniques to simplify the collection, storing and analysis of data.

Develop predictive modeling techniques. Predictive modeling enables organizations to shift gears on data from collection and reporting to taking a forward-looking view of the issues and challenges that may impact the business in the future.

Democratize access to the data. By leveraging mobile and cloud-based technologies, organizations can provide easy access to the data to stakeholders at the time and place where it is relevant.

Consolidate customer, audience and platform data. Consolidation enables organizations to develop a single view of the customer. It also simplifies data outputs, enabling both standardization of data across the enterprise and customization to better target customers.

� Eliminate manual, Excel-based reporting

� Automate performance metrics collection and distribution

� Reduce complexity and volume of internal reporting

� Standardize content information across business units

� Identify vital key levers that drive the business ... sort through the big data “noise”

� Create models that predict performance and variance before they happen

� Enable data-driven, real-time decision-making

� Provide mobile-ready analytics solutions

� Develop visualization techniques that make it easy to consume information

� Enable stakeholders to develop their own custom insights from common standards

� Develop single view of customer

� Develop insights that enable better targeting and customization

� Simplify third-party tools and “own” more customer data

Consolidate customer, audience and platform data

Democratize access to the data

Develop predictive modelling capabilities

Simplify rear-viewreporting

Organizational agility

Utilizing data to drive insights into M&E businesses

Figure 11CFOs are focusing on four initiatives

“CFOs want the ability to efficiently analyze their data to gain insights into context, consumers and community, and to drive commerce and create incremental value ... ultimately elevating this conversation within their organizations.”

Ekta SinghUS Innovation & Digital Strategy LeaderEY

10 Global Media & Entertainment Center10 Global Media & Entertainment Center

A majority of CFOs (59%) believe their organization is doing a good or very good job of using data for responding and upselling to existing customers and identifying trends. Similarly, 52% of CFOs see their organization as doing a good job of using data to determine production rights and content investments as part of the creative process. And yet, only about a third (33%) of CFOs think that their company is doing a good job of using data to effectively generate new leads or find new customers.

In fact, CFOs acknowledge that real-time access to data is their greatest area for improvement. Just over half of the CFOs feel that they have the appropriate tools and processes in place to gather insights and information. Yet they are less confident about managing data in real time and sharing it effectively around the organization. Only 39% believe they can access management information and data in real time when needed. Similarly, only 39% believe their organization is good or very good at sharing data.

Study participants say:“It’s not clear yet which tools to use, what data is valuable and how to use the data. We haven’t yet cracked that code.”

“For our production and content choices, we use high levels of data plus CEO ‘gut feel.’ ”

Figure 12How well CFOs are using their data

do a good or very good job of using data for responding and upselling to existing customers and identifying trends

59%do a good job of using data to determine production rights and content investments as part of the creative process

52%do a good job of using data to effectively generate new leads or find new customers

33%

are good or very good at sharing data around their organization

39%have the appropriate tools and processes to gather insights and information

52%can access management information in real time

39%Figure 13How well CFOs are tracking, accessing and communicating their organization’s performance

11It’s showtime! Digital drives the agenda, data delivers the insights

As the global big data market for M&E continues to grow — 41.1% CAGR estimated between 2012 and 20184 — finding meaningful insights among the exabytes of data becomes increasingly difficult. For example, in 2010, approximately 1,100 exabytes of unstructured data were stored in databases. By 2015, we expect that number to rise to nearly 8,000 exabytes, 68% of which consumers will create primarily through social networks.

Study participant says:“We make this work through brute force. Investment in IT is needed to make it easier to make data- and insights-driven business decisions.”

Figure 14The exponential rise in data makes it harder to find meaningful insight5

To make sense of the data and take full advantage of the insights they gather, and to improve the effectiveness of the organization as a whole, collaboration is key. When asked, 58% of CFOs cited greater collaboration between business units and/or teams as a means of improving their organization’s overall effectiveness. Yet, only 30% intended to make it their top priority.

