expected structure of gst and its impact on business 19...

TRANSCRIPT

1© Rödl & Partner 26.09.2012

Expected Structure of GST and its Impact on Business

19 May 2015

Presented by: Anand Khetan

2© Rödl & Partner 19 May 2015

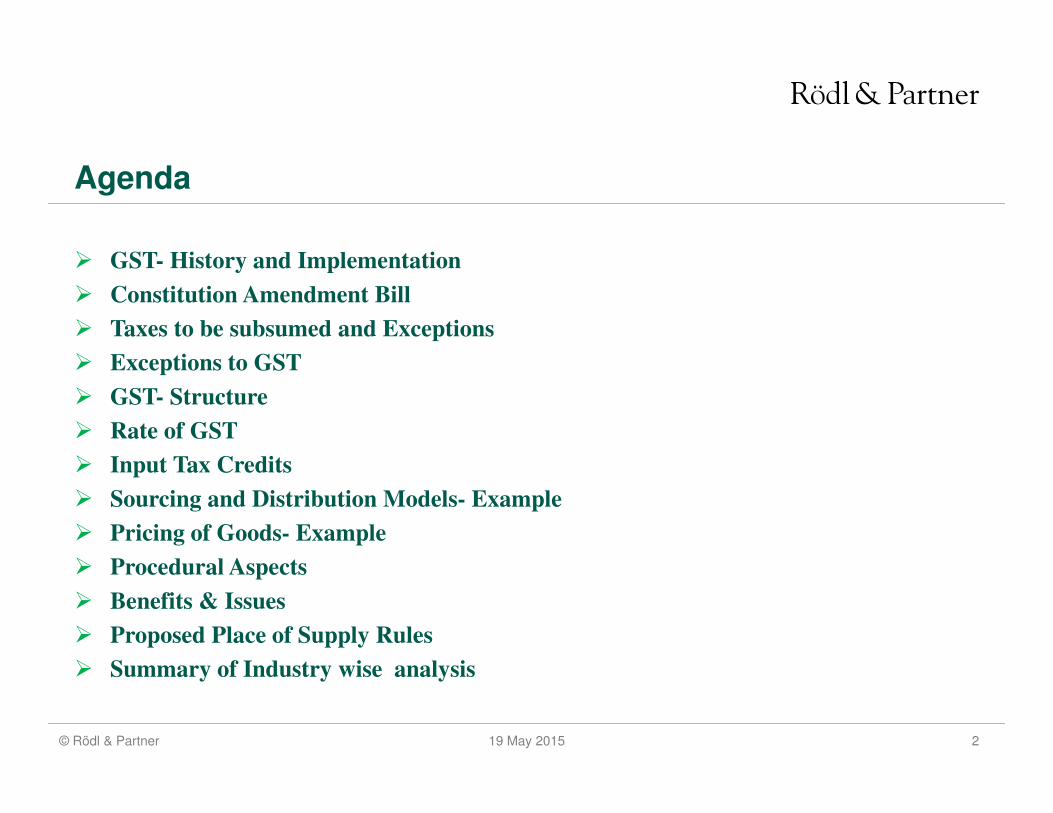

Agenda

� GST- History and Implementation

� Constitution Amendment Bill

� Taxes to be subsumed and Exceptions

� Exceptions to GST

� GST- Structure

� Rate of GST

� Input Tax Credits

� Sourcing and Distribution Models- Example

� Pricing of Goods- Example

� Procedural Aspects

� Benefits & Issues

� Proposed Place of Supply Rules

� Summary of Industry wise analysis

3© Rödl & Partner 19 May 2015

GST- History� February 2007- Government announced its intention to introduce GST by 1 April 2010

� May 2007- Empowered Committee of State Finance Ministers set up

� November 2009- First Discussion Paper released by Empowered Committee

� December 2009- Report of 13th Finance Commission released

� June 2010- Sub-working groups constituted for drafting GST laws

� March 2011- Constitution (115th Amendment) Bill introduced in Parliament

� November 2012- Committee on GST Design constituted by the EC

� February 2013- Committees constituted for threshold, rate, Place of Supply Rules etc

� March 2013- GSTN incorporated as Section 25 company

� August 2013- Standing Committee on Finance submitted report

� December 2014- Constitution (122nd Amendment) Bill introduced in Parliament

� May 2015- Constitution Amendment Bill passed in Lok Sabha

� May 2015- Bill referred to Select Committee of Rajya Sabha (21 Member panel)

4© Rödl & Partner 19 May 2015

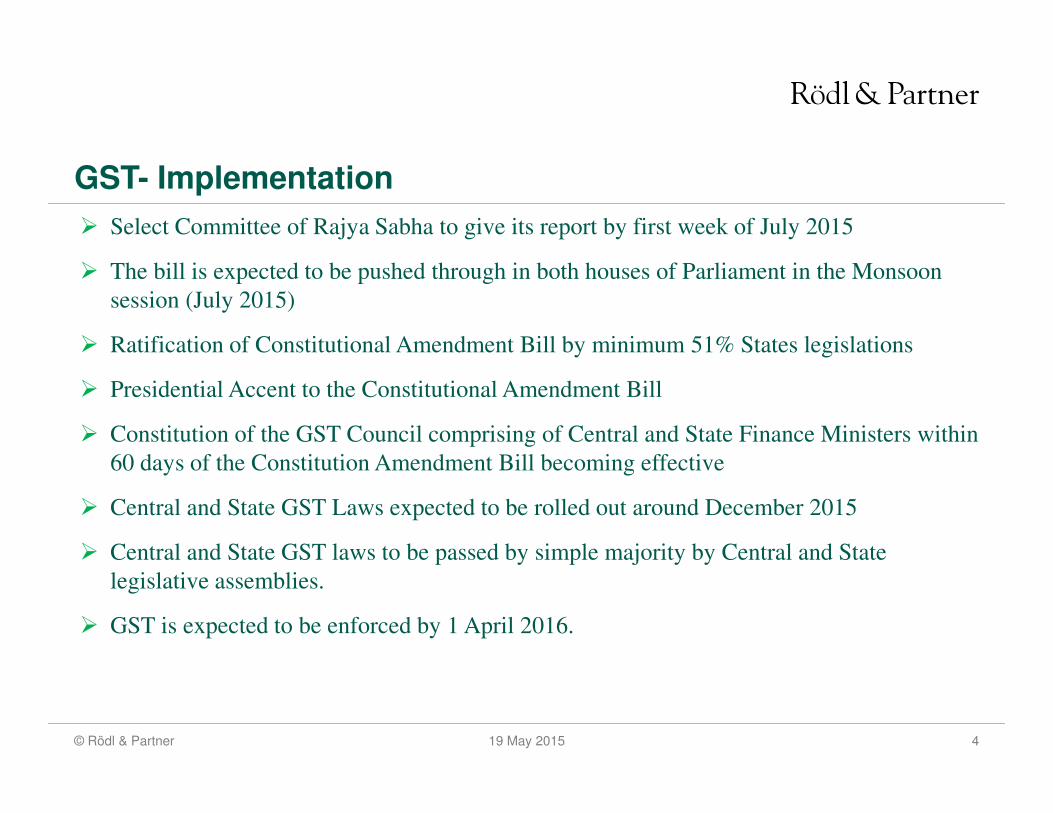

GST- Implementation

� Select Committee of Rajya Sabha to give its report by first week of July 2015

� The bill is expected to be pushed through in both houses of Parliament in the Monsoon

session (July 2015)

� Ratification of Constitutional Amendment Bill by minimum 51% States legislations

� Presidential Accent to the Constitutional Amendment Bill

� Constitution of the GST Council comprising of Central and State Finance Ministers within

60 days of the Constitution Amendment Bill becoming effective

� Central and State GST Laws expected to be rolled out around December 2015

� Central and State GST laws to be passed by simple majority by Central and State

legislative assemblies.

� GST is expected to be enforced by 1 April 2016.

5© Rödl & Partner 19 May 2015

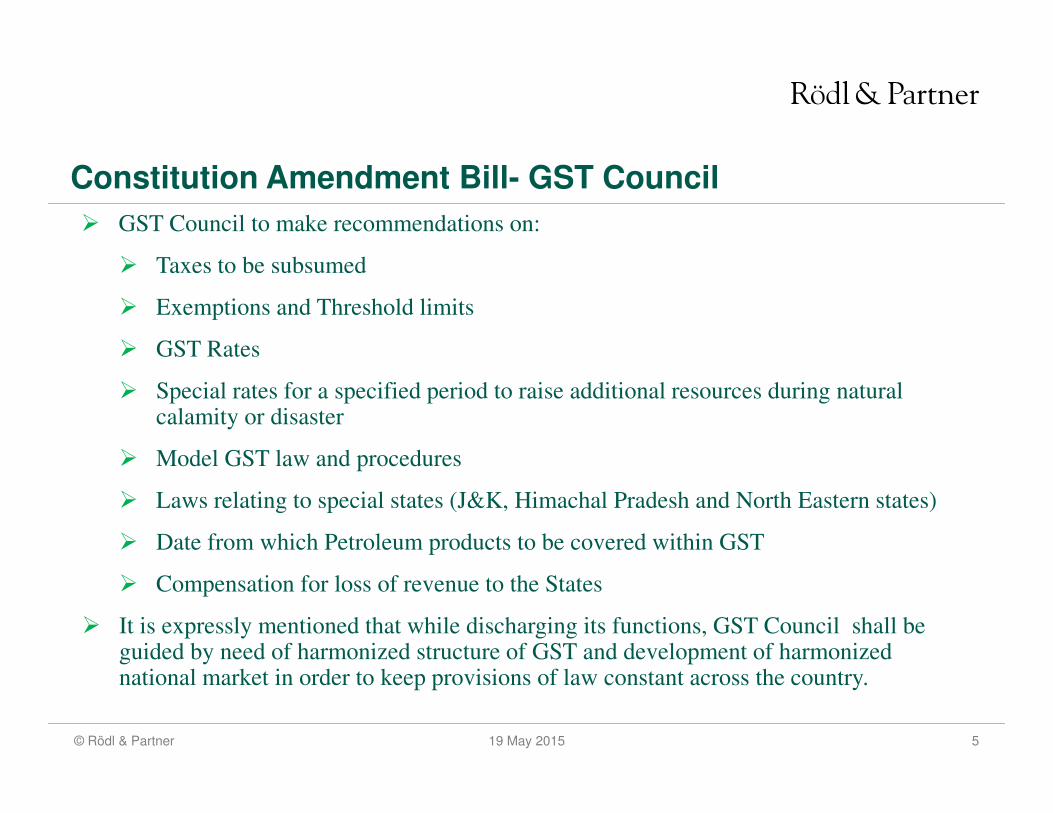

Constitution Amendment Bill- GST Council

� GST Council to make recommendations on:

� Taxes to be subsumed

� Exemptions and Threshold limits

� GST Rates

� Special rates for a specified period to raise additional resources during natural calamity or disaster

� Model GST law and procedures

� Laws relating to special states (J&K, Himachal Pradesh and North Eastern states)

� Date from which Petroleum products to be covered within GST

� Compensation for loss of revenue to the States

� It is expressly mentioned that while discharging its functions, GST Council shall be guided by need of harmonized structure of GST and development of harmonized national market in order to keep provisions of law constant across the country.

