self generation and consumption of solar...

TRANSCRIPT

Self Generation and

Consumption of

Solar Energy

Drivers

Rationale

Models

Enablers

Enerparc AG

Incorporated in 2008 Development in USA Strong EPC Team

IPP (880MW) EPC (1400MW) O&M(950MW)

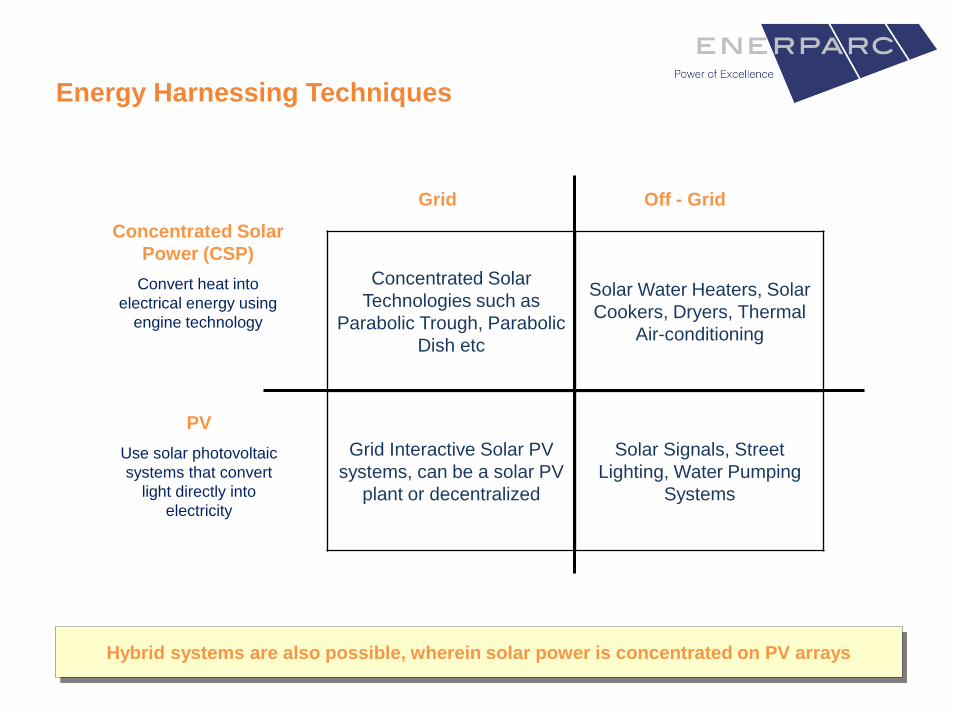

Concentrated Solar

Technologies such as

Parabolic Trough, Parabolic

Dish etc

Solar Water Heaters, Solar

Cookers, Dryers, Thermal

Air-conditioning

Grid Interactive Solar PV

systems, can be a solar PV

plant or decentralized

Solar Signals, Street

Lighting, Water Pumping

Systems

Concentrated Solar

Power (CSP)

Convert heat into

electrical energy using

engine technology

PV

Use solar photovoltaic

systems that convert

light directly into

electricity

Grid Off - Grid

Hybrid systems are also possible, wherein solar power is concentrated on PV arrays