FacebookLinkedIn

TwitterInstagram

Google+Pinterest

90% of all data was unstructured

68% of all unstructured data in 2015 will be

created by consumers

Unstructured data (91%)

0

200

400

600

800

1,000

1,200

0

2,000

4,000

6,000

8,000

10,000

2008 2009 2010 2011 2012 20132010 2015e

Between 2012 and 2018, the global big data market for media and entertainment will grow 41.4% CAGR.

326 8

55 90 14526

150

500

202

277

555500

1,000

1 1080

150 150

350

608

845

1,060

1,150

7012

Average number of likes4.7b May 20132.7b August 2012

Tweets per day500m 20135k 2007

5,300 exabytes of unstructured digital consumer data to be stored in databases by 2015, out of which a large share to be generated by social networks

The rising availability of dataNumber of registered users (in millions)

Volume of digital data stored in databases(in exabytes*)

* One exabyte equals one million terabytes (TB)

1,104

123 2,531

5,379

758

Volume Structure

12 Global Media & Entertainment Center

Transactions focus on what companies already know

Study participant says:“We want to be in big creative markets.”

As if channeling the twin mantras of “bigger is better” and “if you can’t beat them, buy them,” transactions are making a comeback in M&E. Specifically, organizations are looking to grow in areas that they know. From both geographic and investment perspectives, M&E companies are focusing first on existing markets and businesses. Their second choice for growth is new markets and businesses.

Figure 15How CFOs expect their organizations to expand in the market

The focus on existing or core markets makes sense given that the US ranks as the most attractive region in EY’s Digital Media Attractiveness Index. It continues to represent both scale and maturity in all areas. China’s scale and growth in a still- emerging market make it attractive, but the regulatory and business environment makes it a less attractive investment for some M&E companies. Similarly, although Brazil, India and Russia offer vast potential, they too struggle with systemic risk and regulatory issues. Finally, even though Japan, the UK, France and Germany are safe core markets with relatively low costs of entry, their relatively modest size makes them less attractive for M&E companies looking to significantly scale their customer base.

Study participants say:“70% of our business is from core markets, but the other 30% will be driving our growth.”

“It’s much harder now to differentiate between ‘developed’ and ‘emerging’ markets.”

72% are focused on existing/core markets

67% seek “bolt-on” deals to expand geographically in existing businesses

64% are looking at opportunitiesin emerging markets

50% are looking to invest in new business

“In terms of M&E, in existing core markets, we expect the focus to be on size. In emerging markets, we expect the focus to be on volume. Either way, M&E is an industry on the move.”

Tom ConnollyGlobal Media & Entertainment Transaction Advisory Services LeaderEY

As M&E companies look to grow, CFOs are most focused on deals in core markets and geographies. But new opportunities are a tempting option.

13It’s showtime! Digital drives the agenda, data delivers the insights

United States

China

Japan

GermanyUK

FranceAustralia

South Korea

Mexico

South Africa

Saudi Arabia

India

Brazil

Russia

Indonesia

Argentina

1

43

2

Market costs

High

Low

High Low

Mar

ket b

enefi

ts

Size of bubble represents the total weighted score of benefits and costs and is an indicator of earnings potential

Figure 16EY Digital Media Attractiveness Index6

The index blends and weights over 20 indicators from media and entertainment to the wider market.

Benefits Macroeconomic and socio-demographic: economic growth and technology adoption

Market value and monetization: e-commerce and online payments

Costs Macro ease of doing business and risk factors (e.g., political and regulatory risk and piracy)

Media and entertainment environment: foreign ownership, licensing and censorship

Index highlights

The US continues to be the most attractive market, representing scale and maturity in all areas.

1 China’s scale and growth make it attractive, but the regulatory and business environment remains an issue.

2 Brazil, India and Russia offer vast potential but also struggle with wider risk and regulatory issues.

3 Japan, UK, France and Germany are core markets with relatively low costs of entry.

4

14 Global Media & Entertainment Center

For many M&E organizations, the preferred approach to acquisition is to have a majority ownership so that they can control their own destiny. They want to control their brand and the content or intellectual property. At the same time, they understand the value of local knowledge and local customer insights, making local partnerships and alliances their second most preferred choice for acquisitions and their primary rationale for any transaction. Yet for many CFOs there is an indication that their organization is willing to go it alone.

