second quarter 2010 earnings release - snl

TRANSCRIPT

Second Quarter 2010 Earnings Release

August 6, 2010

2

Forward-Looking Statements

Under the Private Securities Litigation Act of 1995This document may contain or incorporate by reference forward-looking statements as defined under the federal securities laws regarding DCP Midstream Partners, LP (the “Partnership”), including projections, estimates, forecasts, plans and objectives. Although management believes that expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to be correct. In addition, these statements are subject to certain risks, uncertainties and other assumptions that are difficult to predict and may be beyond our control. If one or more of these risks or uncertainties materialize, or if underlying assumptions prove incorrect, the Partnership’s actual results may vary materially from what management anticipated, estimated, projected or expected.

The key risk factors that may have a direct bearing on the Partnership’s results of operations and financial condition are highlighted in the earnings release to which this presentation relates and are described in detail in the Partnership’s periodic reports most recently filed with the Securities and Exchange Commission, including its most recent Form 10-K. Investors are encouraged to consider closely the disclosures and risk factors contained in the Partnership’s annual and quarterly reports filed from time to time with the Securities and Exchange Commission. The Partnership undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Information contained in this document is unaudited, and is subject to change.

Regulation GThis document may include certain non-GAAP financial measures as defined under SEC Regulation G, such as distributable cash flow, adjusted EBITDA and adjusted segment EBITDA. In such an event, a reconciliation of those measures to the most directly comparable GAAP measures is included in supplementary material to this presentation on our website at www.dcppartners.com.

3

Today’s Agenda

� Q2 and YTD highlights

� Operational update

� Financial overview and forecast

� Outlook and summary

4

Q2 and YTD Highlights

� Financial results in line with 2010 DCF forecast� Distributable cash flow of $24.9 million in Q2 and $56.6 million YTD

� Distribution coverage ratio of 1.14x YTD

� Delivered on 2010 objective of resuming distribution growth� Declared 1.7% increase in quarterly distribution ($0.61 per unit)

� Executing on growth opportunities which are substantially fee-based� Wholesale propane terminal acquisition expands business into Mid-Atlantic

� Acquisition of additional 55% interest in Black Lake NGL pipeline

� In conjunction with GP, signed letter of intent to create natural gas processing and related NGL infrastructure JV to serve EQT and third party producers in Marcellus and Huron shale areas

