epic research special report of 29 oct 2015

TRANSCRIPT

DAILY REPORT

29th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance European shares ended higher yesrterday as energy stocks rose on the back of a crude oil price rally. The FTSEurofirst 300 closed up 1%, recouping entirely Tuesday's decline. The euro zone's blue-chip Euro STOXX 50 index rose 1.19%. Expectations that the ECB will expand its asset purchases in Dec., combined with a rate cut in China, helped the FTSEurofirst 300 to 2-month highs at the end of last week. Asian stocks mostly advanced on Thursday, encouraged by a stronger finish on Wall Street following the Fed's decision to leave interest rates near zero. Major US averages surged more than 1% overnight, after the Fed kept rates un-changed but signaled that a Dec rate hike was still on the table. The Nasdaq led gains with a 1.3% rise, while DJI Aver-age and S&P 500 closed up 1.1 and 1.2% respectively. Ja-pan's Nikkei 225 index extended gains following the release of Sept industrial output, which suggested that the world's third-biggest economy is embarking on a recovery. US stocks ended sharply higher on Wednesday after a vola-tile session as the Fed gave a vote of confidence in the US economy by signaling a Dec interest rate hike was still on the table. S&P financials, which benefit from higher bor-rowing rates, shot up following the Fed statement and led sector gains. The financial index ended up 2.4%, its biggest percentage gain in seven weeks. The S&P 500 posted 35 new 52-week highs and six new lows; the Nasdaq recorded 155 new highs and 82 new lows. About 8.5 bn shares changed hands on US exchanges. Previous day Roundup The market remained under selling pressure, dragged by banking & financials, pharma and infra stocks. Indian shares extended their losses for a 3rd consecutive session as investors remained cautious about the expiry of monthly derivatives contracts back home this week. The BSE index ended 0.78% lower. Earlier in the session, the index hit a low of 26,919.96, its lowest intraday level since Oct. 16. The NSE index ended down 0.75% after hitting a low of 8,131.80, its lowest intra day level since Oct. 15. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [up 189.20pts], Capital Goods [down 60.22pts], PSU [down 52.89pts], FMCG [down 2.11Pts], Realty [down 17.52pts], Power [down 28.94pts], Auto [down 120.77Pts], Healthcare [down 90.50Pts], IT [up 40.51pts], Metals [down 4.11 pts], TECK [up 22.96pts], Oil& Gas [down 38.02pts].

World Indices

Index Value % Change

D J l 17779.52 +1.13

S&P 500 2090.35 +1.18

NASDAQ 5096.69 +1.30

FTSE 100 6437.80 +1.14

Nikkei 225 18885.91 -0.09

Hong Kong 22920.61 -0.16

Top Gainers

Company CMP Change % Chg

CIPLA 701.95 17.25 2.52

KOTAKBANK 673.30 12.85 1.95

TECHM 548.95 10.15 1.88

AMBUJACEM 208.55 3.15 1.53

ONGC 251.40 3.50 1.41

Top Losers

Company CMP Change % Chg

AXISBANK 484.25 37.55 -7.20

ICICIBANK 272.85 10.85 -3.82

ADANIPORTS 301.20 10.10 -3.24

INDUSINDBK 923.50 30.50 -3.20

YESBANK 728.75 22.55 -3.00

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

AUROPHARMA 858.00 11.90 1.41

GMBREW 607.50 28.65 4.95

JUBILANT 407.00 -17.85 -4.20

IDBI 86.45 0.20 0.23

RUSHIL 290.50 -1.05 -0.36

Indian Indices

Company CMP Change % Chg

NIFTY 8171.20 -61.70 -0.75

SENSEX 27039.76 -213.68 -0.78

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

IDFC 59.45 -0.10 -0.17

KIRLOSBROS 185.00 8.25 4.67

M&MFIN 224.70 -4.95 -2.16

OIL 401.90 -6.25 -1.53

DAILY REPORT

29th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATION [CASH] 3. COX&KINGS [CASH]

