pembrokeshire business survey

DESCRIPTION

The Pembrokeshire Business Survey was commissioned by Pembrokeshire County Council to measure the attitudes and opinions of small and medium sized businesses in the county to current economic and business conditions.TRANSCRIPT

Pembrokeshire Business Survey 2012

A report by Wavehill

May 2012

©Copyright Wavehill Ltd 2012 Page | 1

Contents 1. Introduction ................................................................................................................... 2

2. Method .......................................................................................................................... 6

3. About your Business ...................................................................................................... 9

4. Business Confidence .................................................................................................... 15

5. Business Support .......................................................................................................... 22

6. Business Premises ........................................................................................................ 26

7. Information Technology ............................................................................................... 27

8. Marketing and Advertising ........................................................................................... 29

9. Business Values ............................................................................................................ 33

10. Workforce .................................................................................................................... 35

11. Local Supply Chain ....................................................................................................... 40

12. Cost Management ........................................................................................................ 43

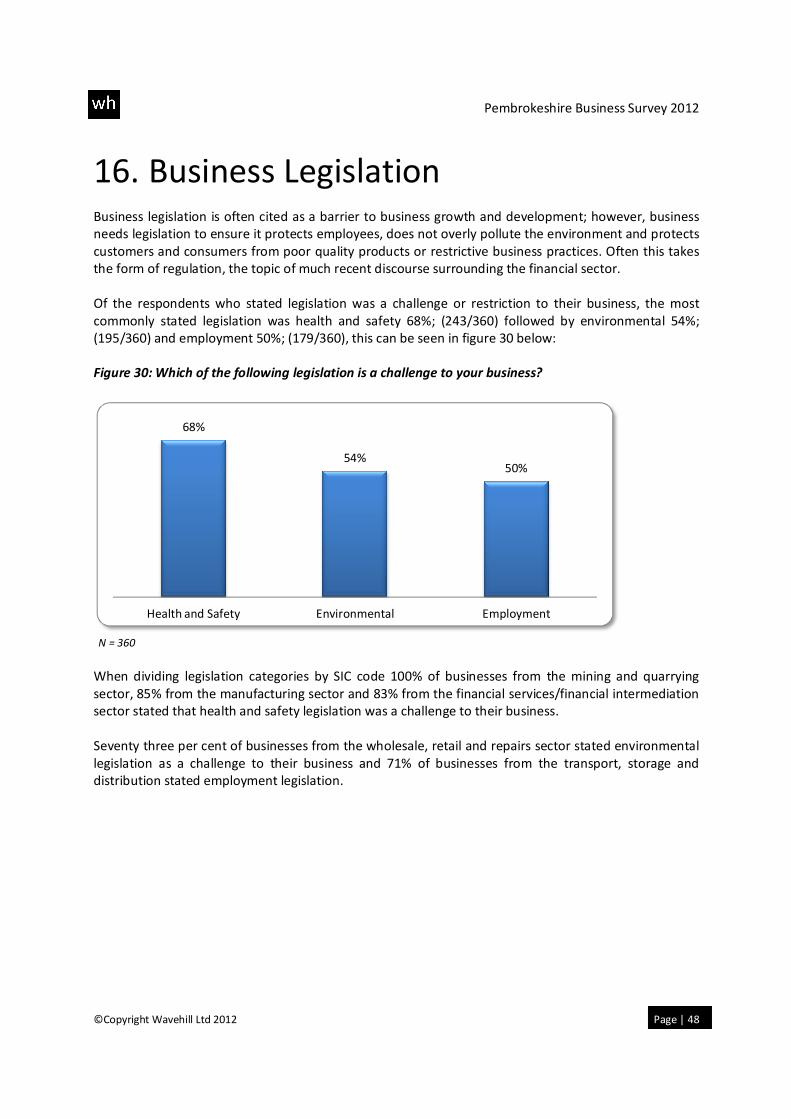

13. Infrastructure ............................................................................................................... 45

14. Innovation.................................................................................................................... 47

15. Business Legislation ..................................................................................................... 48

Annex 1 – Post Survey Weighting ........................................................................................ 52

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 2

1. Executive Summary The Pembrokeshire Business Survey was commissioned by Pembrokeshire County Council to measure

the attitudes and opinions of small and medium sized businesses in the county to current economic and

business conditions.

The survey was undertaken using telephone interviews during March – May 2012. In total 731

businesses responded. Eighty-five per cent of survey respondents were either business directors,

partners or owners meaning the views and opinions are from business leaders.

In terms of the wider economy the survey was undertaken as the UK economy dipped into recession,

recording negative growth or contraction of -0.2% of Gross Domestic Product (Office of National

Statistics (ONS); Q1; 2012), this has continued with -0.3 recorded in Q2; 2012 and -0.5 in Q3; 2012.

There are some relatively weak indicators and findings within the survey and newer or younger

businesses with fewer revenues appear to be affected more by the recession than larger and longer

established businesses.

The following bullet points are summaries of notable elements and findings from the survey report;

• De-registered businesses have exceeded newly registered businesses since 2009 in Pembrokeshire.

The business attrition rate was -230 across the county.

• There has been a decline in new or young businesses. In 2012 businesses less than 3 years old were

proportionally 5% of the survey, in 2006 and 2003 the proportion was 10% and 13%. There has

been a significant reduction in new younger businesses.

• Longer established businesses and businesses with greater revenues were more optimistic or

confident about the future than smaller businesses that had been trading for less time.

• According to ONS data the Retail Price Index (RPI) has risen 30% from 2003 to today in 2012. The

RPI consists of many elements however a major factor or cost driver is the price of oil as a

commodity for energy and transport. The price of Brent Crude has risen from around $20 (2003) a

barrel to around $115 today.

• Whilst 30% of businesses in the Pembrokeshire survey thought their turnover would increase over

the next 12 months, 39% of businesses in the South Wales Chamber Quarterly Economic Survey

believed this would be the case. The proportions who believed their turnover would decrease over

the next 12 months was consistent across both surveys (26%).

• Fewer Pembrokeshire businesses aim to grow their business over the next two to three years, 58%

compared to 74% from the BIS Small Business Survey 2010.1 Businesses in the Pembrokeshire survey

were also less optimistic about planning for growth than those in the South West Wales survey.

1 http://www.bis.gov.uk/assets/biscore/enterprise/docs/b/11-p74-bis-small-business-survey-2010

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 3

• Businesses scored Business Support services with a 6/10, however there was a wide range of

opinion. This may be explained because businesses that make successful applications for grant

support or business funding support are often satisfied with business support and those that have

applications rejected are dissatisfied.

• When asked to think about using mobile technology and IT in general, 30% of businesses stated

they did not think anything needed to be improved in their business in the next 12 months

(217/713), 20% said they would like better mobile phone coverage and signal (144/713) and 20%

said they would prefer faster broadband (19%; 133/713).

• Forty-six per cent of businesses spent between £1,000 and £5,000, 28% of businesses spent under

£999, and 5% spent more than £23,001 with the largest budgets from hotels and restaurants and

construction. Fifty-nine per cent spent between 81% and 100% of their budget within

Pembrokeshire and only 6% of respondents did not spend any of their budgets within the county.

• Businesses rated quality of service then price as their two most important business values.

• Most businesses (81%) do not have a formal training or development plan, 17% have both a formal

training and a development plan and 3% plan to introduce one in the next 12 months (17/520).

Those businesses that have both a formal training plan and a development plan are mainly from

businesses with a larger average annual turnover; for example 26% of businesses with a turnover of

more than £1 million and 18% of businesses with a turnover of between £501,000 and £1,000,000

had both a formal training and a development plan.

• Businesses said that 60% of revenues or turnover come from Pembrokeshire, 19% come from Wales

(not including Pembrokeshire) 18% come from the UK (not including Wales) and 3% worldwide.

• Businesses said that fuel and energy costs (28%), staff costs (28%) and rent and rates (22%) are the

most significant costs affecting their businesses.

• Twenty-three per cent of businesses said that the transport infrastructure in Pembrokeshire does

affect the competitiveness of their business.

• Thirty-two per cent of businesses said that they had introduced new or significantly improved

products or services in the last 12 months.

• Businesses felt that health and safety (68%), environmental (54%) and employment (50%) legislation

was a challenge or restriction to their business.

We would like to thank all of the businesses in Pembrokeshire who gave their time freely to help make

this survey so detailed and interesting.

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 4

2. Introduction The Pembrokeshire Business Survey was first commissioned in 2003 by Pembrokeshire County Council

to measure the attitudes and opinions of small and medium sized businesses in the county to current

economic and business conditions. It was undertaken again by Wavehill in 2006 and now repeated in

2012. The findings are used to inform policy decisions within the council and to better understand the

requirements of businesses across the county.

2.1. Background

The exact content of the survey has changed from year to year, but the overarching aim has remained

the same: to collect the views of SMEs on various business factors. The current survey (2012) covers the

following key themes:

• About your business

• Business Confidence

• Business Support

• Business Premises

• Information Technology

• Marketing & Advertising

• Workforce

• Local Supply Chain

• Cost Management

• Infrastructure

• Innovation

The views of businesses will often be a reflection of the economic climate in which they are operating.

The economy has changed significantly since 2008 and there are still significant downward pressures on

business and business growth.

The table below includes a set of economic indicators which were used in the last two reports and

indicate the health and pressures on the economy which entered its first double dip recession since the

1970s in quarter 1 of 2012.

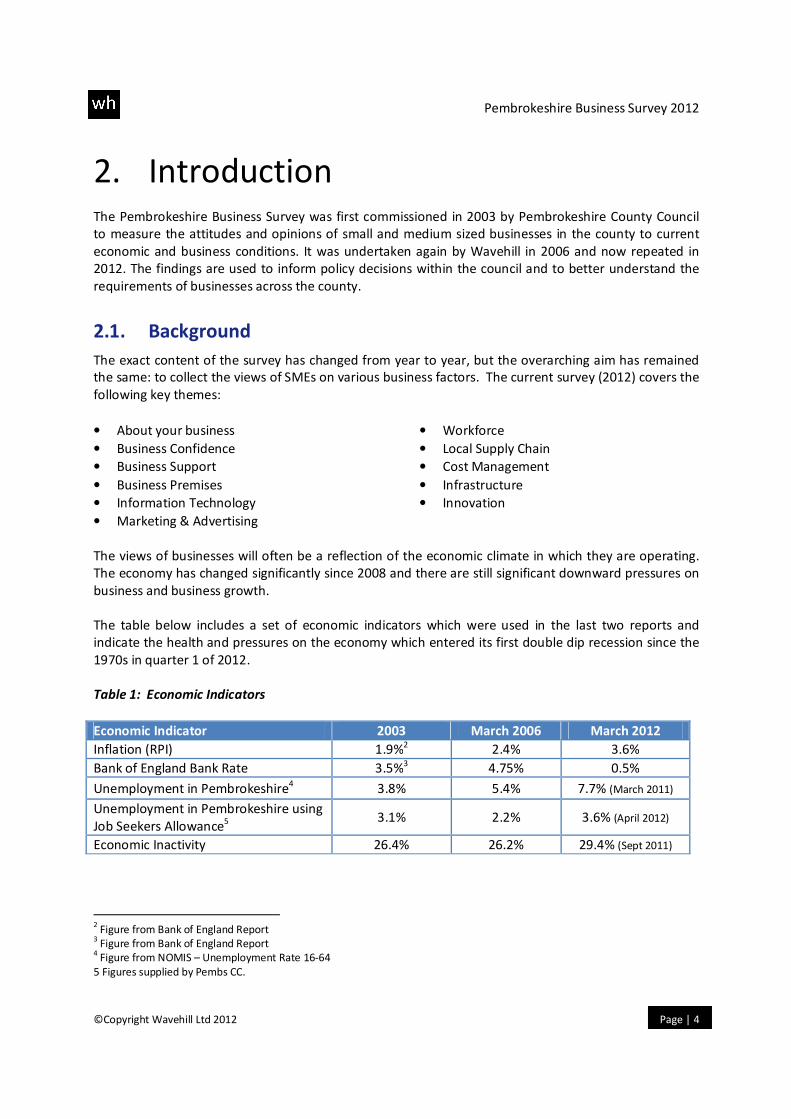

Table 1: Economic Indicators

Economic Indicator 2003 March 2006 March 2012

Inflation (RPI) 1.9%2 2.4% 3.6%

Bank of England Bank Rate 3.5%3 4.75% 0.5%

Unemployment in Pembrokeshire4 3.8% 5.4% 7.7% (March 2011)

Unemployment in Pembrokeshire using

Job Seekers Allowance5

3.1% 2.2% 3.6% (April 2012)

Economic Inactivity 26.4% 26.2% 29.4% (Sept 2011)

2 Figure from Bank of England Report

3 Figure from Bank of England Report

4 Figure from NOMIS – Unemployment Rate 16-64

5 Figures supplied by Pembs CC.

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 5

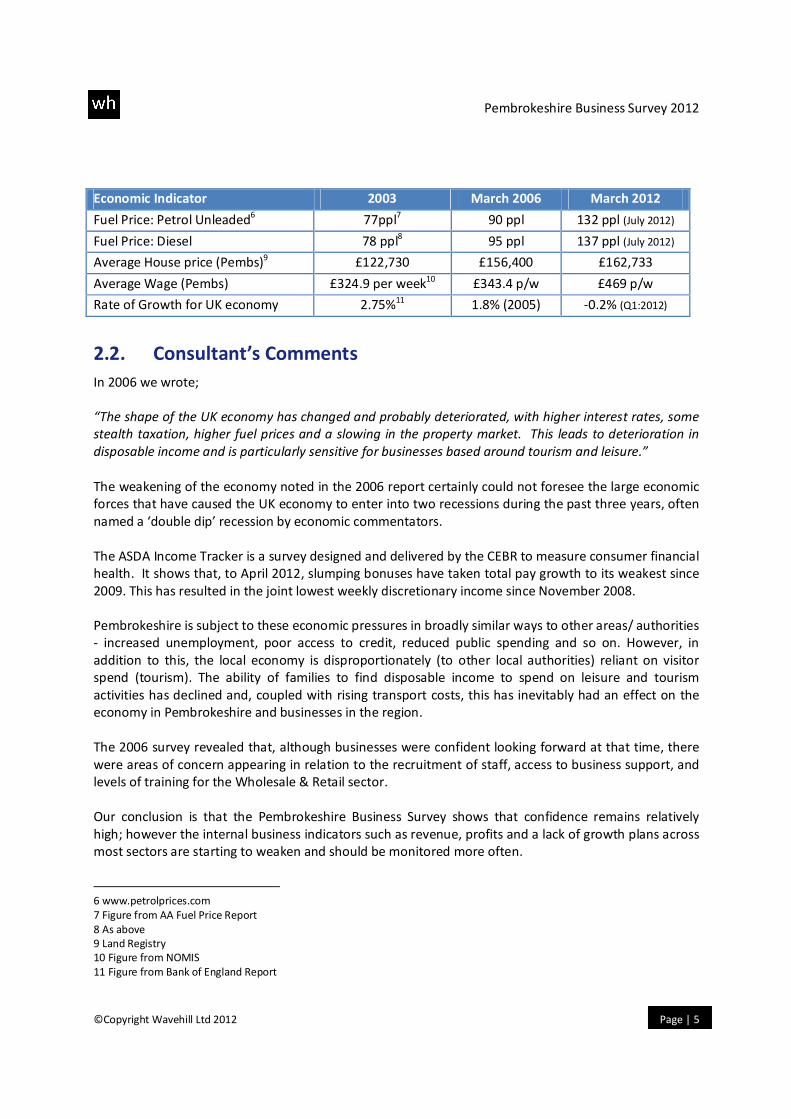

Economic Indicator 2003 March 2006 March 2012

Fuel Price: Petrol Unleaded6 77ppl

7 90 ppl 132 ppl (July 2012)

Fuel Price: Diesel 78 ppl8 95 ppl 137 ppl (July 2012)

Average House price (Pembs)9 £122,730 £156,400 £162,733

Average Wage (Pembs) £324.9 per week10 £343.4 p/w £469 p/w

Rate of Growth for UK economy 2.75%11 1.8% (2005) -0.2% (Q1:2012)

2.2. Consultant’s Comments

In 2006 we wrote;

“The shape of the UK economy has changed and probably deteriorated, with higher interest rates, some

stealth taxation, higher fuel prices and a slowing in the property market. This leads to deterioration in

disposable income and is particularly sensitive for businesses based around tourism and leisure.”

The weakening of the economy noted in the 2006 report certainly could not foresee the large economic

forces that have caused the UK economy to enter into two recessions during the past three years, often

named a ‘double dip’ recession by economic commentators.

The ASDA Income Tracker is a survey designed and delivered by the CEBR to measure consumer financial

health. It shows that, to April 2012, slumping bonuses have taken total pay growth to its weakest since

2009. This has resulted in the joint lowest weekly discretionary income since November 2008.

Pembrokeshire is subject to these economic pressures in broadly similar ways to other areas/ authorities

- increased unemployment, poor access to credit, reduced public spending and so on. However, in

addition to this, the local economy is disproportionately (to other local authorities) reliant on visitor

spend (tourism). The ability of families to find disposable income to spend on leisure and tourism

activities has declined and, coupled with rising transport costs, this has inevitably had an effect on the

economy in Pembrokeshire and businesses in the region.

The 2006 survey revealed that, although businesses were confident looking forward at that time, there

were areas of concern appearing in relation to the recruitment of staff, access to business support, and

levels of training for the Wholesale & Retail sector.

Our conclusion is that the Pembrokeshire Business Survey shows that confidence remains relatively

high; however the internal business indicators such as revenue, profits and a lack of growth plans across

most sectors are starting to weaken and should be monitored more often.

6 www.petrolprices.com

7 Figure from AA Fuel Price Report

8 As above

9 Land Registry

10 Figure from NOMIS

11 Figure from Bank of England Report

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 6

3. Methodology The 2012 Pembrokeshire Business Survey is based somewhat on the previous surveys (2003, 2006),

although elements have changed meaning the 2012 survey it is not directly comparable with previous

years.

The survey itself was designed over several versions or iterations and the survey design team discussed

the inclusion of certain questions and themes carefully. One new aspect to the 2012 survey was the

inclusion of validation questions. These are questions that are found in other surveys, and allow us to

‘test’ whether the Pembrokeshire survey respondents differ from the views of other businesses in other

surveys. This is known as ‘survey validation’ within the technical and academic literature.

In our survey we have used the same wording and response categories to enable a direct comparison to

be made. The surveys that we extracted questions to harmonise from were:

• Pembrokeshire Business Survey (2006) Wavehill

• South Wales Chamber Survey (2011)

• CBI Economic Challenges Facing UK Businesses Survey (2011)

• Small Business Survey (2010)

• The Welsh Rural Observatory Business Survey (2008)

We then tested the questionnaire amongst staff and measured the timings on the survey. The survey

was reduced in length as it was thought to be too long for many businesses, the target time to

completion being 20 minutes.

The sample for the survey was taken from the Dunn & Bradstreet Business Database for Pembrokeshire.

This provides business data classified using the Standard Industry Classification (SIC 2003). Some

classifications for public services such as employment and social care were excluded from the list. We

then subdivided the list of 1,855 businesses into their business classes and selected a proportional

sample randomly. Selecting a sample randomly allows our statistical analysis to infer from the results of

our sample what the whole business population may think. The accuracy within our estimate is referred

to as the statistical confidence level.