� Michigan and Wattenberg acquisition integration efforts on plan

� Continued execution on financial positioning objectives

Delivering on 2010 business plan commitments

5

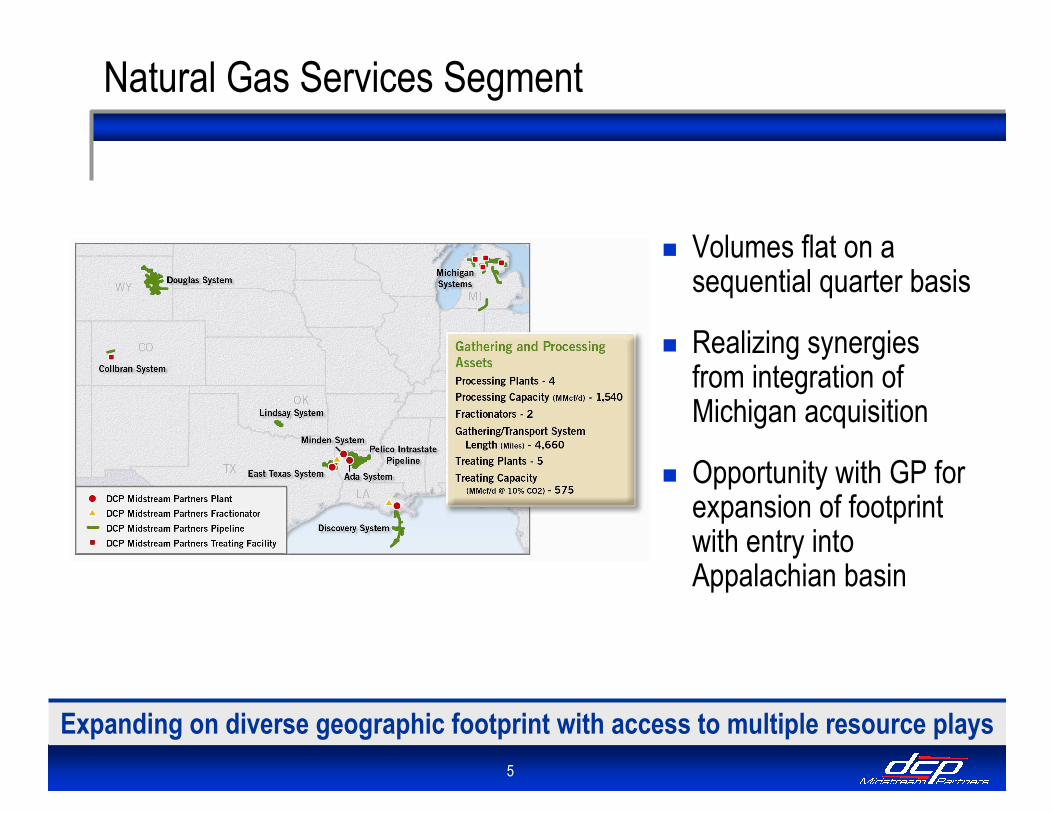

� Volumes flat on a sequential quarter basis

� Realizing synergies from integration of Michigan acquisition

� Opportunity with GP for expansion of footprint with entry into Appalachian basin

Natural Gas Services Segment

Expanding on diverse geographic footprint with access to multiple resource plays

6

NGL Joint Venture in Appalachian Basin

170 MMcf/d Langley Plant

NGL Pipeline

� Expands gas processing and NGL marketing presence into prolific Marcellus shale play

� EQT has industry leading E&P position in the Appalachian basin

� Facilitates additional investment opportunities to meet rapidly growing needs of EQT and other producers

Strategic entry point for emerging shale play

� Signed letter of intent to create natural gas processing and related NGL infrastructure JV to serve EQT and third party producers in the Marcellus and Huron shale areas of Appalachian basin

7

� Sales volumes reflect planned outage related to Providence terminal inspection and warmer weather

� Providence supply contract amendment

� Successful contracting season for winter 2010/2011

� Acquisition expands business into Mid-Atlantic region

Wholesale Propane Logistics Segment

Strengthening supply and logistics capabilities enhance competitive positioning

8

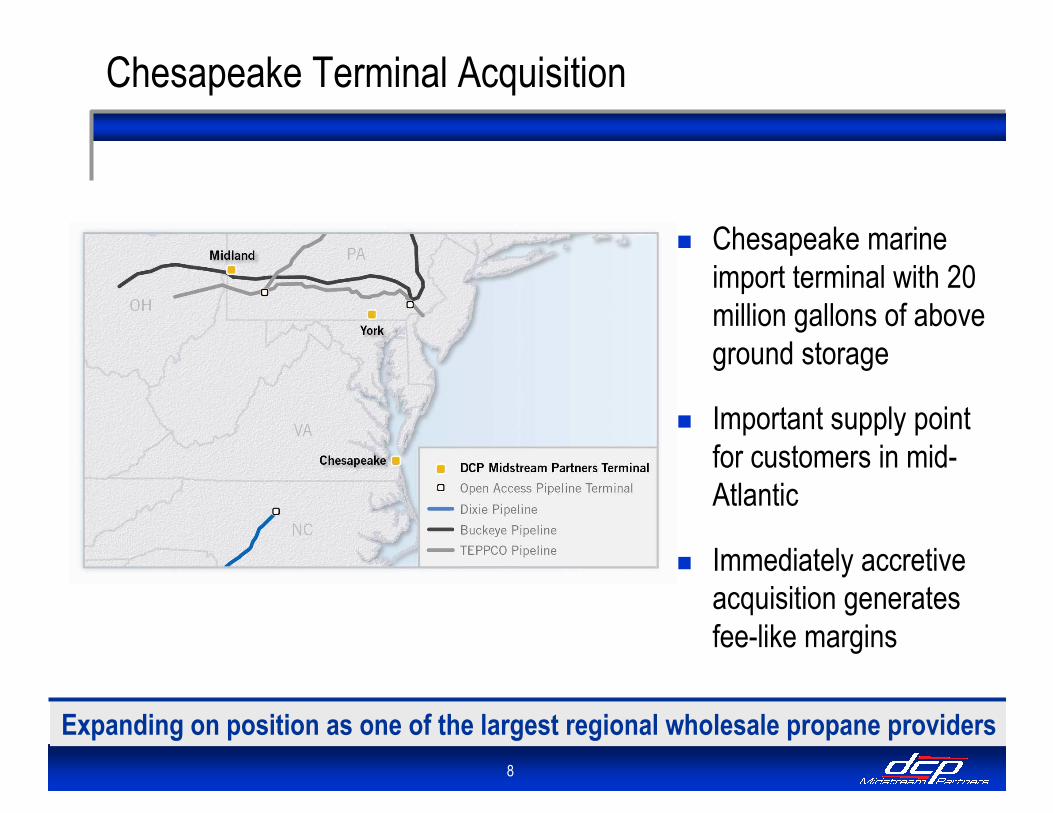

� Chesapeake marine import terminal with 20 million gallons of above ground storage