6© Rödl & Partner 19 May 2015

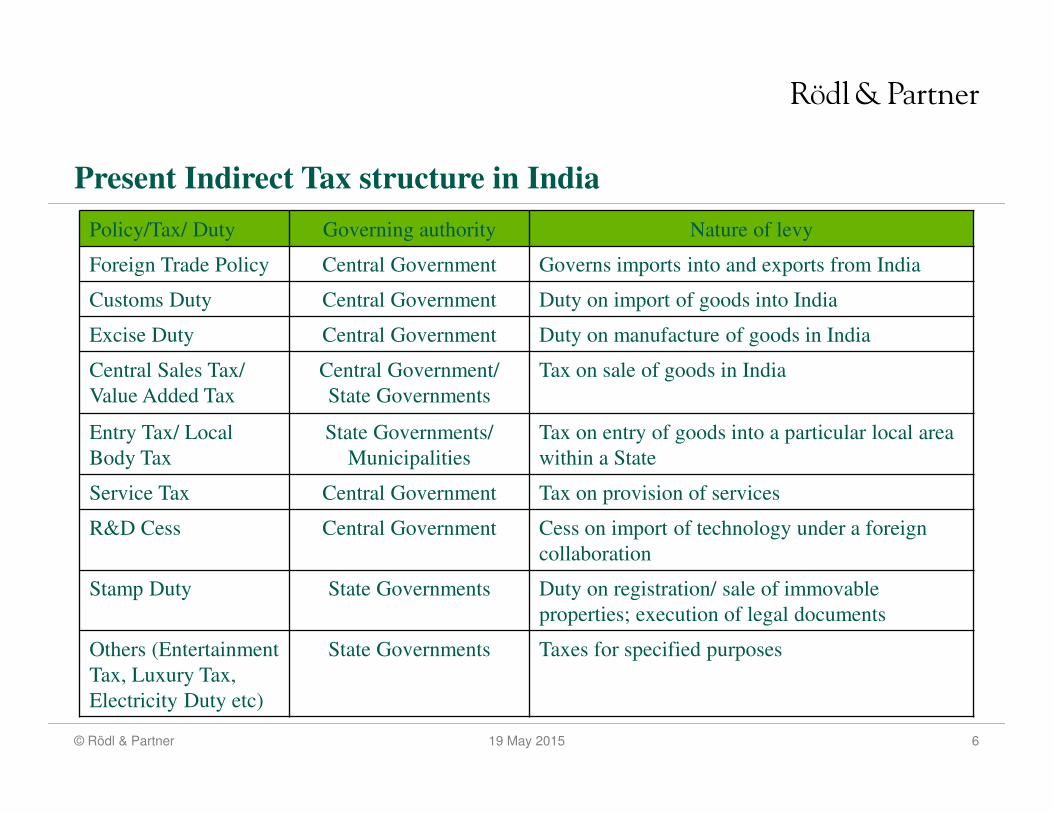

Present Indirect Tax structure in India

Policy/Tax/ Duty Governing authority Nature of levy

Foreign Trade Policy Central Government Governs imports into and exports from India

Customs Duty Central Government Duty on import of goods into India

Excise Duty Central Government Duty on manufacture of goods in India

Central Sales Tax/

Value Added Tax

Central Government/

State Governments

Tax on sale of goods in India

Entry Tax/ Local

Body Tax

State Governments/

Municipalities

Tax on entry of goods into a particular local area

within a State

Service Tax Central Government Tax on provision of services

R&D Cess Central Government Cess on import of technology under a foreign

collaboration

Stamp Duty State Governments Duty on registration/ sale of immovable

properties; execution of legal documents

Others (Entertainment

Tax, Luxury Tax,

Electricity Duty etc)

State Governments Taxes for specified purposes

7© Rödl & Partner 19 May 2015

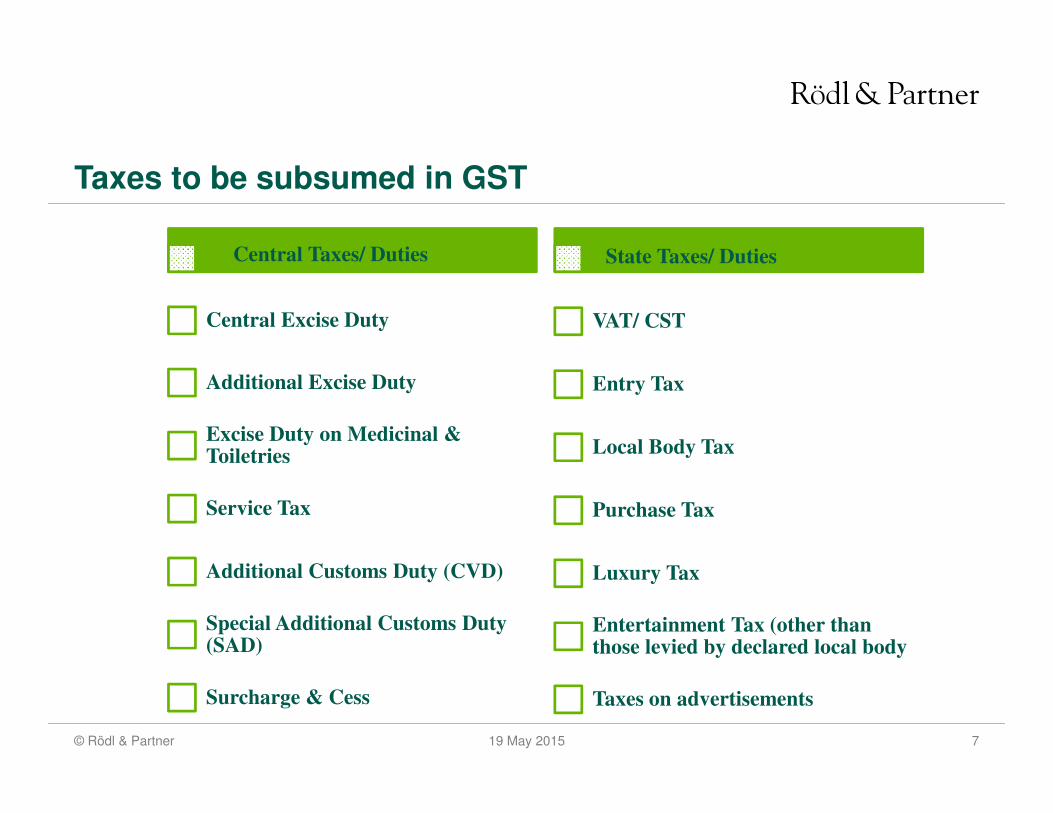

Taxes to be subsumed in GST

Central Taxes/ Duties

Central Excise Duty

Additional Excise Duty

Excise Duty on Medicinal & Toiletries

Service Tax

Additional Customs Duty (CVD)

Special Additional Customs Duty (SAD)

Surcharge & Cess

State Taxes/ Duties

VAT/ CST

Entry Tax

Local Body Tax

Purchase Tax

Luxury Tax

Entertainment Tax (other than those levied by declared local body

Taxes on advertisements

8© Rödl & Partner 19 May 2015

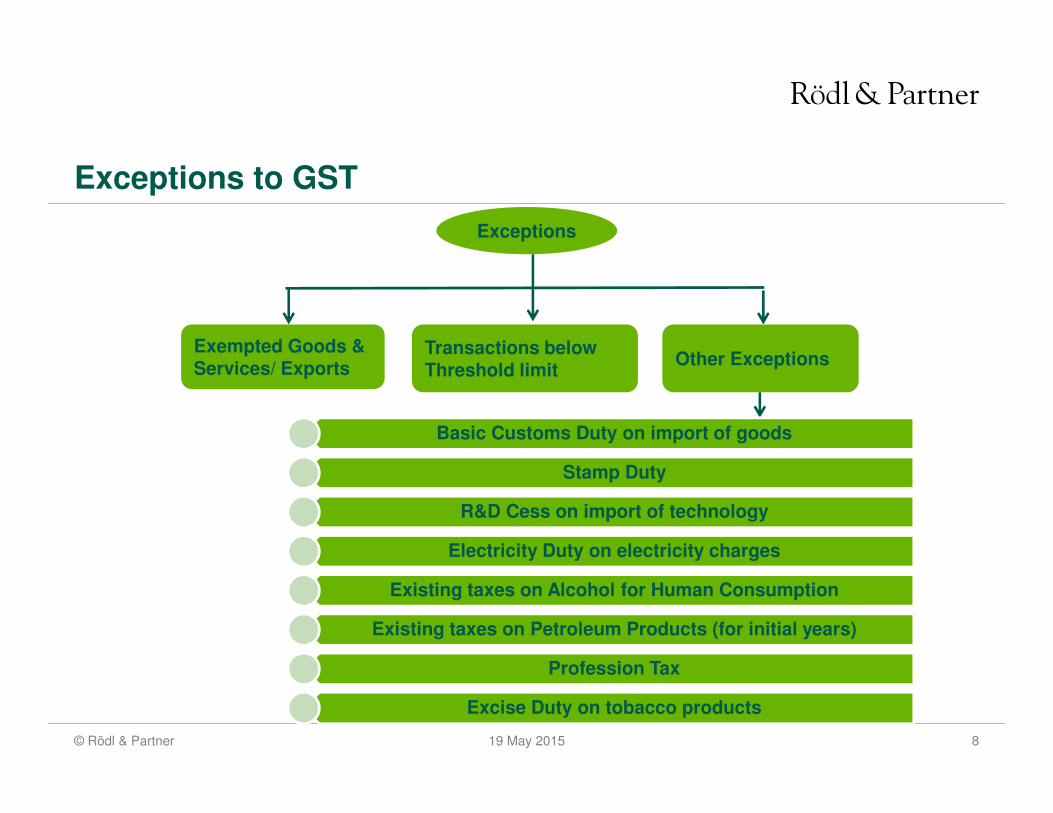

Exceptions to GST

Exceptions

Exempted Goods & Services/ Exports

Transactions below Threshold limit

Other Exceptions

Basic Customs Duty on import of goods

Stamp Duty

R&D Cess on import of technology

Electricity Duty on electricity charges

Existing taxes on Alcohol for Human Consumption

Existing taxes on Petroleum Products (for initial years)

Profession Tax

Excise Duty on tobacco products

9© Rödl & Partner 19 May 2015

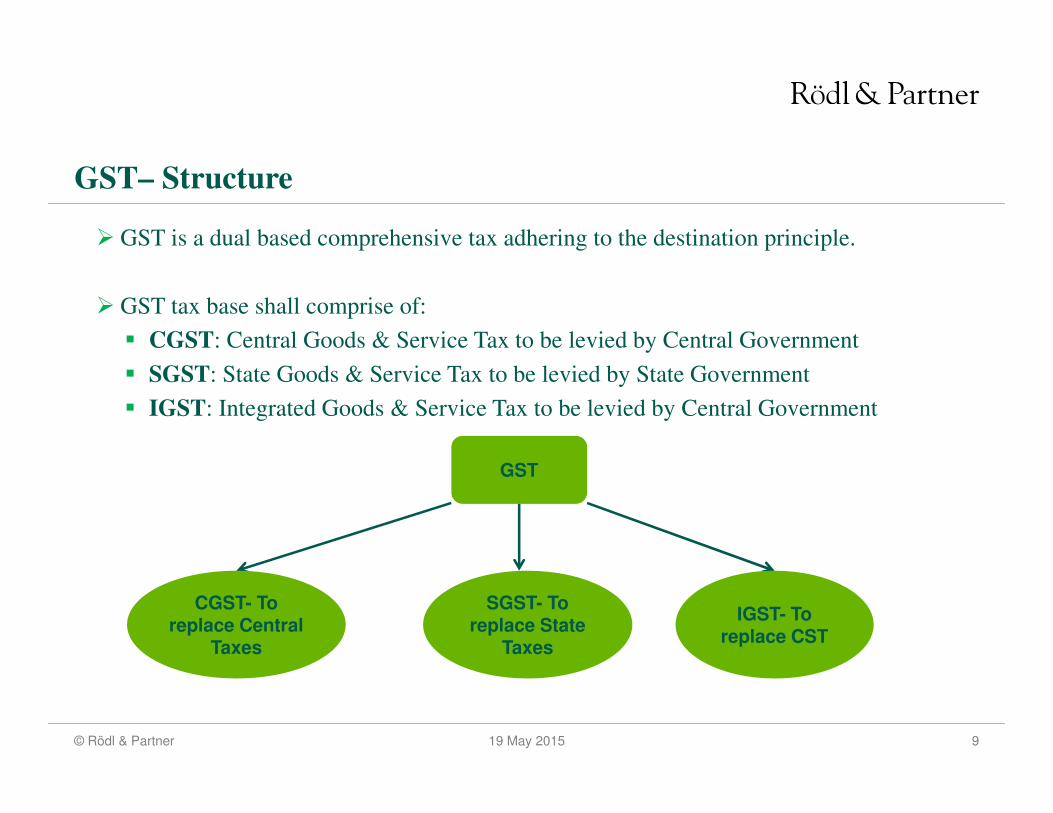

GST– Structure

� GST is a dual based comprehensive tax adhering to the destination principle.