The confidence level varies from question to question depending on the responses, but as an overall

indication of the accuracy of our survey we completed 811 interviews from a population of 1,855

businesses to give a margin of error of +/- 2.6% with a confidence level of 95%. This means that for any

question we can calculate that 95% of business respondents will fall within the answer margins, and one

in twenty (5%) will be outside. This error of margin is generally accepted by social and economic

researchers.

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 7

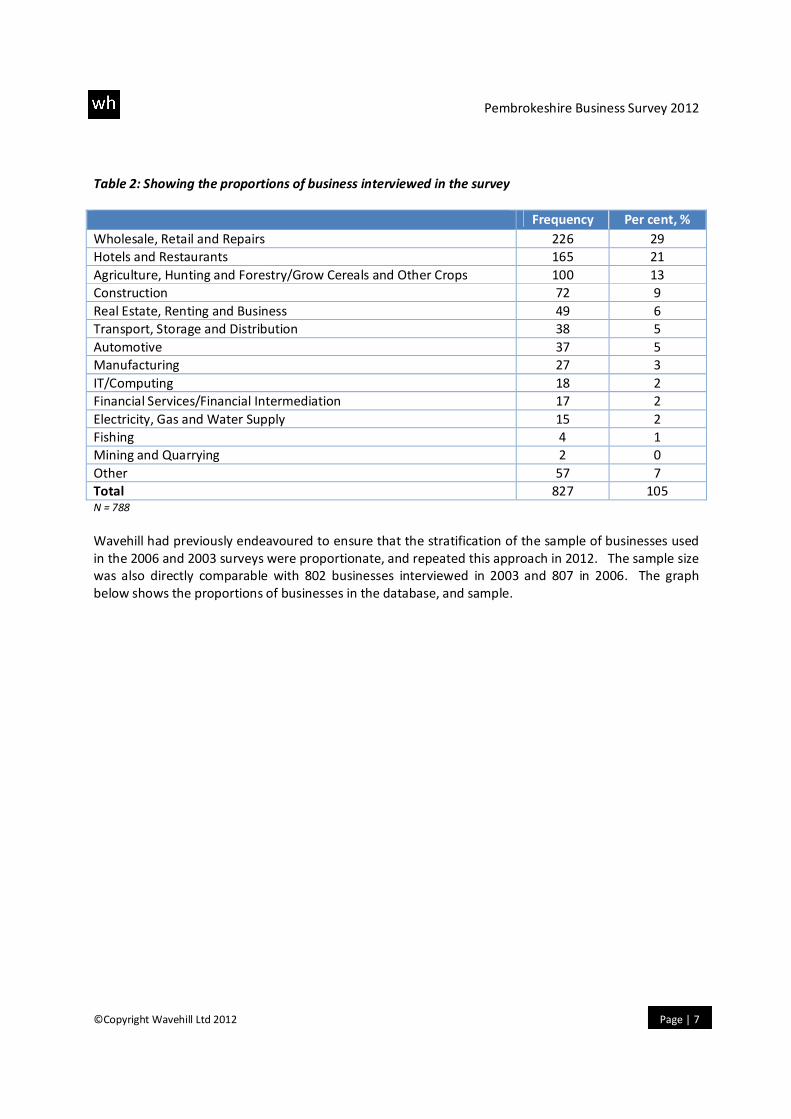

Table 2: Showing the proportions of business interviewed in the survey

Frequency Per cent, %

Wholesale, Retail and Repairs 226 29

Hotels and Restaurants 165 21

Agriculture, Hunting and Forestry/Grow Cereals and Other Crops 100 13

Construction 72 9

Real Estate, Renting and Business 49 6

Transport, Storage and Distribution 38 5

Automotive 37 5

Manufacturing 27 3

IT/Computing 18 2

Financial Services/Financial Intermediation 17 2

Electricity, Gas and Water Supply 15 2

Fishing 4 1

Mining and Quarrying 2 0

Other 57 7

Total 827 105 N = 788

Wavehill had previously endeavoured to ensure that the stratification of the sample of businesses used

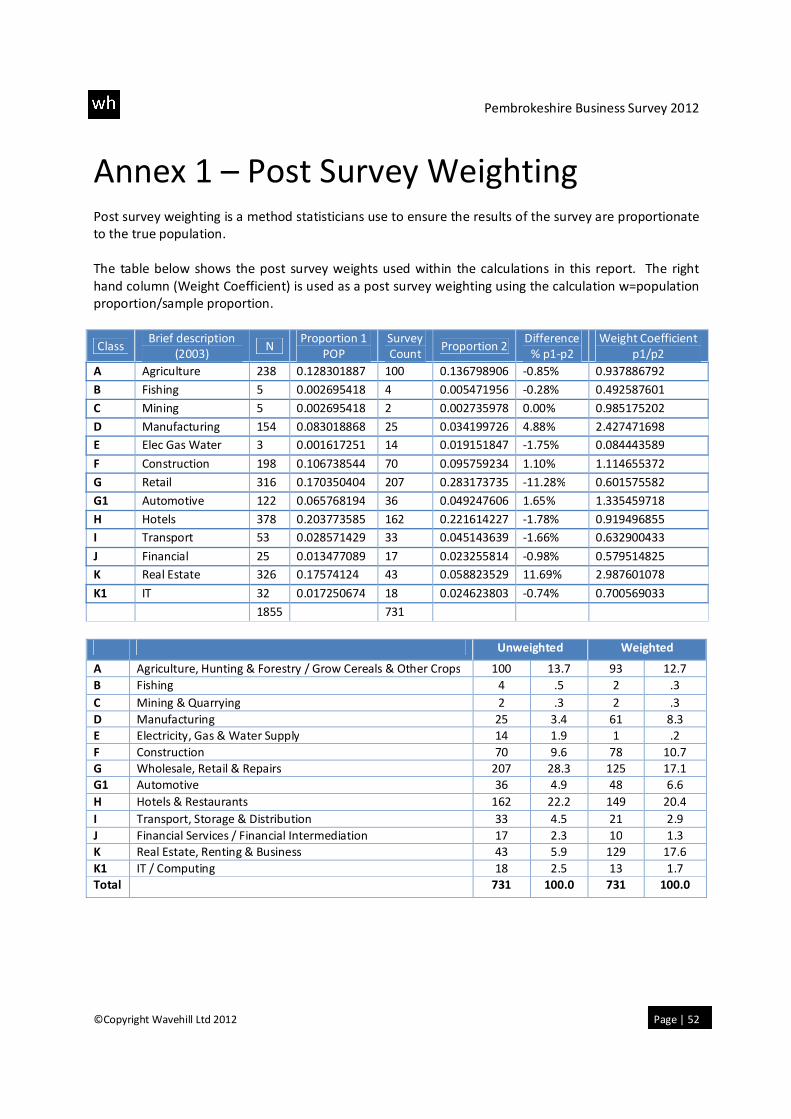

in the 2006 and 2003 surveys were proportionate, and repeated this approach in 2012. The sample size

was also directly comparable with 802 businesses interviewed in 2003 and 807 in 2006. The graph

below shows the proportions of businesses in the database, and sample.

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 8

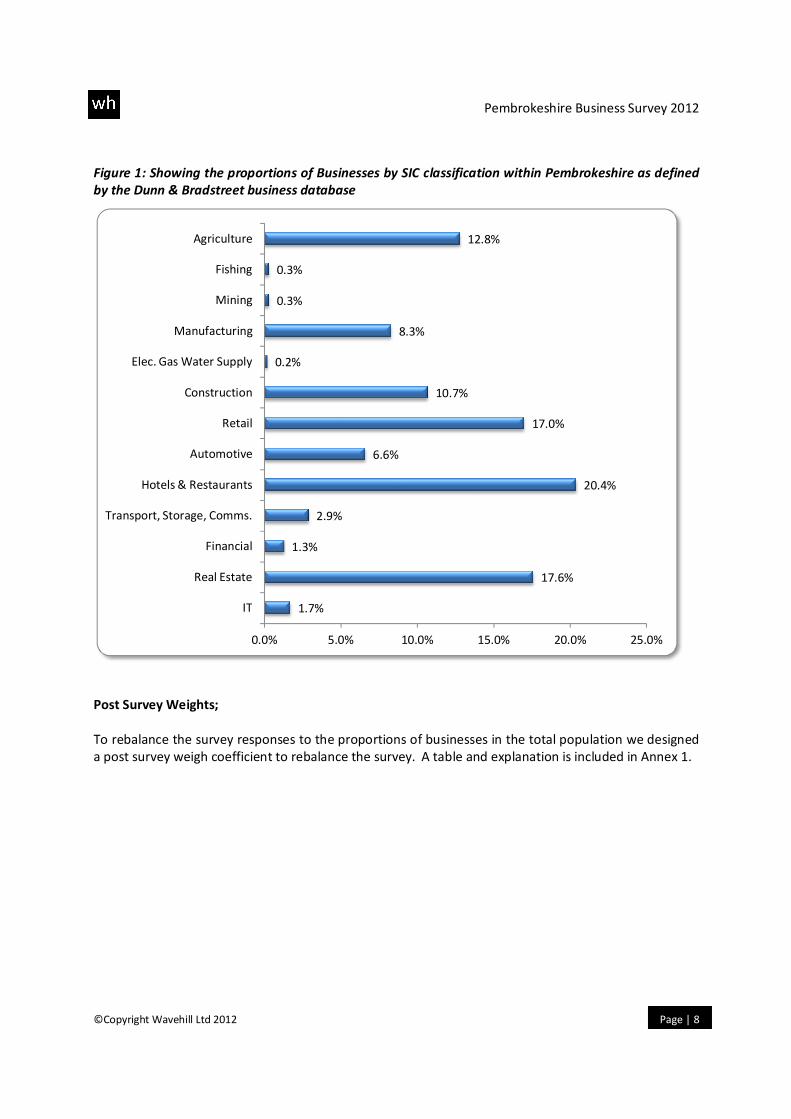

Figure 1: Showing the proportions of Businesses by SIC classification within Pembrokeshire as defined

by the Dunn & Bradstreet business database

Post Survey Weights;

To rebalance the survey responses to the proportions of businesses in the total population we designed

a post survey weigh coefficient to rebalance the survey. A table and explanation is included in Annex 1.

1.7%

17.6%

1.3%

2.9%

20.4%

6.6%

17.0%

10.7%

0.2%

8.3%

0.3%

0.3%

12.8%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

IT

Real Estate

Financial

Transport, Storage, Comms.

Hotels & Restaurants

Automotive

Retail

Construction

Elec. Gas Water Supply

Manufacturing

Mining

Fishing

Agriculture

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 9

4. About your Business The following sections present the data from the survey. The sections start off describing the businesses

in general terms and then specialise into sub chapters that inquire about various business dimensions,

such as workforce, IT and business confidence, for example.

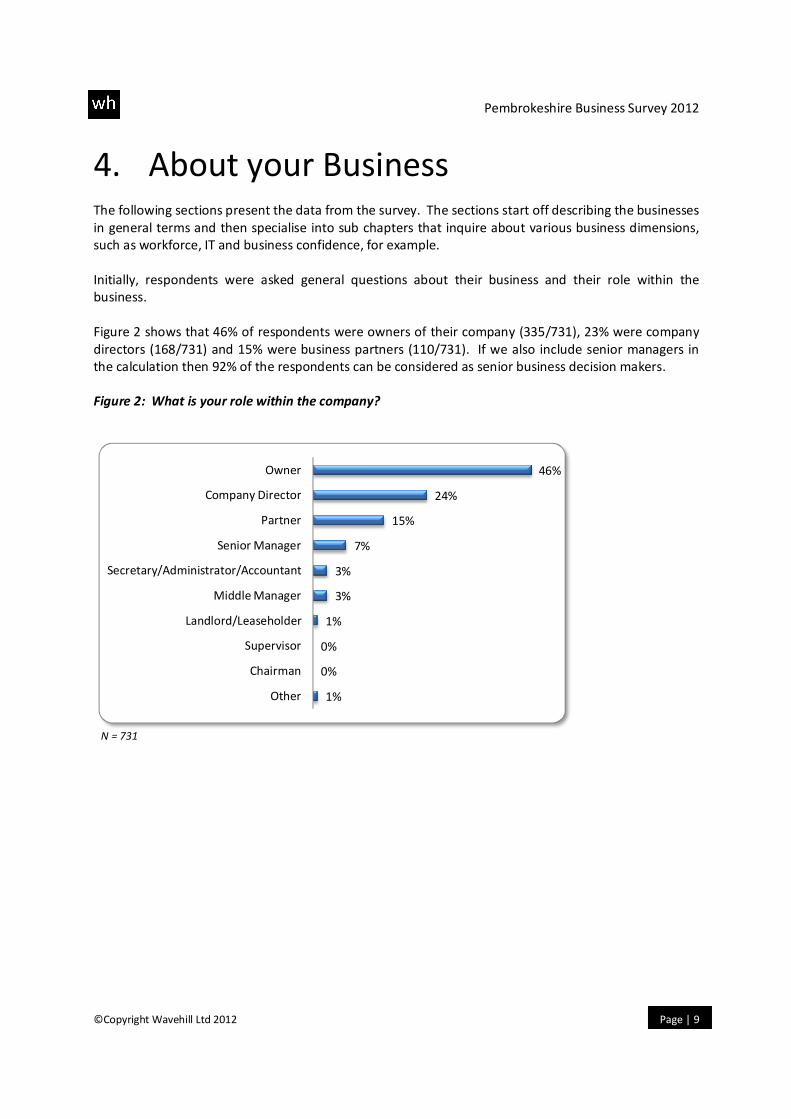

Initially, respondents were asked general questions about their business and their role within the

business.

Figure 2 shows that 46% of respondents were owners of their company (335/731), 23% were company

directors (168/731) and 15% were business partners (110/731). If we also include senior managers in

the calculation then 92% of the respondents can be considered as senior business decision makers.

Figure 2: What is your role within the company?

N = 731

1%

0%

0%

1%

3%

3%

7%

15%

24%

46%

Other

Chairman

Supervisor

Landlord/Leaseholder

Middle Manager

Secretary/Administrator/Accountant

Senior Manager

Partner

Company Director

Owner

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 10

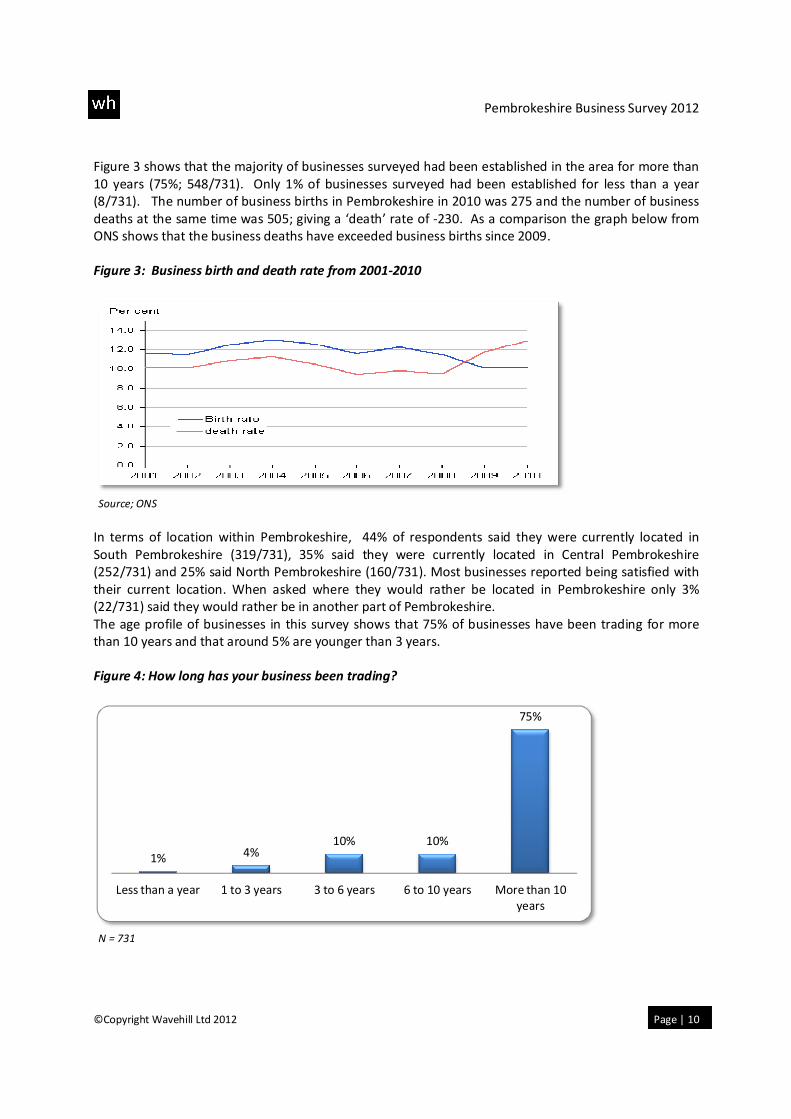

Figure 3 shows that the majority of businesses surveyed had been established in the area for more than

10 years (75%; 548/731). Only 1% of businesses surveyed had been established for less than a year

(8/731). The number of business births in Pembrokeshire in 2010 was 275 and the number of business

deaths at the same time was 505; giving a ‘death’ rate of -230. As a comparison the graph below from

ONS shows that the business deaths have exceeded business births since 2009.

Figure 3: Business birth and death rate from 2001-2010

Source; ONS

In terms of location within Pembrokeshire, 44% of respondents said they were currently located in

South Pembrokeshire (319/731), 35% said they were currently located in Central Pembrokeshire

(252/731) and 25% said North Pembrokeshire (160/731). Most businesses reported being satisfied with

their current location. When asked where they would rather be located in Pembrokeshire only 3%

(22/731) said they would rather be in another part of Pembrokeshire.

The age profile of businesses in this survey shows that 75% of businesses have been trading for more

than 10 years and that around 5% are younger than 3 years.

Figure 4: How long has your business been trading?