� Important supply point for customers in mid-Atlantic

� Immediately accretive acquisition generates fee-like margins

Chesapeake Terminal Acquisition

Expanding on position as one of the largest regional wholesale propane providers

9

� Wattenberg acquisition integration and expansion project on plan to be completed early 2011

� Immediately accretive acquisition of additional 55% ownership interest in Black Lake pipeline

NGL Logistics Segment

Integrated fee-based business providing expansion opportunities

10

Consolidated Financial Results

Six Months

Ended June 30,Three Months Ended June 30,

1.14x

$56.6

$66.3

2010($ in millions)

Coverage Ratio

Distributable Cash Flow

Adjusted EBITDA

1.19x1.03x0.99x

$50.6$23.2$24.9

$72.6$32.4$26.2

200920092010

On track to achieve 2010 DCF forecast

11

Natural Gas Services Segment

Results relatively flat on a sequential quarter basis

28,584

1,108

$14.5

$34.5

2009

Six Months

Ended June 30,

Three Months

Ended June 30,

$27.7$33.2$17.0Operating and maintenance expense

25,20833,36033,846NGL gross production (Bbls/d)

1,0511,1631,161Natural gas throughput (MMcf/d)

Operating Statistics:

$59.0$66.4$33.1Adjusted Segment EBITDA

200920102010($ in millions)

12

Wholesale Propane Logistics Segment

Results tempered by planned outage and warmer weather

13,912

$2.4

$3.5

2009

13,055

$2.6

$(0.5)

2010

Three Months

Ended June 30,

Six Months

Ended June 30,

20092010($ in millions)

25,50223,205Propane sales volume (Bbls/d)

$5.1$5.2Operating and maintenance expense

Operating Statistics:

$26.4$11.2Adjusted Segment EBITDA

13

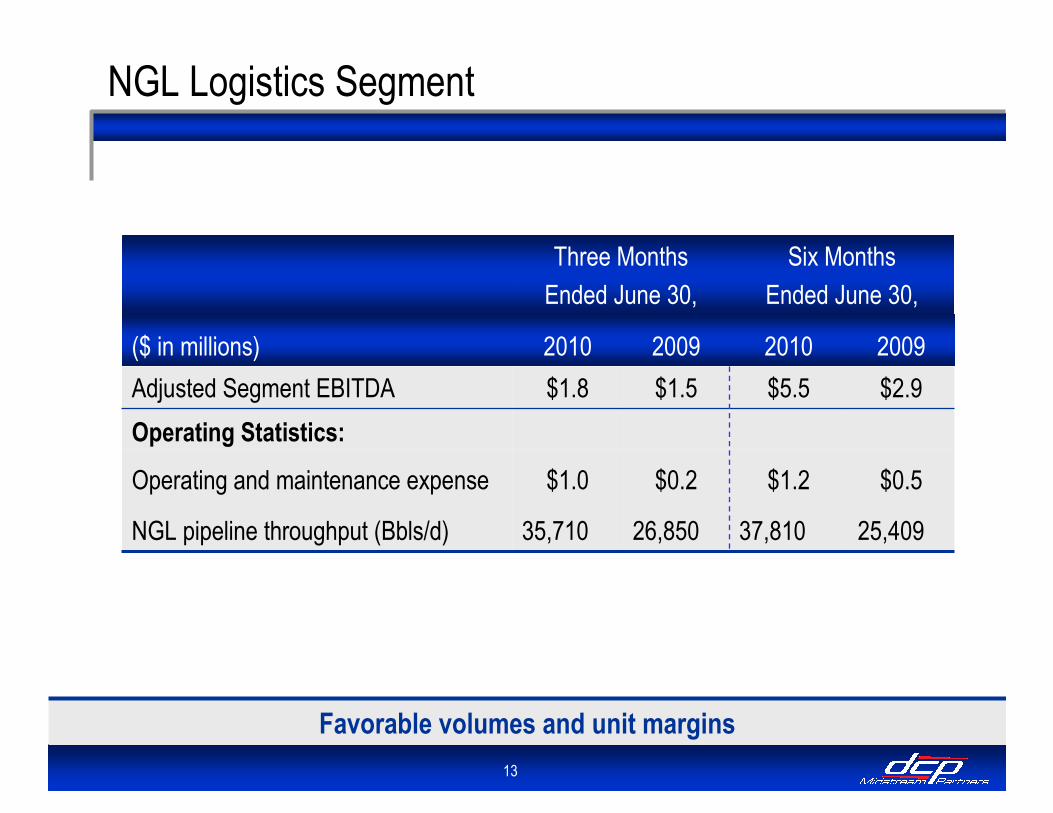

NGL Logistics Segment

Favorable volumes and unit margins

Six Months

Ended June 30,

Three Months

Ended June 30,

26,850

$0.2

$1.5

2009

37,810

$1.2

$5.5

2010 20092010($ in millions)