Energy Harnessing Techniques

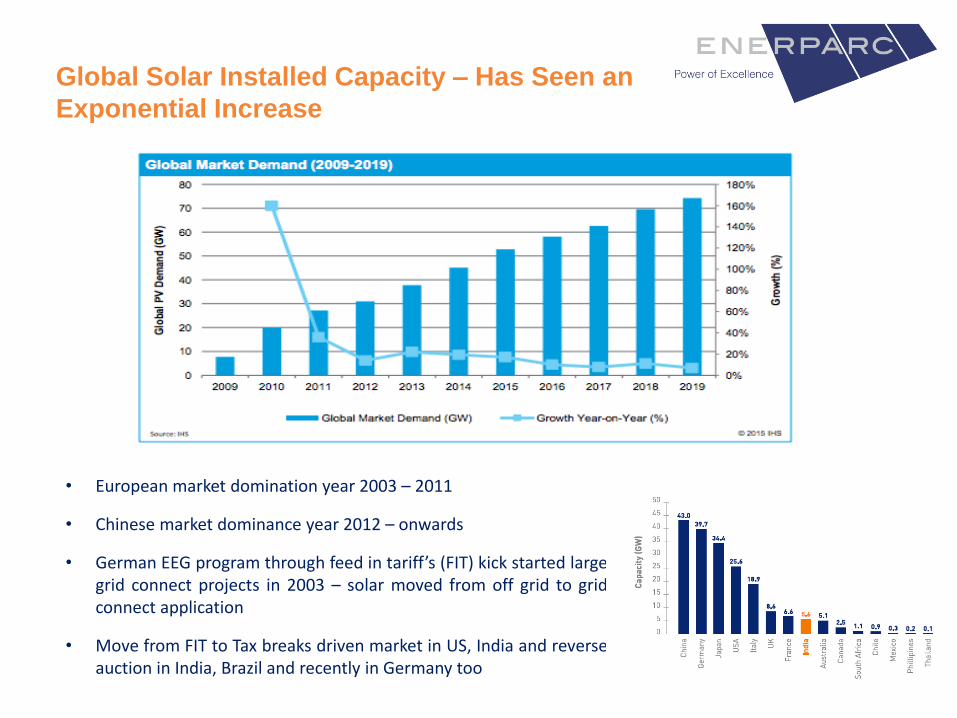

• European market domination year 2003 – 2011

• Chinese market dominance year 2012 – onwards

• German EEG program through feed in tariff’s (FIT) kick started largegrid connect projects in 2003 – solar moved from off grid to gridconnect application

• Move from FIT to Tax breaks driven market in US, India and reverseauction in India, Brazil and recently in Germany too

Global Solar Installed Capacity – Has Seen an

Exponential Increase

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

0

500

1000

1500

2000

2500

3000

3500

4000

2010 2011 2012 2013 2014 2015 2016 e

Cu

mu

lati

ve M

W

MW

Utility C&I Cumulative

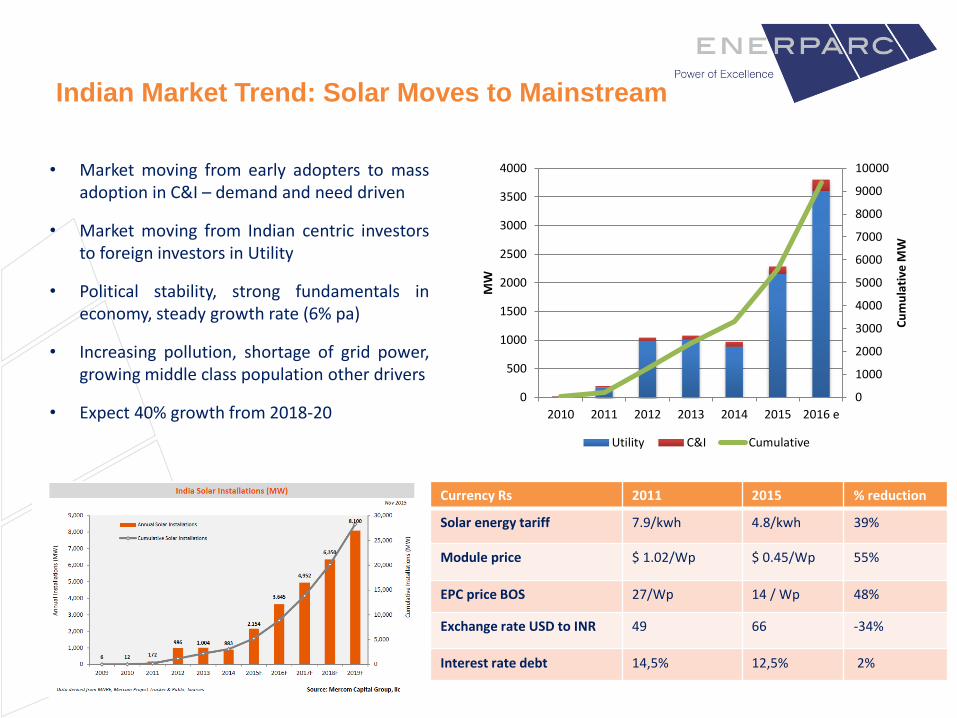

• Market moving from early adopters to massadoption in C&I – demand and need driven

• Market moving from Indian centric investorsto foreign investors in Utility

• Political stability, strong fundamentals ineconomy, steady growth rate (6% pa)

• Increasing pollution, shortage of grid power,growing middle class population other drivers