Figure 17CFOs prefer deals that give them more local knowledge and enable them to better control content, brand and destiny

Percentage of respondents(up to three responses provided)

0% 20% 40% 60%

61%Acquisitions/majority ownership

Local partnerships/alliances

Go it alone/greenfield

Investments/minority ownerships

Content sales/licensing/franchising

Local market knowledge/customer insight

Content/IP ownership

Brand control

Achieve competitiveadvantage

Access to talent

55%

48%

34%

30%

56%

44%

34%

29%

26%

Ranked #1 Ranked #2 Ranked #3

Percentage of respondents(up to three responses provided)

Ranked #1 Ranked #2 Ranked #3

0% 20% 40% 60%

Preferred approach Rationale

15It’s showtime! Digital drives the agenda, data delivers the insights

Study participant says:“We’re looking for young businesses ... it’s all about their potential for growth.”

Although the big deals seem to be occurring among cable operators, CFOs continue to believe, as CEOs did two years ago, that the big winners three years from now will be interactive media companies.

Figure 18Global media and entertainment M&A deals by sub-sectorNumber of announced deals with disclosed transaction values7

*Deals announced through 19 May 2014

2008 2009 2010 2011 20132012 1H’ 14*

100

0

200

300

400

500

600

700

800

900

1,000

574

397425

546493

567

188

$61

$194 $189

$153

$157 $220

$939

Average deal value (US$m)

Publishing and information services

Broadcasting and cable

Film and entertainment

Digital

“Given increases in their market value, some M&E companies are able to access capital markets and use their stock as currency to more aggressively pursue acquisitions in the future — which they need to do as both an offensive and defensive strategy. Companies need to expand to grow. If they don’t, they could become targets.”

Farokh BalsaraIndia Media & Entertainment Sector LeaderEY

Better tax planning accelerates performance

Study participant says:“Tax has a key role to play in creating value for shareholders.”

As M&E businesses seek to grow across geographies and evolve to address disruptive markets and technology, a more closely integrated tax planning strategy that aligns to the organization’s digital strategy becomes more important than ever.

Figure 19In what ways could your organization enhance its current tax strategy to take it to the next level?

For 40% of CFOs, integrating tax planning within the business and operations was their number one priority. They see it as a strategic opportunity to drive growth through increased operational efficiencies and improved processes. They also see it as a means of managing the risks of an increasingly cross-jurisdictional tax landscape. Integrating tax planning into the business enables M&E companies to gain a better understanding of where key management, supply chains and intellectual property are located internationally. This enables organizations to then centralize key parts of the business in tax-advantaged jurisdictions by securing rulings with tax authorities on an agreed legal structure and operating model.

Study participant says:“Tax is not only a burden; it can bring rewards and recognition.”

16 Global Media & Entertainment Center

Integration of tax planning within the businesses and operations

Optimizing tax planning to take advantage of international opportunities

Improved/more consistentlevels of compliance

Migration to global accounting and tax systems and software

Improved relationships with tax authorities, including in regions where

the organization is looking to grow

100 20 30 40 50 60 70

70%

65%

40%

33%

18%

Percentage of respondents(up to three responses provided)

Ranked #1 Ranked #2 Ranked #3

Integrating tax planning that aligns to business and operational strategy is more important than ever for CFOs as tax planning moves into the digital age.

17It’s showtime! Digital drives the agenda, data delivers the insights

Study participant says:“We need to do a better job of integrating tax planning into our contract negotiations.”

By improving relationships with tax authorities, organizations can reduce risks and unwanted exposure. They can also gain certainty and potential tax benefits or incentives that can improve these relationships.

CFOs looking for an integrated, long-term approach to tax planning may want to consider a multipronged strategic approach that uses the transition to digital to offset tax liabilities; positions senior stakeholders and head office in tax-efficient jurisdictions; provides detailed insight into the supply chain in terms of how customers, devices and platforms are changing; and understands the breadth, depth and value of the organization’s intellectual property.