25,40935,710NGL pipeline throughput (Bbls/d)

$0.5$1.0Operating and maintenance expense

Operating Statistics:

$2.9$1.8Adjusted Segment EBITDA

14

2010 DCF Forecast

� Chesapeake and Black Lake acquisitions provide an additional $3 million to 2010 DCF forecast

� Additional 2011 base business contributions� Wattenberg NGL pipeline

integration and expansion completed

� Integration and synergy benefits from recent Michigan acquisition

Base business provides adequate distribution coverage in current environment

Original DCF forecast provided March 2010

$90

1.15x-1.50x1.05x-1.30x1.00x-1.15xDistribution

Coverage Ratio

NGL to Crude Relationship

$125-$150

$115-$130

70%60%50%

$80

$70

$60

Crude ($/Bbl)

($ in millions)

Reflects range of YTD and general market views of commodity prices

$100 - $110

$105 - $115

$105 - $120

$115 - $130

15

3.9x

4.3%

$235

(615)

$850

Credit Facility Leverage Ratio (max 5.0x/5.5x)

Effective Interest Rate

Credit Metrics and Covenants

Net Capacity Available

Less: Revolver Drawn

Credit Facility Commitment

Credit Facility and Liquidity (As of 6/30/10)

Disciplined financial management consistent with investment grade objective

Financial Position

� Continue to execute on investment grade plan� Received Fitch investment grade credit rating in May

� Maintain liquidity to support 2010 plan and future growth� Reinstated $25 million credit facility commitment

� Disciplined approach to long-term financing($ in millions)

16

Growth Opportunities

Strategic and disciplined growth across all segments

� Growth continues to enhance diversity of asset portfolio� Executing on opportunities across all business segments

� Extending geographic footprint

� Recent growth resulting in increased percentage of fee-based margins

Dropdowns

Offshore development

Potential divestitures by majors and E&P

Emerging shale play infrastructure development

Natural Gas Services

Dropdowns

Offshore development

Potential divestitures by majors and E&P

Emerging shale play infrastructure development

Natural Gas Services

- Third party acquisitions

- Organic projects

Footprint expansion

Wholesale Propane Logistics

- Third party acquisitions

- Organic projects

Footprint expansion

Wholesale Propane Logistics

�

�

�

Organic expansion around footprint- DJ Basin

Dropdowns

Potential divestitures by majors

NGL infrastructure development in shale plays

NGL Logistics

Organic expansion around footprint- DJ Basin

Dropdowns

Potential divestitures by majors

NGL infrastructure development in shale plays

NGL Logistics

�

�

�

17

Outlook and Summary

� On track to achieve 2010 business plan commitments and forecast

� Delivered on 2010 objective of resuming distribution growth

� Executing on growth opportunities

� Targeting long-term top quartile total shareholder return

� Sponsorship of DCP Midstream, ConocoPhillips and Spectra

18

Q&A

19

Appendix

20

Consolidated Financial Results

1.19x1.14x1.03x0.99xCoverage ratio

(30.9)(36.5)(16.3)(18.7)Depreciation and amortization expense

1.01x

$24.9

$26.2

$ 26.0

(1.0)

(0.1)

(7.3)

6.6

27.8

(249.7)

3.5

(8.2)

(20.6)

(205.7)

277.5

22.5

$ 255.0

2010

Three MonthsEnded June 30,

Six MonthsEnded June 30,

200920102009($ in millions)

1.26x

$ 50.6

$ 72.6

$ (21.0)

(0.8)

(0.1)

(14.0)

2.6

(8.7)

(445.1)

-

(15.7)

(33.3)

(365.2)

436.4

(38.9)

$ 475.3

1.15x

$56.6

$66.3

$ 51.8

(1.1)

(0.4)

(14.5)

14.5

53.3

(627.9)

3.5

(16.8)

(39.6)

(538.5)

681.2

28.5

$ 652.7

1.15x

$ 23.2

$ 32.4

$ (42.1)

(2.1)

-

(6.9)

3.7

(36.8)

(188.8)

-

(7.1)

(17.1)

(148.3)

152.0

(45.9)

