epic research special report of 05 oct 2015

TRANSCRIPT

DAILY REPORT

05th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance

Japanese stocks ended flat in thin trade on Friday as inves-

tors were reluctant to take large positions before a key U.S.

jobs report due later in the day. The Nikkei share average

edged up 0.02 % to 17,725.13. For the week, it dropped 0.9

%, falling for the third straight week. The broader Topix

dropped 0.2 % to 1,444.92, with 1.887 billion shares chang-

ing hands, the lowest level since Sept. 14. The JPX-Nikkei

Index 400 fell 0.1 % to 12,927.84. Markets in China remain

closed until Wednesday for National Day holidays.

US stocks closed more than 1 percent higher following the

report, with major averages ending the week up more than

1 percent.

European shares closed higher on Friday, as firmer utility

stocks and gains on the Lisbon bourse before weekend

elections in Portugal propped up markets in spite of weak

U.S. jobs data. The pan-European FTSEurofirst 300 index

closed up 0.5 %, while the euro zone's blue-chip Euro

STOXX 50 index finished 0.6 % higher. Portugal's PSI-20 in-

dex was the best-performing market in Europe, climbing

2.1 % as Portugal's prime minister made a final push on

Friday to boost his chances of not only winning this week-

end's election but also of securing an absolute majority and

a more stable government.

Previous day Roundup

The BSE Sensex relinquished most of its gains to close mar-

ginally higher at 26227 and the Nifty ended marginally

down at 7946.10. The BSE midcap and smallcap index were

far more robust unlike their larger peers. However, the in-

dices closed marginally higher. For most part of the day the

larger market traded flat-to-positive although it opened by

testing the 8000 level as overnight US stocks ended higher.

Lupin closed the day top grosser on the Sensex with over 4

% gains. Other contributors to the 30-stock index were

Infosys, Reliance, Larsen and TCS.

Index stats

The Market was very volatile in last session. The sartorial

indices performed as follow; Consumer Durables [down

pts], Capital Goods [up 110.89pts], PSU [down 6.97pts],

FMCG [up 18.23pts], Realty [down 25.41pts], Power [down

10.21pts], Auto [down 78.81Pts], Healthcare [up

260.11Pts], IT [down 27.25pts], Metals [down 8.32pts],

TECK [up 15.30pts], Oil& Gas [up 8.91pts].