� GST tax base shall comprise of:

� CGST: Central Goods & Service Tax to be levied by Central Government

� SGST: State Goods & Service Tax to be levied by State Government

� IGST: Integrated Goods & Service Tax to be levied by Central Government

GST

CGST- To replace Central

Taxes

SGST- To replace State

Taxes

IGST- To replace CST

10© Rödl & Partner 19 May 2015

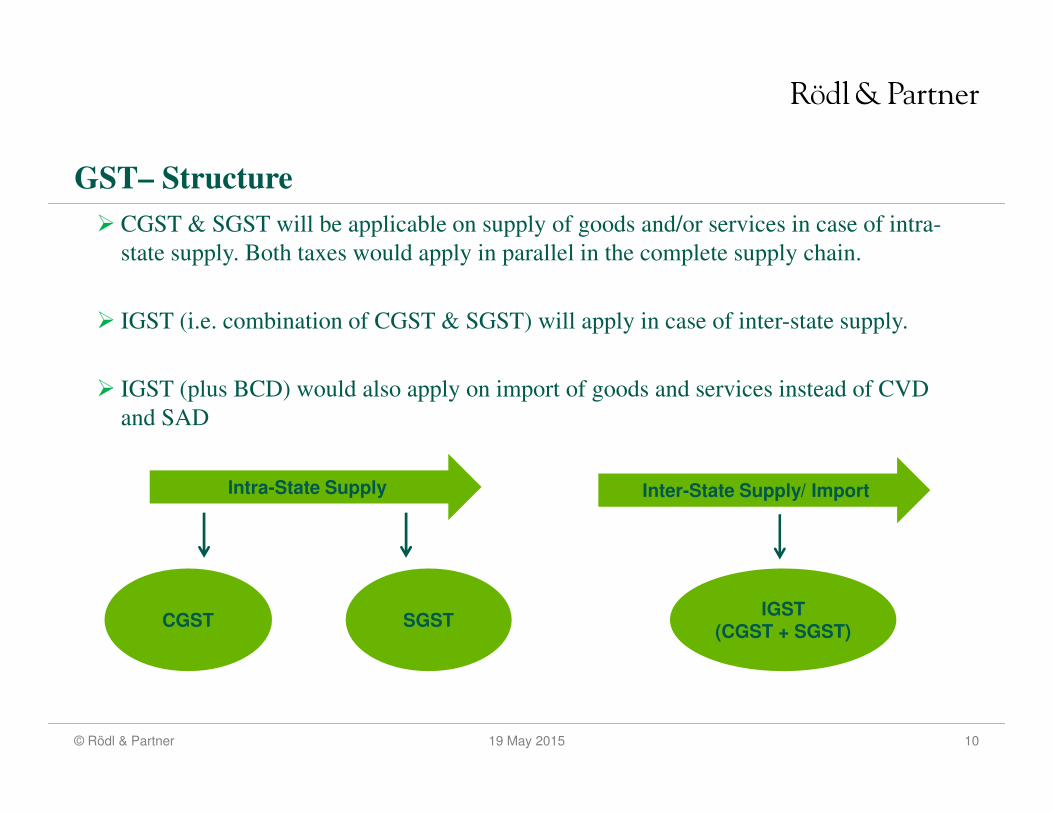

GST– Structure

� CGST & SGST will be applicable on supply of goods and/or services in case of intra-

state supply. Both taxes would apply in parallel in the complete supply chain.

� IGST (i.e. combination of CGST & SGST) will apply in case of inter-state supply.

� IGST (plus BCD) would also apply on import of goods and services instead of CVD

and SAD

CGSTIGST

(CGST + SGST)SGST

Intra-State Supply Inter-State Supply/ Import

11© Rödl & Partner 19 May 2015

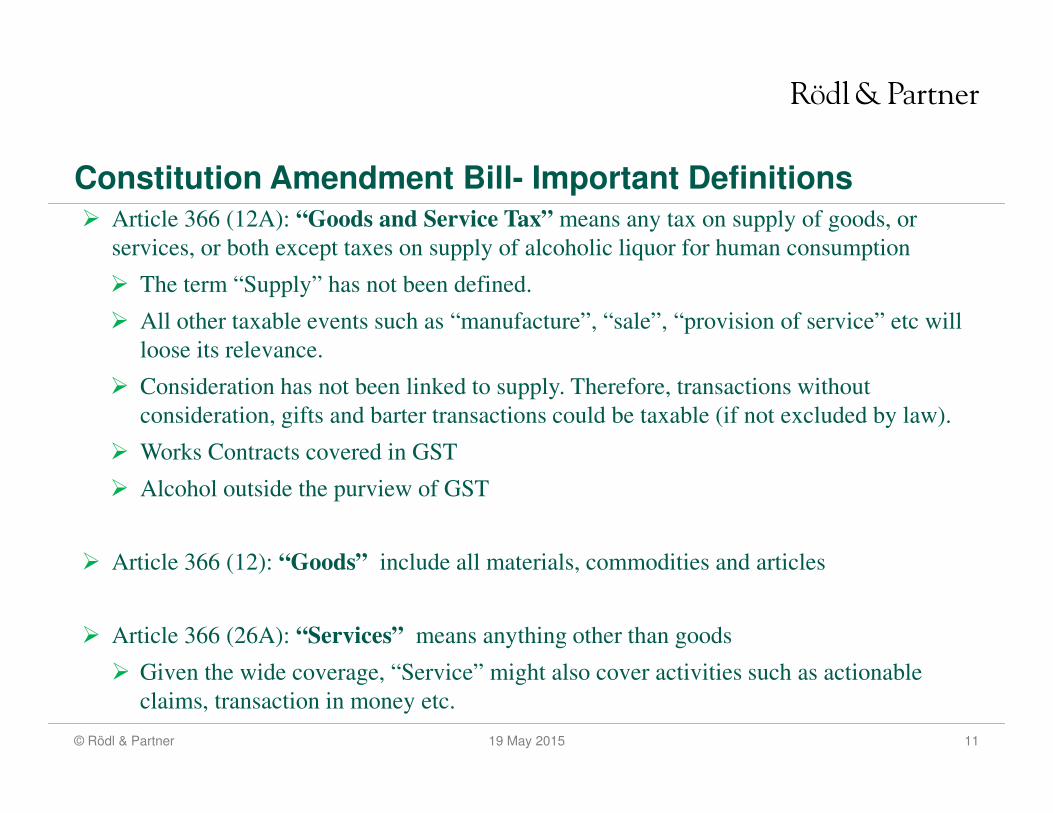

Constitution Amendment Bill- Important Definitions� Article 366 (12A): “Goods and Service Tax” means any tax on supply of goods, or

services, or both except taxes on supply of alcoholic liquor for human consumption

� The term “Supply” has not been defined.

� All other taxable events such as “manufacture”, “sale”, “provision of service” etc will

loose its relevance.

� Consideration has not been linked to supply. Therefore, transactions without

consideration, gifts and barter transactions could be taxable (if not excluded by law).

� Works Contracts covered in GST

� Alcohol outside the purview of GST

� Article 366 (12): “Goods” include all materials, commodities and articles

� Article 366 (26A): “Services” means anything other than goods

� Given the wide coverage, “Service” might also cover activities such as actionable

claims, transaction in money etc.

12© Rödl & Partner 19 May 2015

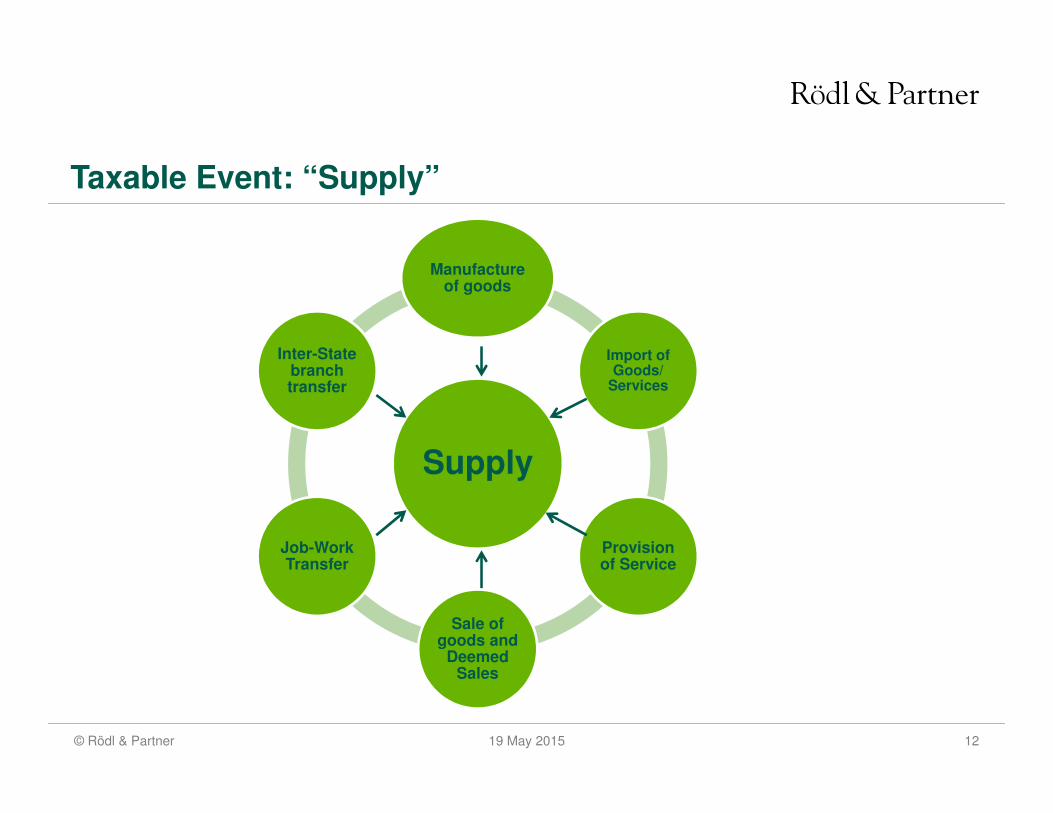

Taxable Event: “Supply”

Supply

Manufacture of goods

Import of Goods/

Services

Provision of Service

Sale of goods and

Deemed Sales

Job-Work Transfer

Inter-State branch transfer

13© Rödl & Partner 19 May 2015

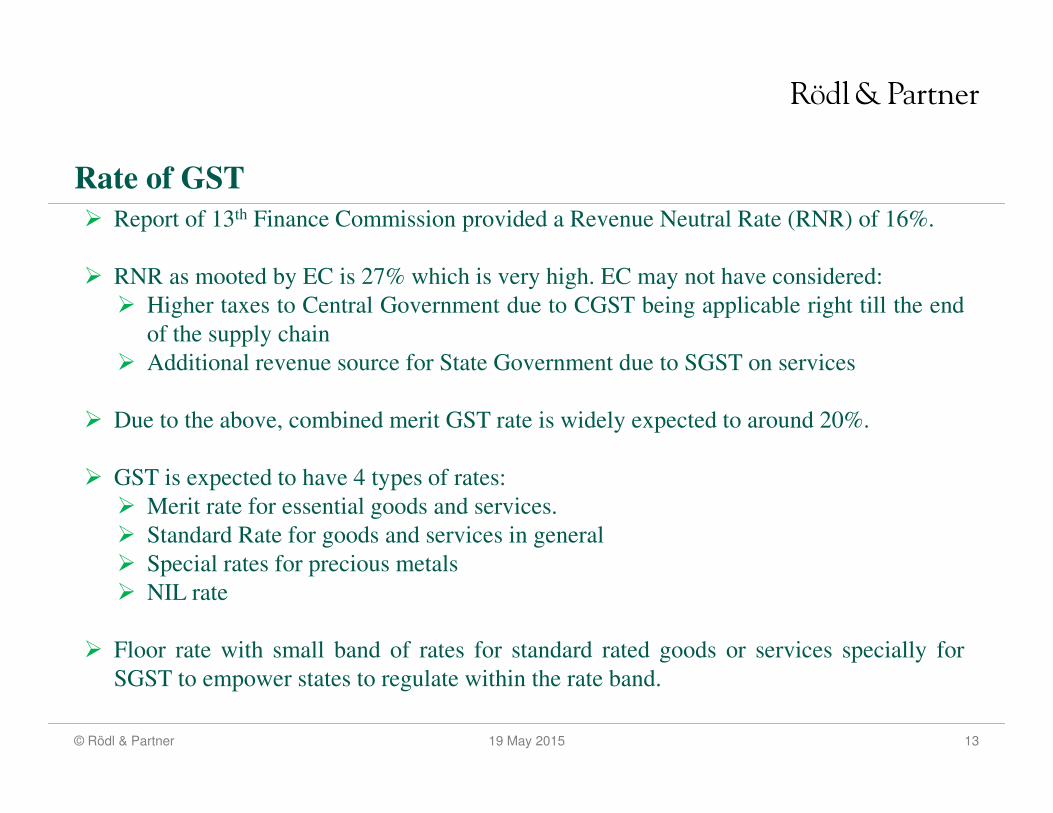

Rate of GST

� Report of 13th Finance Commission provided a Revenue Neutral Rate (RNR) of 16%.