• Expect 40% growth from 2018-20

Currency Rs 2011 2015 % reduction

Solar energy tariff 7.9/kwh 4.8/kwh 39%

Module price $ 1.02/Wp $ 0.45/Wp 55%

EPC price BOS 27/Wp 14 / Wp 48%

Exchange rate USD to INR 49 66 -34%

Interest rate debt 14,5% 12,5% 2%

Indian Market Trend: Solar Moves to Mainstream

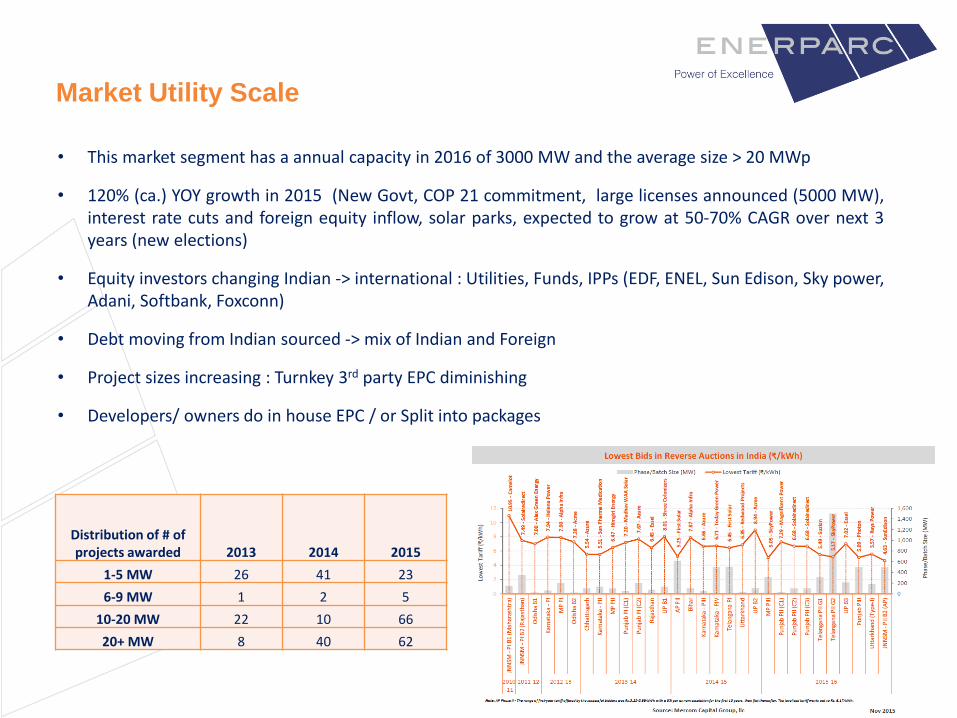

• This market segment has a annual capacity in 2016 of 3000 MW and the average size > 20 MWp

• 120% (ca.) YOY growth in 2015 (New Govt, COP 21 commitment, large licenses announced (5000 MW),interest rate cuts and foreign equity inflow, solar parks, expected to grow at 50-70% CAGR over next 3years (new elections)

• Equity investors changing Indian -> international : Utilities, Funds, IPPs (EDF, ENEL, Sun Edison, Sky power,Adani, Softbank, Foxconn)