COX&KINGS given breakout above 256 it finished with 2.30% gain since RSI also has positive divergence and vol-ume is continuously rising with gains on DMA also near to positive cross over so we advise to buy it above 260 for target of 264 269 275 use stop loss of 255 MACRO NEWS Results: DRL, BharatForge, NTPC, Glenmark, BEL, Emami,

GRASIM, MRF, YesBank, Torrent Pharma, Nestle, Jubilant Life, Shriram Transport, Thomas Cook, Gujarat Pipavav Port, Dishman Pharma, Crompton Greaves, Colgate Pal-molive, Alstom T&D India, GIC Housing, HCC, Heidel-bergCement, ITDC, IFCI, MRPL, Muthoot Finance, Polaris Consulting, Praj Ind, Redington, Sequent, RPG Life Sci-ences, R Systems Int, Firstsource Solutions, Essel

Ambuja Cement Q3 Net Profit Down 35.7% At `153.6 Cr (YoY) Total Income Down 4.2% At `2,110.9 Cr (YoY)

Dabur Q2 net up 19% at Rs 341 cr, input costs aid mar-gins

Petronet faces Rs 10,000 cr hit on costly RasGas contract CBI registers case against REI Agro for causing an alleged

loss to banks CEAT's Q2 consolidated net profit up 30.5 percent at Rs

107.4 crore versus Rs 82.3 crore Deepak Nitrite bags annual contract to supply an agro

intermediate to Bayer Crop Siemens arm leases 3.5 lakh square feet at Cummin India

Campus in Pune for over Rs 25 crore annual rent Mastek bags multi-year contract from National Credit

Guarantee Trustee Co Amara Raja Batteries posted 23% rise in consolidated net

profit at Rs 123cr for the second quarter CCI Imposes `666 Cr Penalty On JP Assoc For Unfair

Trade Practices

STOCK RECOMMENDATIONS [FUTURE] 1. HAVELLS [FUTURE]

HAVELLS Future end with minor loss but it create inverted hammer on daily chart, at last session it made high of 260.35 which is trend line resistance while at down side it has sup-port at 254 so we can see range bound trade in up coming session so we advise to sell it around 258-259 use stop loss of 263 for target of 255 251 246.

2. IBREALEST [FUTURE]

IBREALEST FUTURE given breakdown of channel line pattern in last session it got resistance near to supported channel line while on RSI it has negative divergence while we see on daily chart below 62.50 it may give reverse flag pattern breakdown so sell it around 65-66 use stop loss of 67.60 for target of 63 61 59.

DAILY REPORT

29th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 8,200 22.55 18,06,267 43,33,900

NIFTY CE 8,250 6.30 8,08,942 18,04,150

BANKNIFTY CE 18,000 3.00 1,16,738 8,29,600

AXISBANK CE 490 3.05 8,037 7,81,000

RELIANCE CE 940 4.35 7,887 4,08,750

MARUTI CE 4,600 3.00 7,201 2,14,750

LUPIN CE 1,950 7.00 5,552 81,000

SBIN CE 250 0.35 5,034 38,54,000

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 8,200 36.60 14,91,801 30,98,800

NIFTY PE 8,100 8.60 14,78,141 45,46,550

BANKNIFTY PE 17,500 132.85 1,42,917 4,48,725

AXIABNAK PE 480 3.25 8,575 7,37,000

LUPIN PE 1,900 9.00 7,334 3,83,375

RELIANCE PE 940 5.50 4,911 4,84,500

MARUTI PE 4,500 28.00 4,366 77,750

AXISBANK PE 490 8.00 3,707 2,27,000

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 187170 7035.7 302109 8316.77 760221 26725.9 -1281.06

