brazilian agribusiness at a glance - embrapa labex korea

TRANSCRIPT

© 2010 by Ministry of Agriculture, Livestock and Food Supply.All rights reserved. It is authorized the partial or total reproduction of this material, on condition that the source is identified,without sale purpose or any commercial end.The copyright responsibility of the texts and images of this work belongs to the author.

First edition - comprehensive: 2010Printed: 10.000 issues

Information, production, distribution:Ministry of Agriculture, Livestock and Food SupplySecretariat of Agribusiness International RelationsDepartment of Agribusiness International Promotion

Esplanada dos Ministérios, Bloco D, 3º andar, sala 300CE P: 70043-900, Brasília – DFPhones: + 55 61 3218-2510 / 3225-4497Fax: + 55 61 [email protected]

Technical Elaboration:Eduardo Sampaio MarquesMaurício Pinheiro Fleury CuradoTelma Cristina Ikeda GondoFabrício Bentes Simões

Editorial Coordination: Department of Social Communication

Printed in Brazil

Catalogação na FonteBiblioteca Nacional de Agricultura – BINAGRI

Brazil. Ministry of Agriculture, Livestock and Food Supply.Brazil and agribusiness : at a glance / Ministry of Agriculture, Livestock and Food Supply. Secretariat of Agribusiness International Relations. – 1st ed. comprehensive. – Brasília : Mapa/ACS, 2010.

67 p. : il.

ISBN 978-85-7991-034-0

1. Agribusiness - Brazil. 2. Exportation. I. Secretariat of Agribusiness International Relations. II. Title.

AGRIS E70CDU 339.56

Ministry of agriculture, livestock and food supplysecretariat of agribusiness international relations

Missionto promote the sustainable

development and the agribusinesscompetitiveness in benefit of the

Brazilian society.

Brazilian agribusiness at a glance

BraZil - Brasilia 2010

Brazil is a strategic partner when it comes to agribusiness products supply. At the same time, Brazilian agricultural commodities are recognized for their intrinsic technology and competitiveness. There are, still, some boundaries to surpass and opportunities to show, information and interest being vital for so.

In a time when natural resources, food security and renewable energy are being largely debated, this publication aims at providing brief information on Brazilian agricultural products, the country’s capacity to produce and supply and, furthermore, its care in using sustainable procedures, in order to guarantee food, work and resources for our future generations.

The content of this material came from several lectures given by authorities and technicians of this Ministry in different places and occasions. Due to the high demand of hardcopies after each presentation, we consider that the information can be relevant to your acquaintance.

We hope this information can be useful as a way of making you interested in getting to know more about Brazil and its agricultural production.

Should you need further information, please contact us at: [email protected].

We will be delighted in hearing from you.

Wagner RossiMinister of Agriculture, Livestock and Food Supply

Summary

COuNTry OVErVIEW ...........................................................................6

GLOBaL DyNamICS ............................................................................10

TOP PrODuCTS HIGHLIGHTS ...............................................................18

Grain .................................................................................................21

meat..................................................................................................33

Sugarcane ..........................................................................................38

Coffee ...............................................................................................45

milk ...................................................................................................48

Fruits ..................................................................................................50

SuSTaINaBILITy: aGrICuLTurE & ENVIrONmENT ...................................54

FOrEIGN INVESTmENT OPPOrTuNITIES ................................................60

COuNTry OVErVIEW

7

COUNTRY OVERVIEW

• Area: 8,514,000 km² (5th largest)• Population: 191.3 million (5th biggest population)• GDP: US$ 1.6 trillion (8th biggest economy)• Per capita income: US$ 8 thousand• 2009 exports: US$159 billion• 2009 imports: US$136 billion

Brazil’s Profi le

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

8

AMAZON

49.3%CAATINGA

9.9%

CERRADO

23.9%PANTANAL

1,7%

PAMPA

2.0%

ATLANTICFOREST

13,0%

BraZILIaN TErrITOry

BraZILIaN BIOmES

Amazon Biome 420

Crops 77

Pastures 173

Planted Forests 6

Brazil 851

sources: Ministry of agriculture; Ministry of environment - 2006

Brazil’s continental dimensions gather different biomes (*), protected by national legistation.

agriculture and livestock areas make up around 30% of Brazil’s territory, mainly concentrated in the southern and central regions of the country.