N = 731

1% 4%10% 10%

75%

Less than a year 1 to 3 years 3 to 6 years 6 to 10 years More than 10

years

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 11

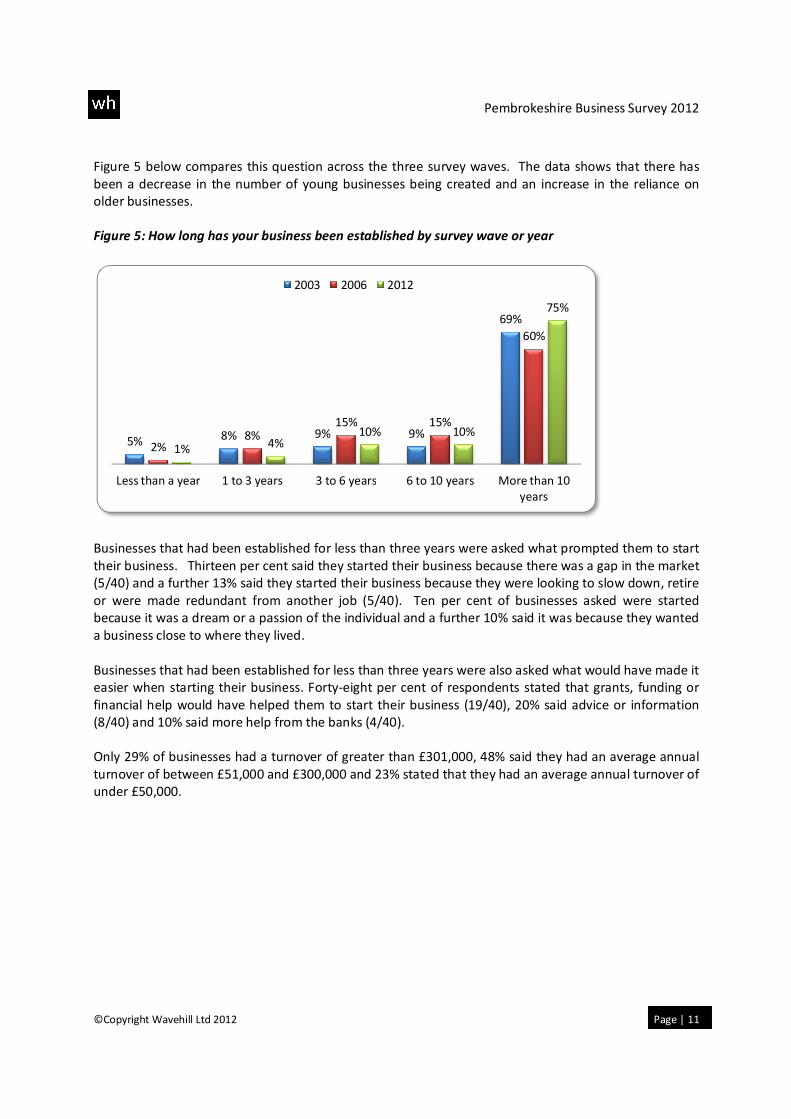

Figure 5 below compares this question across the three survey waves. The data shows that there has

been a decrease in the number of young businesses being created and an increase in the reliance on

older businesses.

Figure 5: How long has your business been established by survey wave or year

Businesses that had been established for less than three years were asked what prompted them to start

their business. Thirteen per cent said they started their business because there was a gap in the market

(5/40) and a further 13% said they started their business because they were looking to slow down, retire

or were made redundant from another job (5/40). Ten per cent of businesses asked were started

because it was a dream or a passion of the individual and a further 10% said it was because they wanted

a business close to where they lived.

Businesses that had been established for less than three years were also asked what would have made it

easier when starting their business. Forty-eight per cent of respondents stated that grants, funding or

financial help would have helped them to start their business (19/40), 20% said advice or information

(8/40) and 10% said more help from the banks (4/40).

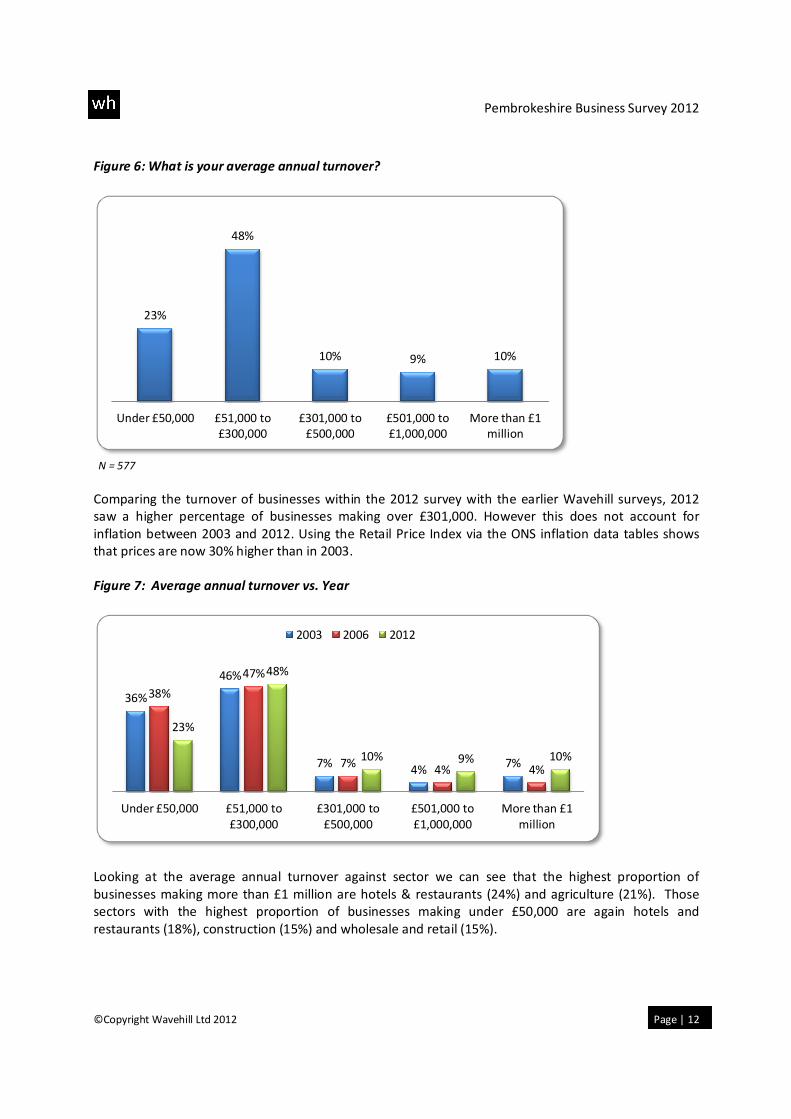

Only 29% of businesses had a turnover of greater than £301,000, 48% said they had an average annual

turnover of between £51,000 and £300,000 and 23% stated that they had an average annual turnover of

under £50,000.

5% 8% 9% 9%

69%

2%8%

15% 15%

60%

1% 4%10% 10%

75%

Less than a year 1 to 3 years 3 to 6 years 6 to 10 years More than 10

years

2003 2006 2012

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 12

Figure 6: What is your average annual turnover?

N = 577

Comparing the turnover of businesses within the 2012 survey with the earlier Wavehill surveys, 2012

saw a higher percentage of businesses making over £301,000. However this does not account for

inflation between 2003 and 2012. Using the Retail Price Index via the ONS inflation data tables shows

that prices are now 30% higher than in 2003.

Figure 7: Average annual turnover vs. Year

Looking at the average annual turnover against sector we can see that the highest proportion of

businesses making more than £1 million are hotels & restaurants (24%) and agriculture (21%). Those

sectors with the highest proportion of businesses making under £50,000 are again hotels and

restaurants (18%), construction (15%) and wholesale and retail (15%).

23%

48%

10% 9% 10%

Under £50,000 £51,000 to

£300,000

£301,000 to

£500,000

£501,000 to

£1,000,000

More than £1

million

36%

46%

7%4%

7%

38%

47%

7%4% 4%

23%

48%

10% 9% 10%

Under £50,000 £51,000 to

£300,000

£301,000 to

£500,000

£501,000 to

£1,000,000

More than £1

million

2003 2006 2012

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 13

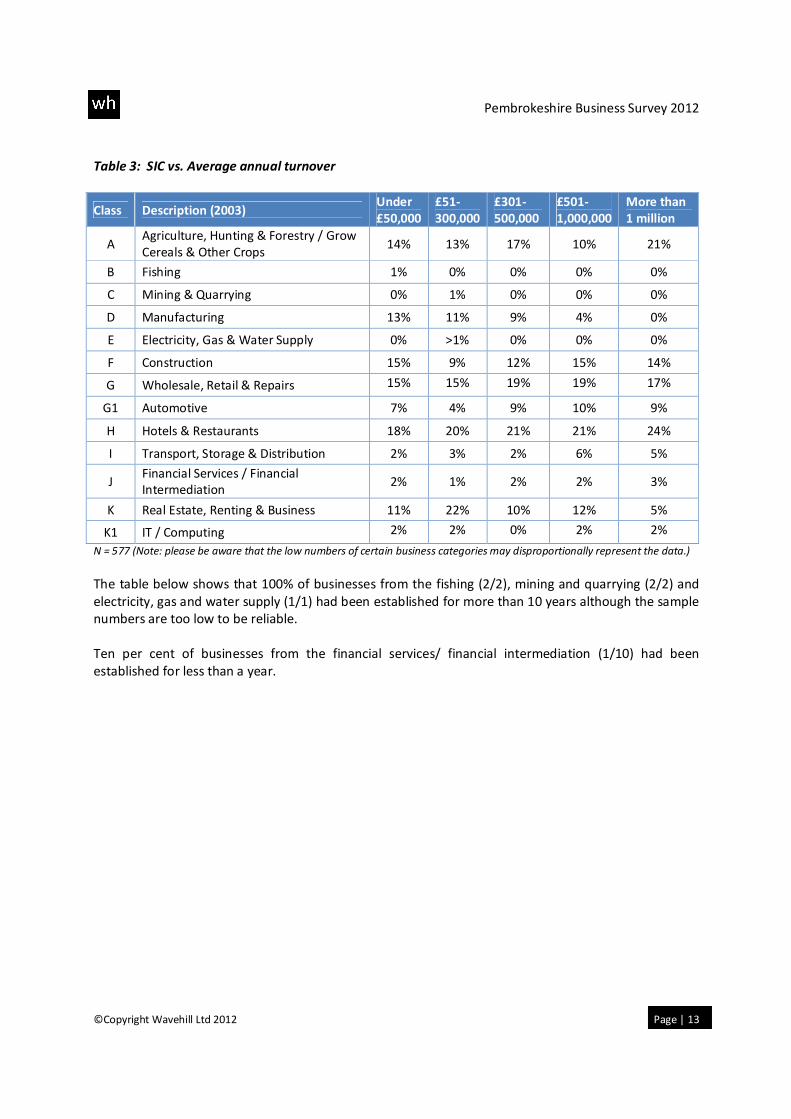

Table 3: SIC vs. Average annual turnover

Class Description (2003) Under

£50,000

£51-

300,000

£301-

500,000

£501-

1,000,000

More than

1 million

A Agriculture, Hunting & Forestry / Grow

Cereals & Other Crops 14% 13% 17% 10% 21%

B Fishing 1% 0% 0% 0% 0%

C Mining & Quarrying 0% 1% 0% 0% 0%

D Manufacturing 13% 11% 9% 4% 0%

E Electricity, Gas & Water Supply 0% >1% 0% 0% 0%

F Construction 15% 9% 12% 15% 14%

G Wholesale, Retail & Repairs 15% 15% 19% 19% 17%

G1 Automotive 7% 4% 9% 10% 9%

H Hotels & Restaurants 18% 20% 21% 21% 24%

I Transport, Storage & Distribution 2% 3% 2% 6% 5%

J Financial Services / Financial

Intermediation 2% 1% 2% 2% 3%

K Real Estate, Renting & Business 11% 22% 10% 12% 5%

K1 IT / Computing 2% 2% 0% 2% 2%

N = 577 (Note: please be aware that the low numbers of certain business categories may disproportionally represent the data.)

The table below shows that 100% of businesses from the fishing (2/2), mining and quarrying (2/2) and

electricity, gas and water supply (1/1) had been established for more than 10 years although the sample

numbers are too low to be reliable.

Ten per cent of businesses from the financial services/ financial intermediation (1/10) had been

established for less than a year.

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 14

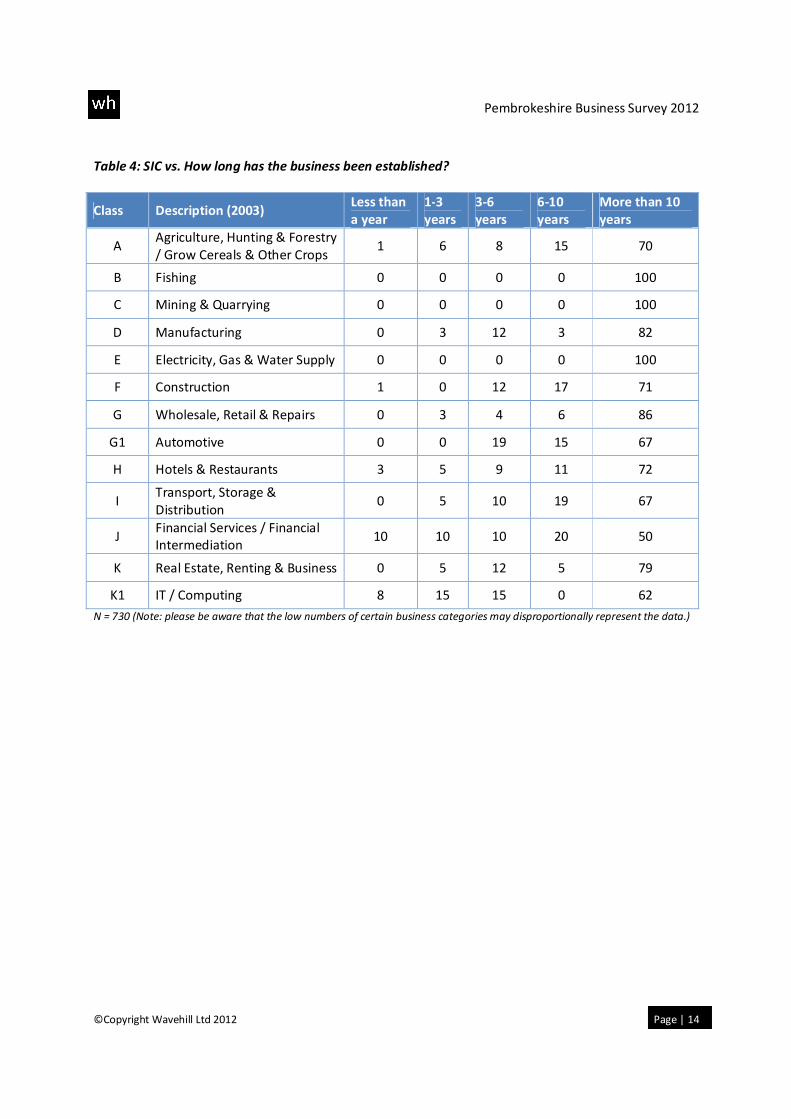

Table 4: SIC vs. How long has the business been established?

Class Description (2003) Less than

a year

1-3

years

3-6

years

6-10

years

More than 10

years

A Agriculture, Hunting & Forestry

/ Grow Cereals & Other Crops 1 6 8 15 70

B Fishing 0 0 0 0 100

C Mining & Quarrying 0 0 0 0 100

D Manufacturing 0 3 12 3 82

E Electricity, Gas & Water Supply 0 0 0 0 100

F Construction 1 0 12 17 71

G Wholesale, Retail & Repairs 0 3 4 6 86

G1 Automotive 0 0 19 15 67

H Hotels & Restaurants 3 5 9 11 72

I Transport, Storage &

Distribution 0 5 10 19 67

J Financial Services / Financial

Intermediation 10 10 10 20 50

K Real Estate, Renting & Business 0 5 12 5 79

K1 IT / Computing 8 15 15 0 62

N = 730 (Note: please be aware that the low numbers of certain business categories may disproportionally represent the data.)

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 15

5. Business Confidence Business confidence is a widely used concept in measuring potential future economic performance, for

this reason it is referred to as a ‘leading indicator’ or a ‘coincident indicator’ (one which leads or is

concurrent with economic conditions). Confident businesses may invest capital, employ more staff or

expand their range of goods, services or geographic market.

When asked to rate Pembrokeshire on a scale of 1 to 10 (1 poor and 10 excellent) as a place to run their

business, the mean score given was 6.6 and the standard deviation of the mean was 2.4. The mode or

most frequently cited score was 8.

There were 34 respondents who rated Pembrokeshire with the lowest score of 1; of these, 35% were

from the real estate, renting and business sector (12/34) and 18% were from hotels and restaurants

(6/34). Explanations for the low score concentrated on business rates and the seasonality of trade:

• “Diabolical, what should happen in seaside resorts is that we should pay rates for 6 months. We are in

the National Park on the development side of the business and we're suffering there too as they are

putting 60% on low cost housing.”

• “It’s just there are fewer businesses here so at the moment it is stagnant.”

• “It is very bad, business rates are too high, the council think we make a lot of money in the summer

but actually we don't as there is only 6 weeks when we're busy the other 9 months we are struggling.”

Eighty-four respondents rated Pembrokeshire with the highest score of 10; of these 84, 24% were from

the hotels and restaurants sector (20/84) and 18% were from real estate, renting and business (15/84).

When asked to explain their answer, example responses were:

• “I find that it seems more or less recession proof here, there are a lot of retirees here who are quite

comfortably off.”

• “The business is tourist driven and Pembrokeshire is a jewel in the choice of British destinations

especially the coast line.”

• “Love it here, everyone is helpful and there are a lot of markets for selling my poultry.”

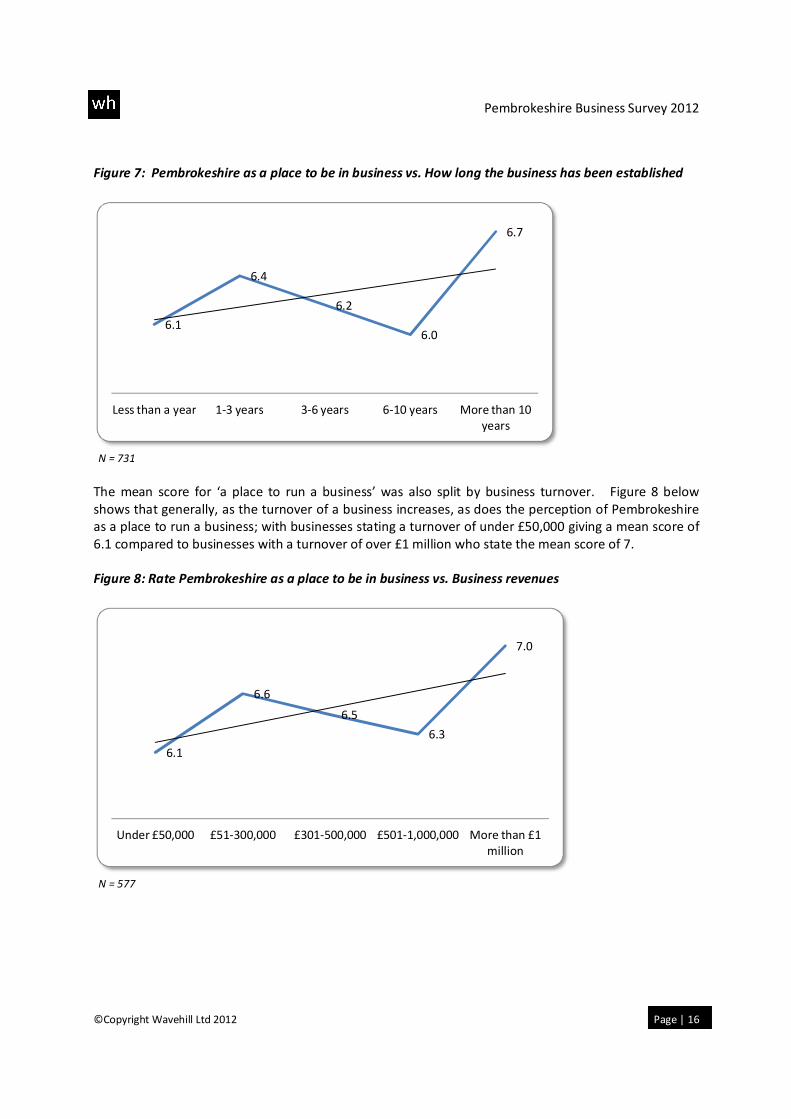

The mean score for ‘a place to run a business’ was divided by how long business had been established in

the area. Figure 7 shows that the longer the business has been established in the area, the higher the

score for Pembrokeshire as a place to run a business is recorded. With the exception of 6-10 years

group where the mean drops to 6.

