the 2016 us presidential election - not your typical year

TRANSCRIPT

The 2016 US Presidential Election - Not

Your Typical Year

Any major economic or political event in the US, especially one that is recurring,

is bound to be tested for its impact on the stock market.

And as far as big events go, there are few as big and closely followed as the US

Presidential elections.

Given the importance of the event, the Internet’s already abuzz with speculation.

There has always existed a fairly evident cyclicality between the stock market’s

performance in the US and its four-year Presidential term.

While each presidential cycle would typically have its own set of unique

circumstances and economic indications, over the past 116 years (period

considered for analysis in this note) the latter part of a presidential term has been

favourable for stock prices. We observe that policy decisions necessary for

improved economic activity and growth typically occur during the first half of a

presidential term.

While the net impact of these decisions are meant to be positive, they could still

imply higher taxes, increased regulation, and tighter controls. As such, they may

not bode well for corporate profit expectations.

As a President approaches the latter part of his term, policies tend to favour the

electorate. Harsher measures are unlikely to be put in place. Of course, external

global factors would still play a role in determining which way the stock market

moves. A case in point is the recent global recession of 2008, where despite

being the last year of a US presidency, the Dow Jones lost 34% of its value led

by the sub-prime crisis and a near freeze on global financial markets.

Having stated the average US stock market behaviour driven by the US

presidential cycle, we believe the 2016 election year would break away from the

trend. While there are a few noteworthy common traits that suggest 2016

shouldn’t stray from the norm, there are some clear emerging trends that, in our

view, could defy it.

The Two Sides of the US Political System

Before we illustrate our findings, here’s an overview of the US political system

with respects to its two oldest parties, i.e. the Democratic Party (est. 1828) and

the Republican Party (est. 1854).

Since the beginning of the 20th century, both parties have shared the presidency

almost equally, 15 for the Republicans and 14 for the Democrats.

Policy-wise and on key issues, both parties differ markedly.

While Democrats are more liberal and progressive, the Republicans tow a

conservative and traditionalistic line.

Here is how they compare on some of the most debated issues in the US.

Both parties have been diametrically opposite on some very contentious issues

in recent US political and economic debates however, some of which include

calls for tighter gun control after a spate of civilian gun shooting incidents, issues

related to immigration especially with the mass exodus of Syrian refugees

currently taking place in the Middle East, and government spending on

healthcare. Looking at the above comparison, one can understand the strong

rhetoric used by the current Republican hopeful Donald Trump with respect to

gun control and immigration.

Some of the more prominent candidates for the nomination of the 2016 US

Presidential election include Donald Trump, Ted Cruz, and Marco Rubio from the

Republican Party. The Democrats have Bernie Sanders and former First Lady

and Secretary of State Hillary Clinton as two of their main candidates.

Presidential Terms and the US Stock Market’s

Cyclicality

Coming back to the impact of a Presidential term on the stock markets, our

empirical analysis backs the view that — historically — the second half of the

four year period has been stronger on average.

The Dow Jones Industrial Average has returned, on average, nearly 12% and 7%

in Year 3 and Year 4 respectively over the past 29 Presidential terms. The

economy has also performed comparatively better on average in that period,

which, in our view, reflects the impact of the measures that the governments

usually put in place during the first half. It’s also worth noting that, historically, a

majority of corporate tax increases have occurred during the first half, while a

majority of the corporate tax cuts have occurred during the second half.