� RNR as mooted by EC is 27% which is very high. EC may not have considered:

� Higher taxes to Central Government due to CGST being applicable right till the end

of the supply chain

� Additional revenue source for State Government due to SGST on services

� Due to the above, combined merit GST rate is widely expected to around 20%.

� GST is expected to have 4 types of rates:

� Merit rate for essential goods and services.

� Standard Rate for goods and services in general

� Special rates for precious metals

� NIL rate

� Floor rate with small band of rates for standard rated goods or services specially for

SGST to empower states to regulate within the rate band.

14© Rödl & Partner 19 May 2015

Rate of GST

� Optional Threshold exemption in both components of GST

� Optional compounding scheme for taxpayers having turnover up to a certain limit.

� HSN codes are likely to be used for classification of goods

� Present Accounting Codes are likely to be used for services

� Non-omittance of Article 366 (29A): Whether an indication towards separate GST rates

for goods and services?

� In case of separate rate for goods and services, classification issues might continue

� Additional non-vatable tax of 1% on inters-state supply of goods (NOT services)

including import of goods for a period of 2 years or more:

� Replacement of CST

� In case of Work Contract, ambiguity to determine the value of goods for levying 1%

additional GST.

15© Rödl & Partner 19 May 2015

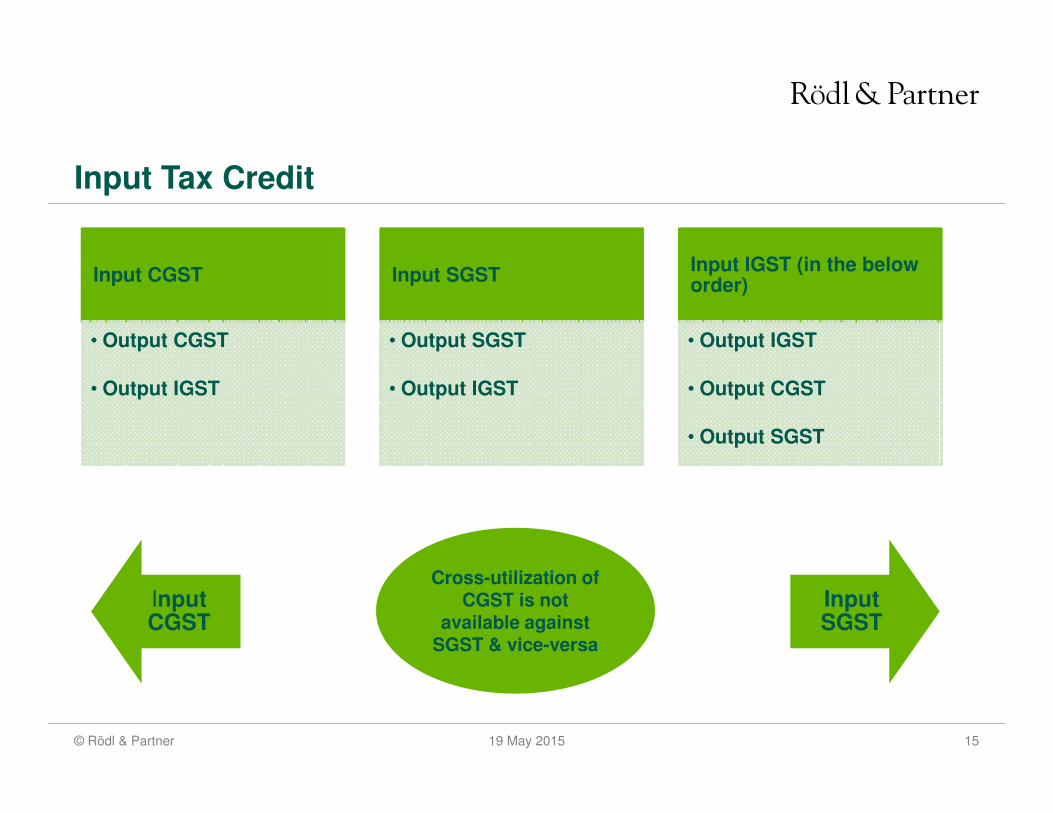

Input Tax Credit

Input CGST

• Output CGST

• Output IGST

Input SGST

• Output SGST

• Output IGST

Input IGST (in the below order)