• Debt moving from Indian sourced -> mix of Indian and Foreign

• Project sizes increasing : Turnkey 3rd party EPC diminishing

• Developers/ owners do in house EPC / or Split into packages

Distribution of # of projects awarded 2013 2014 2015

1-5 MW 26 41 23

6-9 MW 1 2 5

10-20 MW 22 10 66

20+ MW 8 40 62

Market Utility Scale

10

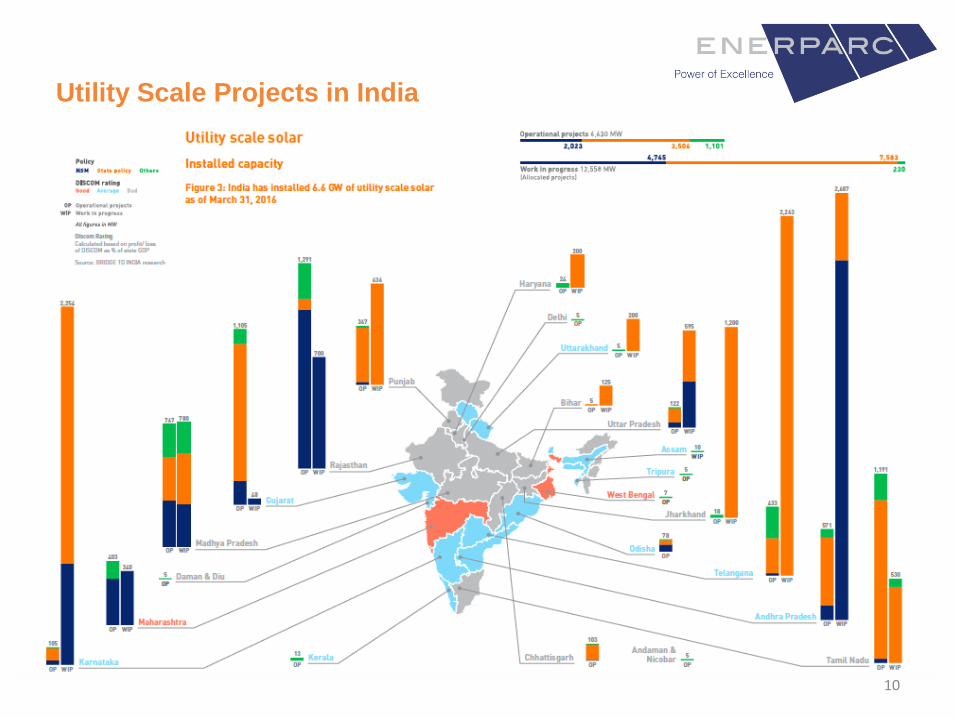

Utility Scale Projects in India

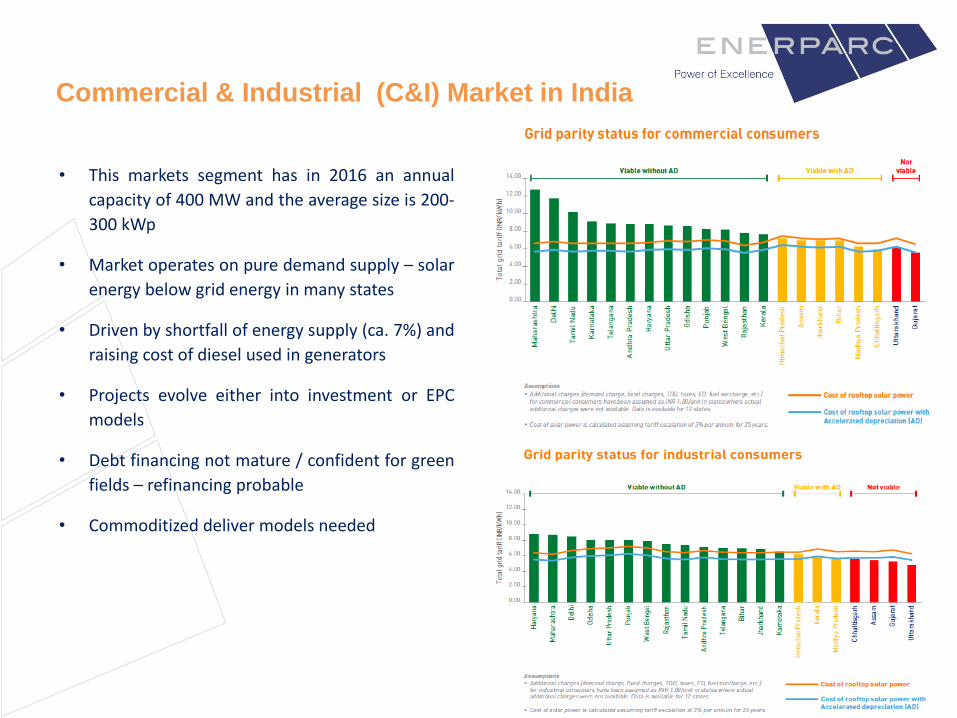

• This markets segment has in 2016 an annual

capacity of 400 MW and the average size is 200-

300 kWp

• Market operates on pure demand supply – solar

energy below grid energy in many states