World Indices

Index Value % Change

D J l 16472.37 +1.23

S&P 500 1951.36 +1.43

NASDAQ 4707.77 +1.74

FTSE 100 6129.98 +0.95

Nikkei 225 17941.62 +1.22

Hong Kong 21892.04 +1.79

Top Gainers

Company CMP Change % Chg

ULTRACEMCO 2,776.00 102.60 3.84

LUPIN 2,099.10 65.10 3.20

ZEEL 401.55 9.10 2.32

SUNPHARMA 888.20 19.80 2.28

ADANIPORTS 305.35 6.35 2.12

Top Losers

Company CMP Change % Chg

HCLTECH 859.00 123.15 -12.54

BHEL 198.80 6.75 -3.28

GAIL 293.50 8.80 -2.91

MARUTI 4,579.00 106.60 -2.28

VEDL 83.45 1.25 -1.48

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

AARTIIND 560.00 9.75 1.77

DISHMAN 353.80 34.10 10.67

INFY 1,173.05 11.10 0.96

LUPIN 2,099.10 65.10 3.20

GMBREW 488.30 -2.35 -0.48

Indian Indices

Company CMP Change % Chg

NIFTY 7950.90 2.00 +0.03

SENSEX 26220.95 +66.12 +0.25

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

GUJGASLTD 484.00 -34.60 -6.67

IDFC 60.80 -8.35 -12.08

ADLABS 110.00 -2.15 -1.92

TITAN 327.50 9.65 3.04

DAILY REPORT

05th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

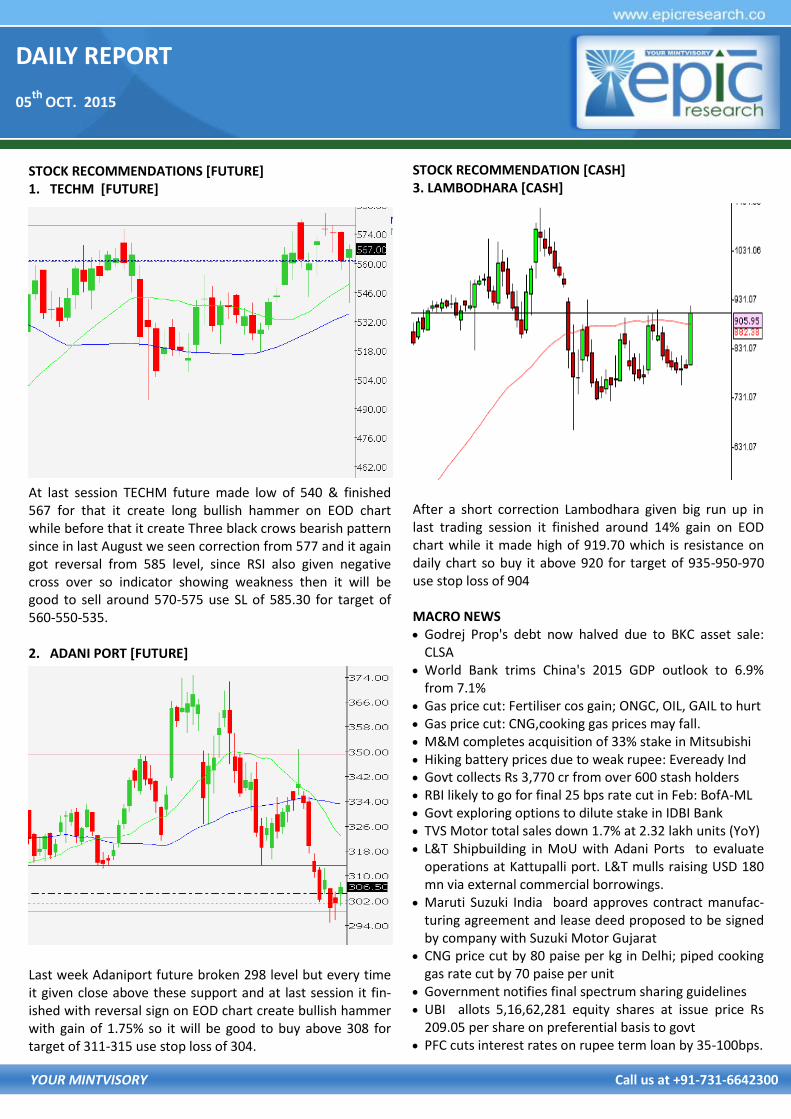

STOCK RECOMMENDATION [CASH] 3. LAMBODHARA [CASH]

After a short correction Lambodhara given big run up in last trading session it finished around 14% gain on EOD chart while it made high of 919.70 which is resistance on daily chart so buy it above 920 for target of 935-950-970 use stop loss of 904 MACRO NEWS Godrej Prop's debt now halved due to BKC asset sale:

CLSA World Bank trims China's 2015 GDP outlook to 6.9%

from 7.1% Gas price cut: Fertiliser cos gain; ONGC, OIL, GAIL to hurt Gas price cut: CNG,cooking gas prices may fall. M&M completes acquisition of 33% stake in Mitsubishi Hiking battery prices due to weak rupee: Eveready Ind Govt collects Rs 3,770 cr from over 600 stash holders RBI likely to go for final 25 bps rate cut in Feb: BofA-ML Govt exploring options to dilute stake in IDBI Bank TVS Motor total sales down 1.7% at 2.32 lakh units (YoY) L&T Shipbuilding in MoU with Adani Ports to evaluate

operations at Kattupalli port. L&T mulls raising USD 180 mn via external commercial borrowings.

