revenue statistics in latin america and the...

TRANSCRIPT

Revenue Statistics in Latin America and the Caribbean 1990-2014

XXVIII ECLAC Regional Seminar on Fiscal Policy Santiago, Chile – March 16-17, 2016

Revenue Statistics in Latin America and the Caribbean

1990 - 2014

Revenue Statistics in Latin America and the Caribbean

• Detailed, internationally comparable data on tax revenues in Latin

American and Caribbean (LAC) economies • 22 LAC economies from 1990-2014 • Comparisons with the average for OECD economies (and on-line data

for 32 non-LAC countries)

• Based on OECD Revenue Statistics methodology, an essential reference source for OECD member countries

• Joint project with the Economic Commission for Latin America and the Caribbean (ECLAC) , the Inter-American Centre for Tax Administrations (CIAT), and Inter-American Development Bank (IDB)

Revenue Statistics in Latin America and the Caribbean

I. Tax revenue trends 1990-2014

II. Tax structure

III. Fiscal revenues from non-renewable natural resources

IV. Future steps and conclusions

Tax revenues in LAC increased slightly in 2014, but continue

to be considerably lower than in most OECD countries

Total tax revenues in LAC and OECD, 1990-2014 (Percentage of GDP)

0

5

10

15

20

25

30

35

40

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Difference (A-B) LAC (22) (A) OECD (34) (B)

Wide national variations exist across LAC countries

(‘Americas Latinas’)

0 10 20 30 40

OECD (34)LAC (22)³

GuatemalaDominican Republic

El SalvadorParaguay²BahamasPanama

Venezuela²Peru

EcuadorMexico²

HondurasChile

ColombiaNicaragua

Costa RicaJamaica²Uruguay

Trinidad and TobagoBolivia²

Barbados²Argentina

Brazil

Total tax revenues in LAC countries and OECD, 2014 (Percentage of GDP)

Tax revenues rose significantly across the region over the

1990-2014 period

Tax to GDP ratios in LAC in 1990 and 2014

ARG

BHS

BRB

BOL

BRA

CHL COL

CRI

DOM

ECU

SLV

GTM

HND

JAM3

MEX NIC2

PAN PRY

PER

TTO URY

VEN2

5

10

15

20

25

30

35

40

5 10 15 20 25 30 35 40

2014

1990

Nevertheless, tax revenues barely increased between 2013

and 2014

Tax to GDP ratios in LAC in 2013 and 2014

ARG

BHS

BRB BOL

BRA

CHL COL

CRI

DOM

ECU

SLV

GTM

HND

JAM

MEX NIC PAN

PRY

PER

TTO URY

VEN

5

10

15

20

25

30

35

40

5 10 15 20 25 30 35 40

2013

2014

Tax revenues increase over GDP in 2014 was driven by

income taxes, and taxes on goods and services

-0.04 -0.02 0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16

Property

Other income tax

Others

Payroll

Social security

Corporate income tax

Goods and services

Personal income tax

Tax revenues growth in LAC, 2014 (Percentage points of GDP)

Revenue Statistics in Latin America and the Caribbean

I. Tax revenue trends 1990-2014

II. Tax structure: tax sources and administration

III. Fiscal revenues from non-renewable natural resources

IV. Future steps and conclusions

Tax collection in LAC is based on high indirect tax receipts

(general taxes), while direct taxation (i.e. personal) is low

Tax sources in LAC and OECD, 2013 (Tax collection as percentage of total tax revenues)

27.4

16.6

31.2

18.3

6.5

LAC (22)1

33.7

26.1

20.2

10.5

9.5

OECD (34)2

Taxes on income and profits Social-security contributions General consumption taxes