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 16

Figure 7: Pembrokeshire as a place to be in business vs. How long the business has been established

N = 731

The mean score for ‘a place to run a business’ was also split by business turnover. Figure 8 below

shows that generally, as the turnover of a business increases, as does the perception of Pembrokeshire

as a place to run a business; with businesses stating a turnover of under £50,000 giving a mean score of

6.1 compared to businesses with a turnover of over £1 million who state the mean score of 7.

Figure 8: Rate Pembrokeshire as a place to be in business vs. Business revenues

N = 577

6.1

6.4

6.2

6.0

6.7

Less than a year 1-3 years 3-6 years 6-10 years More than 10

years

6.1

6.6

6.5

6.3

7.0

Under £50,000 £51-300,000 £301-500,000 £501-1,000,000 More than £1

million

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 17

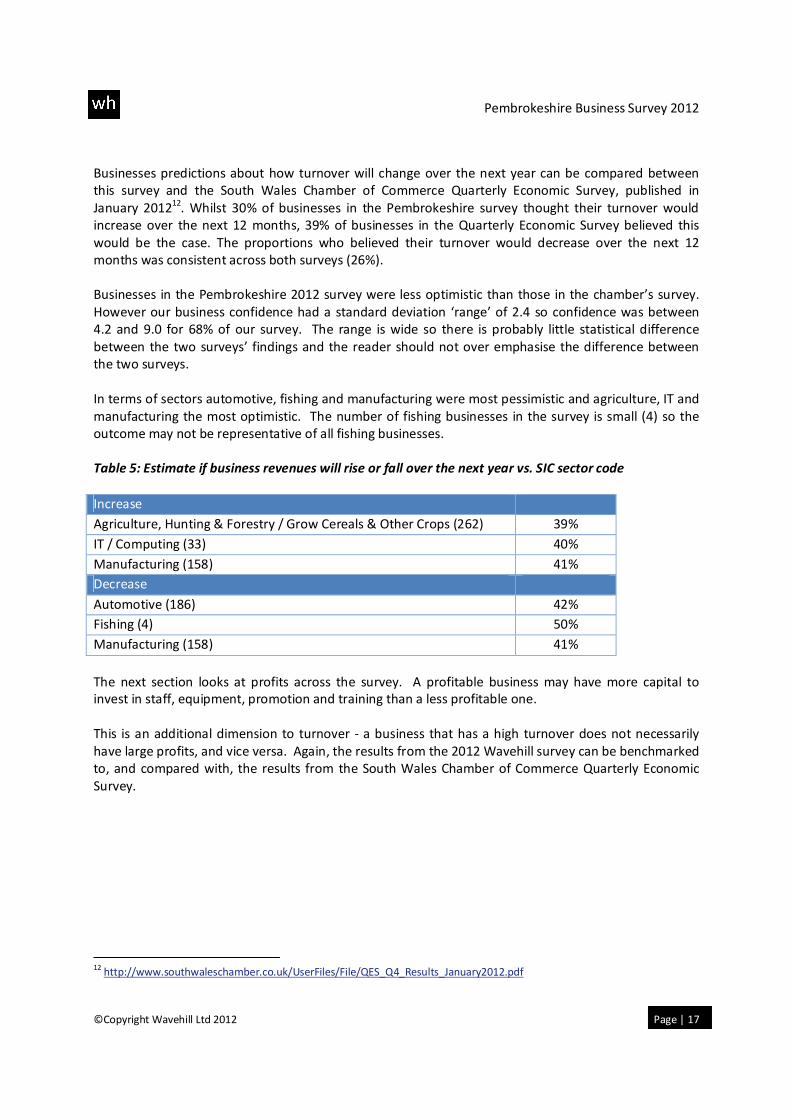

Businesses predictions about how turnover will change over the next year can be compared between

this survey and the South Wales Chamber of Commerce Quarterly Economic Survey, published in

January 201212

. Whilst 30% of businesses in the Pembrokeshire survey thought their turnover would

increase over the next 12 months, 39% of businesses in the Quarterly Economic Survey believed this

would be the case. The proportions who believed their turnover would decrease over the next 12

months was consistent across both surveys (26%).

Businesses in the Pembrokeshire 2012 survey were less optimistic than those in the chamber’s survey.

However our business confidence had a standard deviation ‘range’ of 2.4 so confidence was between

4.2 and 9.0 for 68% of our survey. The range is wide so there is probably little statistical difference

between the two surveys’ findings and the reader should not over emphasise the difference between

the two surveys.

In terms of sectors automotive, fishing and manufacturing were most pessimistic and agriculture, IT and

manufacturing the most optimistic. The number of fishing businesses in the survey is small (4) so the

outcome may not be representative of all fishing businesses.

Table 5: Estimate if business revenues will rise or fall over the next year vs. SIC sector code

Increase

Agriculture, Hunting & Forestry / Grow Cereals & Other Crops (262) 39%

IT / Computing (33) 40%

Manufacturing (158) 41%

Decrease

Automotive (186) 42%

Fishing (4) 50%

Manufacturing (158) 41%

The next section looks at profits across the survey. A profitable business may have more capital to

invest in staff, equipment, promotion and training than a less profitable one.

This is an additional dimension to turnover - a business that has a high turnover does not necessarily

have large profits, and vice versa. Again, the results from the 2012 Wavehill survey can be benchmarked

to, and compared with, the results from the South Wales Chamber of Commerce Quarterly Economic

Survey.

12

http://www.southwaleschamber.co.uk/UserFiles/File/QES_Q4_Results_January2012.pdf

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 18

Figure 9: Compare turnover estimates between Pembrokeshire Survey and South Wales Chamber of

Commerce Survey

N = Wavehill - 638

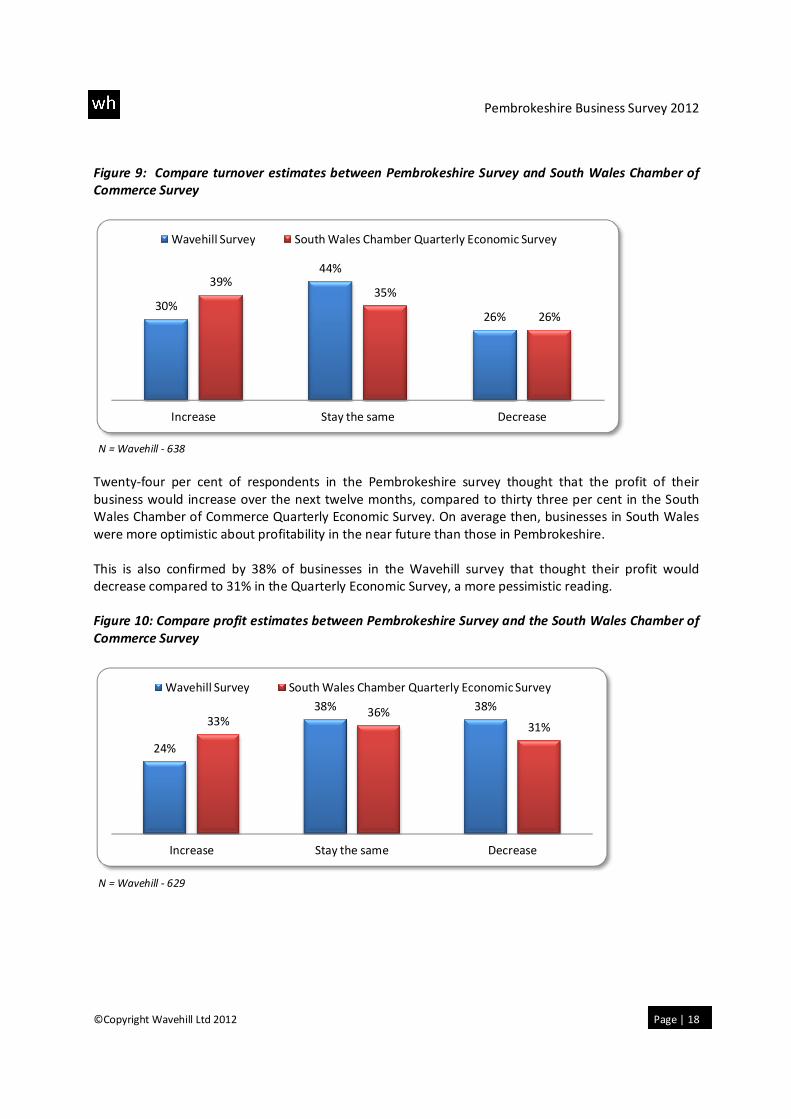

Twenty-four per cent of respondents in the Pembrokeshire survey thought that the profit of their

business would increase over the next twelve months, compared to thirty three per cent in the South

Wales Chamber of Commerce Quarterly Economic Survey. On average then, businesses in South Wales

were more optimistic about profitability in the near future than those in Pembrokeshire.

This is also confirmed by 38% of businesses in the Wavehill survey that thought their profit would

decrease compared to 31% in the Quarterly Economic Survey, a more pessimistic reading.

Figure 10: Compare profit estimates between Pembrokeshire Survey and the South Wales Chamber of

Commerce Survey

N = Wavehill - 629

30%

44%

26%

39%35%

26%

Increase Stay the same Decrease

Wavehill Survey South Wales Chamber Quarterly Economic Survey

24%

38% 38%33%

36%31%

Increase Stay the same Decrease

Wavehill Survey South Wales Chamber Quarterly Economic Survey

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 19

The table below shows that when considered by sector, the IT sector, financial services and agriculture

are the most optimistic about profits. The automotive sector is relatively pessimistic, with 75% of

respondents predicting falling profits.

Table 6: The three most optimistic and pessimistic SIC sectors regarding profit

Increase

IT / Computing (33) 40%

Financial Services / Financial Intermediation (22) 33%

Agriculture, Hunting & Forestry / Grow Cereals & Other Crops (262) 32%

Decrease

Automotive (186) 61%

Fishing (4) 75%

Manufacturing (158) 55%

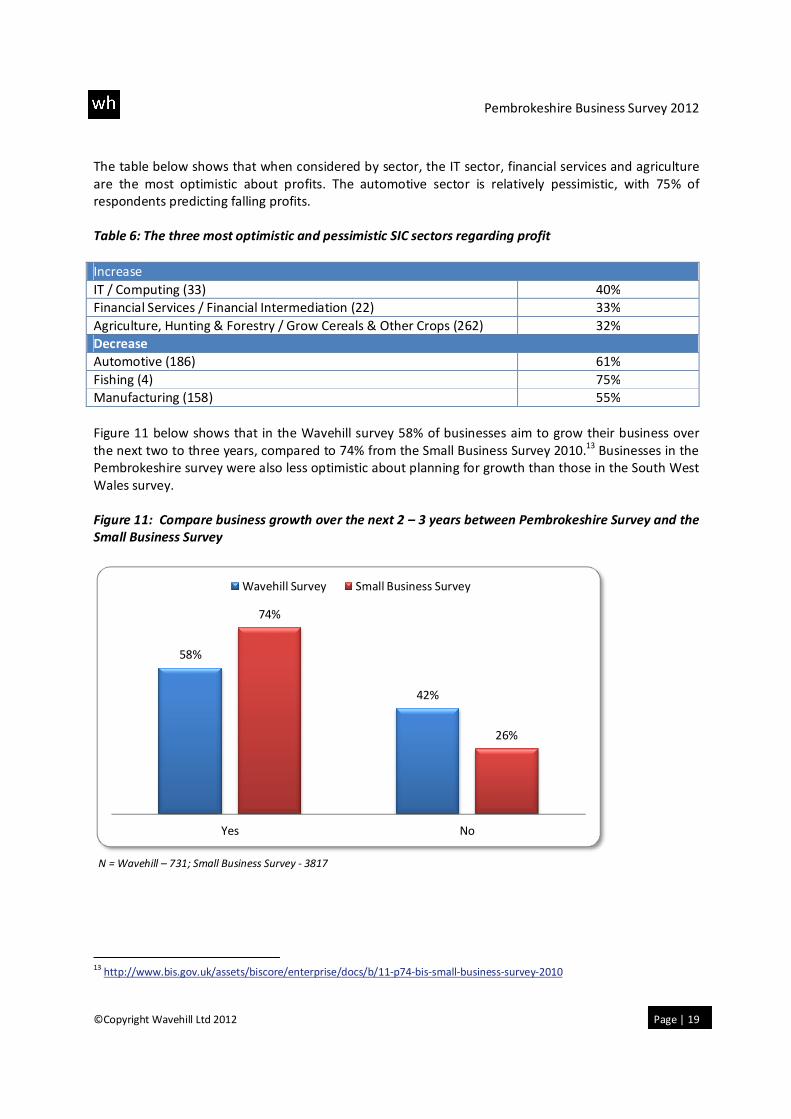

Figure 11 below shows that in the Wavehill survey 58% of businesses aim to grow their business over

the next two to three years, compared to 74% from the Small Business Survey 2010.13

Businesses in the

Pembrokeshire survey were also less optimistic about planning for growth than those in the South West

Wales survey.

Figure 11: Compare business growth over the next 2 – 3 years between Pembrokeshire Survey and the

Small Business Survey

N = Wavehill – 731; Small Business Survey - 3817

13

http://www.bis.gov.uk/assets/biscore/enterprise/docs/b/11-p74-bis-small-business-survey-2010

58%

42%

74%

26%

Yes No

Wavehill Survey Small Business Survey

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 20

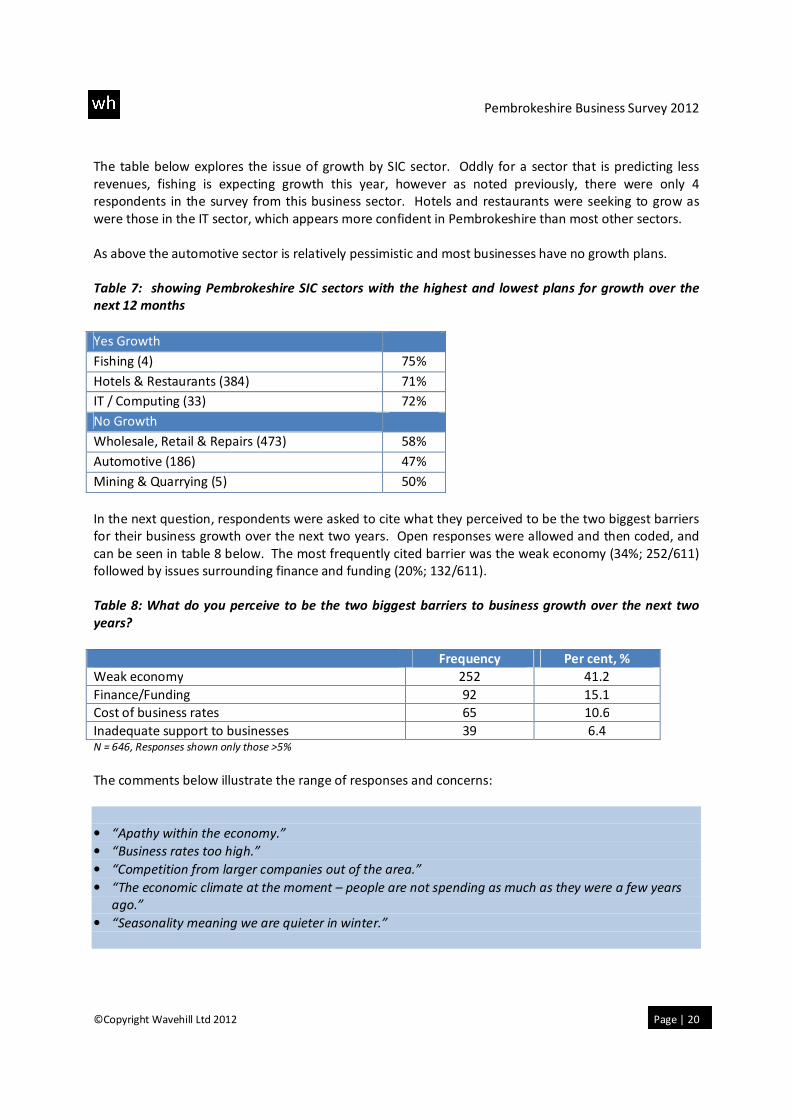

The table below explores the issue of growth by SIC sector. Oddly for a sector that is predicting less

revenues, fishing is expecting growth this year, however as noted previously, there were only 4

respondents in the survey from this business sector. Hotels and restaurants were seeking to grow as

were those in the IT sector, which appears more confident in Pembrokeshire than most other sectors.

As above the automotive sector is relatively pessimistic and most businesses have no growth plans.

Table 7: showing Pembrokeshire SIC sectors with the highest and lowest plans for growth over the

next 12 months

Yes Growth

Fishing (4) 75%

Hotels & Restaurants (384) 71%

IT / Computing (33) 72%

No Growth

Wholesale, Retail & Repairs (473) 58%

Automotive (186) 47%

Mining & Quarrying (5) 50%

In the next question, respondents were asked to cite what they perceived to be the two biggest barriers

for their business growth over the next two years. Open responses were allowed and then coded, and

can be seen in table 8 below. The most frequently cited barrier was the weak economy (34%; 252/611)

followed by issues surrounding finance and funding (20%; 132/611).

Table 8: What do you perceive to be the two biggest barriers to business growth over the next two

years?

Frequency Per cent, %

Weak economy 252 41.2

Finance/Funding 92 15.1

Cost of business rates 65 10.6

Inadequate support to businesses 39 6.4 N = 646, Responses shown only those >5%

The comments below illustrate the range of responses and concerns:

• “Apathy within the economy.”

• “Business rates too high.”

• “Competition from larger companies out of the area.”

• “The economic climate at the moment – people are not spending as much as they were a few years

ago.”

• “Seasonality meaning we are quieter in winter.”

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 21

There were 605 respondents who gave a valid answer when asked whether they thought general

economic conditions in Pembrokeshire would improve, stay the same or get worse over the next 12

months. In the Pembrokeshire 2012 survey, 15% thought the general economic condition would

improve (92/605), 43% thought it would stay the same (258/605) and 42% thought it would get worse

(255/605).

When we validate this with the CBI Economic Challenges Facing UK Businesses Survey 2011 we can see

that 16% of businesses thought the general economic condition of the country would increase

(160/1002), 25% thought that conditions would stay the same (251/1002) and 57% thought the general

economic conditions would get worse (571/1002).

The Pembrokeshire survey appears more optimistic than the CBI UK Business survey.

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 22

6. Business Support Business support is part of Government policy in England and Wales. In Wales the Directorate for

Business, Economy, Technology and Science (BETS) is responsible for the business support strategy. The

premise is that SMEs have the potential to grow rapidly, gain technological advantage, and create

wealth and jobs. However SMEs do not necessarily have the access or capacity to high quality training

which can reduce their competitiveness and sustainability. Business support services help to foster SME

growth.

Businesses were asked what relevant business support was available to them in Pembrokeshire.

Open responses were coded and these are summarised in table 9, below. The results show that nearly

half (47%) of businesses feel there isn’t any support available to them in Pembrokeshire (200/428).

Seventeen per cent of respondents stated that Pembrokeshire Business Initiative was available to them

as support (74/428), 14% of businesses said Pembrokeshire County Council (59/428) offered support

and 7% that Pembrokeshire Tourism (30/428) offered support.