Maruti Suzuki India board approves contract manufac-turing agreement and lease deed proposed to be signed by company with Suzuki Motor Gujarat

CNG price cut by 80 paise per kg in Delhi; piped cooking gas rate cut by 70 paise per unit

Government notifies final spectrum sharing guidelines UBI allots 5,16,62,281 equity shares at issue price Rs

209.05 per share on preferential basis to govt PFC cuts interest rates on rupee term loan by 35-100bps.

STOCK RECOMMENDATIONS [FUTURE] 1. TECHM [FUTURE]

At last session TECHM future made low of 540 & finished 567 for that it create long bullish hammer on EOD chart while before that it create Three black crows bearish pattern since in last August we seen correction from 577 and it again got reversal from 585 level, since RSI also given negative cross over so indicator showing weakness then it will be good to sell around 570-575 use SL of 585.30 for target of 560-550-535. 2. ADANI PORT [FUTURE]

Last week Adaniport future broken 298 level but every time it given close above these support and at last session it fin-ished with reversal sign on EOD chart create bullish hammer with gain of 1.75% so it will be good to buy above 308 for target of 311-315 use stop loss of 304.

DAILY REPORT

05th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 8,200 55.90 4,46,824 41,67,100

NIFTY CE 8,000 141.00 3,77,660 46,22,800

BANKNIFTY CE 18,000 188.00 47,945 6,13,800

IDFC CE 70 0.95 10,719 45,40,000

IDFC CE 75 0.40 8,647 27,54,000

LT CE 1,500 47.50 5,663 2,09,625

HCLTECH CE 900 24.00 4,047 2,75,000

SBIN CE 250 4.50 3,925 34,43,000

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 7,800 96.00 3,52,548 39,19,025

NIFTY PE 7,900 126.90 3,19,799 22,33,450

BANKNIFTY PE 16,500 232.00 25,061 3,10,700

IDFC PE 60 2.95 5,325 14,96,000

RELIANCE PE 840 14.10 2,407 4,24,250

LT PE 1,450 31.40 2,322 1,35,375

INFY PE 1,100 21.30 1,819 2,69,000

HCLTECH PE 860 40.00 1,734 94,250

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 100685 2163.15 53304 1199.49 803434 17915 963.6611

INDEX OPTIONS 423159 9893.77 428954 9870.96 1922747 60142.5 22.8085

STOCK FUTURES 85657 2265.14 95627 2395.71 1783689 44988.2 -130.573

STOCK OPTIONS 53493 1351.13 54063 1371.19 60218 1566.96 -20.0593

TOTAL 835.83

STOCKS IN NEWS Allahabad Bank, SBBJ, Yes Bank and Kotak Mahindra

Bank cut base rate by 0.25 per cent Govt infuses Rs 13,955 crore capital into 8 PSU banks IDBI Bank cuts base rate by 0.25% to 9.75% Repo rate cut, a major relief for textile industry: SIMA GCIL builds Rs 800-crore transmission line linking West

Bengal, Bihar Sterlite Grid, Burns & McDonnell tie up for implement-

ing transmission projects NIFTY FUTURE

Nifty Future in yesterday trading session opened higher and came down immediately in first few hours and for the rest of the day it remained flat to negative. For next session we advise to buy Nifty for RSI and weekly close suggest a little upside, atleast upto 8150. So Buy it around 7950-7960 for the targets of 8070-8170 with strict stop loss of 7750

INDICES R2 R1 PIVOT S1 S2

NIFTY 8,040.00 7,995.00 7,962.00 7,917.00 7,884.00

BANK NIFTY 17,497.00 17,323.00 17,217.00 17043.00 16,937.00

DAILY REPORT

05th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

GOLD

TRADING STRATEGY:

BUY GOLD OCT ABOVE 26500 TGTS 26580,26670 SL BE-

LOW 26400

SELL GOLD OCT BELOW 26200 TGTS 25620,25530 SL

ABOVE 25800

SILVER

TRADING STRATEGY:

BUY SILVER DEC ABOVE 35100 TGTS 35300,35600 SL BE-

LOW 34800

SELL SILVER DEC BELOW 34700 TGTS 34500,34200 SL

ABOVE 35000

COMMODITY ROUNDUP

A promising spurt was witnessed in gold on 2nd October 2015 as the US nonfarm payrolls came in less than ex-pected. Strong physical demand for gold from major con-suming nations also supported the yellow metal. Gold is expected to seek cues from the US economy in the near term and unenthusiastic economic data can offer good sup-port to the yellow metal. Global growth outlook is likely to be revised down due to weak expansion in emerging econo-mies. COMEX Gold hit a one month high of $1156 per ounce, breaking above the 100 day EMA. However, contin-ued selling pressure in global crude oil prices and a modest recovery in global equities pulled gold back.

WTI crude oil futures continued to witness bargain buying in dips amid supportive Chinese and US consumer confidence data. The WTI crude futures continued to witness bargain buying around $44 per barrel mark while MCX Crude eyed Rs 3000 mark as a key pivot point. The latest US nonfarm payrolls data also supported oil. US consumers' outlook on US economy improved in September. The Conference Board, a private research group, said its index of consumer confidence increased to 103.0 in September from a revised 101.3 in August. The initial August reading was 101.5. The present situation index rose to 121.1from a 115.8. The ini-tial August reading was 115.1. Meanwhile, the board's con-sumer expectations for economic activity over the next six months dropped to 91.0 from a revised91.6.

Silver futures moved in tune with the gold prices.MCX Silver futures for December extended a slide after testing highs near Rs 36700 per kg levels in the middle of last week and plummeted once Rs 36000 mark gave up. The counter tested lows near Rs 34400 per kg levels and should rise back towards Rs 35000 mark following the recovery in global prices. Global Silver futures recovered after witnessing con-tinued bargain buying around $14.40 per ounce levels. The metal could extend these gains provided global copper and crude oil prices also maintain their upsides.

The prices of major nonferrous are expected to remain dull and weak in the month of October 2015. So far the per-formance has remained far from being jovial and September was again a month of heavy losses in nonferrous metals compared to last year. The metal has been facing heat from the Chinese data that has dismantled the process of growth. Copper prices in September 2015 settled at $ 5208 per tonne, down 24% from last year. The prices were $ 6868 per tonne during same time last year.

DAILY REPORT

05th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

NCDEX ROUNDUP Cardamom prices rose by 0.40% to Rs 812 per kg in futures trade as speculators built up fresh positions after demand picked up in the spot market. At MCX cardamom for deliv-ery in October edged up by Rs 3.20, or 0.40%, to Rs 812 per kg in a business turnover of 129 lots. Similarly, the spice for delivery in Nov traded higher by 50 paise, or 0.06%, to Rs 833 per kg in 35 lots. Fresh positions built up by traders due to pick up in demand in the spot market amid restricted supplies from producing region mainly led to the rise in car-damom prices at futures trade. Chana prices jumped by 2.25% to Rs 4,912 per quintal in futures market as traders enlarged positions amid fall in supplies from producing belts at the spot market against rising demand. At NCDEX chana for delivery in Oct shot up by Rs 108, or 2.25%, to Rs 4,912 per quintal with OI of 13,670 lots. The commodity for delivery in November traded higher by Rs 93, or 1.89%, to Rs 5,026 per quintal in 87,590 lots. Speculators enlarged positions supported by rising demand in the spot market amid lower arrivals from producing belts which mainly influenced chana prices. Tea production in India is likely to fall this year according to the latest trend in production. Production is slated to fall after a gap of five years. Mentha oil remained higher for the second straight day and prices advanced by 0.23% to Rs 904.90 per kg in futures trade owing to rising demand from consuming industries in the spot market. Besides, tight stocks position in the physi-cal market on restricted arrivals from producing regions, supported the upside. At MCX mentha oil for delivery in Oct gained Rs 2.10, or 0.23%, to Rs 904.90 per kg in a business turnover of 203 lots.