“Ten years ago, CFOs’ focus around tax was on financial statement risk. Today, CFOs would add that integrating tax with their business strategies can create tremendous value for the organization.”

Alan LuchsGlobal Media & Entertainment Tax Services LeaderEY

18 Global Media & Entertainment Center

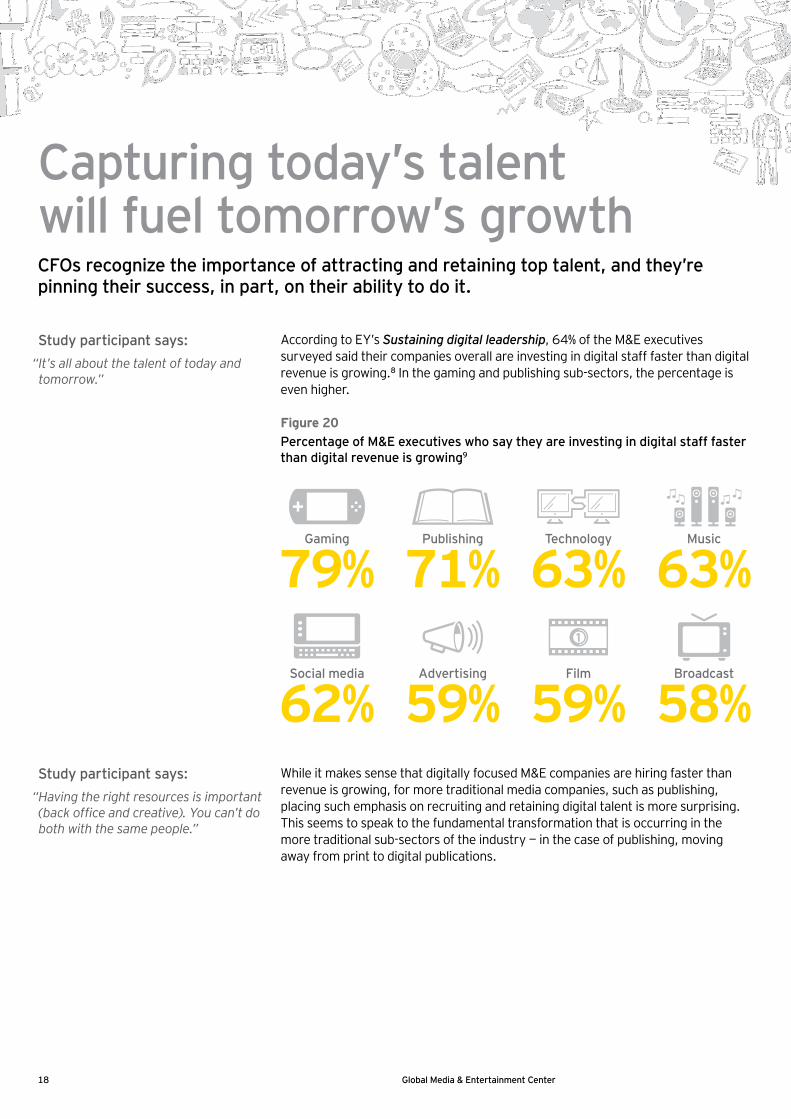

Capturing today’s talent will fuel tomorrow’s growth

Study participant says:“It’s all about the talent of today and tomorrow.”

According to EY’s Sustaining digital leadership, 64% of the M&E executives surveyed said their companies overall are investing in digital staff faster than digital revenue is growing.8 In the gaming and publishing sub-sectors, the percentage is even higher.

Figure 20Percentage of M&E executives who say they are investing in digital staff faster than digital revenue is growing9

While it makes sense that digitally focused M&E companies are hiring faster than revenue is growing, for more traditional media companies, such as publishing, placing such emphasis on recruiting and retaining digital talent is more surprising. This seems to speak to the fundamental transformation that is occurring in the more traditional sub-sectors of the industry — in the case of publishing, moving away from print to digital publications.