Table 9: Which organisations offer business support relevant to your business?

Frequency Percent, %

There isn't any support 200 47

Pembrokeshire Business Initiative 74 17

Pembrokeshire County Council 59 14

Pembrokeshire Tourism 30 7 N = 428, Responses shown only those >5%

When asked how or where they would find business advice, respondents placed an emphasis on using

the internet as a search aid. Twenty-seven per cent of respondents (124/450) stated they would look on

the internet if they wanted to access business support in Pembrokeshire, a further 26% said they would

look to Pembrokeshire Business Initiative (119/450) and another 26% said they would ask

Pembrokeshire County Council (116/450). Seven per cent of businesses said they would contact the

Welsh Government to access business support in Pembrokeshire (29/450).

As table 10 shows, the Pembrokeshire Business Initiative was the most frequently referenced

organisation that businesses contacted for support, followed by Pembrokeshire County Council and the

Welsh Government.

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 23

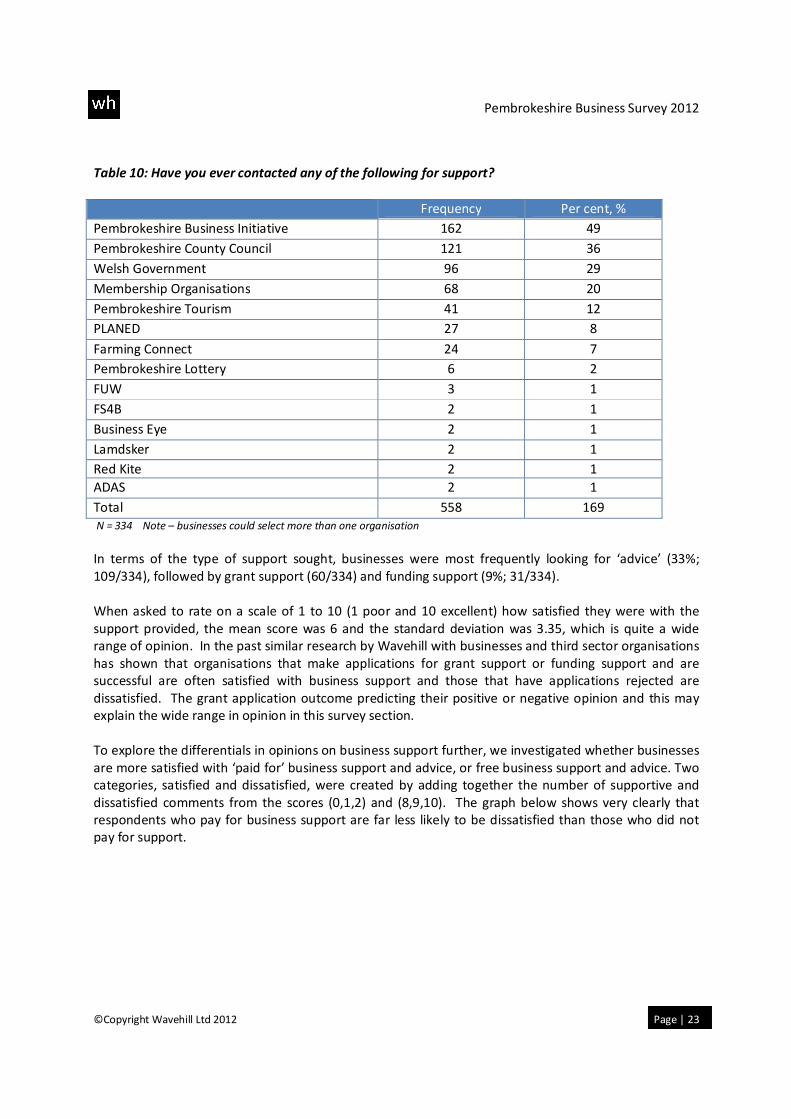

Table 10: Have you ever contacted any of the following for support?

Frequency Per cent, %

Pembrokeshire Business Initiative 162 49

Pembrokeshire County Council 121 36

Welsh Government 96 29

Membership Organisations 68 20

Pembrokeshire Tourism 41 12

PLANED 27 8

Farming Connect 24 7

Pembrokeshire Lottery 6 2

FUW 3 1

FS4B 2 1

Business Eye 2 1

Lamdsker 2 1

Red Kite 2 1

ADAS 2 1

Total 558 169

N = 334 Note – businesses could select more than one organisation

In terms of the type of support sought, businesses were most frequently looking for ‘advice’ (33%;

109/334), followed by grant support (60/334) and funding support (9%; 31/334).

When asked to rate on a scale of 1 to 10 (1 poor and 10 excellent) how satisfied they were with the

support provided, the mean score was 6 and the standard deviation was 3.35, which is quite a wide

range of opinion. In the past similar research by Wavehill with businesses and third sector organisations

has shown that organisations that make applications for grant support or funding support and are

successful are often satisfied with business support and those that have applications rejected are

dissatisfied. The grant application outcome predicting their positive or negative opinion and this may

explain the wide range in opinion in this survey section.

To explore the differentials in opinions on business support further, we investigated whether businesses

are more satisfied with ‘paid for’ business support and advice, or free business support and advice. Two

categories, satisfied and dissatisfied, were created by adding together the number of supportive and

dissatisfied comments from the scores (0,1,2) and (8,9,10). The graph below shows very clearly that

respondents who pay for business support are far less likely to be dissatisfied than those who did not

pay for support.

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 24

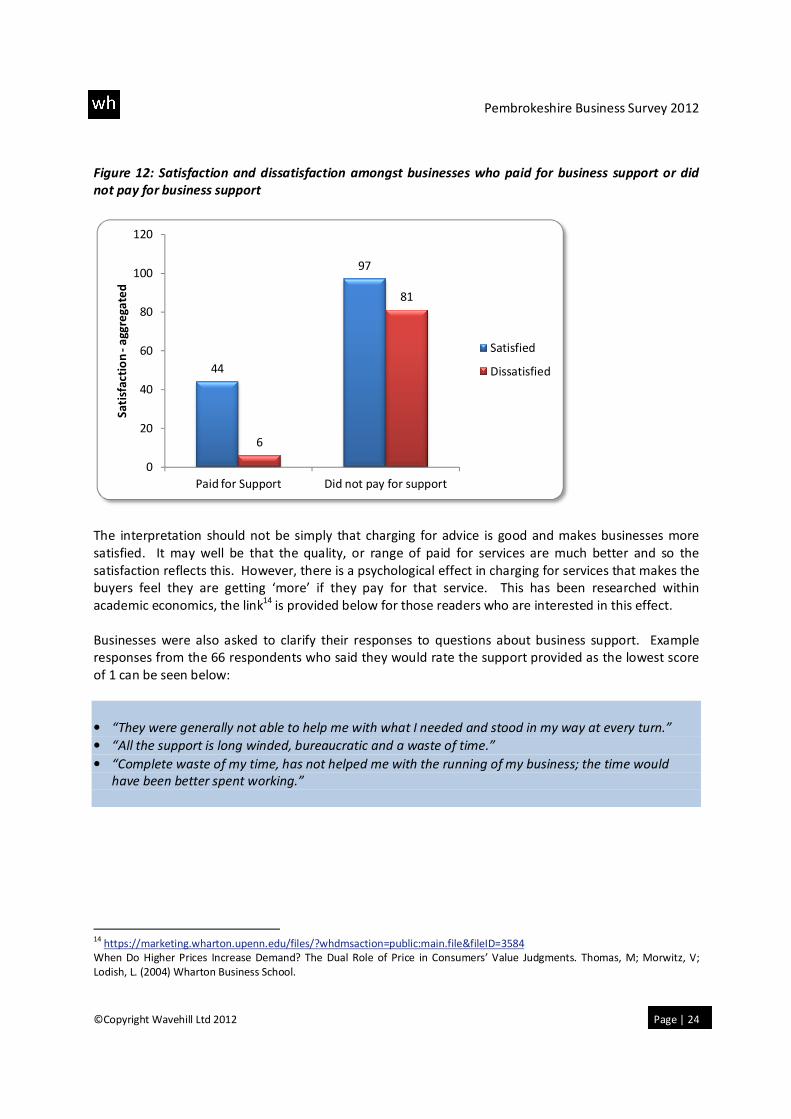

Figure 12: Satisfaction and dissatisfaction amongst businesses who paid for business support or did

not pay for business support

The interpretation should not be simply that charging for advice is good and makes businesses more

satisfied. It may well be that the quality, or range of paid for services are much better and so the

satisfaction reflects this. However, there is a psychological effect in charging for services that makes the

buyers feel they are getting ‘more’ if they pay for that service. This has been researched within

academic economics, the link14

is provided below for those readers who are interested in this effect.

Businesses were also asked to clarify their responses to questions about business support. Example

responses from the 66 respondents who said they would rate the support provided as the lowest score

of 1 can be seen below:

• “They were generally not able to help me with what I needed and stood in my way at every turn.”

• “All the support is long winded, bureaucratic and a waste of time.”

• “Complete waste of my time, has not helped me with the running of my business; the time would

have been better spent working.”

14

https://marketing.wharton.upenn.edu/files/?whdmsaction=public:main.file&fileID=3584

When Do Higher Prices Increase Demand? The Dual Role of Price in Consumers’ Value Judgments. Thomas, M; Morwitz, V;

Lodish, L. (2004) Wharton Business School.

44

97

6

81

0

20

40

60

80

100

120

Paid for Support Did not pay for support

Sa

tisf

acti

on

-a

gg

reg

ate

d

Satisfied

Dissatisfied

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 25

Conversely example responses from the 59 respondents who said they would rate the support as the

highest score of 10 can be seen below:

• “They are both very efficient and did what they said they would.”

• “We got really good advice and information on sourcing other companies, finding good suppliers,

having open days and events.”

• “Support was good and local advice was tailored to us.”

Businesses were asked to describe the most important type of support that the public sector currently

provides to small and medium sized businesses. Grants, tax reductions and funding were the most

frequently noted assistance, accounting for 59% of responses. Only 12% of business responses

identified business advice as the most important form of support. The proportion focusing on grant

support was very high and may reflect the availability of grants in the Wales objective one convergence

region. It may be suggestive of an emergent business culture that expects business grants over business

advice.

• Reduced business rates 36%

• Business grants 13%

• Business advice 12%

• Business funding 10%

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 26

7. Business Premises The requirement for larger business premises can indicate that a business is growing, investing capital

and possibly expanding its workforce requirement. Businesses that need larger premises could be

targeted with business support.

Seven per cent of respondents stated they would need a larger business premises in the future (49/731).

When this group was asked what type of premises they required, 41% said an industrial unit (20/49),

39% a shop (19/49), 22% an office (11/49) and 26% stated other (16/49) Other responses included

agricultural land, workshops and larger garages.

When split by sector we can see that of the 49 respondents who stated they would need larger premises

in the future, 24% came from the sector of wholesale, retail and repairs (11/49), 21% came from hotels

and restaurants and 21% came from construction (10/49).

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 27

8. Information Technology The use of information technology, accessing cloud services and being able to have local broadband

networks to connect to the internet is important for many businesses if they wish to remain

competitive.

Seventy-five per cent of respondents (546/731) use broadband in the course of their normal business;

this is much higher than was identified in the 2006 Wavehill Pembrokeshire Business Survey, where only

30% of businesses surveyed stated that they used broadband as part of their business. Of the 75% of

the respondents in this survey who use broadband in the course of their normal business, 68% believe

that the service they currently receive is adequate for their business (373/546), but 32% do not

(173/546). Splitting this by sector it is possible to see that 29% of businesses from the hotel and

restaurant sector (50/172) do not feel that the broadband service is good enough for their business.

This may be because they often share the broadband connection internally across many rooms or

several WiFi points, requiring much higher bandwidth allocations and connection speeds than a business

where internet access is primarily used by employees. Those respondents who stated the service is not

good enough for their business explain that the service is too slow 70%; (149/213), unreliable or

intermittent 20%; (41/213). Other responses (7) included that the cost was too expensive, and a limited

choice when choosing internet providers.

Although 48% of respondents stated that they have no further broadband requirements at the moment

(265/546); 50% state they would like a faster speed (274/546), 8% said improved reliability (43/546), 7%

said competitive prices (37/546) and 5% said better coverage (25/546). BETS has stated that ‘… all

businesses in Wales will have access to Next Generation Broadband by 2015, with the ambition that 50%

or more have access to 100Mbps.’ (BETS, 2011).

Ninety-four per cent of respondents stated that they did not access WiFi using public networks, for

example in libraries and internet cafés. Those 6% who do access WiFi using public networks were asked

why they did so, some example responses can be seen below:

• “I'm out of the office quite a lot, pick up emails.”

• “This is done whilst visiting customers.”

• “Usually when we're out and about meeting clients, it means we can take the office with us.”

When asked whether they had a website for their business, 52% of respondents said yes (376/731). It is

interesting to compare this figure to the Wavehill Pembrokeshire Business Survey from 2006 where only

28% of businesses had a website.

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 28

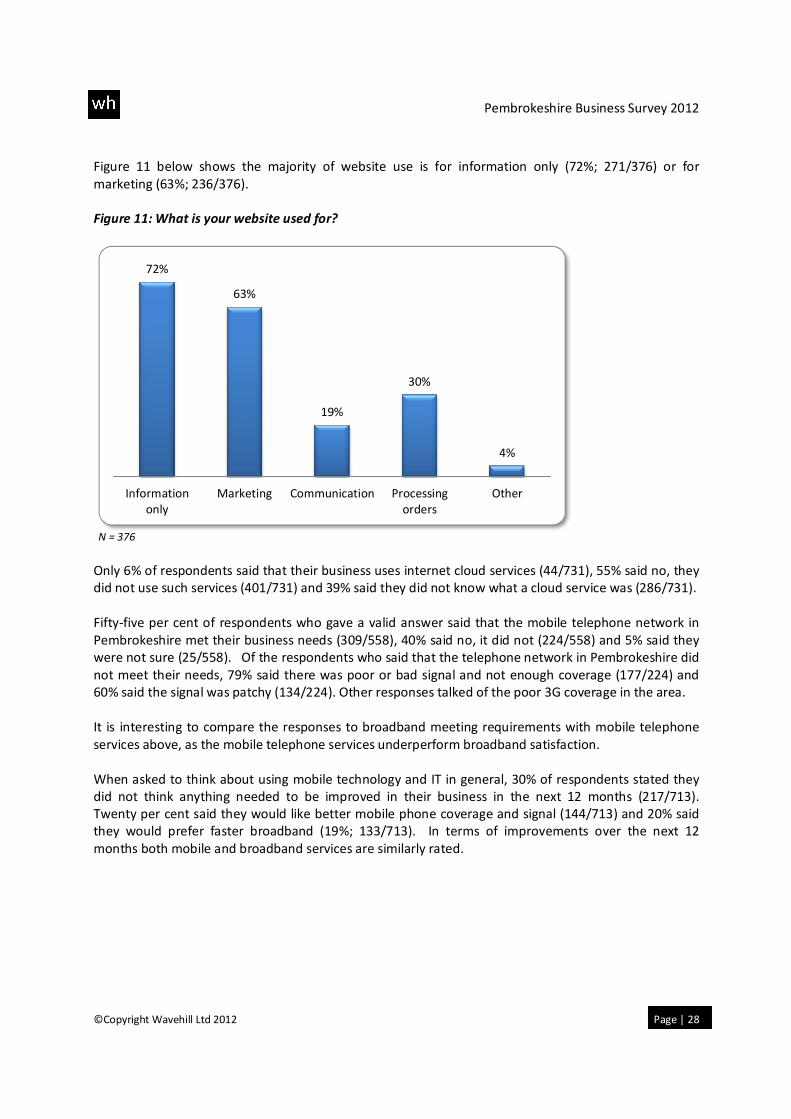

Figure 11 below shows the majority of website use is for information only (72%; 271/376) or for

marketing (63%; 236/376).

Figure 11: What is your website used for?

N = 376

Only 6% of respondents said that their business uses internet cloud services (44/731), 55% said no, they

did not use such services (401/731) and 39% said they did not know what a cloud service was (286/731).

Fifty-five per cent of respondents who gave a valid answer said that the mobile telephone network in

Pembrokeshire met their business needs (309/558), 40% said no, it did not (224/558) and 5% said they

were not sure (25/558). Of the respondents who said that the telephone network in Pembrokeshire did

not meet their needs, 79% said there was poor or bad signal and not enough coverage (177/224) and

60% said the signal was patchy (134/224). Other responses talked of the poor 3G coverage in the area.

It is interesting to compare the responses to broadband meeting requirements with mobile telephone

services above, as the mobile telephone services underperform broadband satisfaction.

When asked to think about using mobile technology and IT in general, 30% of respondents stated they

did not think anything needed to be improved in their business in the next 12 months (217/713).

Twenty per cent said they would like better mobile phone coverage and signal (144/713) and 20% said

they would prefer faster broadband (19%; 133/713). In terms of improvements over the next 12

months both mobile and broadband services are similarly rated.

72%

63%

19%

30%

4%

Information

only

Marketing Communication Processing

orders

Other

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 29

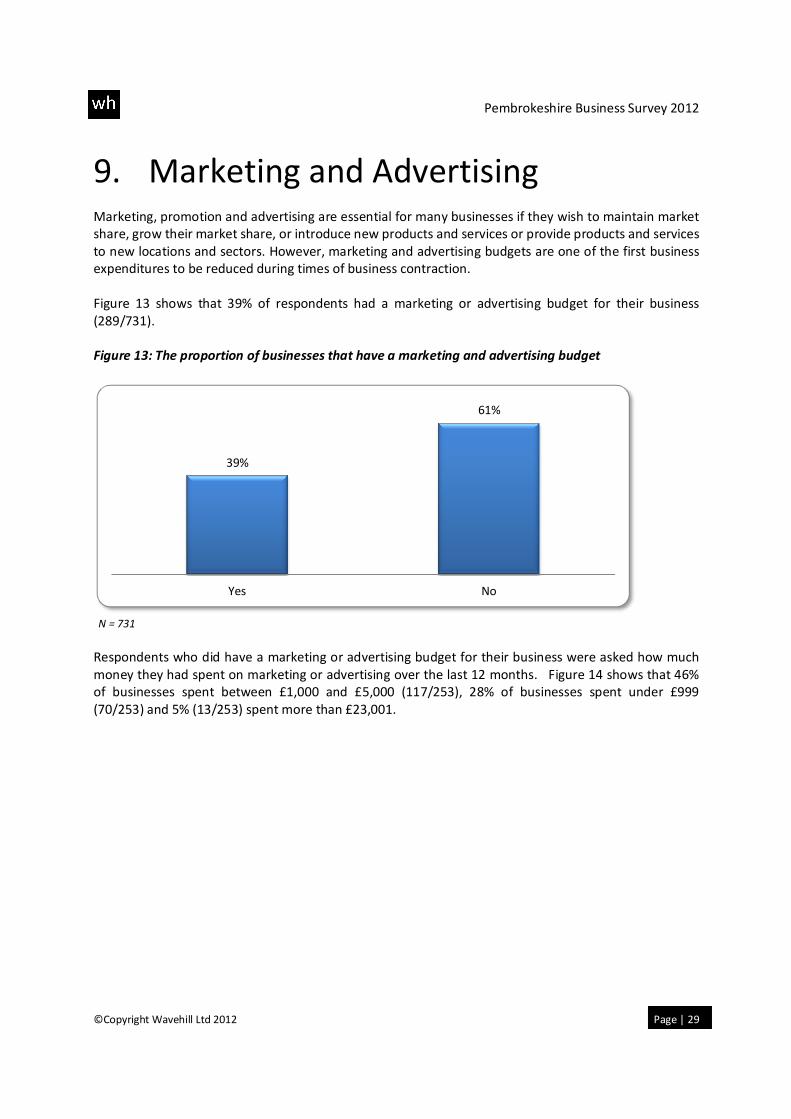

9. Marketing and Advertising Marketing, promotion and advertising are essential for many businesses if they wish to maintain market

share, grow their market share, or introduce new products and services or provide products and services

to new locations and sectors. However, marketing and advertising budgets are one of the first business

expenditures to be reduced during times of business contraction.