Specific consumption taxes Other taxes

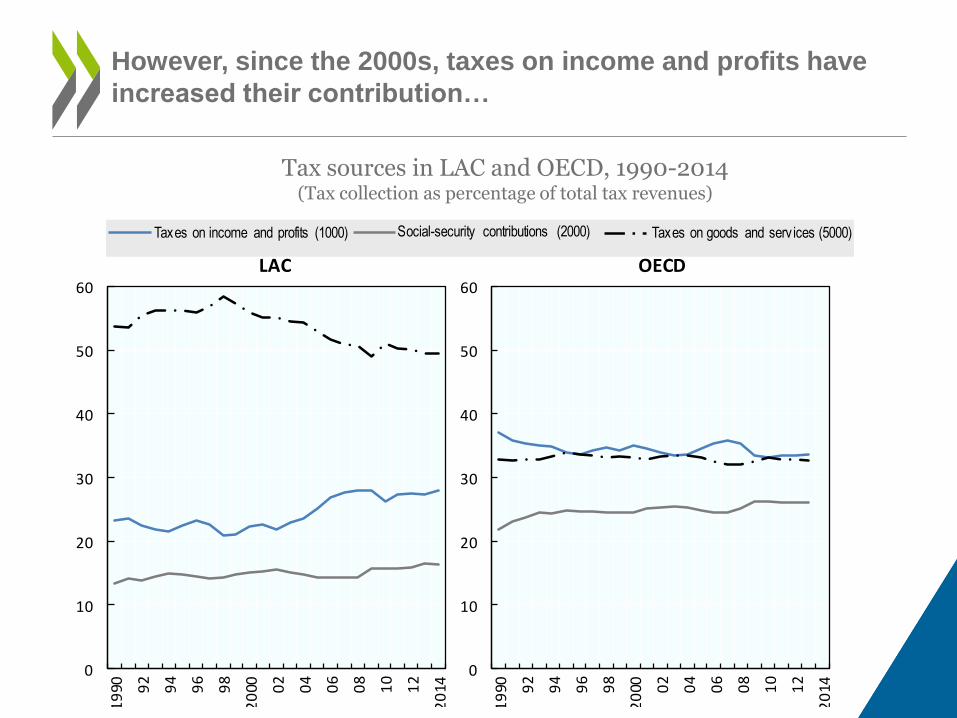

However, since the 2000s, taxes on income and profits have

increased their contribution…

0

10

20

30

40

50

60

19

90 92

94

96

98

20

00 02

04

06

08

10

12

20

14

LAC

0

10

20

30

40

50

60

19

90 92

94

96

98

20

00 02

04

06

08

10

12

20

14

OECD

Taxes on income and profits (1000) Social-security contributions (2000) Taxes on goods and serv ices (5000)

Tax sources in LAC and OECD, 1990-2014 (Tax collection as percentage of total tax revenues)

… notably thanks to the corporate income tax, but also to

personal income taxes

0

2

4

6

8

10

12

19

90 92

94

96

98

20

00 02

04

06

08

10

12

20

14

LAC

0

2

4

6

8

10

12

19

90 92

94

96

98

20

00 02

04

06

08

10

12

20

14

OECD

Personal income tax Corporate income tax Other income taxSocial-security contributions Taxes on goods and services

Tax sources in LAC and OECD, 1990-2014 (Percentage of GDP)

Again, tax structures reflects a wide variation across the LAC

region

Tax sources in LAC countries, 2014 (Tax collection as percentage of total tax revenues)

0 20 40 60 80 100

OECD (32)²LAC (22)³

BahamasBolivia¹

Paraguay¹Costa RicaArgentina

BrazilUruguayEcuadorPanama

Barbados¹HondurasNicaragua

Mexico²GuatemalaDominican…

ColombiaVenezuela¹

ChileJamaica¹

El SalvadorPeru

Trinidad…

Income and profits Property Social security contributions Payroll Goods and services Other

In the Americas Latinas, value added taxes raised more

revenues than income taxes in most countries…

VAT vs Income taxes in LAC countries and OECD, 2014 (Percentage of GDP)

0

5

10

15

20

25

VAT Taxes on income and profits

… mostly explained by weak personal income tax collection

Personal and Corporate income tax revenues in ALC countries and OECD, 2014 (Percentage of GDP)

Note: For OECD, the data for 2013 are used. The share of taxes on income and the share of taxes on profits may not add up to the total share of taxes on incomes and profits due to unallocable revenue. Only countries that could allocate 75% or more of revenue of taxes on incomes and profits into the sub categories taxes on income and taxes on profits are shown in the figure above.