• Driven by shortfall of energy supply (ca. 7%) and

raising cost of diesel used in generators

• Projects evolve either into investment or EPC

models

• Debt financing not mature / confident for green

fields – refinancing probable

• Commoditized deliver models needed

Commercial & Industrial (C&I) Market in India

12

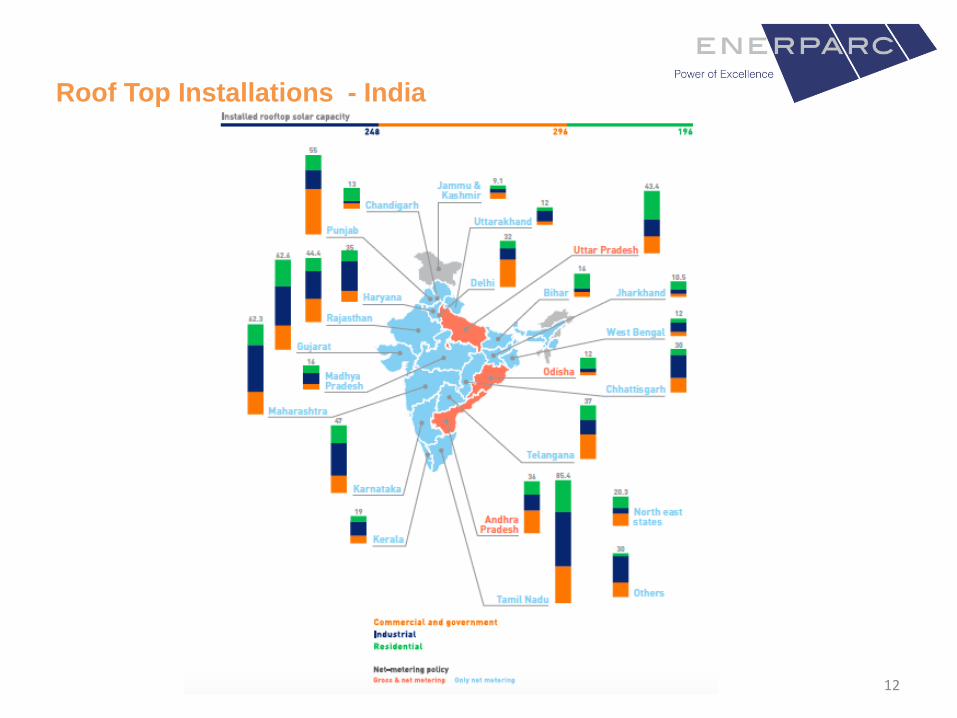

Roof Top Installations - India

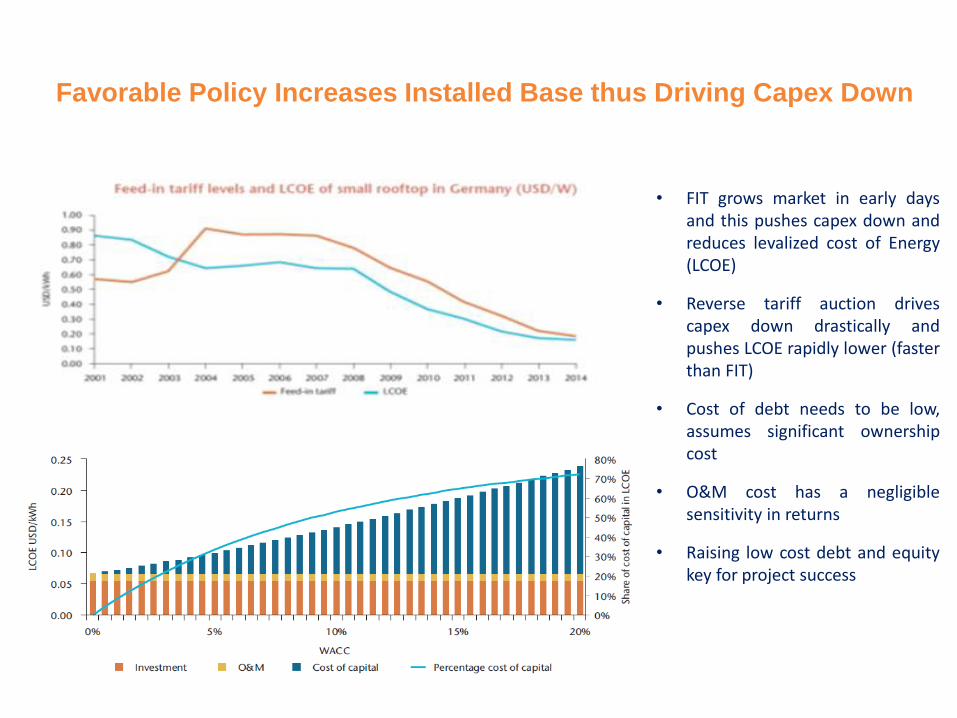

• FIT grows market in early daysand this pushes capex down andreduces levalized cost of Energy(LCOE)

• Reverse tariff auction drivescapex down drastically andpushes LCOE rapidly lower (fasterthan FIT)