NCDEX INDICES

Index Value % Change

CAETOR SEED 4108 -0.32

CHANA 4952 +3.08

CORIANDER 11182 -0.08

COTTON SEED 1593 +2.12

GUAR SEED 3836 +1.11

JEERA 15670 +0.10

MUSTARDSEED 4562 +3.26

REF. SOY OIL 605.75 +1.29

TURMERIC 7492 -0.08

WHEAT 1551 -0.19

RECOMMENDATIONS

DHANIYA

BUY CORIANDER OCT ABOVE 11350 TARGET 11377 11457

SL BELOW 11323

SELL CORIANDER OCT BELOW 11150 TARGET 11123 11043

SL ABOVE 11177

GUARSGUM

BUY GUARGUM OCT ABOVE 8300 TARGET 8350 8420 SL

BELOW 8240

SELL GUARGUM OCT BELOW 8180 TARGET 8130 8060 SL

ABOVE 8240

DAILY REPORT

05th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 65.5540 Yen-100 54.5400

Euro 73.0796 GBP 99.1701

CURRENCY

USD/INR

BUY USD/INR OCT ABOVE 65.9 TARGET 66.03 66.18 SL BE-

LOW 65.7

SELL USD/INR OCT BELOW 65.78 TARGET 65.65 65.5 SL

ABOVE 65.98

EUR/INR

BUY EUR/INR OCT ABOVE 73.6 TARGET 73.75 73.95 SL BE-

LOW 73.4

SELL EUR/INR OCT BELOW 73.2 TARGET 73.05 72.85 SL

ABOVE 73.4

CURRENCY MARKET UPDATES:

The rupee extended gains for the fourth straight day against the US currency Thursday, advancing by 7 paise to close at 65.51 per dollar on selling of dollar by banks and exporters on hopes of more foreign capital inflows into equity market. FPIs net bought shares worth Rs 116.08 cr yesterday, as per the provisional figures issued by stock exchanges. The rupee resumed steady at 65.58 per dollar at the Interbank Forex market in view of cautious ap-proach. It moved in a range of 65.48 per dollar and 65.67 per dollar before ending at 65.51 per dollar, showing a gain of seven paise or 0.11%. It has gained 65 paise or 0.98 per-cent in the last four sessions. The rupee hardened further against the pound sterling to finish at 99.23 from yester-day's close of 99.58 and also firmed up further against the Euro to 73.09 from 73.51. However, it dropped against the Japanese currency to settle at 54.71 per 100 yen from 54.52 yesterday.

The concept of rupee-denominated bonds or “masala bonds” seems to be gaining currency, aided in good meas-ure by rupee bond offerings made by the International Fi-nance Corporation. IFC, an arm of the World Bank and a major global financial institution that fosters private sector development in developing countries, has seen its rupee-denominated borrowing in international markets during fiscal 2015.

The dollar nursed losses on Monday, edging away from a nearly two-week low against a basket of currencies marked in the previous session after weak U.S. jobs data led trad-ers to pare bets that the Federal Reserve was poised to hike interest rates as early as this month. The key nonfarm payrolls report showed that employers added only 142,000 jobs last month, falling far short of economists' consensus expectation for a rise of 203,000 jobs, according to a Reuters poll. Moreover, the August figures were revised sharply lower. That raised doubts that the U.S. economy was strong enough to justify the Fed's long-awaited inter-est rate increase, which would be the first since 2006.

The dollar index .DXY slid to 95.218, its lowest level since Sept. 21. It last stood at 95.887, up about 0.1 percent.