$ 197.9

General and administrative expense

Total operating revenues

Gains (losses) from commodity derivative activity, net*

Operating and maintenance expense

Operating income (loss)

Adjusted EBITDA

Interest expense, net

Earnings from unconsolidated affiliates

Cash distribution coverage

Distributable cash flow

Net income (loss) attributable to partners

Net income attributable to noncontrolling interests

Total operating costs and expenses

Income tax expense

Other income

Purchases of natural gas, propane and NGLs

Sales, transportation, processing and other revenues

* Details on following page

21

Commodity Derivative Activity

Six Months

Ended June 30,

Three Months

Ended June 30,

$(45.9)

-

8.2

$(54.1)

$(54.1)

-

$(54.1)

2009

$28.5

(2.0)

-

$30.5

$30.1

(0.4)

$30.5

2010

$(53.8)$22.3Non-cash gains (losses)

(0.5)-Non-cash losses – other*

$(53.3)$22.3Non-cash gains (losses) – commodity derivative

--Cash commodity hedge settlements paid

(38.9)$22.5Gains (losses) from commodity derivative activity, net

20092010($ in millions)

14.40.2Cash commodity hedge settlements received

$(53.3)$22.3Non-cash gains (losses) – commodity derivative

* Other non-cash losses represent the amortization of the deferred net losses related to our change in accounting method from cash flow hedge accounting to mark-to-market accounting. These losses were classified to sales of natural gas, propane, NGLs and condensate during the current period.

22

Balance Sheet

¹ Long-term debt includes $0 and $10 million outstanding on the term loan portion of our credit facility as of June 30, 2010 and December 31, 2009, respectively. These amounts are fully secured by restricted investments.

$ 1,481.5

227.7

377.7

72.0

613.0

$ 191.1

$ 1,481.5

273.7

1,000.1

10.0

195.6

$ 2.1

December 31, 2009

$ 1,413.2

224.2

379.6

53.6

615.0

$ 140.8

$ 1,413.2

270.0

1,008.5

-

129.9

$ 4.8

June 30, 2010

Total liabilities and equity

Noncontrolling interest

Partners’ equity

Other long term liabilities

Long-term debt¹

Current liabilities

Total assets

Other long term assets

Property, plant and equipment, net

Restricted investments¹

Other current assets

Cash and cash equivalents

($ in millions)

23

2010 Margin

Contracts and Commodity Sensitivities

* Excluding keep whole sensitivities

** Impact to Adjusted EBITDA increases/decreases by ~$1.6MM for each $20/Bbl increase/decrease in crude oil price from $70/Bbl

Over 90% of 2010 margins are fee-based or supported by commodity hedges

+/- $5.6

+/- $1.3

+/- $0.2

Impact to Adjusted EBITDA ($MM)

+/- 5 percentage point change (assuming 60% NGL to crude relationship and $70/Bbl crude)

+/- $5.00/Bbl change in crude at 60% NGL to crude relationship

+/- $1.00/MMBtu change

Amount of Change

NGL to Crude Relationship**

Crude Oil

Natural Gas

Commodity

Estimated 2010 Annual Commodity Sensitivities*

2010 MarginPercentage of

Proceeds/Liquids 32%

Fee-Based 56%

Condensate 7%Keep Whole

5%

Fee-Based

56%

Commodity

Hedged

37%

Commodity

Unhedged

7%

24

Long-Term Cash Flow Stability

(1) As of 7/30/10

Multi-year hedge positions provide cash flow stability

2,665

2,600

2,125

2,050

1,500

500

$67.04 $68.28 $68.47$72.57

$82.61

$92.00$80.14

$83.48 $85.15 $86.05 $86.97 $88.18

0

500

1000

1500

2000

2500

3000

2010 2011 2012 2013 2014 2015

Hed

ge Volum

e (Bbls/d)

$0

$25

$50

$75

$100

$125

Crude

Oil

Hedged Crude Volume (Bbls/d)

Weighted Average Swap Price

Forward Price (1)4,539

2,900

2,900

1,800

1,000

$6.32 $6.16

$5.06

$5.83$6.32

$5.19

$4.64

$5.18 $5.16$4.95

0

1000

2000

3000

4000

5000

2010 2011 2012 2013 2014Hedge Volum

e (MMBtu/d)

$0

$2

$4

$6

$8

$10

Natural Gas

Hedged Natural Gas Volume (MMBtu/d)

Weighted Average Swap Price

Composite Forward Price (1)

� Over 55% of 2010 forecasted margin is fee-based

� For commodity-based margins, 80+% hedged on crude oil equivalent basis in 2010

Crude Oil Hedge Position Natural Gas Hedge Position