(*) any of several major life zones of interrelated plants and animals determined by the climate.

In million ha

9

COUNTRY OVERVIEWagricultural production started primarily in the southern region and, later on, expanded to other areas towards the middle-west of the country.

High levels of productivity as a result of investments in tropical technology allow coexistence of expansion of food and energy production, along with environmental protection.

1970

1980

1990

1960

aGrIBuSINESS EXPaNSION

GLOBaL DyNamICS

11

GLOBAL DYNAMICS

Main Products Production ExportsNumber of

Markets

Exports

US$ Billion

Sugar 1st 1st 124 8.378

Coffee 1st 1st 81 3.762

Orange Juice 1st 1st 75 1.619

Soybean 2nd 2nd 46 11.413

Beef 2nd 1st 142 4.118

Tobacco 2nd 1st 100 2.992

Ethanol 2nd 1st 48 1.338

Broiler 3rd 1st 146 5.307

Corn 4th 3rd 49 1.259

Pork 4th 4th 81 1.225

sources: usda, Ministry of agriculture

2009 ranking: Brazilian Production and Exports

Brazil plays a leading role as a global supplier of agribusiness products, exporting for more than 180 markets.

Diversifi ed product range ensures food security for the world.

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

12

Total: uS$ 64.8 billion

Brazilian agribusiness Exports main Products

source: Ministry of development, industry and foreign trade – 2009 elaboration: Ministry of agriculture

Brazil exports a great deal of agricultural products, including traditional goods, such as coffee and sugar, besides recently introduced ones, such as corn and ethanol.

Soybean & Products26.6%

Meat18.2%

Sugar & Ethanol15.0%

Coffee6.6%

Tobacco & Products4.6%

Orange Juice2.5%

Corn1.9%

Leather1.8%

Others22.7%

13

GLOBAL DYNAMICS

Total: uS$ 64.8 billion

Brazilian agribusiness Exports main Destinations

source: Ministry of development, industry and foreign trade – 2009 elaboration: Ministry of agriculture

Brazil’s diversifi ed product portfolio enables strategic partnerships around the world.

Besides the capacity to assure food security, Brazilian agribusiness has recently been seen as an opportunity for foreign investment.

EU-2729.3%

China13.8%

USA7.0%

Russia4.3%

India2.8%

Japan2.8%

Hong Kong2.6%

Venezuela2.4%

Saudi Arabia2.3%

South Korea2.0%

Others30.6%

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

14

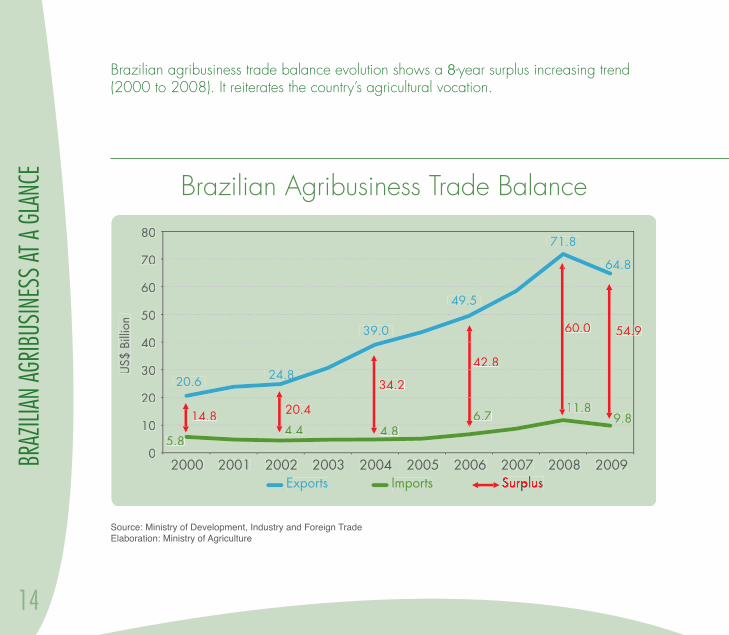

source: Ministry of development, industry and foreign tradeelaboration: Ministry of agriculture

Brazilian agribusiness Trade Balance

20.6 24.8

39.0

49.5

71.8

64.8

4.4

11.8 9.8

0

10

20

30

40

50

60

70

80

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

20.4

US$

Bill

ion

5.8 5.8 4.8

6.7

Exports Imports Surplus Surplus Surplus

54.9 54.9 60.0

42.8

34.2

14.8

Brazilian agribusiness trade balance evolution shows a 8-year surplus increasing trend (2000 to 2008). It reiterates the country’s agricultural vocation.