DAILY REPORT

05th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

CALL REPORT

PERFORMANCE UPDATES

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

01/10/15 NCDEX DHANIYA OCT. BUY 8200 8250-8320 8140 SL TRIGGERED

01/10/15 NCDEX DHANIYA OCT. SELL 8130 8080-8010 8190 NOT EXECUTED

01/10/15 NCDEX GUARGUM OCT. BUY 11277 11304-11384 11250 BOOKED FULL PROFIT

01/10/15 NCDEX GUARGUM OCT. SELL 11160 11133-11053 11187 SL TRIGGERED

01/10/15 MCX GOLD OCT. BUY 26000 26080-26170 25900 BOOKED PROFIT

01/10/15 MCX GOLD OCT. SELL 25700 25620-25530 25800 NOT EXECUTED

01/10/15 MCX SILVER DEC. BUY 34700 34900-35200 34700 NP PROFIT NO LOSS

01/10/15 MCX SILVER DEC. SELL 34400 34200-33900 34700 NOT EXECUTED

01/10/15 USD/INR OCT. BUY 65.95 66.08-66.23 65.75 NOT EXECUTED

01/10/15 USD/INR OCT. SELL 66.86 66.73-66.58 67.06 NOT EXECUTED

01/10/15 EUR/INR OCT. BUY 73.90 74.05-74.25 73.70 NOT EXECUTED

01/10/15 EUR/INR OCT. SELL 73.80 73.65-73.45 74.00 BOOKED FULL PROFIT

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

01/10/15 NIFTY FUTURE SELL 7990-8000 7890-7750 8200 NO PROFIT NO LOSS

01/10/15 TECHM FUTURE SELL 570-575 560-550-535 585.30 NOT EXECUTED

01/10/15 SKSMICRO FUTURE BUY 413 419-427-435 406 BOOKED PROFIT

01/10/15 JUBILANT CASH BUY 389 394-400-410 384 NOT EXECUTED

30/09/15 NIFTY FUTURE SELL 7950 7850-7750 8200 NO PROFIT NO LOSS

DAILY REPORT

05th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any responsibility (or

liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere efforts have been made to present the

right investment perspective. The information contained herein is based on analysis and up on sources that we consider reliable. This material is for per-

sonal information and based upon it & takes no responsibility. The information given herein should be treated as only factor, while making investment

decision. The report does not provide individually tailor-made investment advice. Epic research recommends that investors independently evaluate par-

ticular investments and strategies, and encourages investors to seek the advice of a financial adviser. Epic research shall not be responsible for any trans-

action conducted based on the information given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projec-

tions shown are not necessarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change

without notice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone who is

browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either the site or its owners

or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this disclaimer. All Rights Reserved. Investment

in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the completeness thereof. We are not responsible for any

loss incurred whatsoever for any financial profits or loss which may arise from the recommendations above epic research does not purport to be an invi-

tation or an offer to buy or sell any financial instrument. Our Clients (Paid or Unpaid), any third party or anyone else have no rights to forward or share

our calls or SMS or Report or Any Information Provided by us to/with anyone which is received directly or indirectly by them. If found so then Serious

Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, OCT. 05

10 AM ISM NONMANUFACTURING INDEX SEPT. 57.5% 59.0%

TUESDAY, OCT. 06

8:30 AM TRADE DEFICIT AUG. -$48.1 BLN -$41.9 BLN

WEDNESDAY, OCT. 07

3 PM CONSUMER CREDIT AUG. -- $19 BLN

THURSDAY, OCT. 08

8:30 AM WEEKLY JOBLESS CLAIMS OCT. 3 271,000 277,000

2 PM FOMC MINUTES SEPT. 17

FRIDAY, OCT. 09

8:30 AM IMPORT PRICE INDEX SEPT. -- -1.8%

10 AM WHOLESALE INVENTORIES AUG. -- -0.1%