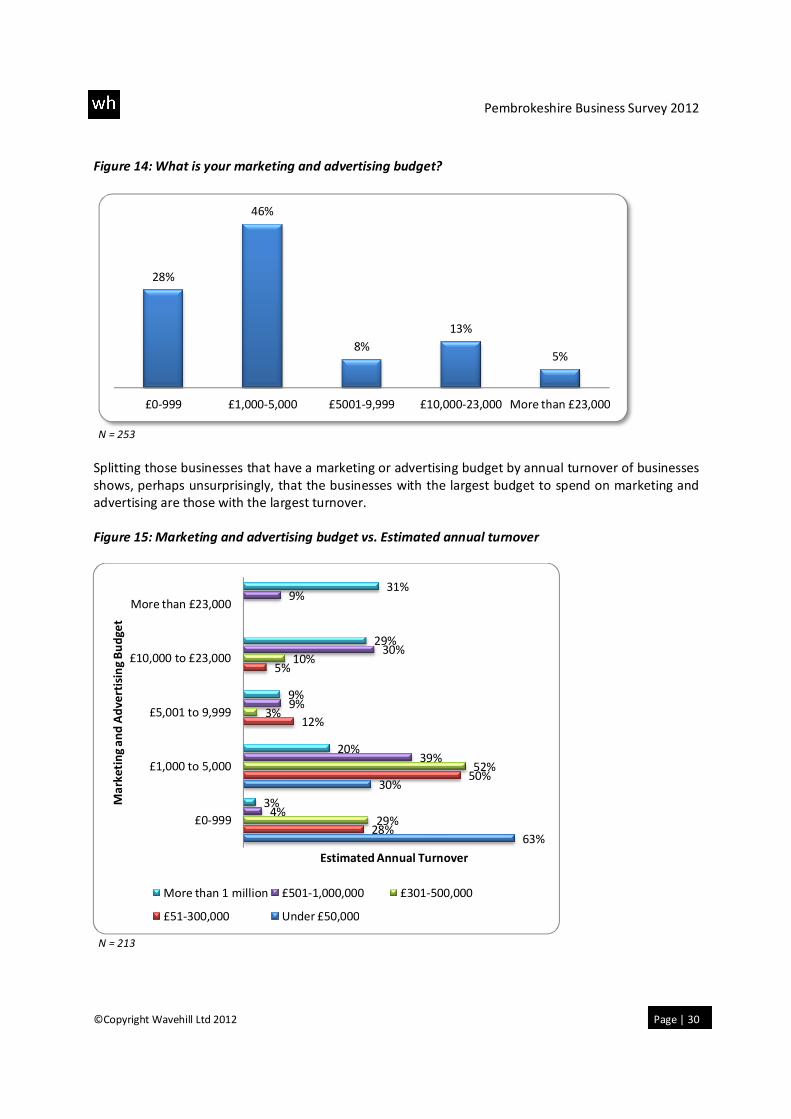

Figure 13 shows that 39% of respondents had a marketing or advertising budget for their business

(289/731).

Figure 13: The proportion of businesses that have a marketing and advertising budget

N = 731

Respondents who did have a marketing or advertising budget for their business were asked how much

money they had spent on marketing or advertising over the last 12 months. Figure 14 shows that 46%

of businesses spent between £1,000 and £5,000 (117/253), 28% of businesses spent under £999

(70/253) and 5% (13/253) spent more than £23,001.

39%

61%

Yes No

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 30

Figure 14: What is your marketing and advertising budget?

N = 253

Splitting those businesses that have a marketing or advertising budget by annual turnover of businesses

shows, perhaps unsurprisingly, that the businesses with the largest budget to spend on marketing and

advertising are those with the largest turnover.

Figure 15: Marketing and advertising budget vs. Estimated annual turnover

N = 213

28%

46%

8%

13%

5%

£0-999 £1,000-5,000 £5001-9,999 £10,000-23,000 More than £23,000

63%

30%

28%

50%

12%

5%

29%

52%

3%

10%

4%

39%

9%

30%

9%

3%

20%

9%

29%

31%

£0-999

£1,000 to 5,000

£5,001 to 9,999

£10,000 to £23,000

More than £23,000

Estimated Annual Turnover

Ma

rke

tin

g a

nd

Ad

ve

rtis

ing

Bu

dg

et

More than 1 million £501-1,000,000 £301-500,000

£51-300,000 Under £50,000

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 31

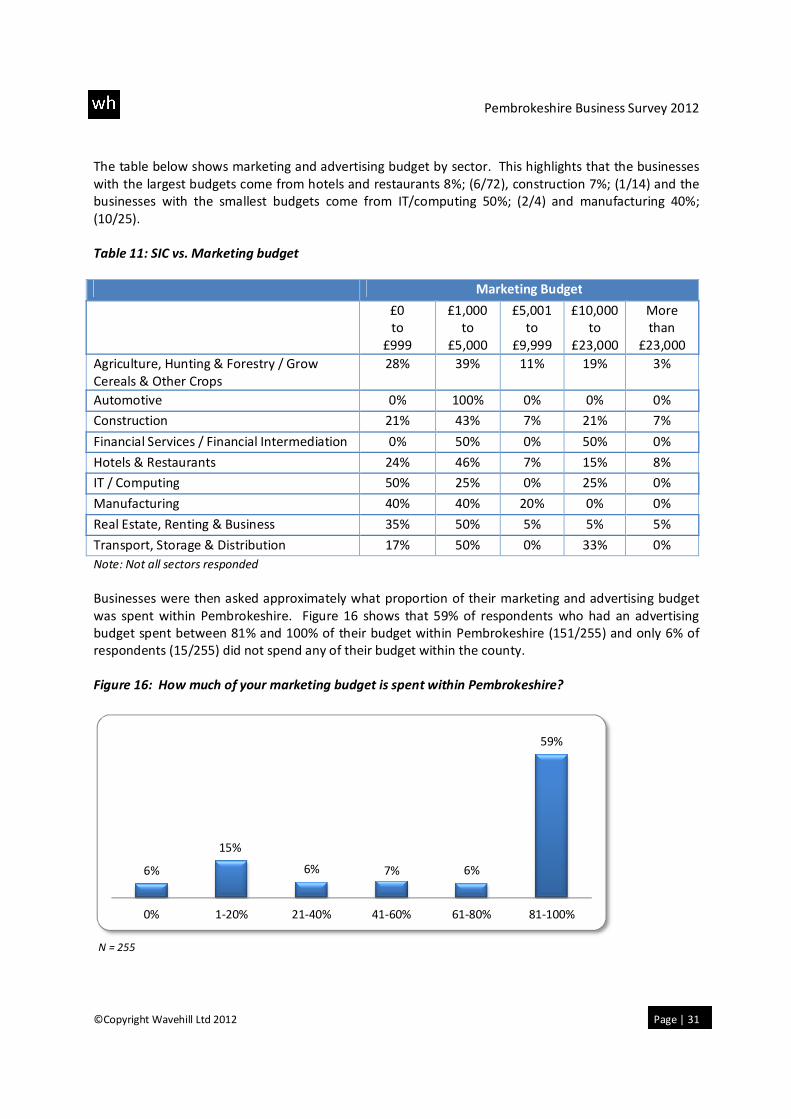

The table below shows marketing and advertising budget by sector. This highlights that the businesses

with the largest budgets come from hotels and restaurants 8%; (6/72), construction 7%; (1/14) and the

businesses with the smallest budgets come from IT/computing 50%; (2/4) and manufacturing 40%;

(10/25).

Table 11: SIC vs. Marketing budget

Marketing Budget

£0

to

£999

£1,000

to

£5,000

£5,001

to

£9,999

£10,000

to

£23,000

More

than

£23,000

Agriculture, Hunting & Forestry / Grow

Cereals & Other Crops

28% 39% 11% 19% 3%

Automotive 0% 100% 0% 0% 0%

Construction 21% 43% 7% 21% 7%

Financial Services / Financial Intermediation 0% 50% 0% 50% 0%

Hotels & Restaurants 24% 46% 7% 15% 8%

IT / Computing 50% 25% 0% 25% 0%

Manufacturing 40% 40% 20% 0% 0%

Real Estate, Renting & Business 35% 50% 5% 5% 5%

Transport, Storage & Distribution 17% 50% 0% 33% 0%

Note: Not all sectors responded

Businesses were then asked approximately what proportion of their marketing and advertising budget

was spent within Pembrokeshire. Figure 16 shows that 59% of respondents who had an advertising

budget spent between 81% and 100% of their budget within Pembrokeshire (151/255) and only 6% of

respondents (15/255) did not spend any of their budget within the county.

Figure 16: How much of your marketing budget is spent within Pembrokeshire?

N = 255

6%

15%

6% 7% 6%

59%

0% 1-20% 21-40% 41-60% 61-80% 81-100%

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 32

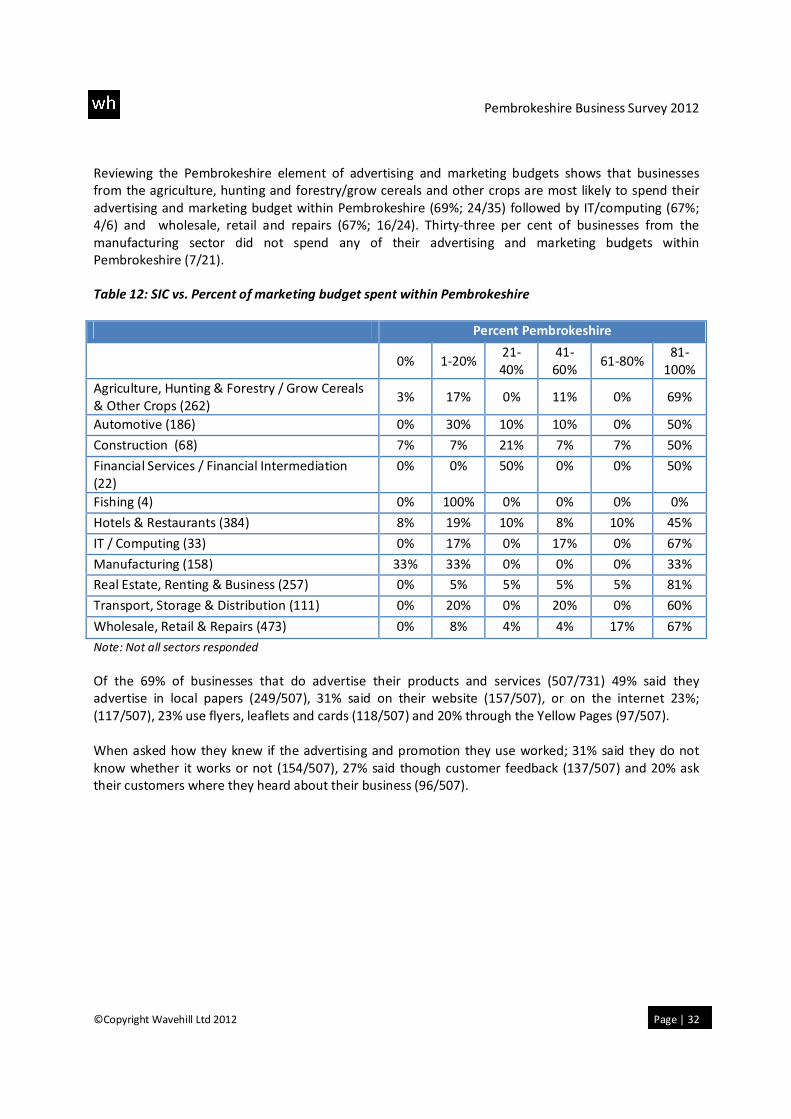

Reviewing the Pembrokeshire element of advertising and marketing budgets shows that businesses

from the agriculture, hunting and forestry/grow cereals and other crops are most likely to spend their

advertising and marketing budget within Pembrokeshire (69%; 24/35) followed by IT/computing (67%;

4/6) and wholesale, retail and repairs (67%; 16/24). Thirty-three per cent of businesses from the

manufacturing sector did not spend any of their advertising and marketing budgets within

Pembrokeshire (7/21).

Table 12: SIC vs. Percent of marketing budget spent within Pembrokeshire

Percent Pembrokeshire

0% 1-20%

21-

40%

41-

60% 61-80%

81-

100%

Agriculture, Hunting & Forestry / Grow Cereals

& Other Crops (262) 3% 17% 0% 11% 0% 69%

Automotive (186) 0% 30% 10% 10% 0% 50%

Construction (68) 7% 7% 21% 7% 7% 50%

Financial Services / Financial Intermediation

(22)

0% 0% 50% 0% 0% 50%

Fishing (4) 0% 100% 0% 0% 0% 0%

Hotels & Restaurants (384) 8% 19% 10% 8% 10% 45%

IT / Computing (33) 0% 17% 0% 17% 0% 67%

Manufacturing (158) 33% 33% 0% 0% 0% 33%

Real Estate, Renting & Business (257) 0% 5% 5% 5% 5% 81%

Transport, Storage & Distribution (111) 0% 20% 0% 20% 0% 60%

Wholesale, Retail & Repairs (473) 0% 8% 4% 4% 17% 67%

Note: Not all sectors responded

Of the 69% of businesses that do advertise their products and services (507/731) 49% said they

advertise in local papers (249/507), 31% said on their website (157/507), or on the internet 23%;

(117/507), 23% use flyers, leaflets and cards (118/507) and 20% through the Yellow Pages (97/507).

When asked how they knew if the advertising and promotion they use worked; 31% said they do not

know whether it works or not (154/507), 27% said though customer feedback (137/507) and 20% ask

their customers where they heard about their business (96/507).

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 33

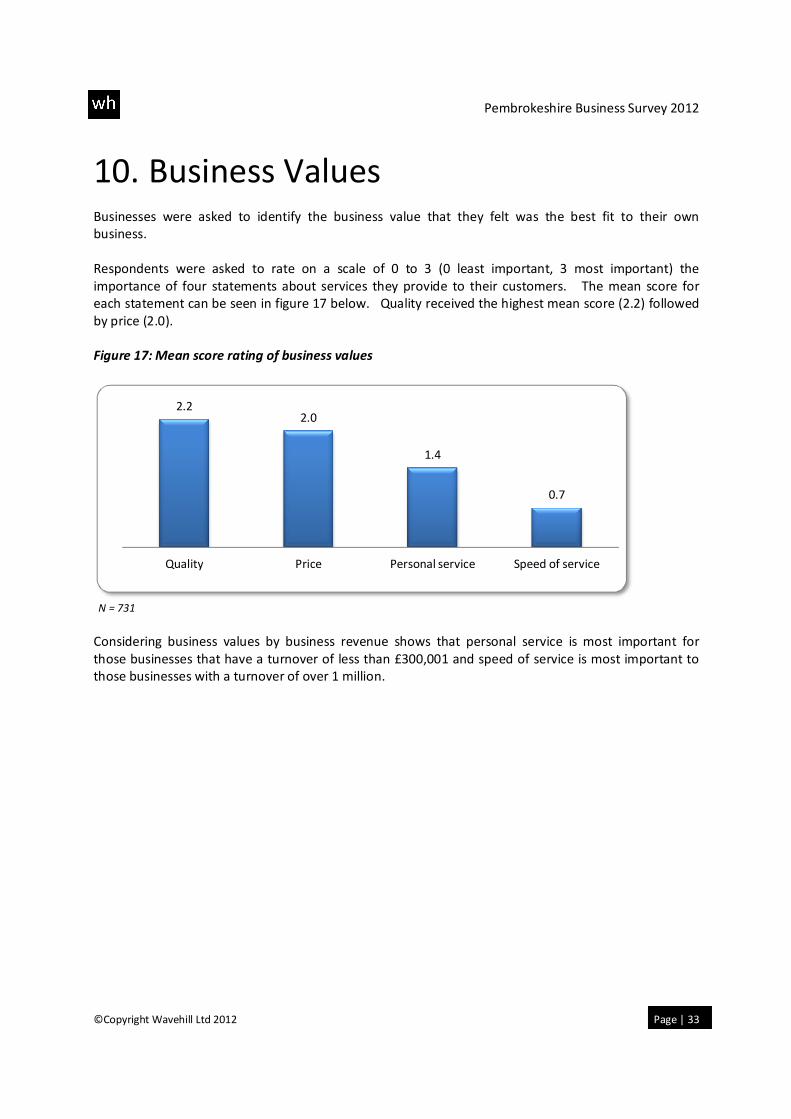

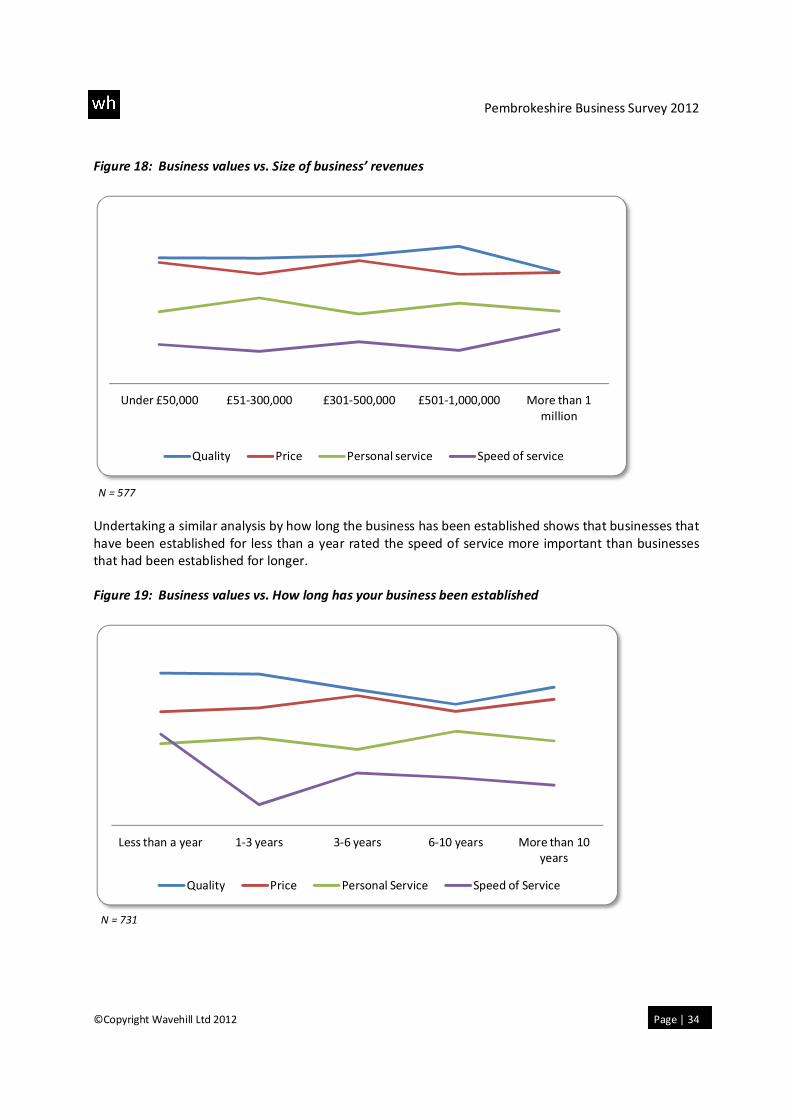

10. Business Values Businesses were asked to identify the business value that they felt was the best fit to their own

business.