• Output IGST

• Output CGST

• Output SGST

Input CGST

Input SGST

Cross-utilization of CGST is not

available against SGST & vice-versa

16© Rödl & Partner 19 May 2015

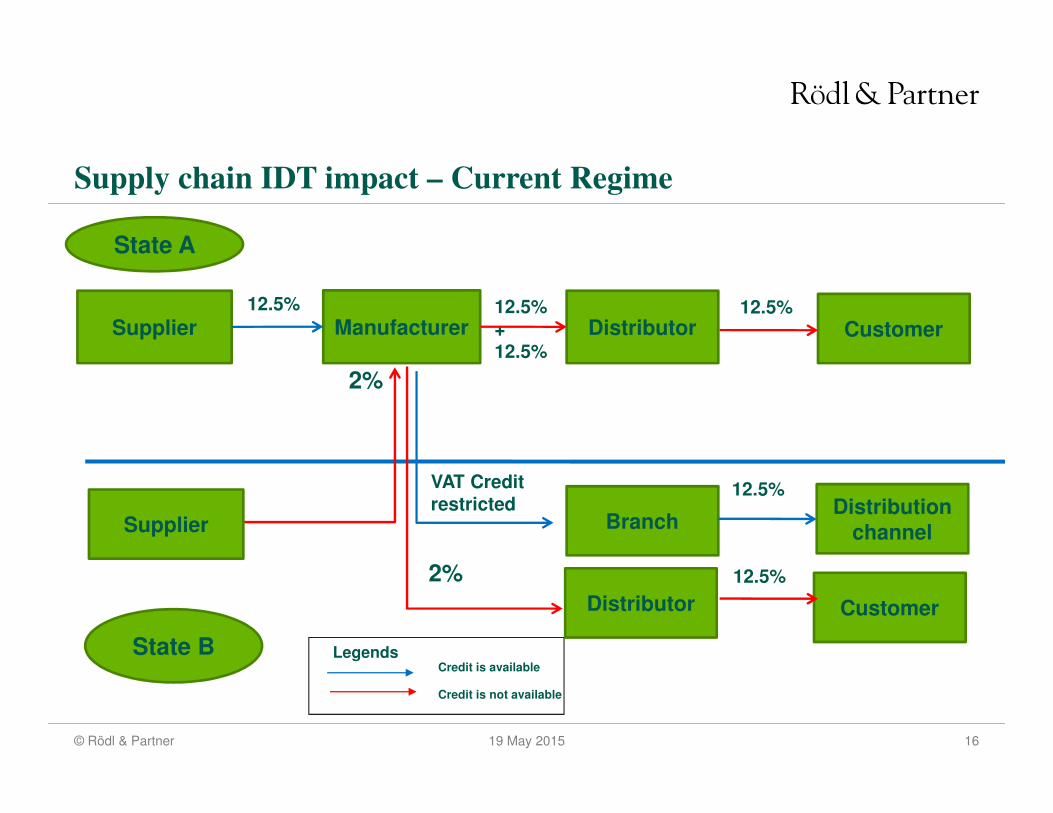

Supply chain IDT impact – Current Regime

State A

State B

Supplier

2%

Credit is available

Credit is not available

Legends

Manufacturer Distributor Customer

Supplier BranchDistribution

channel

12.5% 12.5%+12.5%

12.5%

12.5%

Distributor

2%

Customer

12.5%

VAT Credit restricted

17© Rödl & Partner 19 May 2015

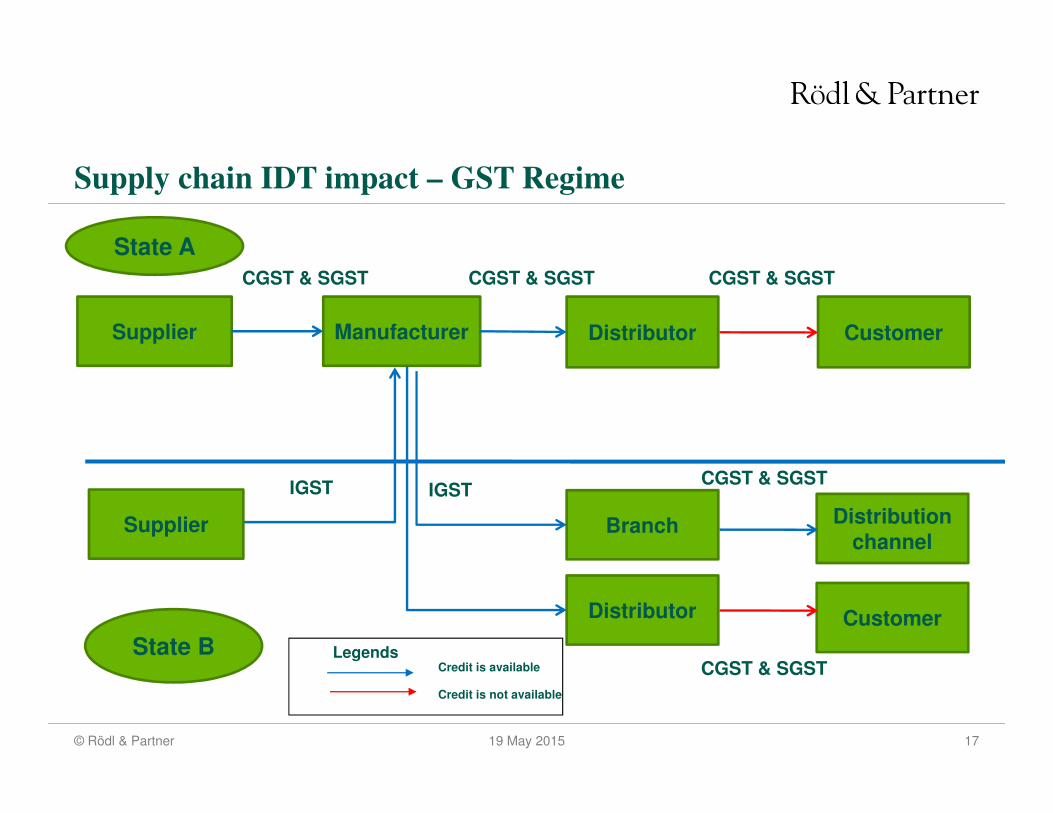

Supply chain IDT impact – GST Regime

State A

State B

Supplier Manufacturer Distributor Customer

Supplier Branch Distribution

channel

Distributor Customer

CGST & SGST CGST & SGST CGST & SGST

IGST IGSTCGST & SGST

CGST & SGSTLegends

Credit is available

Credit is not available

18© Rödl & Partner 19 May 2015

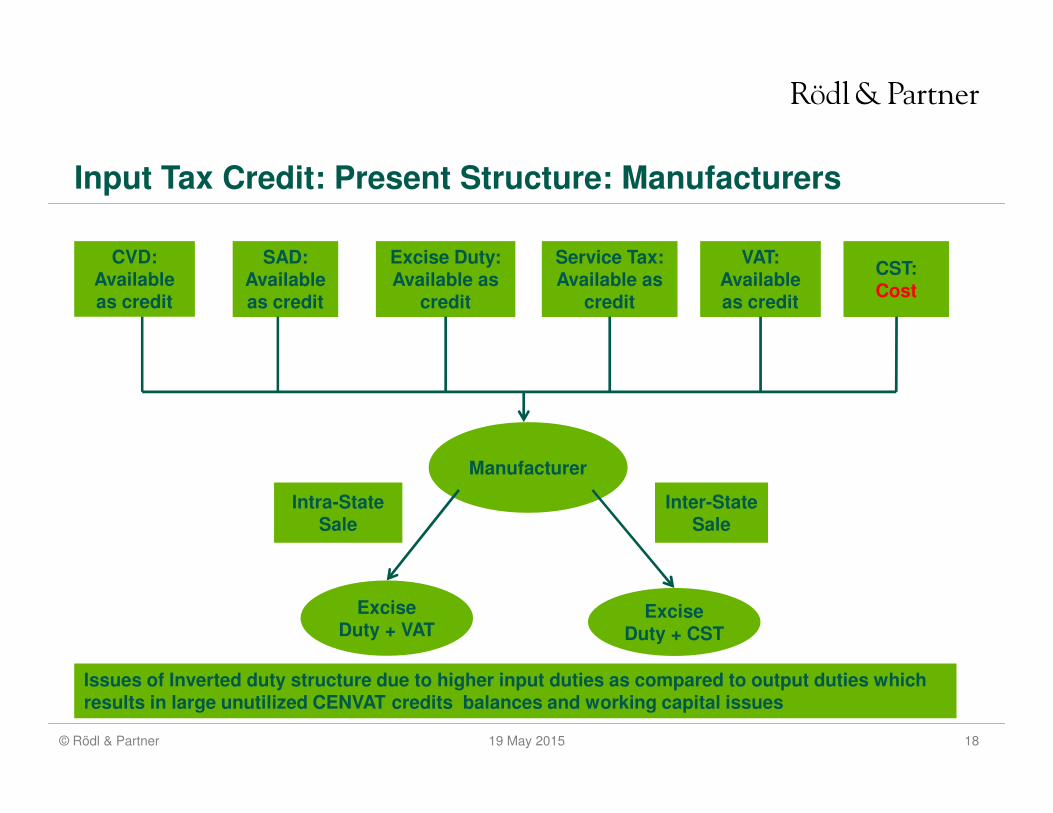

Input Tax Credit: Present Structure: Manufacturers

CVD: Available as credit

Intra-State Sale

Manufacturer

SAD:Available as credit

Excise Duty: Available as

credit

Service Tax:Available as

credit

VAT:Available as credit

CST:Cost

Inter-State Sale

Excise Duty + VAT

Excise Duty + CST

Issues of Inverted duty structure due to higher input duties as compared to output duties which results in large unutilized CENVAT credits balances and working capital issues

19© Rödl & Partner 19 May 2015

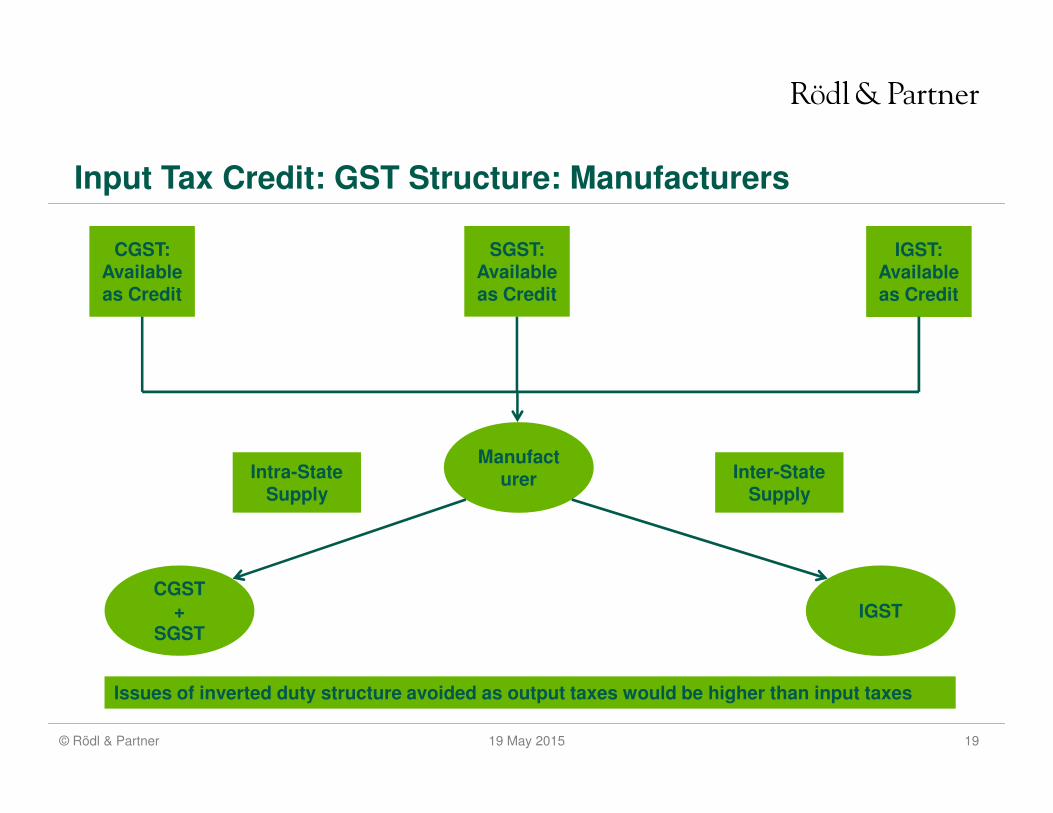

Input Tax Credit: GST Structure: Manufacturers

CGST:Available as Credit

Manufacturer

SGST:Available as Credit

IGST:Available as Credit

CGST+

SGSTIGST

Issues of inverted duty structure avoided as output taxes would be higher than input taxes

Intra-State Supply

Inter-State Supply

20© Rödl & Partner 19 May 2015

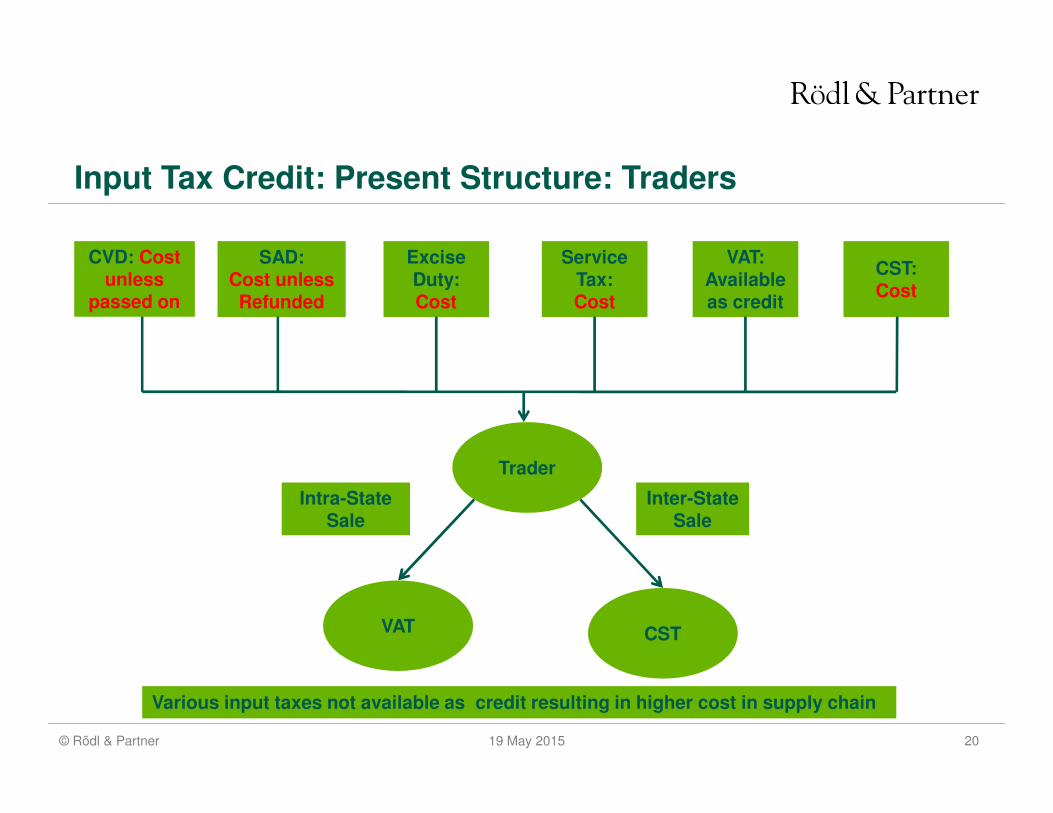

Input Tax Credit: Present Structure: Traders

CVD: Cost unless

passed on

Intra-State Sale

Trader

SAD:Cost unless Refunded

Excise Duty: Cost

Service Tax:Cost

VAT:Available as credit

CST:Cost

Inter-State Sale

VAT CST

Various input taxes not available as credit resulting in higher cost in supply chain

21© Rödl & Partner 19 May 2015

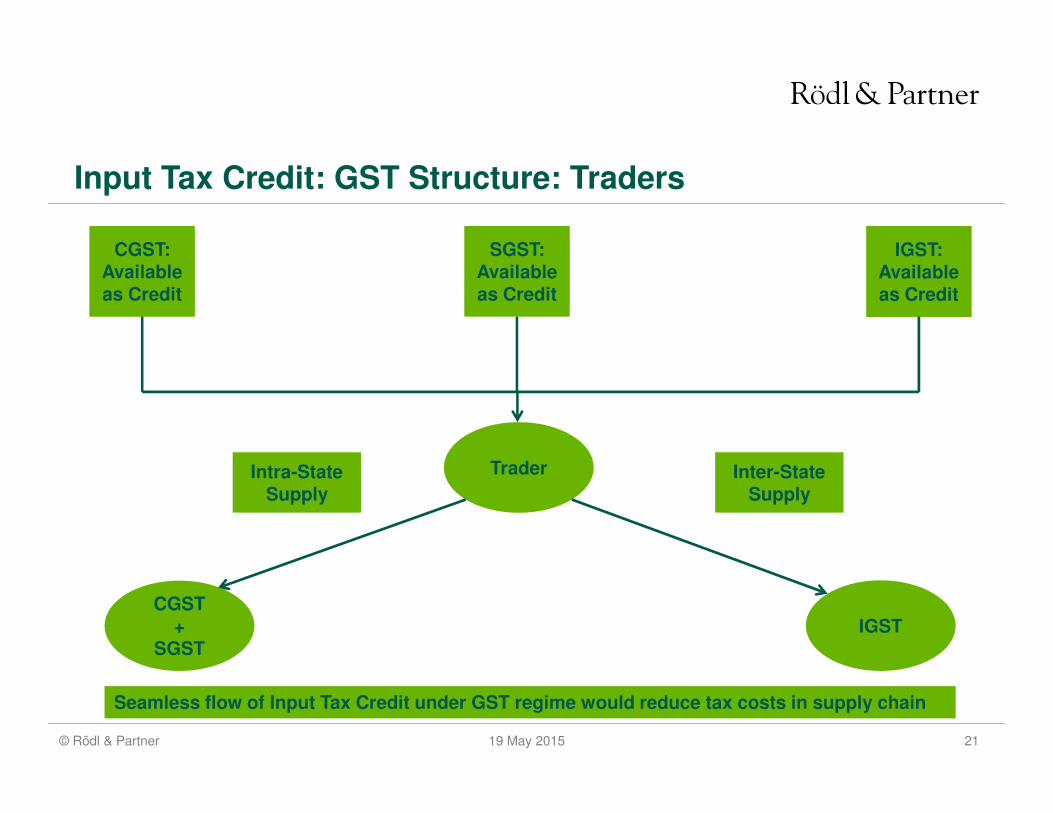

Input Tax Credit: GST Structure: Traders

CGST:Available as Credit

Trader

SGST:Available as Credit

IGST:Available as Credit

CGST+

SGSTIGST

Seamless flow of Input Tax Credit under GST regime would reduce tax costs in supply chain