• Cost of debt needs to be low,assumes significant ownershipcost

• O&M cost has a negligiblesensitivity in returns

• Raising low cost debt and equitykey for project success

Favorable Policy Increases Installed Base thus Driving Capex Down

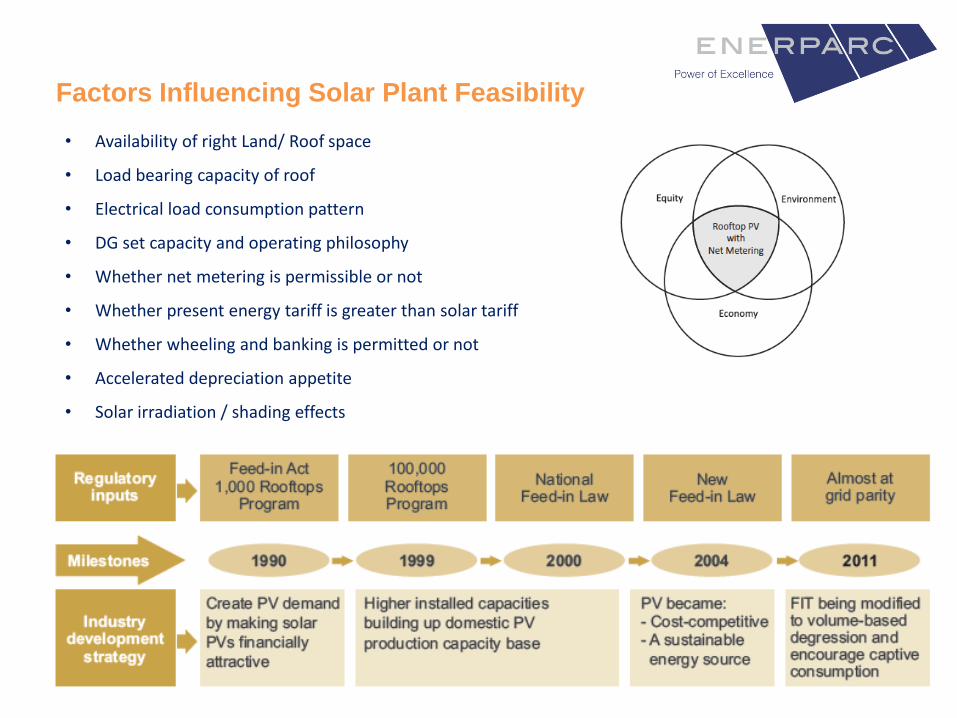

• Availability of right Land/ Roof space

• Load bearing capacity of roof

• Electrical load consumption pattern