Respondents were asked to rate on a scale of 0 to 3 (0 least important, 3 most important) the

importance of four statements about services they provide to their customers. The mean score for

each statement can be seen in figure 17 below. Quality received the highest mean score (2.2) followed

by price (2.0).

Figure 17: Mean score rating of business values

N = 731

Considering business values by business revenue shows that personal service is most important for

those businesses that have a turnover of less than £300,001 and speed of service is most important to

those businesses with a turnover of over 1 million.

2.22.0

1.4

0.7

Quality Price Personal service Speed of service

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 34

Figure 18: Business values vs. Size of business’ revenues

N = 577

Undertaking a similar analysis by how long the business has been established shows that businesses that

have been established for less than a year rated the speed of service more important than businesses

that had been established for longer.

Figure 19: Business values vs. How long has your business been established

N = 731

Under £50,000 £51-300,000 £301-500,000 £501-1,000,000 More than 1

million

Quality Price Personal service Speed of service

Less than a year 1-3 years 3-6 years 6-10 years More than 10

years

Quality Price Personal Service Speed of Service

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 35

11. Workforce The workforce in a business is perhaps its most crucial element. Businesses need a flexible and skilled

labour force to produce goods and services efficiently and to meet the labour demands of businesses in

a timely way. A stronger economy tends to increase demand for workers and unemployment falls, a

weak economy tends to reverse this effect.

Table 13 below shows that the mean number of full time, permanent employees is 5.1, and 2.0 part

time employees.

Table 13: Number of employees

Overall total Mean

Full-time permanent employees 3735 5.12

Part-time employees 1490 2.04

Seasonal employees 849 1.16

Casual demand workers 284 0.39

When asked whether the number of employees has changed over the last 12 months, 76% say they

employ the same number of staff (555/726), 8% say they employ more staff (61/726) and 15% say they

employ less staff now than they did 12 months ago (111/555). This finding fits with the general trading

(economic) conditions at the moment as approximately half as many businesses have increased their

workforce (8%) than have reduced it (15%).

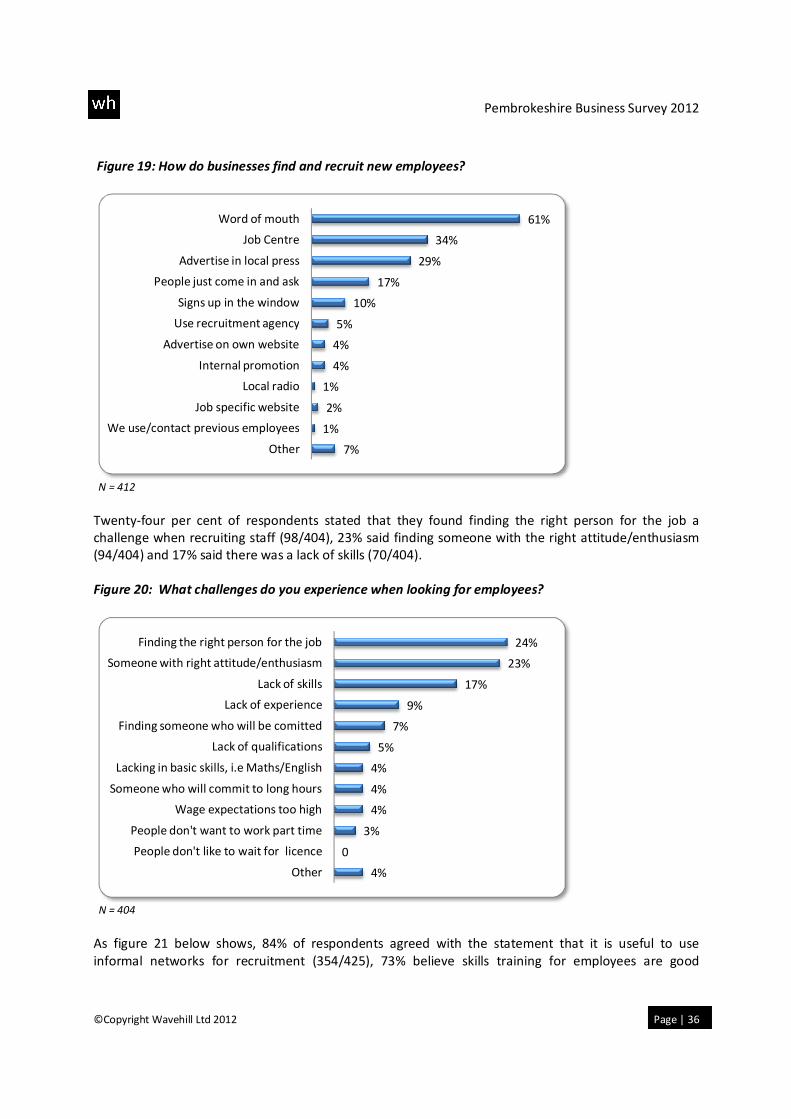

Respondents were asked what methods they usually use when recruiting staff. Of the respondents who

gave a valid answer, 61% said they recruit through word of mouth (250/412), 34% through the Job

Centre (139/412) and 29% advertise in the local press (120/412). The importance of word-of-mouth

employment echoes findings from investigations of social capital. The Office for National Statistics has

investigated the link between social capital and employment.

Labour market participation: the influence of social capital by Keith Brook, Labour Market Division,

Office for National Statistics (2005).

Social capital and the labour market ONS has adopted a definition of social capital given by Cote and

Healy (2001) from the Organisation for Economic Cooperation and Development. They describe social

capital as ‘networks together with shared norms, values and understandings that facilitate cooperation

within or among groups’. Three forms of social capital have been proposed, namely bonding, bridging

and linking. Bonding refers to the interaction between similar types of people such as family members

and close personal friends. Bridging includes looser ties with casual friends, colleagues or associates and,

while weaker and more diverse than bonding relationships, is more important in ‘getting ahead’. Linking

describes connections with organisations and institutions and assists in accruing support from people in

authority, for example, from the UK welfare state system. Active membership of social, educational,

political, religious and voluntary organisations, both within and outside the workplace, may also

contribute to an individual’s social capital. Participation in such groups may help an individual to develop

skills or strengthen and extend networks which may assist in acquiring a job.

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 36

Figure 19: How do businesses find and recruit new employees?

N = 412

Twenty-four per cent of respondents stated that they found finding the right person for the job a

challenge when recruiting staff (98/404), 23% said finding someone with the right attitude/enthusiasm

(94/404) and 17% said there was a lack of skills (70/404).

Figure 20: What challenges do you experience when looking for employees?

N = 404

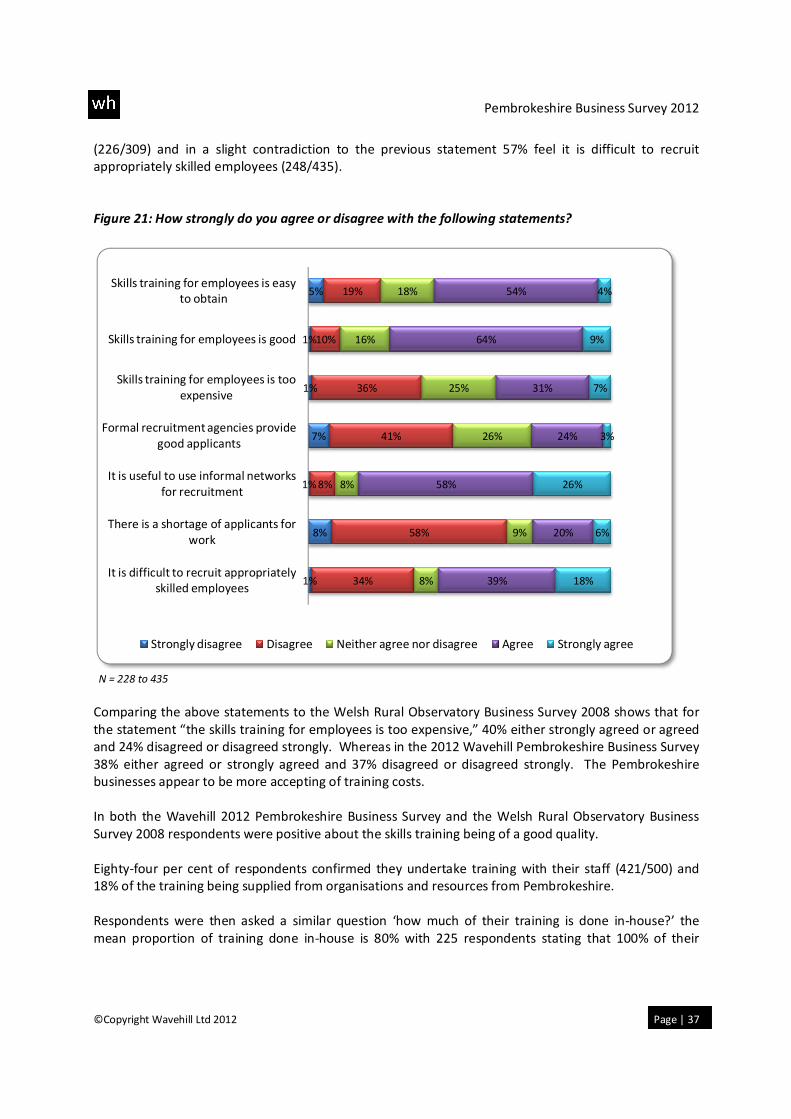

As figure 21 below shows, 84% of respondents agreed with the statement that it is useful to use

informal networks for recruitment (354/425), 73% believe skills training for employees are good

7%

1%

2%

1%

4%

4%

5%

10%

17%

29%

34%

61%

Other

We use/contact previous employees

Job specific website

Local radio

Internal promotion

Advertise on own website

Use recruitment agency

Signs up in the window

People just come in and ask

Advertise in local press

Job Centre

Word of mouth

4%

0

3%

4%

4%

4%

5%

7%

9%

17%

23%

24%

Other

People don't like to wait for licence

People don't want to work part time

Wage expectations too high

Someone who will commit to long hours

Lacking in basic skills, i.e Maths/English

Lack of qualifications

Finding someone who will be comitted

Lack of experience

Lack of skills

Someone with right attitude/enthusiasm

Finding the right person for the job

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 37

(226/309) and in a slight contradiction to the previous statement 57% feel it is difficult to recruit

appropriately skilled employees (248/435).

Figure 21: How strongly do you agree or disagree with the following statements?

N = 228 to 435

Comparing the above statements to the Welsh Rural Observatory Business Survey 2008 shows that for

the statement “the skills training for employees is too expensive,” 40% either strongly agreed or agreed

and 24% disagreed or disagreed strongly. Whereas in the 2012 Wavehill Pembrokeshire Business Survey

38% either agreed or strongly agreed and 37% disagreed or disagreed strongly. The Pembrokeshire

businesses appear to be more accepting of training costs.

In both the Wavehill 2012 Pembrokeshire Business Survey and the Welsh Rural Observatory Business

Survey 2008 respondents were positive about the skills training being of a good quality.

Eighty-four per cent of respondents confirmed they undertake training with their staff (421/500) and

18% of the training being supplied from organisations and resources from Pembrokeshire.

Respondents were then asked a similar question ‘how much of their training is done in-house?’ the

mean proportion of training done in-house is 80% with 225 respondents stating that 100% of their

1%

8%

1%

7%

1%

1%

5%

34%

58%

8%

41%

36%

10%

19%

8%

9%

8%

26%

25%

16%

18%

39%

20%

58%

24%

31%

64%

54%

18%

6%

26%

3%

7%

9%

4%

It is difficult to recruit appropriately

skilled employees

There is a shortage of applicants for

work

It is useful to use informal networks

for recruitment

Formal recruitment agencies provide

good applicants

Skills training for employees is too

expensive

Skills training for employees is good

Skills training for employees is easy

to obtain

Strongly disagree Disagree Neither agree nor disagree Agree Strongly agree

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 38

needs were met in-house. A mean proportion of 5% was the amount of training delivered through

distance learning and a mean of 93% was delivered face to face.

Three per cent of respondents (19/731) had an International Organisation for Standardisation (ISO)

certificate which is about half the rate (6%) that the BSI estimates across businesses in the UK. When

divided by business turnover 58% of businesses with an estimated annual turnover of £1million

compared to none with a turnover of under £50,000 had an ISO certificate in the Pembrokeshire survey.

The investment in ISO accreditation may be too much for smaller businesses, but necessary for larger

ones.

In a study to examine the effects of ISO 9001 on employee outcomes such as employment, earnings, and

health and safety, David I. Levine of the University of California at Berkeley and Michael W. Toffel of the

Harvard Business School analyzed a matched sample of nearly 1,000 companies in California. ISO

adopters realized higher rates of growth of sales, employment, payroll, and average annual earnings.

Injury rates also declined slightly at ISO 9001 adopters, although total injury costs did not.

Source: Quality Management and Job Quality: How the ISO9001 Standard for Quality management Systems Affects Employees

and Employers

When viewed by sector, the highest per cent of businesses with ISO’s came from hotels and restaurants

53%; (10/19) and wholesale, retail and repairs 21%; (4/19). Wholesale, retail and repair sector may have

to use an ISO as part of their supply chain requirements, leading to these results.

Two per cent of respondents (16/731) had Investors in People (IIP). Businesses with the larger turnover

were most likely to have Investors in People status; for example no businesses with an estimated annual

turnover of under £50,000 had an IIP, compared to 13% of business with a turnover of over 1 million.

Splitting this by sector we can see that those sectors which have the greatest percentage of businesses

with an IPP are transport, storage and distribution 5%; (1/20), agriculture, hunting and forestry/grow

cereals and other crops (4%; 4/89) and hotels and restaurants 4%; (6/144), although all are relatively

low.

Five per cent of respondents have other training systems and awards such as Federation of Small

Businesses, MCS, CHAS and International Safety Management.

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 39

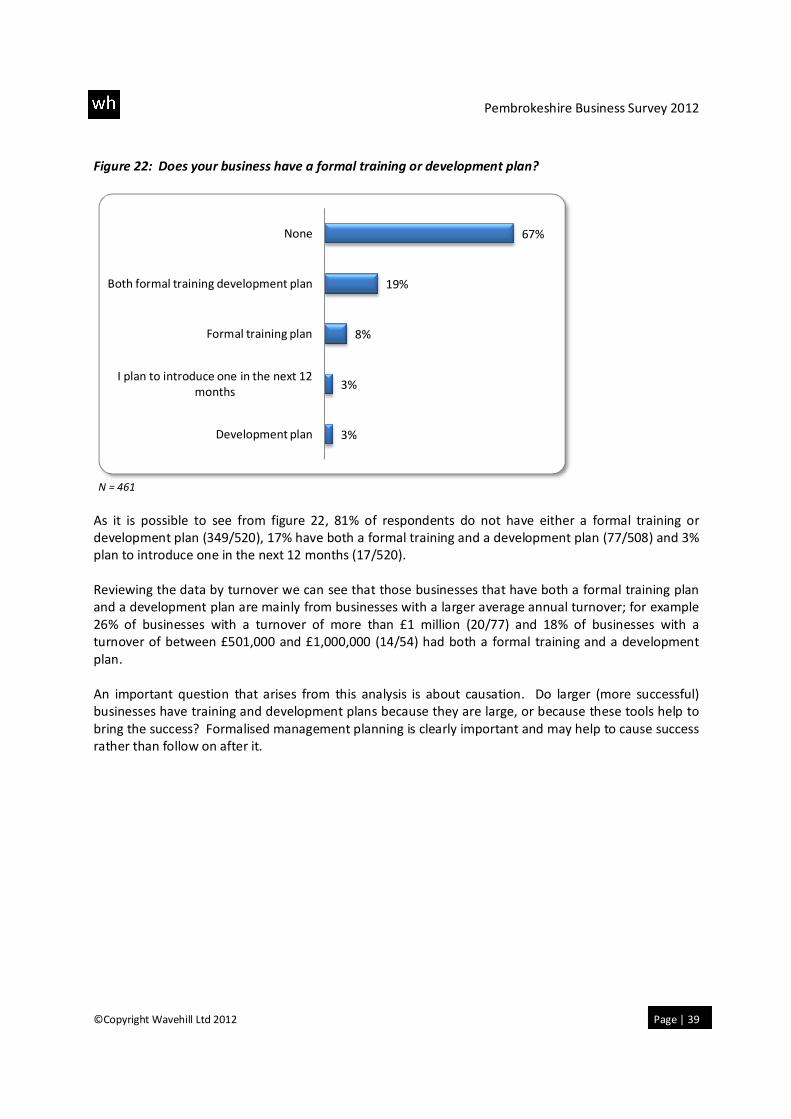

Figure 22: Does your business have a formal training or development plan?

N = 461

As it is possible to see from figure 22, 81% of respondents do not have either a formal training or

development plan (349/520), 17% have both a formal training and a development plan (77/508) and 3%

plan to introduce one in the next 12 months (17/520).

Reviewing the data by turnover we can see that those businesses that have both a formal training plan

and a development plan are mainly from businesses with a larger average annual turnover; for example

26% of businesses with a turnover of more than £1 million (20/77) and 18% of businesses with a

turnover of between £501,000 and £1,000,000 (14/54) had both a formal training and a development

plan.

An important question that arises from this analysis is about causation. Do larger (more successful)

businesses have training and development plans because they are large, or because these tools help to

bring the success? Formalised management planning is clearly important and may help to cause success

rather than follow on after it.