15

GLOBAL DYNAMICS

source: Ministry of development, industry and foreign trade elaboration: Ministry of agriculture

Brazilian Trade Balance

The positive results of the Brazilian trade balance rely on agriculture. Solid institutional framework and resilient economy mitigate risk of agribusiness commodities exports setback.

25.5

-29.3

1980 1982 1984 1986 1988 1990 19941992 1996 1998 2000 2002 2004 2006 2008

54.8

0-10

-30-20

-50-40

10203040506070

US$

Bill

ion

-29.3

TOTAL

AGRIBUSINESS

OTHERS

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

16

Domestic Consumption and Exports

Domestic Consumption Exports

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Ethanol

Sugar

Coffee

Beef

Broiler

Soybean

Corn

Cotton

sources: Ministry of agriculture, Brazilian institute of geography and statistics - 2009

roughly 70% of the Brazilian agricultural production aims the national market. Domestic demand ensures critical mass for market predictability, enabling expansion planning.

TOP PrODuCTS HIGHLIGHTS

19

TOP PRODUCTS HIGHLIGHTS

Total: uS$ 170 billion

major agricultural Products in Brazil Production – Gross Value

Beef21%

Soybean16%

Sugarcane10%Corn

7%

Milk7%

Broiler6%

Coffee5%

Rice4%

Beans3%

Others21%

source: Brazilian confederation of agriculture and livestock – June 2009

Brazilian agricultural production has been reaching successive records in gross value. Worldwide leading products such as beef, soybean, sugar, broiler and coffee account for the majority of the production value.

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

20

agriculture area2007/2008 Harvest

0

20

40

60

80

100

120

140

160

180

200

2.3 7.0 14.3 21.6

172.3

Coffee SugarcaneCorn

SoybeanPasture

Mill

ion

ha

0

20

40

60

80

100

120

140

160

180

200200

2.32.3 7.07.0 14.314.3 21.621.621.6

172.3172.3

Coffee SugarcaneCorn

SoybeanPasture

Mill

ion

ha

sources: Ministry of agriculture, Brazilian institute of geography and statistics (pasture – 2006)

Pasture lands occupy nearly 70% of the total area dedicated to agricultural production.

Pasture productivity is still low – 1 head per hectare. Improvements on cattle raising enable agriculture growth over these areas.

Grain

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

22

Grain - Production and area

Harvested Area Growth: 27% = 1.3% / year

Growth: 145% = 4.8% / year

Prod

uctio

n M

illio

n to

ns/M

illio

n ha

57.9 68.3

81.1 78.4 82.4

100.3

123.2 122.5

114.7

131.7 135.2

143.7 141.6

37.9

19910

20

40

60

80

100

120

140

160

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010(E)

35.6 38.5 36.6 36.9 37.843.9 49.1 46.2 47.7 48.1

Growth: 27% = 1.3% / year

Harvested Area Production

source: national company of food supply

Increase in grain production over the last 20 years has been a result of high levels of productivity. Grain volume has increased by 2.5 in the period, while the harvested area has grown less than 30%. Productivity in the area, therefore, doubled.

23

TOP PRODUCTS HIGHLIGHTS

Product Area

(1,000 ha)% of Total Grain Area

1,000 Tons

Soybean 21,743 42% 57,166

Corn 14,171 38% 51,004

Bean 4,147 3% 3,491

Rice 2,909 9% 12,602

Wheat 2,396 4% 5,884

Cotton 843 2% 1,891

source: national company of food supply - 2009

main Grains

Grain crops’ increasing productivity allows supply of domestic market while Brazil stands out as a big exporter of soybean, corn and cotton.

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

24

Grain Productivity Evolution Index

source: national company of food supply

Grain productivity has been increasing in Brazil over the years, as a result of technology use and best practices dissemination.

0

50

100

150

200

250

300

350

400

1990

/91

1991

/92

1992

/93

1993

/94

1994

/95

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10(

E)

Cotton Rice Bean Soybean Corn

Inde

x

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

26

In 2008/2009 harvest, Brazilian cotton producers reached the highest productivity in the world, making a high-quality, competitive product that stands out from the top 5 global producers. That was a cornerstone to recover its leading position in this market.