• DG set capacity and operating philosophy

• Whether net metering is permissible or not

• Whether present energy tariff is greater than solar tariff

• Whether wheeling and banking is permitted or not

• Accelerated depreciation appetite

• Solar irradiation / shading effects

Factors Influencing Solar Plant Feasibility

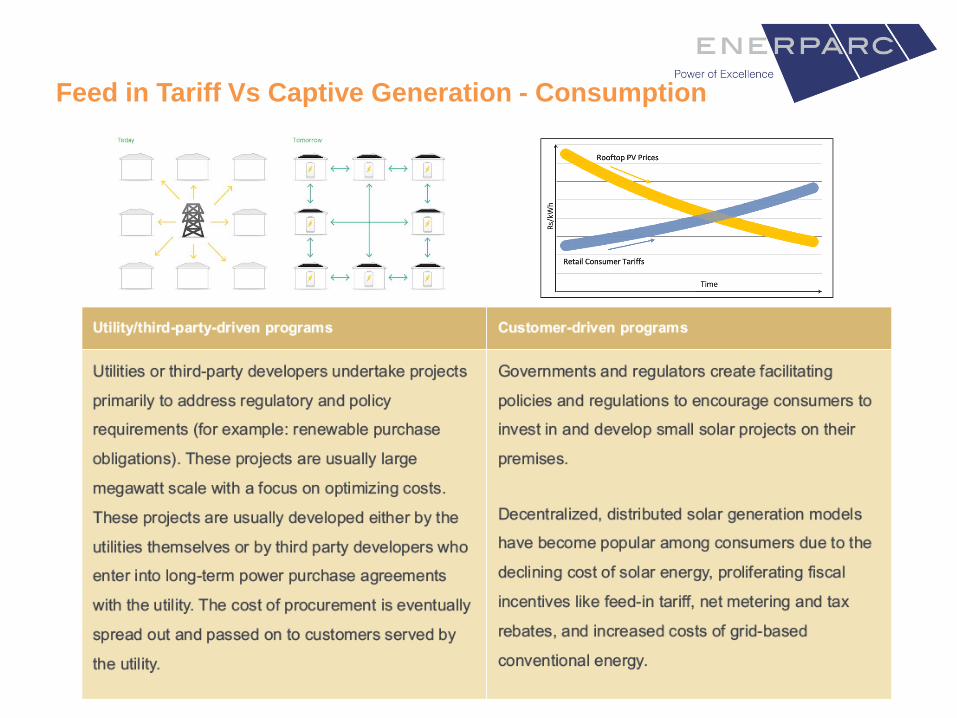

Feed in Tariff Vs Captive Generation - Consumption