Intra-State Supply

Inter-State Supply

22© Rödl & Partner 19 May 2015

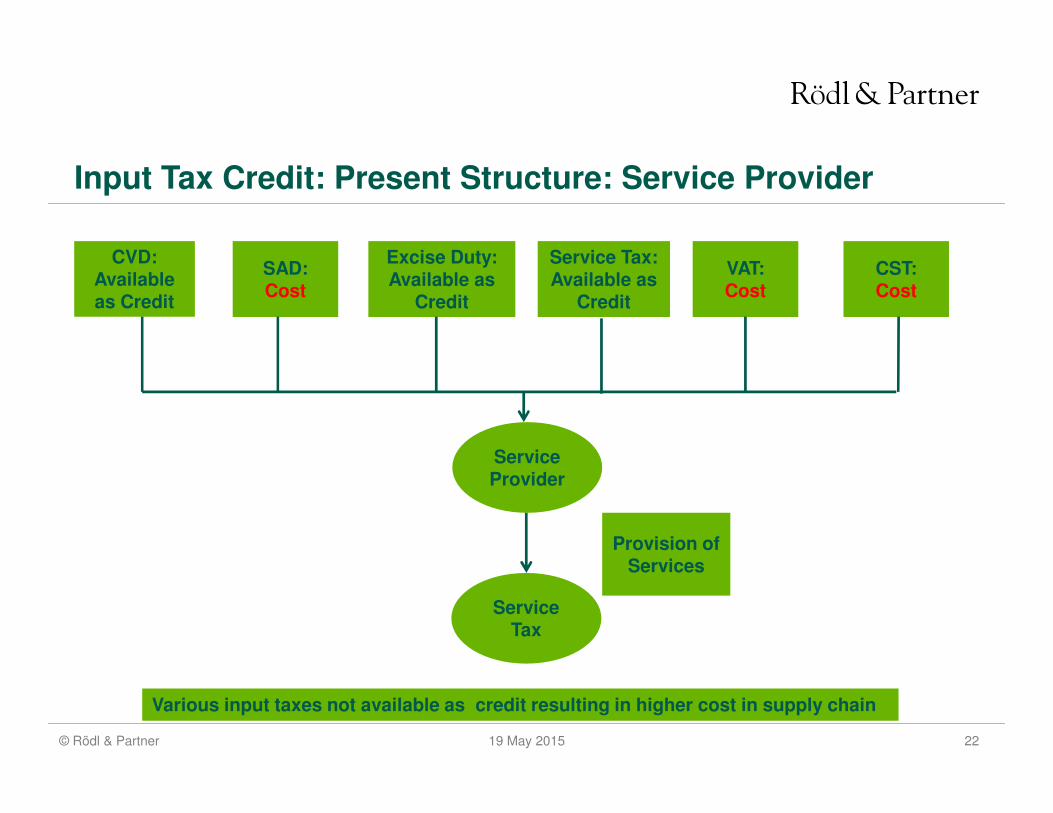

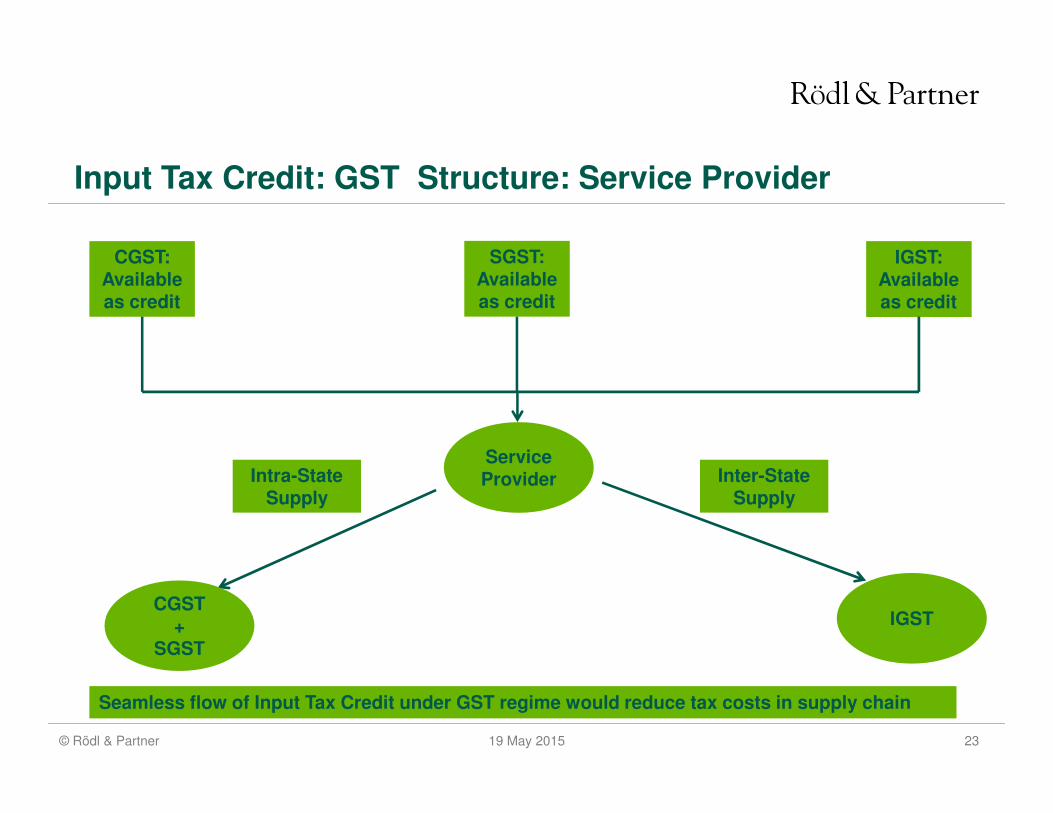

Input Tax Credit: Present Structure: Service Provider

CVD: Available as Credit

Service Provider

SAD:Cost

Excise Duty: Available as

Credit

Service Tax:Available as

Credit

VAT:Cost

CST:Cost

Provision of Services

Service Tax

Various input taxes not available as credit resulting in higher cost in supply chain

23© Rödl & Partner 19 May 2015

Input Tax Credit: GST Structure: Service Provider

CGST:Available as credit

Service Provider

SGST:Available as credit

IGST:Available as credit

CGST+

SGST

IGST

Seamless flow of Input Tax Credit under GST regime would reduce tax costs in supply chain

Intra-State Supply

Inter-State Supply

24© Rödl & Partner 19 May 2015

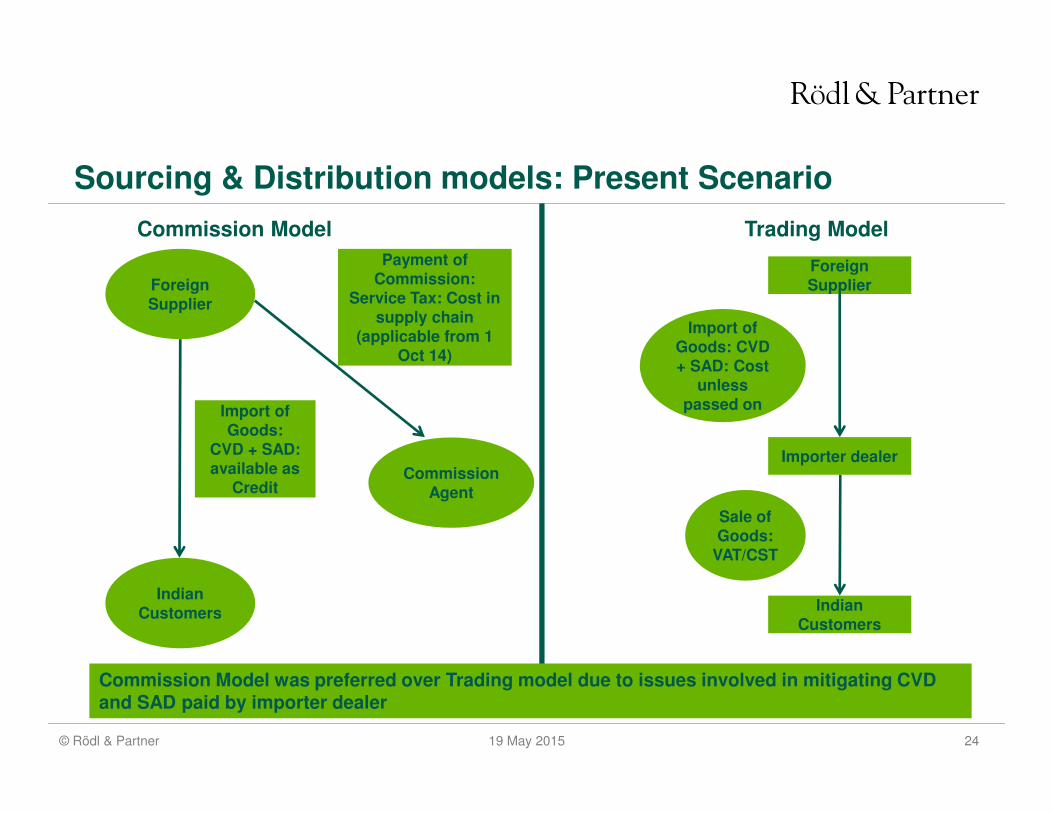

Commission Model Trading Model

Foreign Supplier

Indian Customers

Commission Agent

Foreign Supplier

Importer dealer

Indian Customers

Payment of Commission:

Service Tax: Cost in supply chain

(applicable from 1 Oct 14)

Import of Goods:

CVD + SAD: available as

Credit

Import of Goods: CVD + SAD: Cost

unless passed on

Sale of Goods:

VAT/CST

Commission Model was preferred over Trading model due to issues involved in mitigating CVD and SAD paid by importer dealer