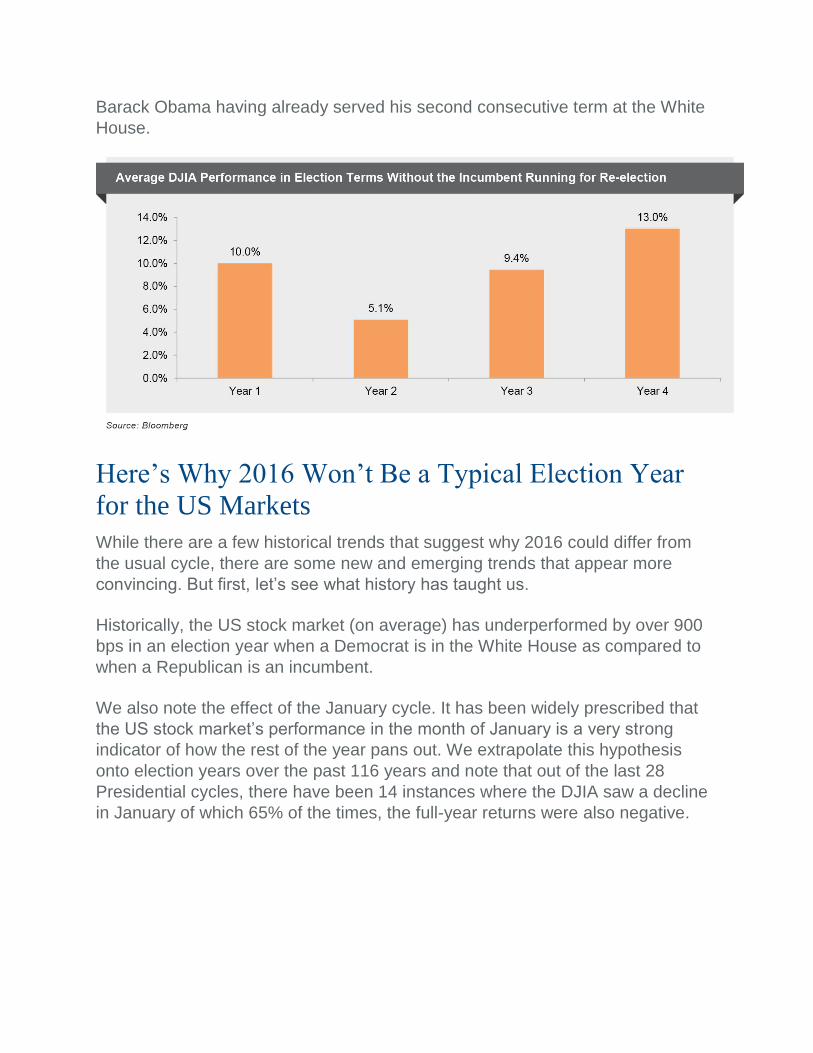

Another interesting anecdote to note is that the US stock market, in an election

year, has gained (on average) its highest when the incumbent President is not

running for a re-election. This is the case in 2016, with the current President

Barack Obama having already served his second consecutive term at the White

House.

Here’s Why 2016 Won’t Be a Typical Election Year

for the US Markets

While there are a few historical trends that suggest why 2016 could differ from

the usual cycle, there are some new and emerging trends that appear more

convincing. But first, let’s see what history has taught us.

Historically, the US stock market (on average) has underperformed by over 900

bps in an election year when a Democrat is in the White House as compared to

when a Republican is an incumbent.

We also note the effect of the January cycle. It has been widely prescribed that

the US stock market’s performance in the month of January is a very strong

indicator of how the rest of the year pans out. We extrapolate this hypothesis

onto election years over the past 116 years and note that out of the last 28

Presidential cycles, there have been 14 instances where the DJIA saw a decline

in January of which 65% of the times, the full-year returns were also negative.

The year 2016 saw the DJIA fall by over 5% in the month of January. Over the

past 115 years, over 60% of the time, January’s performance has been an

accurate indicator of how the entire year would settle.

The World Is a Different Playground Now

While we’ve noticed a few trends in history that suggest 2016 will defy the norm,

the fundamentally different global economic scenario that the current election

year is encountering could make a huge difference.

The biggest game changing factor of all, in our opinion, is China.

The Asian economy now contributes almost 16% to global GDP and is the

second largest in the world. US’ trade deficit with China has increased nearly 5x

over the past decade and a half alone. Therefore, China’s rapid economic

slowdown is likely to build pressure in 2016.

The current oil price dynamic also has no precedent.

Oil prices have lost almost 70% of their value since the mid-2014. As much as

the tepid global economic growth scenario has a role to play, the ongoing geo-

political crisis has exacerbated the fall. Some might argue that $30/barrel is

pretty much the floor; volatility on the way up could still keep US markets on the

edge in 2016. Only three times in last 116 years has the price of oil dropped as

much or more in the year preceding an election year.

Finally, the US dollar has seen significant gains in the past 12-15 months and

could also put some pressure on overall economic growth in the US. A strong

American Dollar makes US goods more expensive in foreign markets, leading to

a negative impact on the US’ overall trade balance. 2016 could also see a much

more definitive move up in the Fed fund rates, putting further pressure on US

equities.

We also note that 2015 saw the dollar index increase by almost 10%, among the

highest gains any year has seen going into the election year. Our analysis

suggests that over the past 50 years, the dollar index and the Dow Jones

Industrial Average have an inverse correlation of 48% suggesting that a

strengthening dollar, going into 2016, has a good chance of keeping the equity

market under check.

Valuation doesn’t seem to be in favour of the US equity market either.

The S&P 500, adjusted for inflation and cyclicality, is trading at near all-time high

levels, excluding the technology bubble seen at the start of the last decade.

We, therefore, believe it would be unwise to position one’s portfolio towards US

equities purely on the basis of the US market’s cyclicality with Presidential

election years. There are clearly more than a few factors that are likely to be

headwinds for the market. The ongoing Presidential campaigns and debates too

have been rather vague and uninspiring, leading to more scepticism. We believe

US’ safe haven tag and lack of alternatives for equity investments elsewhere

globally are the two key factors that are likely to extend support to the market.

About Aranca:

Aranca is a leading provider of high quality, customized and cost effective research and analytics to global

clients. Founded in UK in 2003, Aranca has a global presence including in the US, Europe and Middle East,

and a state-of-the-art delivery center in Mumbai, India.

Our research solutions are structured around four complementary business lines: Investment Research,

Business Research, Valuation and Advisory Services and Intellectual Property Research.

Over the years, Aranca has become a trusted partner to over 1500 global organizations including Fortune

500 companies, SMBs, investment banks, brokerage firms, asset management firms, consulting firms, PE

and VC firms, law firms, government bodies, trade associations and universities.