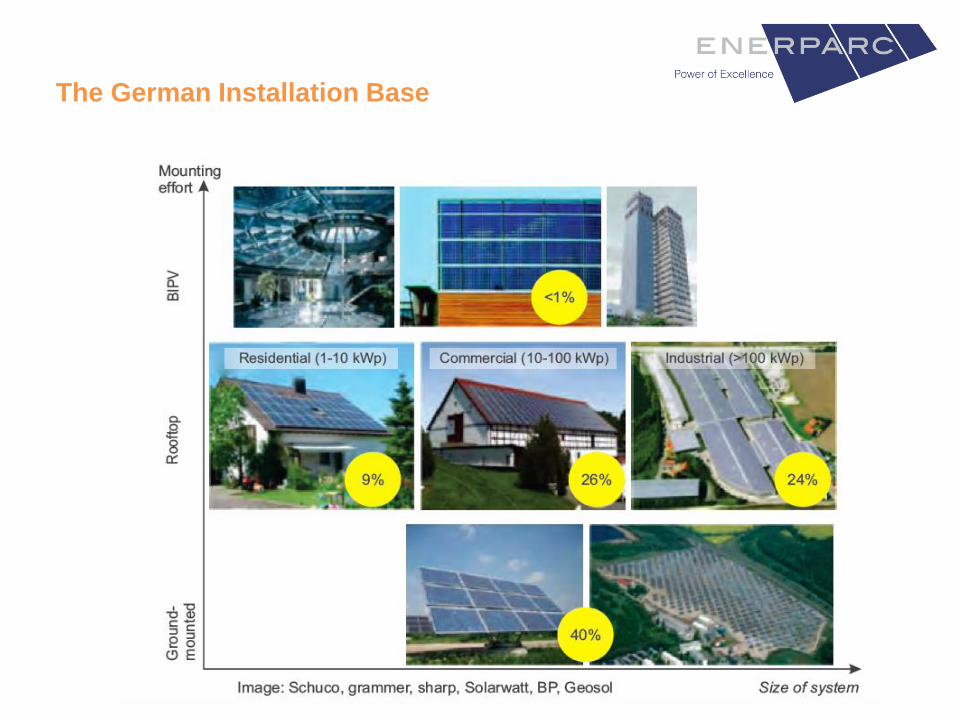

The German Installation Base

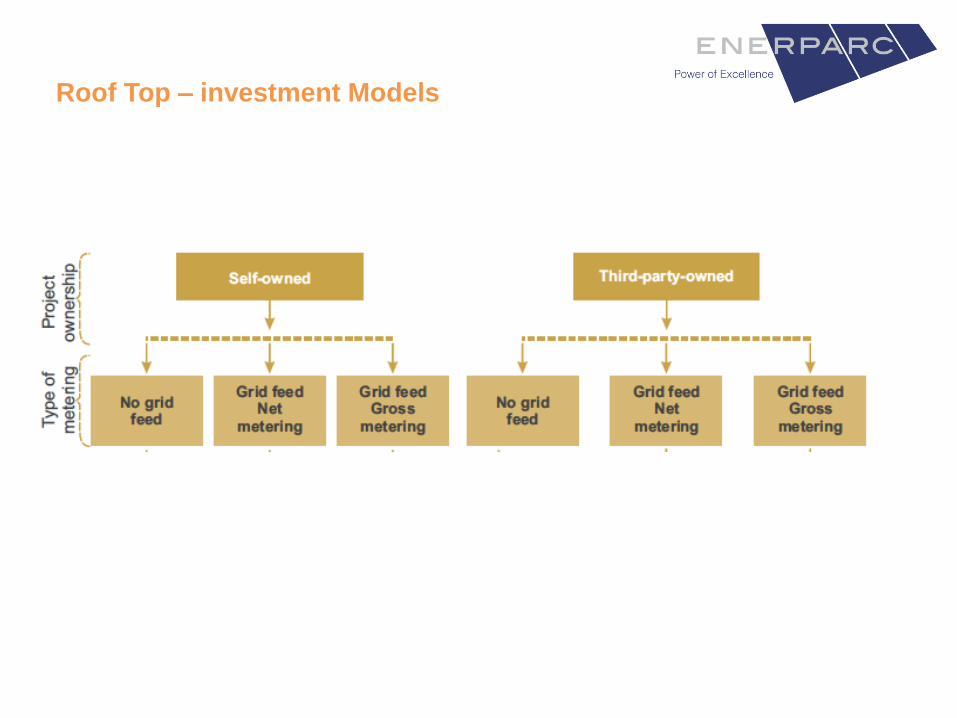

Roof Top – investment Models

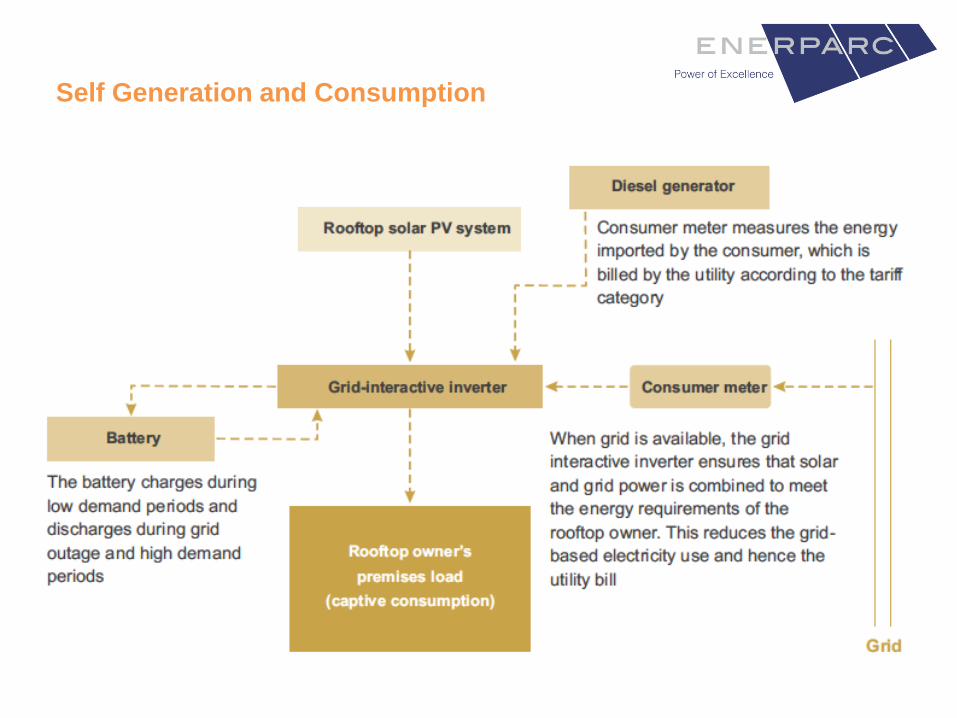

Self Generation and Consumption

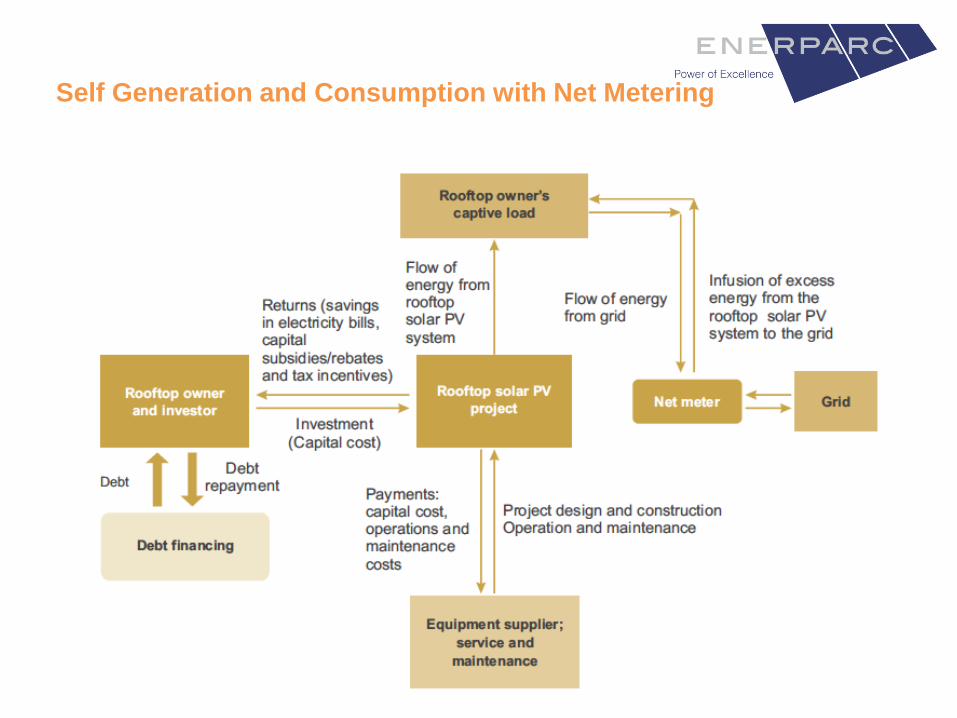

Self Generation and Consumption with Net Metering

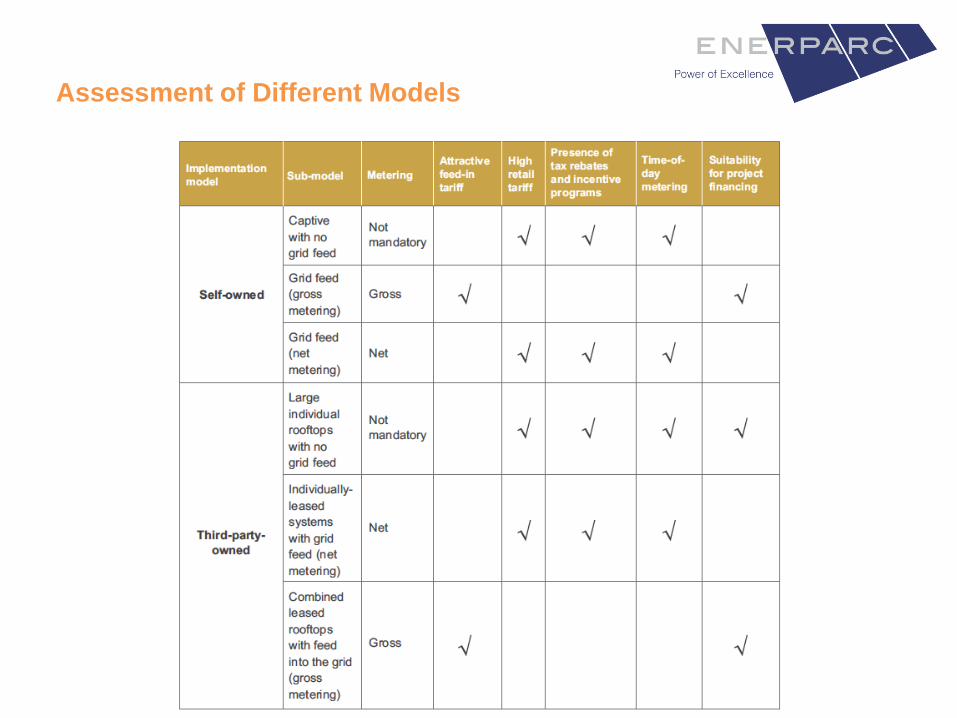

Assessment of Different Models

Your Partner in Creating a Greener World