Cotton Productivity

0

150

300

450

600

750

900

1050

1200

1350

1500

Kg/ha

758

14431310

911

523

WorldBrazil

ChinaUSA

Indiasource: usda - 2008/09elaboration: Ministry of agriculture

27

TOP PRODUCTS HIGHLIGHTS

Soybean – Production and area

Mill

ion

tons

/Mill

ion

ha

10

-

20

30

40

50

60

70

80

1991

/92

1993

/94

1992

/93

1994

/95

1995

/96

1996

/97

1997

/98

1998

/99

1999

/2000

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10(E)

Harvested Area Production

source: national company of food supply

Soybean is the major agricultural crop in Brazil. Its production increase has been a result of high levels of productivity. Over the last 20 years, soybean volume has increased by 3.5, fi lling up domestic consumption and enabling Brazil’s leverage to second biggest world exporter position.

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

28

Total: uS$ 17.2 billion

Soybean Exports – Grain, meal and Oilmain Destinations

EU-2739.9%

China39.2%

Iran5.1%

Thailand4.3%

Japan1.5%

India1.6%

Taiwan1.3%

Others9.5%

although China and the European union were the destinations for 79% of soybean and its products’ exports in 2009, dozens of other markets also imported from Brazil, since these products compound both animal and human diets.

source: Ministry of development, industry and foreign trade – 2009 elaboration: Ministry of agriculture

29

TOP PRODUCTS HIGHLIGHTSSince 2006, private representatives of the soybean segment declared “moratorium“ to the soybean produced in the amazon Biome - a comprehensive commitment prohibiting to buy or sell the product of such region. Satellite monitoring controls the origin of the product and ensures the rain Forest protection.

sources: Ministry of agriculture, Brazilian institute of geography and statistics

AMAZON BIOME

Since the “moratorium”, soybean area

decreased to 0.27% of the Amazon Biome.

“Soybean is no longer an issue for the Amazon Biome deforestation”.

Minister of Environment of Brazil

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

30

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

-

10

20

30

40

50

60

Mill

ion

tons

1991

/92

1990

/91

1993

/94

1992

/93

1994

/95

1995

/96

1996

/97

1997

/98

1998

/99

1999

/2000

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10(E)

2nd harvest share of total productionMain harvest2nd harvest

Corn – Double Cropping

The increasing production of corn from double cropping, planted after the soybean summer crop, reduces fi xed costs, boosts the growth of the meat industry in Brazil and, at the same time, allows Brazil to become a relevant exporter in these segments.

source: national company of food supply

31

TOP PRODUCTS HIGHLIGHTS

Scale, mechanization. Two crops in the same year without irrigation.

Double CroppingCorn after Soybean

Sowing corn(2nd harvest)

Harvestingsoybean

No tillage(environmentally friendly)

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

32

Total: uS$ 1.3 billion

source: Ministry of development, industry and foreign trade – 2009 elaboration: Ministry of agriculture

Iran22.5%

Malaysia10.3%

Colombia10.1%

Taiwan9.6%

South Korea7.9%

Saudi Arabia7.8%

Morocco5.4%

EU-274.0%

Others22.4%

Corn Exportsmain Destinations

meat

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

34

The combined expansion of the meat production and industrialization in Brazil leveraged the country to the #1 position in exports worldwide, while keeping up with the domestic market, which presents a high and growing per capita consumption (more than 80kg/inhabitant/year).

meat Production Evolution

sources: aBiec, aBef, uBa, aBipecselaboration: Ministry of agriculture

0

2

4

6

8

10

12

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Beef Broiler Pork

Mill

ion

tons Beef: +83% (1994-09)

Broiler: +216% (1994-09)

Pork: + 140% (1994-09)

35

TOP PRODUCTS HIGHLIGHTS

Beef* Exportsmain Destinations

Total: uS$ 3.0 billion

Brazil is the worldwide leading supplier of both beef and Halal beef. Brazilian beef is recognized as the “green beef”, once cattle is raised free, in vast pastures. Vegetal feeding avoids harmful illnesses to human beings, such as the mad Cow Disease.