INDEX OPTIONS 627950 18192.7 621205 17406.8 2179801 74159.7 785.9018

STOCK FUTURES 476401 16813.7 512236 18128.7 1293125 52069.3 -1314.98

STOCK OPTIONS 75576 2175.85 79833 2267.38 144233 3923.59 -91.5261

TOTAL -1901.66

STOCKS IN NEWS Idea looking to buy Videocon's spectrum in 6 circles

Axis Bank tanks 7% on asset quality

Indigo's Rs 3018-cr IPO fully subscribed

Syndicate Bank Q2 profit up 5%; tax cost hurts, NPA rises

Hero aims to sell 6 lakh two-wheelers in October

Opto Circuits US arm files for bankruptcy to facilitate debt restructuring

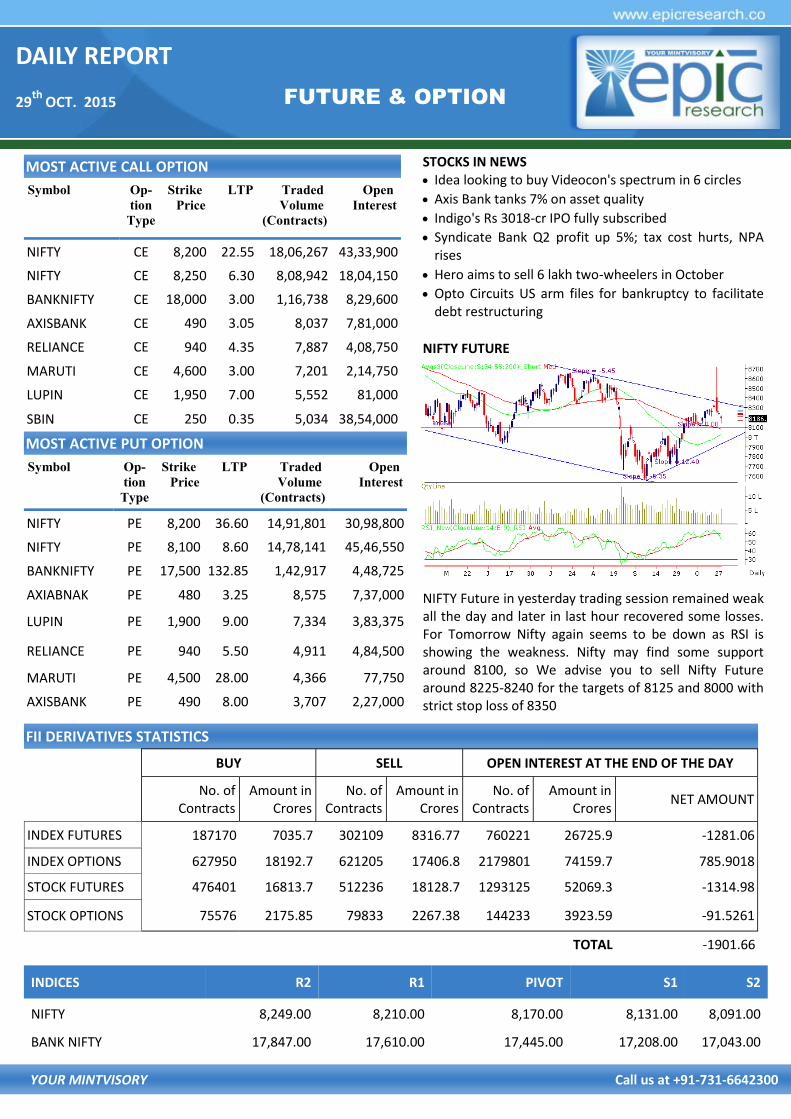

NIFTY FUTURE

NIFTY Future in yesterday trading session remained weak all the day and later in last hour recovered some losses. For Tomorrow Nifty again seems to be down as RSI is showing the weakness. Nifty may find some support around 8100, so We advise you to sell Nifty Future around 8225-8240 for the targets of 8125 and 8000 with strict stop loss of 8350

INDICES R2 R1 PIVOT S1 S2

NIFTY 8,249.00 8,210.00 8,170.00 8,131.00 8,091.00

BANK NIFTY 17,847.00 17,610.00 17,445.00 17,208.00 17,043.00

DAILY REPORT

29th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

GOLD

TRADING STRATEGY:

BUY GOLD DEC ABOVE 27100 TGTS 27180,27270 SL BE-

LOW 26900

SELL GOLD DEC BELOW 26900 TGTS 26820,26730 SL

ABOVE 27100

SILVER

TRADING STRATEGY:

BUY SILVER DEC ABOVE 37100 TGTS 37300,37600 SL BE-

LOW 37800

SELL SILVER DEC BELOW 36800 TGTS 36600,36300 SL

ABOVE 37100

COMMODITY ROUNDUP Gold gained today after moving in a narrow range earlier this week. The yellow metal remained well bid on strong Chinese gold import data and ideas that Indian retail de-mand would remain firm ahead of the peak festive season. Slight weakness in the US dollar, which eased after hitting a two month high against the Euro also benefitted Gold. In-vestors are contemplating whether US Federal Reserve might refrain from raising rates on Wednesday. COMEX Gold is quoting at $1174 per ounce, up 0.72% on the day. MCX Gold futures are trading at Rs 27035 per 10 grams, up 0.41% on the day. Gold speculator and large futures traders sharply increased their gold bullish positions last week, MCX SILVERM Nov contract was trading at Rs 37205 up Rs 131, or 0.35 percent. The SILVERM rate touched an intraday high of Rs 37265 and an intraday low of Rs 37101. So far 5845 contracts have been traded. SILVERM prices have moved down Rs 5855, or 13.6% in November series so far. MCX SILVERM February contract was trading at Rs 37911 up Rs 131, or 0.35 percent. The SILVERM rate touched an intra-day high of Rs 37940 and an intraday low of Rs 37801. So far 157 contracts have been traded. SILVERM prices have moved up Rs 410, or 1.09% in the Feb series so far Copper futures fell to a one-week low on Wednesday, as persistent worries about future demand from top consumer China weighed. Copper for December delivery on the Comex division of the NYMEX shed 1.1 cents, or 0.45%, to trade at $2.351 a pound during morning hours in London. Meanwhile, mining major Antofagasta reported that Group copper production for the first nine months of the year was at 460,400 tonnes was 11.0% lower than in the same period last year. Q3 Copper production of 157,000 tonnes, in line with the previous quarter, despite lower grades and recov-eries at Centinela Concentrates. MCX Copper was trading at Rs 340.70 per kg, down 0.39%. The prices tested a high of Rs 341.85 per kg and a low of Rs 338.75 per kg. Zinc prices moved down 0.27% to Rs 112.10 per kg in fu-tures market today largely in tandem with a weak global trend. In futures trading at the MCX, zinc for delivery in Oc-tober contracts shed 30 paise, or 0.27%, to Rs 112.10 per kg, in a business turnover of 769 lots. Nickel futures eased 0.42% to Rs 690 per kg today as partici-pants reduced their exposure amid a weak trend overseas. At Multi Commodity Exchange, nickel for delivery in Novem-ber fell Rs 2.90, or 0.42%, to Rs 690 per kg in a business turnover of 583 lots.

DAILY REPORT

29th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

NCDEX ROUNDUP

Cardamom prices drifted 0.41% to Rs 793 per kg in futures trade as speculators booked profits at prevailing higher lev-els amid sluggish demand in the spot markets. At the MCX cardamom for delivery in Dec fell Rs 3.30, or 0.41%, to Rs 793 per kg in a business turnover of 21 lots. Similarly, the spice for delivery in Nov. traded lower by Rs 3.20, or 0.41%, to Rs 769.10 per kg in 139 lots. Apart from profit-booking by speculators, sluggish demand in the spot markets mainly kept pressure on cardamom prices at futures trade.

Buoyed by rising spot demand and restricted arrivals from producing belts, chana prices shot up by 1.61% to Rs 4,856 per quintal in futures trade as participants widened their positions. Also, covering-up of short positions by specula-tors supported the upside. At NCDEX chana for delivery in Dec month rebounded Rs 77 or 1.61% to Rs 4,856 per quin-tal with an OI of 54,660 lots. The Nov contract traded higher by Rs 72 or 1.53% to Rs 4,773 per quintal in 32,100 lots. The recovery in chana prices to increased positions built up by speculators driven by pick up in spot demand against re-stricted supplies from producing belts.