0

2

4

6

8

10

12

14

16

18

TTO PER COL CHL BOL HND BRA ARG SLV GTM DOM BRB URY CRI JAM OECD

Personal income tax Corporate income tax

Sub-national government finances are also limited in LAC…

Tax revenues by sub-sectors of general government in LAC and OECD, 2013 (Receipts as percentage of total tax revenue)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

LAC

OECD

Central government State or local Social-Security Funds Supranational

…with the exceptions of Argentina, Brazil and Colombia

Tax revenues by sub-sectors of general government in LAC countries, 2014 (Receipts as percentage of total tax revenue)

0 10 20 30 40 50 60 70 80 90 100

VenezuelaUruguay

Trinidad and TobagoPeru

ParaguayPanama

NicaraguaMexico

JamaicaHonduras

GuatemalaEl Salvador

EcuadorDominican Republic

Costa RicaColombia

ChileBrazil

BoliviaBarbadosBahamasArgentina

LAC

Central governmentGobierno central

State or local Social-Security FundsFondos de seguridad social

Revenue Statistics in Latin America and the Caribbean

I. Tax revenue trends 1990-2014

II. Tax structure

III. Fiscal revenues from non-renewable natural resources

IV. Future steps and conclusions

Fiscal revenues from non-renewable natural resources are

key in half of the countries in LAC

Non-renewable natural resources revenues in LAC countries, 2014 (USD billion and percentage of GDP)

0 20 40 60 80 100

Jamaica

Suriname

Dominican Republic

Trinidad and Tobago

Bolivia (Plur. State of)

Peru

Chile

Argentina

Ecuador

Colombia

Brazil

Venezuela (Bol. Rep. of)

Mexico

As % of GDP

PEMEX

8.9

12.3

0.5

5.8

0.04

4.2

1.7

10.8

1.9

1.8

2.3

13.8

7.3

The reliance on non-renewable natural resources explains

the fall in total revenues in these countries in 2014…

2013 (r) 2014 (p) Δ 2013 (r) 2014 (p) Δ 2013 (r) 2014 (p) Δ

Argentina 1.8 1.9 0.1 1.7 1.8 0.1 0.1 0.1 0.0

Bolivia (Plur. State of) 14.2 13.8 -0.4 13.5 13.1 -0.4 0.7 0.7 0.0

Brazil 2.2 1.7 -0.5 1.8 1.6 -0.2 0.4 0.1 -0.3

Chile 2.1 1.8 -0.3 .. .. .. 2.1 1.8 -0.3

Colombia 5.1 4.2 -1.0 4.8 3.9 -0.9 0.4 0.3 -0.1

Dominican Republic 0.6 0.5 -0.1 .. .. .. 0.6 0.5 -0.1

Ecuador 12.1 10.8 -1.3 12.1 10.8 -1.3 .. .. ..

Jamaica 0.1 0.0 -0.1 .. .. .. 0.1 0.0 -0.1

Mexico 8.0 7.3 -0.8 7.8 7.0 -0.8 0.2 0.2 0.0

Peru 2.8 2.3 -0.5 1.9 1.6 -0.3 0.9 0.7 -0.3

Suriname 6.2 5.8 -0.4 5.5 5.0 -0.6 0.6 0.9 0.2

Trinidad and Tobago 11.7 12.3 0.5 11.7 12.3 0.5 .. .. ..

Venezuela (Bol. Rep. of) 12.2 8.9 -3.3 12.2 8.9 -3.3 .. .. ..

Latin America and the

Caribbean 6.1 5.5 -0.6 7.3 6.6 -0.7 0.6 0.5 -0.1

Country

Total Hydrocarbons1Mining

Public revenues from non-renewable natural resources in LAC countries, 2013-2014 (Percentage of GDP)

… and more falls are to come in 2015

Non-renewable natural resource revenues in LAC countries, 2000-2015(e) (Percentage of GDP)

Notes: Mining covers Argentina, Bolivia, Brazil, Chile, Colombia, Dominican Republic, Jamaica, Mexico, Peru and Suriname. Hydrocarbons include Argentina, Bolivia , Brazil, Colombia, Ecuador, Mexico, Peru, Suriname, Trinidad and Tobago and Venezuela

Looking forward, commodity prices are not expected to return to

pre-2014 levels soon

Commodity prices (Observed and forecasts ; index 100 = 2005)

0

50

100

150

200

250

2011 2012 2013 2014 2015 2016 2017

Minerals and metals Crude oil

Source: ECLAC, based on data from IMF

Revenue Statistics in Latin America and the Caribbean

I. Tax revenue trends 1990-2014

II. Tax structure

III. Fiscal revenues from non-renewable natural resources

IV. Future steps and conclusions

• Improve direct tax data

• Deepen the analysis on regional governments

• Broaden the analysis on commodity revenues (i.e. food)