Russia30.1%

Iran11.1%

Hong Kong10.5%

EU-279.8%

Egypt6.6%

Venezuela5.5%

Algeria4.7%

Others21.7%

* In naturasource: Ministry of development, industry and foreign trade – 2009 elaboration: Ministry of agriculture

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

36

Broiler* Exportsmain Destinations

Saudi Arabia15.4%

Japan12.8%

Hong Kong12.2%

UAE6.5%EU-27

6.5%Venezuela

6.0%

Kuwait5.6%

Iraq4.0%

Others30.9%

Total: uS$ 4.8 billion

Brazilian chicken is present in the meals of consumers of most markets in the world. The integration of the productive chain, from egg to tailored cuts, make the Brazilian chicken products competitive and adaptable to each and every market niche. Brazil is the biggest world exporter of both broiler and Halal broiler.

* In naturasource: Ministry of development, industry and foreign trade – 2009 elaboration: Ministry of agriculture

37

TOP PRODUCTS HIGHLIGHTS

Russia50.6%

Hong Kong14.5%

Ukraine9.5%

Singapore6.3%

Argentina4.5%

Angola3.8%

Other10.8%

Total: uS$ 1.1 billion

Pork* Exportsmain Destinations

The Brazilian integrated pork productive system results in high quality goods, according to the world’s most rigid standards.

* In naturasource: Ministry of development, industry and foreign trade – 2009 elaborated by Mynistry of agriculture

Sugarcane

39

TOP PRODUCTS HIGHLIGHTS

Sugar and Ethanol: Production and area

Sugarcane can be transformed in sugar and ethanol, besides other sub-products, such as fertilizer and electricity (from bagasse). In Brazil, production of food, fuel and energy can increase substantially, coexisting with all other food crops and environmental preservation.

sources: Ministry of agriculture, national company of food supply

35 20

18

16

14

10

8

12

6

4

2

0

30

25

20

15

10

11.5

7.4

31.3

27.6

5

1991

/92

1992

/93

1993

/94

1994

/95

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

0

Prod

uctio

n

Harvested area (m

illion ha)

Ethanol (million m3)Sugar (million tons)Harvested area

SugarGrowth 2002-09: 93.2% (8.6% p.y.)

EthanolGrowth 2002-09: 142.4% (11.7% p.y.)

Harvested AreaGrowth 2002-09: 44.5% (5.4% p.y.) 4.3

8.9

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

40

Total: uS$ 8.3 billion

Sugar Exportsmain Destinations

India17.5%

Russia10.4%

UAE7.1%

Nigeria4.9%

Bangladesh4.8%Algeria

4.0%Saudi Arabia4.0%

Canada3.6%

Others43.7%

Brazil is the #1 exporter of sugar, accounting for almost half of the world’s market.

source: Ministry of development, industry and foreign trade – 2009 elaboration: Ministry of agriculture

41

TOP PRODUCTS HIGHLIGHTSBrazil leads the exports of ethanol, although 90% of its production is consumed domestically. The use of ethanol as fuel reduces the emission of pollutants.

source: Ministry of development, industry and foreign trade – 2009 elaboration: Ministry of agriculture

Ethanol Exports main Destinations

EU-2728.7%

Jamaica11.4%

South Korea10.4%

USA10.1%

India9.4%

Japan8.1%

Others21.9%

Total: uS$ 1.3 billion

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

42

Energy mix

almost half of the sources of the Brazilian energy matrix are renewable, sugarcane being the second most important one.

source: Ministry of energy and Mining – 2009elaboration: Ministry of agriculture

Oil and Oil Products

38%

Oil and Oil Products

35%

Sugarcane18%

Biomass14%

Hydraulic and Electricity

15%

Natural Gas9%

Coal5%

Uranium1%

Oil and Oil oducts

Oil and Oil Products

35%

Coal24%

Natural Gas21%

Hydraulic and Electricity2%

Uranium6%

Biomass11%

Share of renewable energy in the total primary energy: 47%

WorldBrazil

43

TOP PRODUCTS HIGHLIGHTS

Flex-fuel Cars – Evolution

0

50

1.0

1.5

2.0

2.5

3.0

3.5

0

50

1.0

1.5

2.0

2.5

3.0

3.5

2004 20052006

20072008

2009

GASOLINE

FLEX FUEL

ETHANOL

DIESEL3.193.222.98

2.612.532.31

Mill

ion

units

source: anfaveaelaboration: Ministry of agriculture

Flex-fuel technology allows the use of gasoline, ethanol or its mixture at any proportion. Currently, more than 10 million cars in Brazil have fl ex-fuel engines. Ethanol is also being used as fuel for Formula Indy competition cars, as well as trucks and airplanes.