Sourcing & Distribution models: Present Scenario

25© Rödl & Partner 19 May 2015

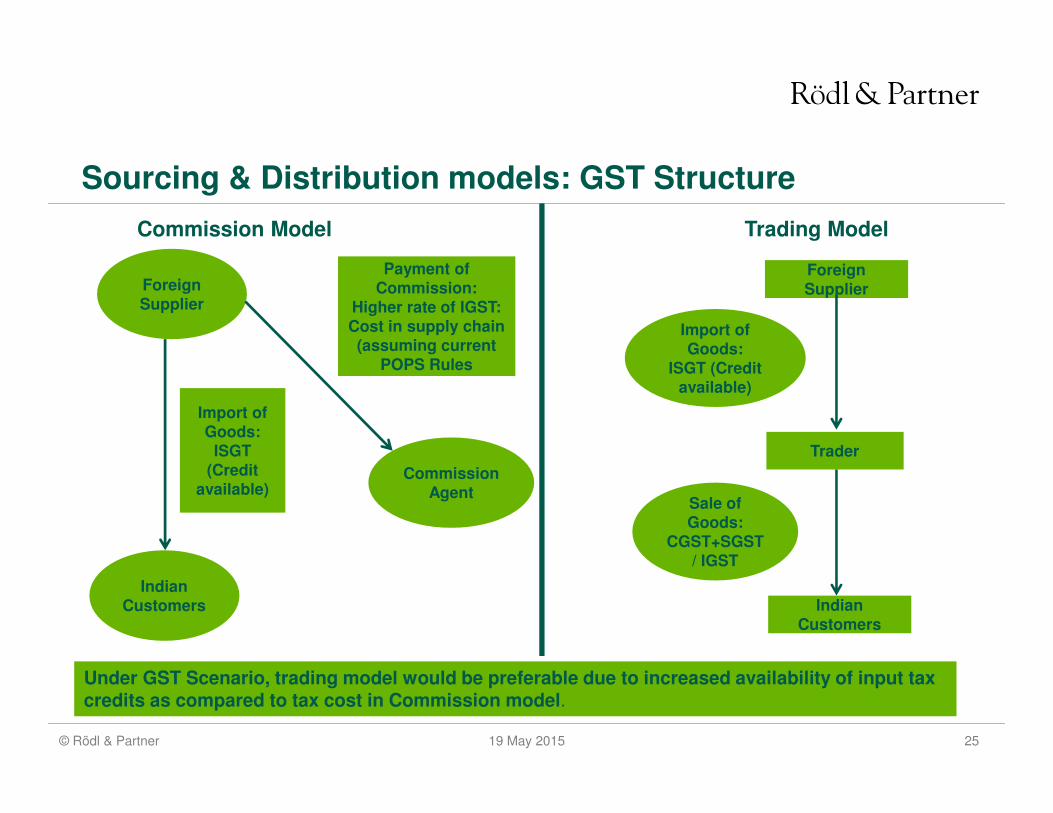

Commission Model Trading Model

Foreign Supplier

Indian Customers

Commission Agent

Foreign Supplier

Trader

Indian Customers

Payment of Commission:

Higher rate of IGST: Cost in supply chain (assuming current

POPS Rules

Import of Goods:

ISGT (Credit

available)

Import of Goods:

ISGT (Credit available)

Sale of Goods:

CGST+SGST/ IGST

Under GST Scenario, trading model would be preferable due to increased availability of input tax credits as compared to tax cost in Commission model.

Sourcing & Distribution models: GST Structure

26© Rödl & Partner 19 May 2015

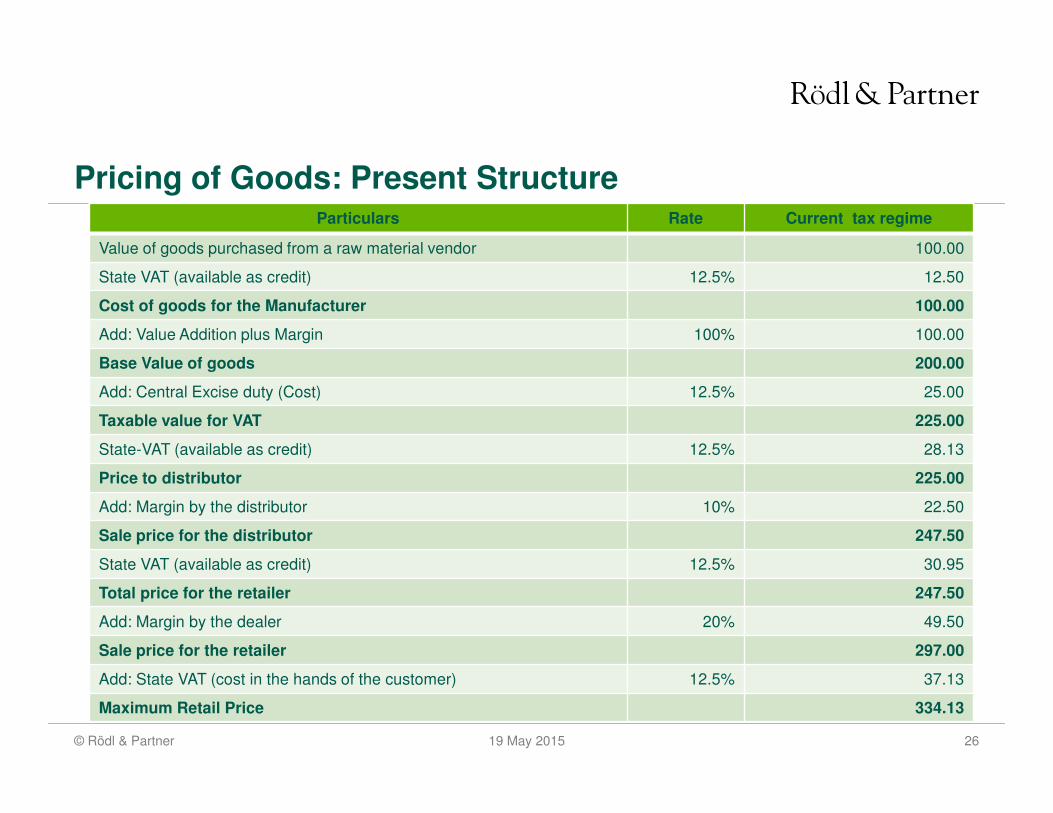

Pricing of Goods: Present StructureParticulars Rate Current tax regime

Value of goods purchased from a raw material vendor 100.00

State VAT (available as credit) 12.5% 12.50

Cost of goods for the Manufacturer 100.00

Add: Value Addition plus Margin 100% 100.00

Base Value of goods 200.00

Add: Central Excise duty (Cost) 12.5% 25.00

Taxable value for VAT 225.00

State-VAT (available as credit) 12.5% 28.13

Price to distributor 225.00

Add: Margin by the distributor 10% 22.50

Sale price for the distributor 247.50

State VAT (available as credit) 12.5% 30.95

Total price for the retailer 247.50

Add: Margin by the dealer 20% 49.50

Sale price for the retailer 297.00

Add: State VAT (cost in the hands of the customer) 12.5% 37.13

Maximum Retail Price 334.13

27© Rödl & Partner 19 May 2015

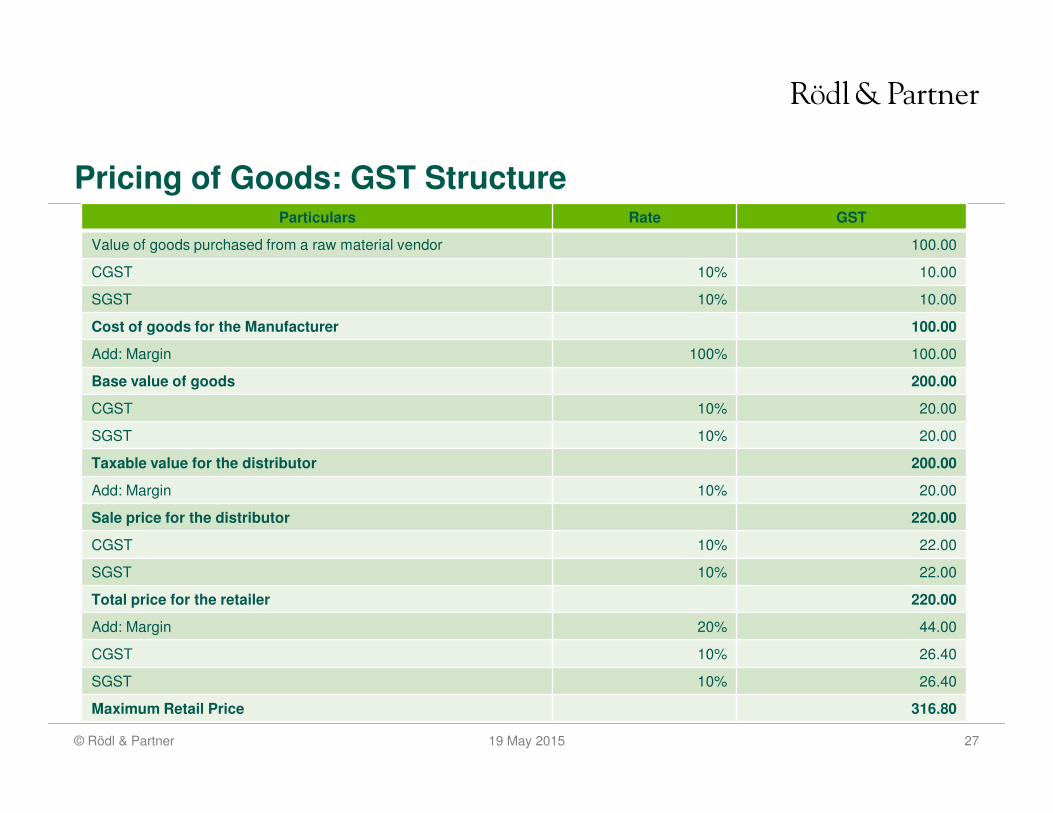

Pricing of Goods: GST StructureParticulars Rate GST

Value of goods purchased from a raw material vendor 100.00

CGST 10% 10.00

SGST 10% 10.00

Cost of goods for the Manufacturer 100.00

Add: Margin 100% 100.00

Base value of goods 200.00

CGST 10% 20.00

SGST 10% 20.00

Taxable value for the distributor 200.00

Add: Margin 10% 20.00

Sale price for the distributor 220.00

CGST 10% 22.00

SGST 10% 22.00

Total price for the retailer 220.00

Add: Margin 20% 44.00

CGST 10% 26.40

SGST 10% 26.40

Maximum Retail Price 316.80

28© Rödl & Partner 19 May 2015

Procedural Aspects

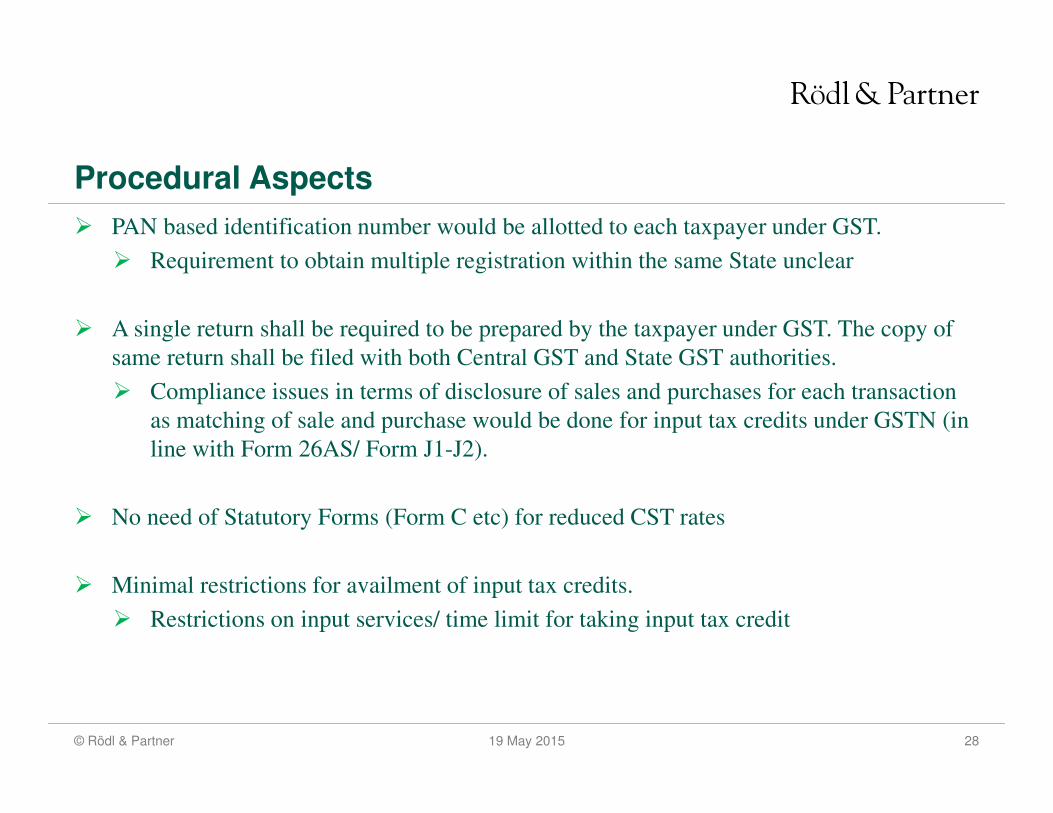

� PAN based identification number would be allotted to each taxpayer under GST.