Study participant says:“Having the right resources is important (back office and creative). You can’t do both with the same people.”

79%Gaming

71%Publishing

63%Technology

63%Music

62%Social media

59%Advertising

59%Film

58%Broadcast

CFOs recognize the importance of attracting and retaining top talent, and they’re pinning their success, in part, on their ability to do it.

19It’s showtime! Digital drives the agenda, data delivers the insights

Figure 21Recruiting, attracting and retaining talent

Although creative skills differ from finance skills, CFOs echoed the importance of talent, with 58% indicating that their organization’s ability to attract and retain top talent will enable them to improve their organization’s effectiveness; 47% say recruiting and retaining the right talent will be a determining factor in the success of their performance three years from now. For CFOs, the right talent means finding people that have more than technical accounting skills. Today’s finance resources must also possess excellent communication skills and commercial and entrepreneurial acumen.

Study participant says:“My personal priority is talent. The talent I am seeing doesn’t align with needs and expectations ... hard to find people with the right digital skills to help us transform.”

Yet, for all the desires CFOs have to recruit, train and retain talent, many are finding it difficult to identify the right resources to fill their digital talent gaps. Many of the people they are interviewing do not have the right skills to fit the needs of the organization. As one CFO put it, “I can’t find the blend of skills, experience and background that I think we need to transform.”

say recruiting and retaining the right talent will be a determining factor in the success of their performance three years from now47%

say attracting and retaining talent would make their organization more effective58%

say capturing talent, skills and expertise makes a M&A deal more attractive43% “That traditional businesses

such as publishing are investing almost as much in digital staffing as gaming companies underscores the huge transformation that M&E companies are experiencing across sub-sectors.”

Ian EddlestonGlobal Media & Entertainment Assurance Services LeaderEY

20 Global Media & Entertainment Center

Conclusion

Study participant says:“Anything that is a commodity should be outsourced. Strategy should never be.”

Digital transformation, data analytics that turn insights into action, M&A activity in core and emerging markets, tax planning that optimizes operational efficiencies, and recruiting, training and retaining the right talent are the areas M&E CFOs identified as being important to their organization.

When we asked CFOs how they would measure their own success three years from now, their responses revealed that CFOs are no longer content to focus their personal performance on financial management and hindsight reporting. For 57% of CFOs, meeting or exceeding the company’s financial performance is still important. However, 65% of CFOs were more interested in looking forward. They want to use their role to enable their organization to develop a more competitive and successful business strategy. “Most of the time, I try to look to the future, design new strategies and ways to grow and deliver what consumers demand,” remarked one CFO. Another stated; “You need to have a deep understanding of the market trends — this should drive your strategy.” CFOs see participating in the development of a competitive business strategy and aligning the organization to that strategy as fundamental to their role.

As digital continues to drive the agenda, CFOs are looking forward — strategizing, planning and executing in ways that enable their organizations to grow and sustain market leadership.

“CFOs are still managing a changing business landscape, regulatory compliance and tax strategies and maximizing shareholder value. At the same time, their focus is shifting more and more toward driving better data, better analytics and better reporting.”

Jennifer WalshNortheast Media & Entertainment Market Segment LeaderEY

21It’s showtime! Digital drives the agenda, data delivers the insights

Study participant says:“My personal priority is to enable my organization to develop a more competitve and successful business strategy.”

To achieve their performance goals three years from now, CFOs plan to:

Manage the transition to digital by helping to shape digital business and revenue models with the flexibility to withstand a constantly changing digital landscape

Evolve analytics and reporting capabilities to enable real-time insights that improve strategic decision-making

Support transaction opportunities into new markets or geographies

Maximize tax planning opportunities that support growth initiatives

Attract, develop and retain top digital talent with the right skills and experience to position their organization for success now and in the future

It’s showtime for CFOs. As digital continues to drive the agenda, their role as strategic advisors, data wranglers, tax planners and talent purveyors will enable them to deliver the insights their organizations need to grow and sustain market leadership in a constantly and rapidly evolving digital M&E landscape.