Cof fee

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

46

4.0

39.1

2.1

3.4

50

Million ha

Mill

ion

sack

s

45

40

35

25

20

15

10

5

0

1990

/91

1991

/92

1992

/93

1993

/94

1994

/95

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10(E

)

30

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

31.0

Area Production

Coffee: Production and area

Brazil is the world’s leading exporter of coffee. Over the last 20 years, investment on technology has increased production by 26%, while area has decreased by 38%.

sources: usda , embrapa and national food supply company (as of 1996)elaboration: Ministry of agriculture

47

TOP PRODUCTS HIGHLIGHTS

Total: uS$ 3.7 billion

Coffee Exportsmain Destinations

EU-2757.1%

USA19.2%

Japan7.7%

Canada1.6%

Argentina1.5%

Syria1.4%

Others11.5%

Brazil exports mainly arabic coffee. Europe is its main market. yet, under different brands and presentations, the Brazilian coffee can be savored by consumers all over the world.

source: Ministry of development, industry and foreign trade – 2009 elaboration: Ministry of agriculture

milk

49

TOP PRODUCTS HIGHLIGHTS

Mill

ion

tons

+ 99 % (1990-08)

1991

30

25

20

15

10

5

01990 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

milk Production

source: Milk national forum – Brazilian confederation of agriculture and livestock

The increasing milk production in Brazil made the country self-suffi cient and exporter of dairy products.

Frui ts

51

TOP PRODUCTS HIGHLIGHTS

FruitsBrazil’s Production and ranking in the World

0

2

4

6

8

10

12

14

16

18

201st

1st

4th

4th

15th7th 11th 3rd

Mill

ion

tons

OrangeBanana Coconut Papaya Grape

AppleMangoTagerine

0

2

4

6

8

10

12

14

16

18

201st

1st

4th

4th

15th7th 11th 3rd

OrangeBanana Coconut Papaya Grape

AppleMangoTagerine

Brazilian climate diversity allows the production of several types of fruits in distinctive regions of the country. It is also possible to produce in different seasons of the year.

source: iBraf - 2009elaboration: Ministry of agriculture

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

52

PAPAYA

PEAR

GRAPE

PAPAYA

AVOCADO

PINEAPPLE

BANANA

PERSIMMON

CASHEW NUTS

COCONUT

CUPUAÇU

FIGS

STONE FRUITS

GUAVA

KIWI

ORANGE AND TANGERINE

LIME

APPLE

MANGO

PASSION FRUIT

MELLON AND WATERMERLON

BLUEBERRY

STRAWBERRY

AÇAI

Fruits – Production map

SuSTaINaBILITy aGrICuLTurE & ENVIrONmENT

55

SUSTAINABILITY AGRICULTURE & ENVIRONMENTBrazil is a big exporter of wood, wood products and celulosis. It has leadership in the hardwood pulp market.

Wood and paper industries in Brazil are based on planted forests.

source: aBrafelaboration: Ministry of agriculture

(Mill

ion

ha)

5.0

6.3

0

1

2

3

4

5

6

7

8

9

10

2004 2005 2006 2007 2008 2009

Forestry Planted area

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

56

• Brazil has the largest extension of arable lands of the world;

• Brazil contains the greatest diversity of ecosystems and unique biodiversity;

• Brazilian legislation protects preserved areas of all biomes.

Legal restrictions to Land utilization

Region Legal ReserveLand Available for

economical use

Amazon Forest 80% 20%

Savannas neighboring Amazon 35% 65%

Other areas 20% 80%

Moreover, it is mandatory to preserve river banks, areas around lagoons, lakes or water reservoirs, peaks, among others.

amazon rain Forest Our Greatest Treasure

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

58

No tillage system is a way of growing crops without disturbing the soil through ploughing. It has increased fast in Brazil and is largely used in grain production.