� Requirement to obtain multiple registration within the same State unclear

� A single return shall be required to be prepared by the taxpayer under GST. The copy of

same return shall be filed with both Central GST and State GST authorities.

� Compliance issues in terms of disclosure of sales and purchases for each transaction

as matching of sale and purchase would be done for input tax credits under GSTN (in

line with Form 26AS/ Form J1-J2).

� No need of Statutory Forms (Form C etc) for reduced CST rates

� Minimal restrictions for availment of input tax credits.

� Restrictions on input services/ time limit for taking input tax credit

29© Rödl & Partner 19 May 2015

Benefits of GST

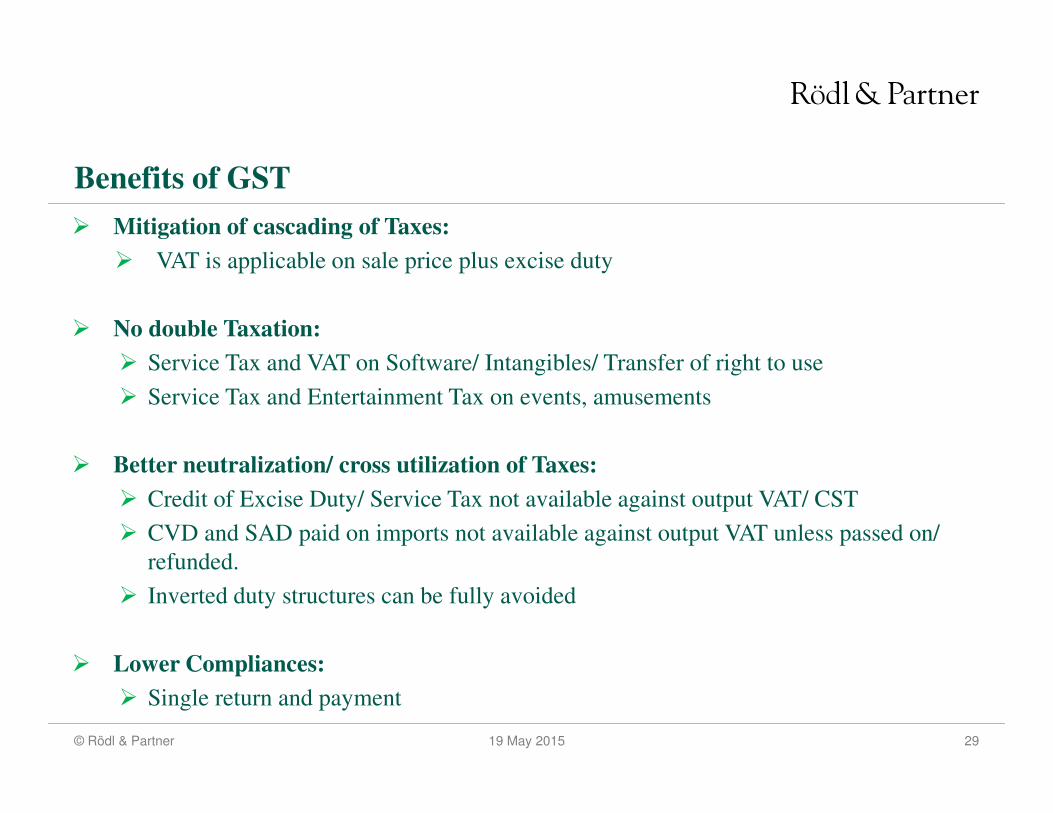

� Mitigation of cascading of Taxes:

� VAT is applicable on sale price plus excise duty

� No double Taxation:

� Service Tax and VAT on Software/ Intangibles/ Transfer of right to use

� Service Tax and Entertainment Tax on events, amusements

� Better neutralization/ cross utilization of Taxes:

� Credit of Excise Duty/ Service Tax not available against output VAT/ CST

� CVD and SAD paid on imports not available against output VAT unless passed on/

refunded.

� Inverted duty structures can be fully avoided

� Lower Compliances:

� Single return and payment

30© Rödl & Partner 19 May 2015

Issues

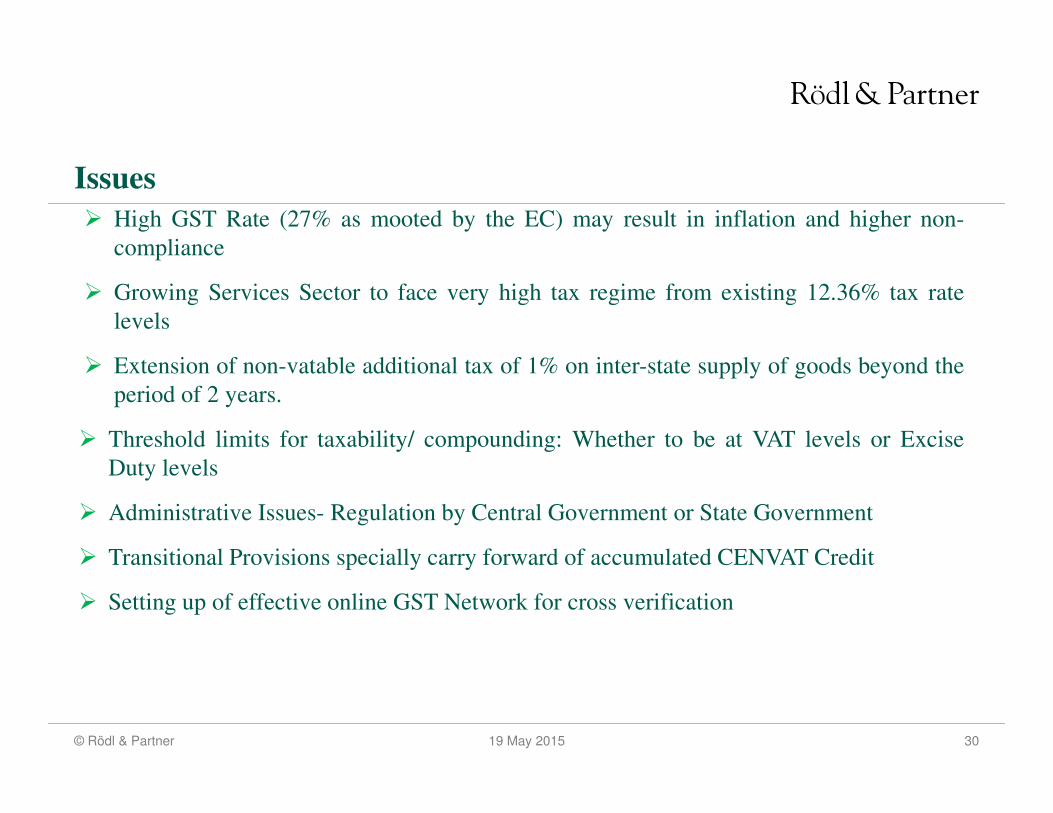

� High GST Rate (27% as mooted by the EC) may result in inflation and higher non-

compliance

� Growing Services Sector to face very high tax regime from existing 12.36% tax rate

levels

� Extension of non-vatable additional tax of 1% on inter-state supply of goods beyond the

period of 2 years.

� Threshold limits for taxability/ compounding: Whether to be at VAT levels or Excise

Duty levels

� Administrative Issues- Regulation by Central Government or State Government

� Transitional Provisions specially carry forward of accumulated CENVAT Credit

� Setting up of effective online GST Network for cross verification

31© Rödl & Partner 19 May 2015

Place of Supply Rules- Proposed

� In the international GST model, place of supply is determined on the basis of supplies

made under Business to Business (B2B) model and Business to Consumer (B2C) model.

� In case of B2B supply, the place of supply is the place where the receiver is located

� In case of B2C model, the place of supplier is the place of supply.

� The above is imperative to affect the concept of destination based GST

� However, under the Indian federal tax system, the said models would undergo significant

changes for certain types of services, such as:

� Immovable property

� Telecommunication service

� Electronic supplied service

� Banking & other financial service

� Intangibles

32© Rödl & Partner 19 May 2015

Summary of GST Impact: Industry wise

Software

� Software exports expected to be Zero Rated as of now.

� For companies paying output taxes of around 25% (Service tax: 12.36% plus VAT:

12.50%), increased in GST rates would not be a challenge. Service providers would have

higher taxes on output.

� The most vexed issue of applicability of both VAT and Service Tax on sale of software/

software license would get resolved.

� Improved input tax credits due to elimination of VAT/ CST

33© Rödl & Partner 19 May 2015

Summary of GST Impact: Industry wiseAuto Sector

� As major sales of auto sector represent inter-state sales, reduction of CST cost and further tax

cascading of VAT charged by dealers would be a benefit.

� Elimination of Excise duty which is presently a cost to the dealers would also be beneficial.

� Requirement of maintaining multiple warehouses in separate states in order to avoid CST on

interstate sales would not be required as IGST charged on interstate sales would be available as

input tax credit to the customers without any restriction.

� No need of undertaking complex transactions such as in-transit sales which involved paper-

work and possibility of disallowance by tax department

� Reduced compliances and simplified duty structure

� Reduction of input tax credits on account of interstate stock transfers would not be required.

� Some exemptions enjoyed by the auto sector (like tractors etc) are expected to be repealed.

� Lack of clarity about treatment of GST under the Packaged Scheme of Incentives.

34© Rödl & Partner 19 May 2015

Summary of GST Impact: Industry wise

Transportation Industry

� To become costlier due to increase in output taxes (IGST Vs Service Tax)

� As petroleum products are kept outside the purview of GST, input taxes paid on such

procurements would become a cost resulting in higher tax costs in the supply chain.

Coal & Electricity

� Lack of clarity on treatment of electricity as the same has not been specifically excluded

from GST- Double Taxation (GST + Electricity Duty)

� Electricity duty would continue to be cost to all consumers.

� Including coal within GST ambit without subsuming electricity duty would contribute to

hike in prices.

35© Rödl & Partner 19 May 2015

Summary of GST Impact: Industry wise

Pharma

� The issue of inverted duty structure for most pharma companies would be addressed as

inputs were being taxed at higher rates as compared to output taxes on medicines.

� GST is expected to bring an end to area based exemption. With taxes on the output, input

taxes would be available.

� Due to the proposed use of HSN Tariff, classification issues for chemicals may continue.

36© Rödl & Partner 19 May 2015

Q&A

Questions Discussion

37© Rödl & Partner 19 May 2015

As an integrated professional services firm, Rödl & Partner is active at 102 wholly-owned locations in 46 countries. It owes its dynamic success in the service lines audit, legal, management and IT consulting, tax consulting as well as tax declaration and BPO to 3,700 entrepreneurial minded partners and colleagues. In close collaboration with our clients we develop information for well-founded decisions that we implement together – both nationally and internationally. In India, Rödl & Partner is providing services through subsidiaries of the German based Rödl & Partner Group

Rödl & Partner

Rechtsanwaltsgesellschaft Steuerberatungsgesellschaft mbH –

Nuremberg/ Germany

Contact Person: Martin WörleinTilmann Ruppert

Äußere Sulzbacher Straße 10090491 NurembergPhone: +49 (911) 91 93-3125E-Mail: [email protected]

Roedl & Partner India Pvt. Ltd. – Delhi

Contact Person: Michael WekezerUnit No. 4, German Centre, 12th Floor, Building 9B,DLF Cyber City, Phase III, Gurgaon-122 002,Phone: +91 (124) 4 83 75 50E-Mail: [email protected]

Roedl & Partner India Pvt. Ltd. – Mumbai

Contact Person: Rahul Oza3rd floor, Dev Nibiru,Linking RoadKhar (W), Mumbai-400052,Phone: +91 (22) 42 33 18 18E-Mail: [email protected]

Roedl & Partner Consulting Private Limited – Pune

Contact Person: Rahul Oza307/308, Lunkad Sky Vista, New Airport Road,Viman Nagar, Pune-411 014,Phone: +91 (20) 6625 7100E-Mail: [email protected]

38© Rödl & Partner 19 May 2015

We and the Castellers of Barcelona

The human-towers are like us:“Everyone counts“