3%

3%

8%

19%

67%

Development plan

I plan to introduce one in the next 12

months

Formal training plan

Both formal training development plan

None

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 40

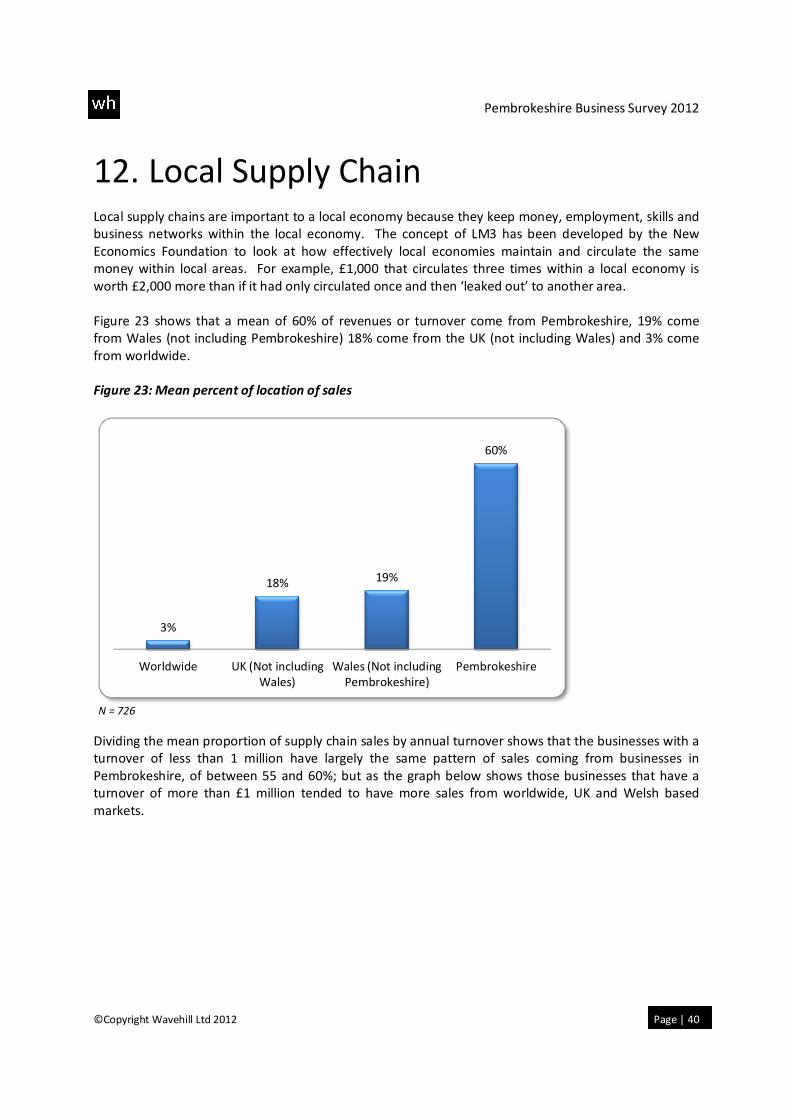

12. Local Supply Chain Local supply chains are important to a local economy because they keep money, employment, skills and

business networks within the local economy. The concept of LM3 has been developed by the New

Economics Foundation to look at how effectively local economies maintain and circulate the same

money within local areas. For example, £1,000 that circulates three times within a local economy is

worth £2,000 more than if it had only circulated once and then ‘leaked out’ to another area.

Figure 23 shows that a mean of 60% of revenues or turnover come from Pembrokeshire, 19% come

from Wales (not including Pembrokeshire) 18% come from the UK (not including Wales) and 3% come

from worldwide.

Figure 23: Mean percent of location of sales

N = 726

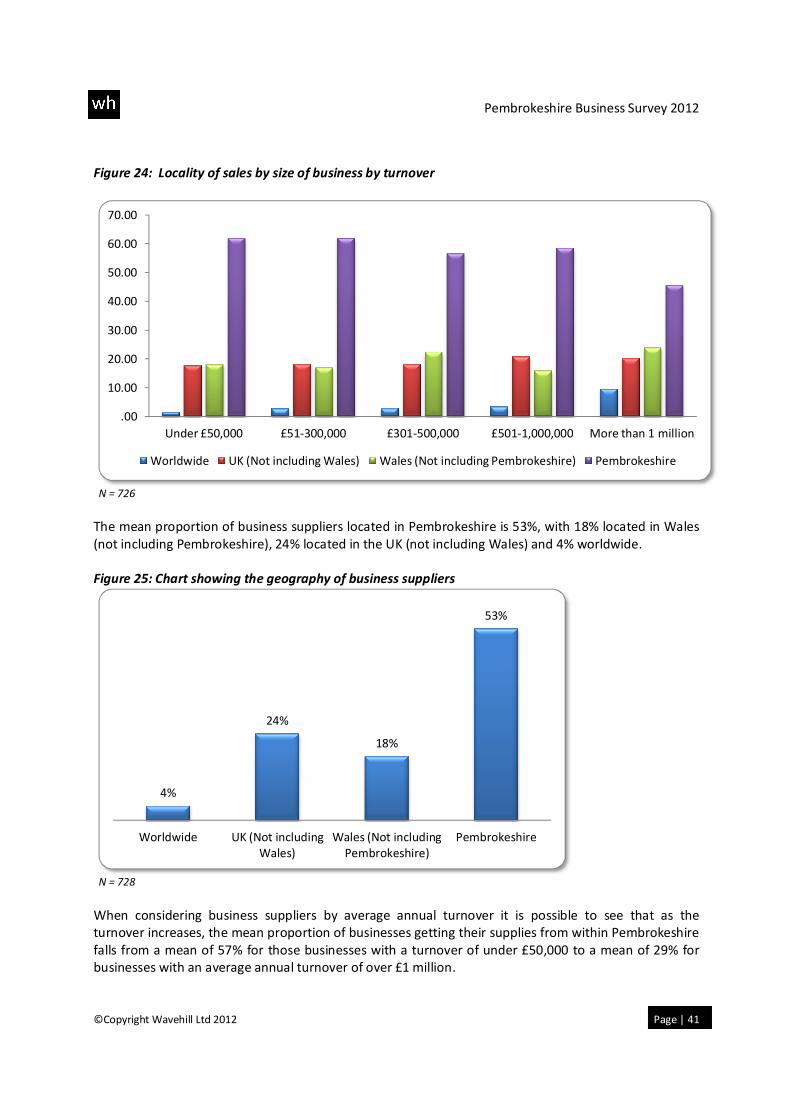

Dividing the mean proportion of supply chain sales by annual turnover shows that the businesses with a

turnover of less than 1 million have largely the same pattern of sales coming from businesses in

Pembrokeshire, of between 55 and 60%; but as the graph below shows those businesses that have a

turnover of more than £1 million tended to have more sales from worldwide, UK and Welsh based

markets.

3%

18% 19%

60%

Worldwide UK (Not including

Wales)

Wales (Not including

Pembrokeshire)

Pembrokeshire

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 41

Figure 24: Locality of sales by size of business by turnover

N = 726

The mean proportion of business suppliers located in Pembrokeshire is 53%, with 18% located in Wales

(not including Pembrokeshire), 24% located in the UK (not including Wales) and 4% worldwide.

Figure 25: Chart showing the geography of business suppliers

N = 728

When considering business suppliers by average annual turnover it is possible to see that as the

turnover increases, the mean proportion of businesses getting their supplies from within Pembrokeshire

falls from a mean of 57% for those businesses with a turnover of under £50,000 to a mean of 29% for

businesses with an average annual turnover of over £1 million.

.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

Under £50,000 £51-300,000 £301-500,000 £501-1,000,000 More than 1 million

Worldwide UK (Not including Wales) Wales (Not including Pembrokeshire) Pembrokeshire

4%

24%

18%

53%

Worldwide UK (Not including

Wales)

Wales (Not including

Pembrokeshire)

Pembrokeshire

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 42

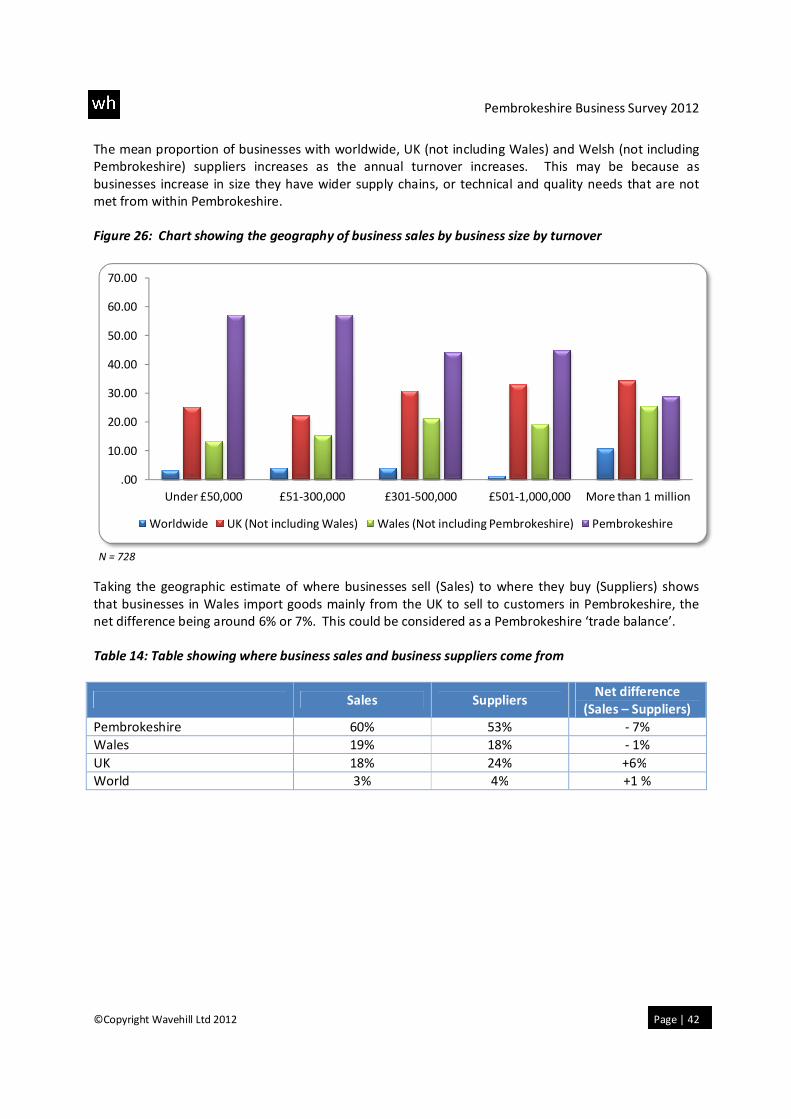

The mean proportion of businesses with worldwide, UK (not including Wales) and Welsh (not including

Pembrokeshire) suppliers increases as the annual turnover increases. This may be because as

businesses increase in size they have wider supply chains, or technical and quality needs that are not

met from within Pembrokeshire.

Figure 26: Chart showing the geography of business sales by business size by turnover

N = 728

Taking the geographic estimate of where businesses sell (Sales) to where they buy (Suppliers) shows

that businesses in Wales import goods mainly from the UK to sell to customers in Pembrokeshire, the

net difference being around 6% or 7%. This could be considered as a Pembrokeshire ‘trade balance’.

Table 14: Table showing where business sales and business suppliers come from

Sales Suppliers Net difference

(Sales – Suppliers)

Pembrokeshire 60% 53% - 7%

Wales 19% 18% - 1%

UK 18% 24% +6%

World 3% 4% +1 %

.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

Under £50,000 £51-300,000 £301-500,000 £501-1,000,000 More than 1 million

Worldwide UK (Not including Wales) Wales (Not including Pembrokeshire) Pembrokeshire

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 43

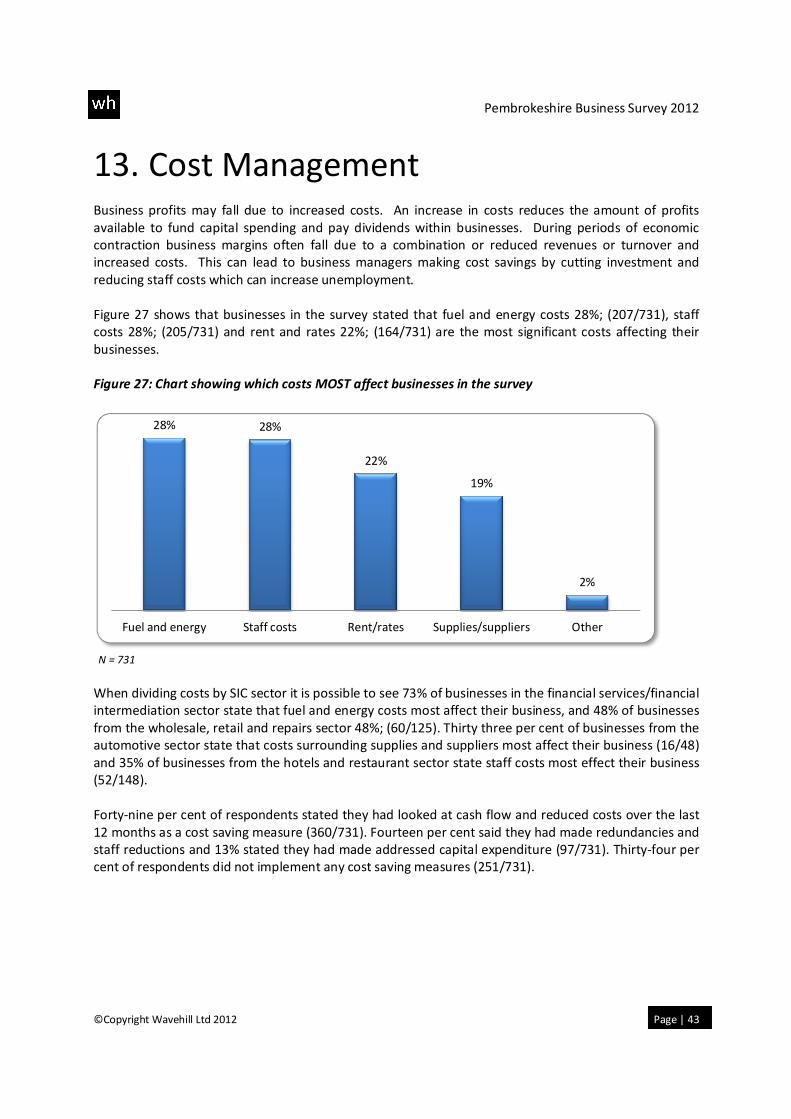

13. Cost Management Business profits may fall due to increased costs. An increase in costs reduces the amount of profits

available to fund capital spending and pay dividends within businesses. During periods of economic

contraction business margins often fall due to a combination or reduced revenues or turnover and

increased costs. This can lead to business managers making cost savings by cutting investment and

reducing staff costs which can increase unemployment.

Figure 27 shows that businesses in the survey stated that fuel and energy costs 28%; (207/731), staff

costs 28%; (205/731) and rent and rates 22%; (164/731) are the most significant costs affecting their

businesses.

Figure 27: Chart showing which costs MOST affect businesses in the survey

N = 731

When dividing costs by SIC sector it is possible to see 73% of businesses in the financial services/financial

intermediation sector state that fuel and energy costs most affect their business, and 48% of businesses

from the wholesale, retail and repairs sector 48%; (60/125). Thirty three per cent of businesses from the

automotive sector state that costs surrounding supplies and suppliers most affect their business (16/48)

and 35% of businesses from the hotels and restaurant sector state staff costs most effect their business

(52/148).

Forty-nine per cent of respondents stated they had looked at cash flow and reduced costs over the last

12 months as a cost saving measure (360/731). Fourteen per cent said they had made redundancies and

staff reductions and 13% stated they had made addressed capital expenditure (97/731). Thirty-four per

cent of respondents did not implement any cost saving measures (251/731).

28% 28%

22%

19%

2%

Fuel and energy Staff costs Rent/rates Supplies/suppliers Other

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 44

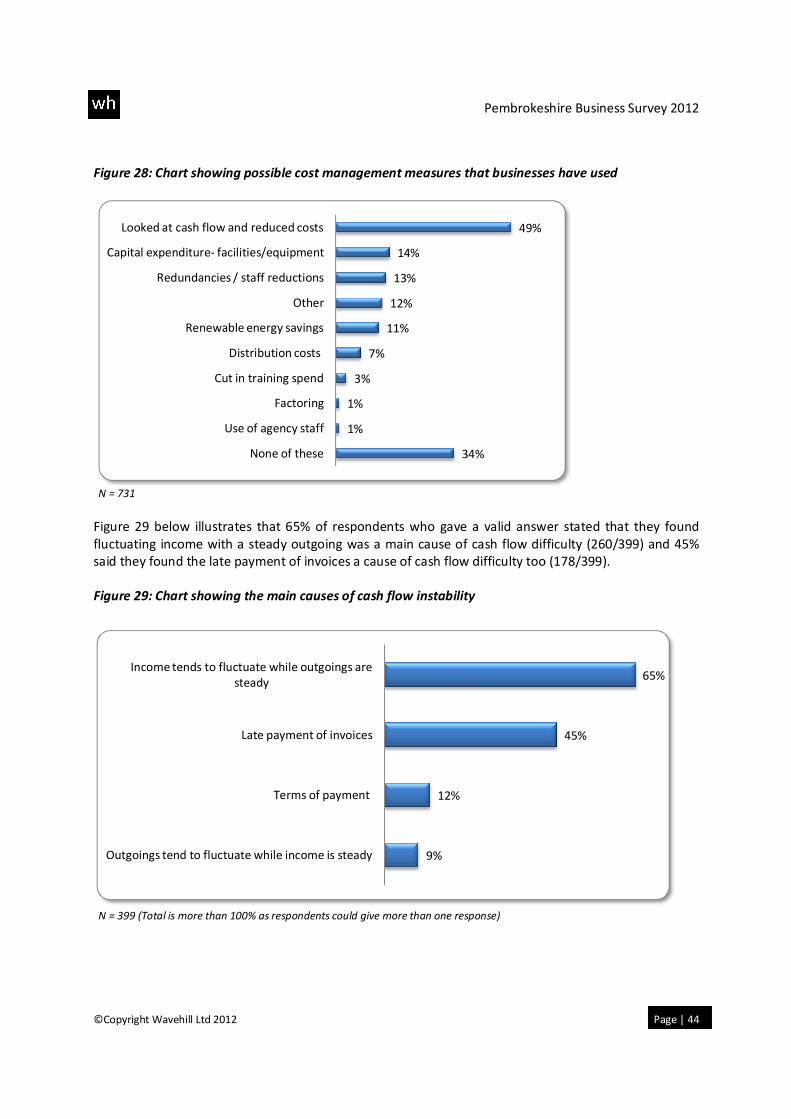

Figure 28: Chart showing possible cost management measures that businesses have used

N = 731

Figure 29 below illustrates that 65% of respondents who gave a valid answer stated that they found

fluctuating income with a steady outgoing was a main cause of cash flow difficulty (260/399) and 45%

said they found the late payment of invoices a cause of cash flow difficulty too (178/399).

Figure 29: Chart showing the main causes of cash flow instability

N = 399 (Total is more than 100% as respondents could give more than one response)

34%

1%

1%

3%

7%

11%

12%

13%

14%

49%

None of these

Use of agency staff

Factoring

Cut in training spend

Distribution costs

Renewable energy savings

Other

Redundancies / staff reductions

Capital expenditure- facilities/equipment

Looked at cash flow and reduced costs

9%

12%

45%

65%

Outgoings tend to fluctuate while income is steady

Terms of payment

Late payment of invoices

Income tends to fluctuate while outgoings are

steady

Pembrokeshire Business Survey 2012

©Copyright Wavehill Ltd 2012 Page | 45

Dividing cash flow difficulties by income it is possible to see that smaller businesses, i.e. those with an

average annual turnover of under £50,000, are more likely to state ‘income tends to fluctuate while

outgoings are steady’ as a reason for cash flow difficulty. This compares to the larger businesses, i.e.

those businesses with an average annual turnover of more than £501,000 who are more likely to cite

terms of payment and late payment of invoices as key influences on cash flow.

Terms of payment is stated as a difficulty of cash flow from 21% of automotive businesses (7/33) and

13% from businesses from the wholesale, retail and repairs sector (14/112). Late payment of invoices is

cited as a problem by 44% of businesses in construction (21/48), 58% of businesses in the transport,

storage and distribution sector (8/15).

Dividing the ‘income tends to fluctuate while outgoings are steady’ comments by how long the business

has been established shows that the longer the business has been in existence, the less likely they are to