The price of rubber at home and abroad has continued to fall. On Wednesday, the Bangkok market, global headquar-ters of natural rubber (NR), quoted Rs 82 a kg for RSS-3 grade; SMR-20, preferred by importers, was Rs 77 a kg. Poor demand from major importing countries, especially of China, was the main reason. In India, the Rubber Board quotes Rs 114 a kg for the RSS-4 variety. Market sources say trading is at a much lower price of Rs 100 a kg. Experts point to two reasons, a drop in demand and the crash in crude oil prices, which drops the price of synthetic rubber.

NCDEX INDICES

Index Value % Change

CAETOR SEED 4255 +1.09

CHANA 4785 +1.79

CORIANDER 9175 -4.77

COTTON SEED 1678 -0.53

GUAR SEED 3885 +0.39

JEERA 15945 -0.34

MUSTARDSEED 4969 +0.28

REF. SOY OIL 624.3 +0.51

TURMERIC 2760 -0.47

WHEAT 8810 -1.54

RECOMMENDATIONS

DHANIYA

BUY CORIANDER NOV ABOVE 9300 TARGET 9335 9415 SL

BELOW 9251

SELL CORIANDER NOV BELOW 9057 TARGET 9022 8942 SL

ABOVE 9106

GUARSGUM

BUY GUARGUM NOV ABOVE 8240 TARGET 8290 8360 SL

BELOW 8180

SELL GUARGUM NOV BELOW 8040 TARGET 7990 7920 SL

ABOVE 8100

DAILY REPORT

29th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 65.0408 Yen-100 54.0100

Euro 71.7530 GBP 99.5840

CURRENCY

USD/INR

BUY USD/INR NOV ABOVE 65.41 TARGET 65.54 65.69 SL BE-

LOW 65.21

SELL USD/INR NOV BELOW 65.21 TARGET 65.08 64.93 SL

ABOVE 65.41

EUR/INR

BUY EUR/INR NOV ABOVE 72.42 TARGET 72.57 72.77 SL BE-

LOW 72.22

SELL EUR/INR NOV BELOW 72.15 TARGET 72 71.8 SL ABOVE

72.35

CURRENCY MARKET UPDATES: Snapping its two-day losing streak, the rupee today recov-ered by 4 paise to close at 64.93 per dollar on fag-end sell-ing of the American currency by banks and exporters amid lower greenback overseas. The rupee resumed lower at 65.07 per dollar as against the last closing level of 64.97 at the Interbank Foreign Exchange market and moved down further to 65.09 on initial dollar demand from banks and importers. However, it trimmed its initial losses against the dollar and recovered to 64.91 before settling at 64.93, showing a gain of four paise or 0.06%. It had dropped by 14 paise or 0.22% in the previous two days. It moved in a range of 64.91 and 65.09 per dollar during the day. The rupee firmed up further against the pound sterling to finish at 99.27 from 99.61 previously while moved down further against the euro to 71.88 from 71.82. The domestic currency ended higher against the Japanese currency at 53.94 per 100 yen from 54.02. The dollar index was trading lower by 0.19 per cent against a basket of six currencies in the late afternoon trade. The US dollar edged slightly lower against a basket of cur-rencies on Wednesday, but remained near the two month peak attained in the previous week. The dollar index, which measures the greenback's strength against a trade-weighted basket of six major currencies, was down 0.17% at 96.87, still close to Friday's two-month highs of 97.30. Investors continue to await the conclusion of the Federal Reserve's two-day policy meeting. The Fed was not ex-pected to raise interest rates later Wednesday, but many investors still expected the U.S. central bank to signal that rates could still rise at its Dec meeting. Meanwhile, the European unit edged up 0.13% to trade at 1.1059 versus the greenback. Sentiment on the single cur-rency remained fragile after European Central Bank Presi-dent Mario Draghi signaled that further monetary easing is likely later this year. As against the pound, dollar was steady with GBP/USD at 1.5296. The dollar was fractionally lower against the yen, with USD/JPY easing 0.09% to 120.35.