• reduces labor and machinery requirements

• saves fuel

• reduces soil erosion

• improves water retention and quality

• reduces release of carbon gases

• long - term productivity improvements

GrainPlanted area

No Tillage Systemmain advantages

No tillage69%

Conventional31%

source: national company of food supply – 2008/09

59

SUSTAINABILITY AGRICULTURE & ENVIRONMENT

Good agricultural Practices

• Use of varieties adapted to local soil and climate conditions;

• Integrated crop-livestock-forestry production systems;

• No Tillage System (saves energy, controls erosion);

• Use of clean energy sources:

• agrienergy: biofuels, biodigesters, wind and solar energy;

• Use of alternative techniques that dispense agricultural chemicals (biological control and integrated pest management);

• Adoption of micro basins as the basic planning units for rural land use.

FOrEIGN INVESTmENT OPPOrTuNITIES

61

FOREIGN INVESTMENT OPPORTUNITIES

Global Trends

World population growth with increasing per capita income

Increasing demand for higher-quality, better, protein-intensive food (i.e.meat)

Continuous need of food production increase

Shortage of new lands for agricultural production

Challenges to food security

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

62

Brazilian agribusinessCompetitive advantages

• Strong, thriving economy & institutional framework;

• Leadership in tropical technology;

• Abundance of natural resources (land, water, solar energy);

• Farming vocation combined with business entrepreneurship.

63

FOREIGN INVESTMENT OPPORTUNITIES

Producer Support Estimate(Public Support to Farmers)

OECD shows that Brazilian governmental subsidies to farmers are among the smallests vis-a-vis other countries. Brazil’s competitiveness in the international arena is due to a combination of the country’s natural resources, investments on r&D and private entrepreneurship initiatives.

source: organization for economic cooperation and development

1%5% 6%

9%14%12%14%

21%26%

30%

50%

NewZeland Brazil

MexicoRussia

OECDJapan

AustraliaChina

USACanada

EU

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

64

Strong, Thriving Economy &Institutional Framework

New social and economic paradigms, with:

• Social inclusion and income distribution;

• Upgrowth of the middle class, ensuring solid and diversifi ed domestic demand;

• Investment enhancement;

• Stable, consolidated democracy, legal and institutional framework;

• Infrastructure long-term investment program with strategic actions;

• Sustainable growth based on macroeconomic prudential policies;

• Infl ation under control (effi cient infl ation target regime);

• Robust fi scal rules (primary surplus & continuous reduction of public defi cit);

• Low external vulnerability.

65

FOREIGN INVESTMENT OPPORTUNITIES

Source: Exame Infrastructure Yearbood 2009-2010Produced by: Ministry of Finance

7.5

5.2

2.5

1.2

2.2

0.5

Investment in US$ billion

Santo AntônioHydroeletric

Power Plant (PPP)*

New Trans-NortheasternRailway (PPP)

São Francisco RiverInterchange

(Public)

Port of Açu(Private) Oil

Platforms (PPP)

Angra 3Nuclear Power Plant (PPP)Comperj (PPP)

Port of Santos(PPP)

Metropolitan São PauloRodoanel

(South Portion)(Public)São Paulo

Subway (PPP)

BR 101 Highway(Northeast andSouth Portions)

(Public)

North-SouthRailway

(South Portion)

North-SouthRailway

(North Portion)(PPP)

To be concluded in 2010Estimated conclusion in the coming yearsPPP = Public-Private Partnership*Includes public-private partnerships and concessions

East-WestRailway

Cacimbas-CatuGas Pipeline

(PPP)

TucuruiLock

(Public)Belo MonteHydroeletricPower Plant

Jirau HydroeletricPower Plant (PPP)*

Bullet Train12.8

2.8

3.6 20.0

10.7 4.7

2.9

1.1

7.0

3.4

10.6

1.7

2.0

accelerated Growth ProgrammeInfrastructure to Come

BRAZ

ILIAN

AGRIB

USIN

ESS

AT A

GLAN

CE

66

Leadership in Tropical Technology

• Continuous & persistent public and private investments on R&D;

• Opened partnerships with other countries;

• Expressive results on productivity;

• Effi cient use of natural resources.

67

FOREIGN INVESTMENT OPPORTUNITIES

Foreign Investment in agribusiness

The agribusiness productive chains offer several possibilities for foreign investors:

• Direct Investment on Projects (Transportation, Storage, Harbourage);

• Contract Farming (Payment in Products );

• Capital Markets (Stocks, Investment Funds );

• Partnerships and Joint Ventures.

Production

Machinery and Equipments

Infrastructure

Logistics

Food Processing

Distribution