“As CFOs look to the future, they see the critical role analytics has to play — that by moving toward data visualization and real-time data, they become more valuable partners to the business. Delivering real insights in real time results in more responsive decision making. The new insights digitization can bring will fundamentally change the way CFOs drive the business.”

David McGregorAsia-Pacific Technology, Media & Telecommunications Market LeaderEY

22 Global Media & Entertainment Center

Endnotes

1 EY’s 2012 CEO Study: Opportunity and optimism: how CEOs are embracing digital growth.

2 “Pivot Table: Worldwide Consumer Market Model, 2010–2017, Version 2,” IDC, February 2014, Doc #246993; “Global Multichannel Comparison Table,” SNL Kagan, April 2014, © 2014 SNL Kagan, a division of SNL Financial LC, estimates; All rights reserved; “State of the Internet Q4 2010” Akamai Technologies, Inc., 2011; “State of the Internet Q4 2013,” Akamai Technologies, Inc., 2014; “Cisco Visual Networking Index: Forecast and Methodology, 2010–2015,” Cisco Systems, Inc., 1 June 2011; “Cisco Visual Networking Index: Forecast and Methodology, 2011–2016,” Cisco Systems, Inc., 30 May 2012; “Cisco Visual Networking Index: Forecast and Methodology, 2012–2017,” Cisco Systems, Inc., 29 May 2013.

3 “Bicentennial Edition: Historical Statistics of the United States, Colonial Times to 1970,” US Census Bureau website, census.gov/prod/www/statistical_abstract.html, accessed 13 May 2014; “General Telephone Statistics: 1948,” International Telecommunication Union website, itu.int/en/history/Pages/HistoricalStatistics.aspx, accessed 13 May 2014; “Challenges to the network: Internet for development,” International Telecommunication Union website, itu.int/ITU-D/ict/publications/inet/1999/chal_exsum.pdf, accessed 13 May 2014; “Reaching 50 Million Users,” Visual.ly website, visual.ly/reaching-50-million-users, accessed 20 May 2014; “Google Plus vs Facebook Infographics,” Visual.ly website, visual.ly/google-plus-vs-facebook-infographics, accessed 20 May 2014; “iPad Races Towards 50 Million,” 9Clouds website, 9clouds.com/2010/05/13/ipad-races-towards-50-million-users-chart/, accessed 20 May 2014; “Google+ Hits the 50 Million Users Mark in Record Time,” Dazeinfo website, dazeinfo.com/2011/09/27/google-hits-the-50-million-users-mark-in-record-time/, accessed 20 May 2014; “What are iPad’s Sales All Time,” About.com website, ipod.about.com/od/ipadmodelsandterms/f/ipad-sales-to-date.htm, accessed 20 May 2014; “The Inside Story of Snapchat: The World’s Hottest App or A $3 Billion Disappearing Act?,” Forbes website, forbes.com/sites/jjcolao/2014/01/06/the-inside-story-of-snapchat-the-worlds-hottest-app-or-a-3-billion-disappearing-act/, accessed 20 May 2014.

23It’s showtime! Digital drives the agenda, data delivers the insights

4 “The Growth of Social Media,” Search Engine Journal website, searchenginejournal.com/growth-social-media-2-0-infographic/77055/, accessed 20 May 2014; “LinkedIn Corp: CQ2: Impressive Results, Downgrading on Valuation,” Morgan Stanley, 5 August 2011, via ThomsonOne; “LinkedIn Corp: Awaiting an Infl ection,” Morgan Stanley, 28 April 2014, via ThomsonOne; “Social Media’s New Big Data Frontiers,” Business Insider website, businessinsider.com.au/social-medias-new-big-data-frontiers-artifi cial-intelligence-deep-learning-and-predictive-marketing-2014-2, accessed 20 May 2014; “Big Data Market to Reach $48.3B by 2018,” Enterprise Apps Today website, enterpriseappstoday.com/data-management/big-data-market-to-reach-48.3b-by-2018.html, accessed 20 May 2014.