DAILY REPORT

29th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

CALL REPORT

PERFORMANCE UPDATES

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

28/10/15 NCDEX DHANIYA NOV. BUY 9850 9878-9958 9823 BOOKED FULL PROFIT

28/10/15 NCDEX DHANIYA NOV. SELL 9560 9532-9452 9587 BOOKED FULL PROFIT

28/10/15 NCDEX GUARGUM NOV. BUY 8110 8160-8230 8050 BOOKED FULL PROFIT

28/10/15 NCDEX GUARGUM NOV. SELL 8040 7990-7920 8100 NOT EXECUTED

28/10/15 MCX GOLD DEC. BUY 26900 26980-27070 26800 NOT EXECUTED

28/10/15 MCX GOLD DEC. SELL 26700 26620-26530 25800 NOT EXECUTED

28/10/15 MCX SILVER DEC. BUY 37100 37300-37700 36600 BOOKED FULL PROFIT

28/10/15 MCX SILVER DEC. SELL 36800 36600-36300 36900 NOT EXECUTED

28/10/15 USD/INR OCT. BUY 65.03 65.16-65.13 64.83 NOT EXECUTED

28/10/15 USD/INR OCT. SELL 64.90 64.77-64.62 65.10 NOT EXECUTED

28/10/15 EUR/INR OCT. BUY 71.90 72.05-72.25 71.70 NOT EXECUTED

28/10/15 EUR/INR OCT. SELL 71.80 71.65-71.45 72.00 NOT EXECUTED

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

28/10/15 NIFTY FUTURE SELL 8260 8330-8400 8150 NOT EXECUTED

28/10/15 BHEL FUTURE SELL 216-217 213-211 220.6 BOOKED PROFIT

28/10/15 SKSMICRO FUTURE SELL 398 393-388 405 NOT EXECUTED

28/10/15 EROS MEADIA CASH SELL 364 360-350 370 NOT EXECUTED

27/10/15 CROMPTON

GREAVES FUTURE SELL 182.5 180.5-178 186.60 CALL OPEN

27/10/15 NDL CASH BUY 136 138.5-142 135 BOOKED FULL PROFIT

DAILY REPORT

29th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any

responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere ef-

forts have been made to present the right investment perspective. The information contained herein is based on analysis and up on sources

that we consider reliable. This material is for personal information and based upon it & takes no responsibility. The information given

herein should be treated as only factor, while making investment decision. The report does not provide individually tailor-made invest-

ment advice. Epic research recommends that investors independently evaluate particular investments and strategies, and encourages in-

vestors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the infor-

mation given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not nec-

essarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without no-

tice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone

who is browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either

the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this dis-

claimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the

completeness thereof. We are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the

recommendations above epic research does not purport to be an invitation or an offer to buy or sell any financial instrument. Our Clients

(Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Pro-

vided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, OCT. 26

10 AM NEW HOME SALES SEPT. 550,000 552,000

TUESDAY, OCT. 27

8:30 AM DURABLE GOODS ORDERS SEPT. -1.5% -2.3%

10 AM CONSUMER CONFIDENCE INDEX OCT. 101.0 103.0

WEDNESDAY, OCT. 28

8:30 AM ADVANCED TRADE IN GOODS SEPT. -$64.8 BLN -$67.2 BLN

THURSDAY, OCT. 29

8:30 AM WEEKLY JOBLESS CLAIMS OCT. 17 N/A N/A

8:30 AM GROSS DOMESTIC PRODUCT 3Q 2.1% 3.9%

FRIDAY, OCT. 30

8:30 AM PERSONAL INCOME SEPT. 0.2% 0.3%

8:30 AM CONSUMER SPENDING SEPT. 0.1% 0.4%

8:30 AM CORE INFLATION SEPT. 0.2% 0.1%

8:30 AM EMPLOYMENT COST INDEX 3Q 0.6% 0.2%

10 AM CONSUMER SENTIMENT INDEX OCT. -- 92.1