• Continue expanding country coverage

• …

Future steps

Future steps (I): Within taxes on income and profits, there

is still room for improvement in data allocation

32%

61%

23%

LAC

76%

25%

2%

OECD

Personal income tax Corporate income tax Unallocable income tax

Future steps (II): Data and analysis by sub-sectors of

government merits (more) attention

Tax revenues by sub-sectors of general government in LAC countries, 2014 (Receipts as percentage of total tax revenue)

0 10 20 30 40 50 60 70 80 90 100

VenezuelaUruguay

Trinidad and TobagoPeru

ParaguayPanama

NicaraguaMexico

JamaicaHonduras

GuatemalaEl Salvador

EcuadorDominican Republic

Costa RicaColombia

ChileBrazil

BoliviaBarbadosBahamasArgentina

LAC

Central governmentGobierno central

State or local Social-Security FundsFondos de seguridad social

Future steps (III): Public revenues from food commodities

are a relevant part of the tax story in the LAC region

Source: Alberola, I. Kataryniuk, A. Melguizo and R. Orozco (2015), “Fiscal policy and the cycle in Latin America: the role of financial conditions and fiscal rules” , BIS Working Paper 543

Fiscal balance in Argentina, 2000-2013 (Percentage of GDP)

-4.00%

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013.0 2014

Commodity linked Argentina Primary balance Structural Primary balance

Future steps (and IV): Continue expanding country coverage

• Antigua and Barbuda • Belize • Cuba • Dominica • Grenada • Guyana • Haiti • St. Kitts and Nevis • St. Lucia • St. Vincent and the Grenadines • Suriname • …

Conclusions (I): Beyond Americas Latinas, tax revenue

trends confirm LAC-OECD convergence has stalled

• The average tax burden in LAC increased from 21.5% in 2013 to 21.7% GDP in 2014. This followed a rise of 1.5 percentage since 2010, reversing the decline during the financial crisis

• The average tax burden in LAC countries is still far behind from the OECD average (34.4% of GDP in 2013). The gap has remained steady at 13 percentage points since 2008

• There is a wide variation across countries. The tax to GDP ratios in LAC countries range from 12.6% (Guatemala), 14.1% (Dominican Republic) and 16.5% ( El Salvador) to 30.4% (Barbados), 32.2% (Argentina) and 33.4% (Brazil)

Conclusions (II): Tax structures in LAC countries are

centralised, and heavily based on indirect taxes

• Following strong growth over the past decades, general consumption taxes (mainly VAT and sales taxes) account for nearly one third of tax revenues in the LAC countries in 2013 (31.2%), compared with one fifth (20.2%) in OECD

• Contributions from direct taxes are significantly lower in LAC countries. Taxes on income and profits accounted for 27.4% of revenues on average in the LAC countries and social security contributions represented 16.6% (in OECD the corresponding figures are 33.7% and 26.1% respectively)

Conclusions (III): Public revenues are decreasing in some

commodity-rich countries in LAC

• The sharp decline in international oil prices resulted in a significant reduction of hydrocarbon-related revenues in the region (from 7.3% of GDP in 2013 to 6.6% of GDP in 2014). Non-tax revenues bore the brunt of the decline, falling sharply in Ecuador and Venezuela

• In 2015, hydrocarbon revenues are estimated to have returned to their pre-boom level, falling from an average of 6.6% of GDP in 2014 to 4.5% of GDP

• Mining revenues were also affected by falling prices, dropping to 0.5% of GDP on average from 0.6% of GDP in 2013. Tax revenues, derived mainly from corporate income taxes, fell sharply as profit margins in the sector tightened. The rise in production coupled with currency depreciations served to smooth the shock

• Given the persistent economic slowdown and the weak price projections for most commodities, a no-policy change scenario suggests that the gap in tax revenues between LAC countries and the OECD will persist

• Some countries in the region are implementing/defining/debating structural fiscal reforms that increase revenues. Sufficiency, efficiency, equity and simplicity principles should drive these process, accompanied by institutional improvements (e,g, fiscal frameworks, rules, councils)

• For non-renewable natural resources, institutions to ensure commodity booms traslate into sustainable economic development should be implemented (e.g. stabilisation funds)

Conclusions (and IV): Policy action is needed

Abiertos a escuchar más ideas - Gracias!

www.latameconomy.org/es/revenue-statistics/