5 Ibid.

6 EY analysis of data from Ovum, eMarketer, IHS Insight, MAGNA GLOBAL, Oxford Economics, Excipio, The World Bank, OECD, IFPI and WAN-I.

7 EY analysis of Capital IQ data.

8 EY, Sustaining digital leadership, (pg. 9), 2014.

9 Sustaining digital leadership!, EYGM Limited, 2014.

www.ey.com/mediaentertainment

Mobile app: eyinsights.comFollow us on Twitter

EY Global Media & Entertainment on Twitter, @EY_MandE

Connect with us

Global Media & Entertainment Center24

Telephone Email

Global Media & Entertainment sector leaderJohn Nendick, Global M&E Leader (Los Angeles, US) +1 213 977 3188 [email protected]

Media & Entertainment service line leadersHoward Bass, Global M&E Advisory Services Leader (New York, US) +1 212 773 4841 [email protected]

Thomas J. Connolly, Global M&E Transaction Advisory Services Leader (New York, US) +1 212 773 7146 [email protected]

Ian Eddleston, Global M&E Assurance Services Leader(Los Angeles, US) +1 213 977 3304 [email protected]

Alan Luchs, Global M&E Tax Services Leader (New York, US) +1 212 773 4380 [email protected]

Media & Entertainment regional contactsFarokh Balsara (Mumbai, India) +91 22 6192 0280 [email protected]

Jean-Benoit Berty (London, England) +44 20 7951 0256 [email protected]

Mark Besca (New York, US) +1 212 773 3423 [email protected]

Mark J. Borao, (Los Angeles, US) +1 213 977 3633 [email protected]

Peter YF Chan (Hong Kong, China) +852 2846 9936 [email protected]

Peter Lennartz (Munich, Germany) +49 30 25471 20631 [email protected]

David McGregor (Melbourne, Australia) +61 3 9288 8491 [email protected]

Yuichiro Munakata (Tokyo, Japan) +81 3 3503 1100 [email protected]

Bruno Perrin (Paris, France) +33 1 46 93 65 43 [email protected]

Michael Rudberg (London, England) +44 20 7951 2370 [email protected]

Ekta Singh (New York, US) +1 212 773 8432 [email protected]

Jennifer Walsh (New York, US) +1 212 773 7168 [email protected]

Global Media & Entertainment center teamKatie Ackerman, M&E Advisory Services Resident (New York, US) +1 212 773 2571 [email protected]

Sylvia Ahi Vosloo, M&E Marketing Leader (Los Angeles, US) +1 213 977 4371 [email protected]

Karen Angel, M&E Implementation Director (Los Angeles, US) +1 213 977 5809 [email protected]

Matt Askins, National Accounting M&E Resident (New York, US) +1 212 773 0681 [email protected]

Ray Cheng, M&E Tax Resident (New York, US) +1 212 773 4412 [email protected]

Raghav Mani, M&E Knowledge Leader (Los Angeles, US) +1 213 977 5855 [email protected]

Martyn Whistler, M&E Lead Analyst (London, England) +44 20 7980 0654 [email protected]

EY Global Media & Entertainment key contacts

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

How EY’s Global Media & Entertainment Center can help your business In an industry synonymous with creativity and innovation, the bar for business excellence is set high. You need to embrace new technology, develop new distribution models and satisfy the demands of a voracious and outspoken consumer. At the same time it’s important to manage costs, exceed stakeholder expectations and comply with new regulations. There’s always another challenge just around the corner. EY’s Global Media & Entertainment Center can help. We bring together a high-performance, worldwide team of media and entertainment professionals with deep technical experience in providing assurance, tax, transaction and advisory services to the industry’s leaders. Our network of professionals collaborate and share knowledge around the world, to provide exceptional client service and leverage our leading market share position to provide you with actionable information, quickly and reliably.

© 2014 EYGM Limited.All Rights Reserved.

EYG no. EA0083 (revised)WR #1404-1231022 West

ED 0114

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice. The views of third parties set out in this publication are not necessarily the views of the global EY organization or its member firms. Moreover, they should be seen in the context of the time they were made.

ey.com